By Sherry Bunting, Farmshine, October 28, 2022 (updated with additional information after publication)

The National Milk Producers Federation (NMPF) Board gets high marks for passing a Federal Milk Marketing Order Modernization Plan this week at its annual meeting in Denver, Colorado that includes returning the Class I mover to the previous ‘higher of’ formula — a virtually unanimous consensus item that came out of the Farm Bureau Forum in Kansas City earlier in the month.

However, the NMPF modernization plan also includes a few items that were not fully discussed, items that seem to run counter to what dairy farmers were prioritizing, and it leaves out a few items the consensus-builders were vocal about in Kansas City.

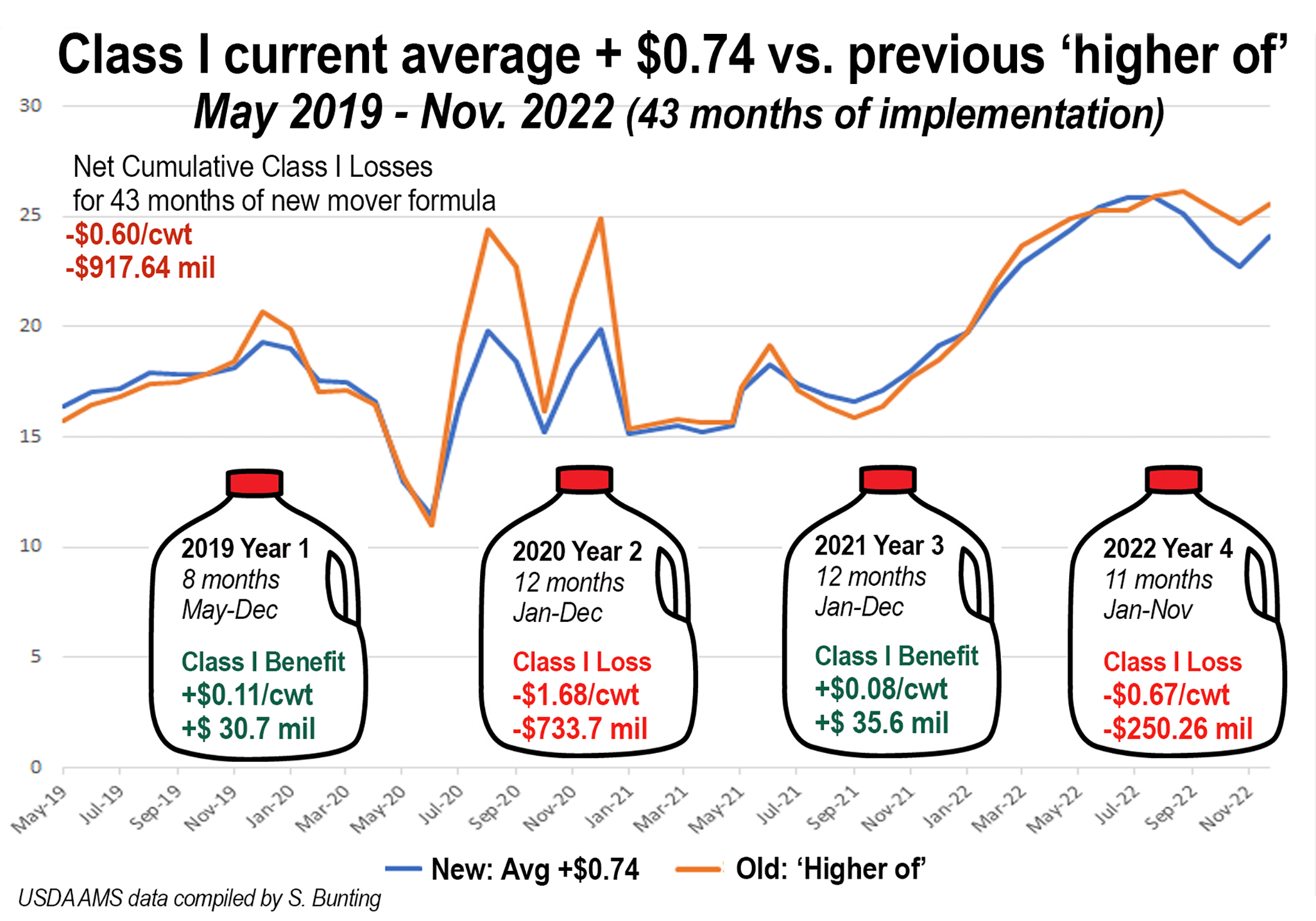

The recommendation to return to the higher of Class I mover is an important response by NMPF to dairy farmer concerns. That ball has been in USDA’s court after the first two years of implementation, according to the farm bill language that changed it to an averaging method in the first place. Four years and nearly $1 billion in cumulative Class I net value losses have passed (see chart), but Ag Secretary Tom Vilsack said he needed to see “consensus” before allowing a hearing to be opened.

In post-conference interviews, several Farm Bureau Forum attendees said this was their main priority for participating – to show Secretary Vilsack there is consensus to “fix the mistake.”

For NMPF to include it in their plan is a win.

Another item in the NMPF plan is to develop a process to ensure make allowances are reviewed more frequently through legislation directing USDA to conduct mandatory processor cost studies every two years and to update the make allowances contained in the USDA milk pricing formulas.

There was general agreement from stakeholders in Kansas City that processor costs need to be evaluated and make allowances updated. Over half of the table-groupings identified this. There was also healthy discussion of some ways to do this to minimize the sudden impact on farmer milk checks – all good points for developing a process and for a USDA hearing process to fully evaluate it.

Of the bones to pick, one NMPF recommendation that runs counter to what more than half of the table-groupings prioritized in Kansas City concerns expansion of the pricing survey to include more products. NMPF’s task force decided not to add any products to the price survey, and in fact they are recommending dropping one.

On the chopping block is the 500-pound barrel cheese price in the protein calculation for Class III.

Initially, NMPF’s task force committees looked at adding unsalted butter, skim milk powder (a higher value more standardized product than nonfat dry milk), and they looked at mozzarella cheese. In all three cases, the task force chose not to recommend additional products.

The fact that they are recommending elimination of a product from the pricing survey is curious.

