By Sherry Bunting, Farmshine, Sept. 11, 2020 and preview Sept. 18, 2020

Whole milk sales up 6.5% Jan through May, total milk sales flat

While consumer packaged goods (CPG) reports indicate fluid milk sales being up 4 to 5% through the Coronavirus pandemic — and flattening as of the end of August back to year ago levels — the other side of that coin is the loss of institutional, foodservice and coffee house demand. Thus, the extra CPG sales at supermarkets slightly more than covered the lost usage in foodservice and the net wholesale volume of fluid milk sales reported by milk handlers January through May 2020 was virtually unchanged (up 0.2%) compared with a year ago, according to USDA.

Within that volume are some important shifts. Conventional fluid milk sales to all uses were down 0.5% vs. year ago in the first 5 months of 2020 while organic fluid milk sales were 14% higher than a year ago.

Within the conventional milk sales, whole milk was up 6.5% and reduced fat (2%) milk was up 3.3%. Also gaining in sales January through May 2020 were “other” fluid milk sales, which includes ultrafiltered milk such as Fairlife, up 10.5% vs. year ago.

The big losers were fat free milk down 12% from year ago and flavored fat reduced milk down 22%.

These numbers were reported in the most recent USDA product sales report. Given that this included the mid-March through early May period when shortages and purchase limits were put on fluid milk in many stores throughout the country, it will be interesting to see June and July data when they are reported in the next 30 to 60 days.

Clearly, consumers are shifting even more strongly to whole and 2% milk and away from 1% and fat-free milk. With organic sales also experiencing sales increases, it is a sign that consumers are looking at health indicators, and a sense for wanting what’s real, natural and perceived to be most local when choosing milk for home. At the same time, overall sales of conventional milk are negatively impacted by the steep drop in institutional, foodservice and coffee house demand.

Class I milk markets get demand push from gov. purchases

At the wholesale milk handler level, USDA reports tightening milk supplies in the eastern U.S. relative to Class I usage. Specifically, the USDA Eastern Fluid Milk and Cream Report Wednesday, Sept. 9 indicated Class I sales picking up this week in the Northeast with balancing operations receiving steady to lighter milk volumes compared with recent weeks.

In the Mid-Atlantic region, milk reported to be adequate for Class I needs, and loads traveled to the Southeast for immediate needs as USDA reports Southeast milk production is tight and output is down with most milk loads clearing only to Class I plants and no loads to manufacturing.

USDA reports production of seasonal milk beverages such as pumpkin spiced flavored milk and eggnog have begun to pick up.

USDA reports that the steady to higher Class I demand is due to some schools returning to session along with government programs purchasing extra loads from manufacturers this week. In fact, reports USDA, bottlers in eastern markets are receiving milk from other regions, which is loosening up the previously tighter cream availability.

Block cheese rallies past $2/lb, but futures rally is short-lived

Cheese markets made significant gains