Less than one-third of the Kansas City table-groupings listed elimination of barrel cheese pricing as a priority. Few people questioned NMPF economist Peter Vitaliano on the sensibility of this recommendation – except for yours truly.

I asked this question: “On the blocks and barrels, what do you foresee happening if the barrels are dropped? Right now we’ve got barrels doing more trading than blocks. We’re really not seeing much trading at all in blocks on the CME spot market. Also, would this mean that the cost of making those barrels will be backed out of the processing cost survey in terms of establishing new make allowances?

Vitaliano gave this answer: “That’s an interesting question. I’ve heard different interpretations of what’s going to happen to barrels if they are not used in the formula. Some folks feel they’ll just be priced at a discount to blocks, and the cash market for barrels will go away. I’m not sure I buy into that totally because barrel cheese is becoming a different product.”

The NMPF economist continued with his answer: “Under current quality standards, barrel cheese is the only major way that you can get uncolored whey, which is demanding a premium in the marketplace because all of these nutrition products, these high value nutrition products in demand by millennials and others, they don’t want to show ‘bleached whey’ on the label, they want the white uncolored whey powder that comes from barrel cheese production.”

Apparently, yellow whey from block Cheddar production is less desirable. But we’ve known this for at least 15 years.

In other words, according to Vitaliano, there is right now a ‘subsidy’ effect from the premium paid for the higher value of the uncolored whey that creates the environment to produce more barrel cheese – regardless of what the cheese market is doing.

Vitaliano noted that FDA is going to consider some changes that might alter how this cross-product scenario is playing out by allowing microfiltered milk to be used in plants producing standard-of-identity cheese, but the bottom line is that barrel processors making whey protein concentrate as co-products benefit from the white-whey premium whereas block cheese processors do not.

When the two are averaged together in the Class III protein formula, they represent different markets when they historically moved together, said Vitaliano.

Interestingly, however, barrels have traded higher — not lower — than blocks on the CME for most of this year.

In the purely cheese market history, barrels and blocks moved together more closely, then in times of market shocks beginning in 2009, we would see periods of wide spreads and inversions, sometimes barrels over blocks and most of the time blocks over barrels. During intervals in 2016-17, barrels sold at 10 to 20-cent discounts to blocks. Since 2018, we’ve seen long intervals of barrels over blocks by up to 25 cents and then the flipside with blocks over barrels.

This year (2022), barrels have sold at a premium to blocks consistently since April. The barrel premium over blocks stood at 15 cents per pound last week. That’s a significant impact on farm-level milk prices — to the good.

Coincidentally, barrel prices crashed this week, losing 22 cents, where blocks lost a nickel, thereby pushing barrels under blocks by a few cents on Oct. 25, the same day that the NMPF Board voted unanimously to endorse the multi-pronged modernization plan that includes dropping 500-lb barrel cheese out of the FMMO end-product pricing formula.

For the year (2022), barrels will likely average a nickel above blocks.

There is also the question of price discovery. For the year, we have seen more barrels traded on the CME compared with the volume of blocks.

When following up in a question about what happens to price discovery if the barrels are eliminated from the pricing formula, Vitaliano responded that 15% of the cheese reported in USDA’s weekly price survey is barrel cheese. Rather than reduce the weighted average to reflect that, and rather than including mozzarella in the pricing survey (a higher volume and value item than cheddar), NMPF is simply recommending the elimination of barrels to avoid the block/barrel spread.

Vitaliano said pricing formulas are based on the USDA price survey, not on the CME spot market. However, the CME spot market is used to set pricing for the USDA-reported sales.

Vitaliano also noted that price discovery on the CME spot market is achieved even if no product changes hands because it is a marginal market-clearing trade in the first place.

“The whole industry is watching that market, so if that block price is, let’s say, overvalued, and I have extra blocks and I think that market is high, anybody can go to that market and sell; or if you think it’s undervalued, you can go to that market to buy,” he said. “Just because there’s not a lot of trading, doesn’t mean it’s not necessarily representative of the market… we just have to trade the marginal excess or shortage.”

According to Vitaliano, even the regulators have looked at this and concluded that since the whole industry watches that market — everybody has the opportunity to jump in, and they are not shy if they have a different idea about what the market should be, they can go in and make bids or offers. Those bids and offers move the market whether or not a trade is completed.

Even in light of these explanations, the NMPF recommendation to eliminate barrels from the pricing formula remains a bit of a head-scratcher and needs more discussion and evaluation.

NMPF also wants to expand the forward pricing window for whey and nonfat dry milk (NFDM) price-reporting to 45 days instead of 30 in order to “capture more of the global market in the pricing formula.”

However, when asked why NMPF is not seeking to expand the price reporting to include skim milk powder (SMP) – the globally traded powder – as a means of capturing more of the higher-value global market, Vitaliano said SMP is sold at differing standardized protein rates as a value-added product. NFDM, on the other hand, often has more protein in it, but it’s variable and a lower-priced bulk commodity. It’s a true bulk product that is made to soak up excess milk, he explained.

Vitaliano also noted that NFDM is used by domestic cheese makers, whereas SMP is not.

Ditto the answer for unsalted butter. While the sales of unsalted rival salted butter in volume, and it is a bulk product more consistent with higher-value global markets, the NMPF task force perspective is that the unsalted butter is also a step up as a value-added product for a specific market in foodservice, not a commodity bulk product a plant would make with excess milk.

Ditto for mozzarella, which NMPF maintains is already priced off the USDA-reported cheddar price even though the U.S. sells more mozzarella than cheddar today.

Next week, we’ll dig into the yield factor changes in the NMPF plan and the glaring absence of a recommendation on depooling issues across the country. Solving the depooling conundrum was a priority listed by over half of the consensus-building table-groupings at the Farm Bureau Forum and producers from multiple regions were vocal about it throughout the three-day meeting.

-30-

Seems like USDA is quietly in mea culpa mode and willing to undo their their “higher of” to “average +” fiasco costing producers at least $3 billion. NMPF Board Members owe farmers a full explanation!! Ag Oversight Committee and DOJ should review this change to interpret how these deductions could have just showed up with NO PUBLIC

HEARINGS. Now Vilsac wants a single

directive with full pre-determined outcome before a public hearing. Looks like USDA is a top-down authoritarian type of organization. Just thinking.

LikeLike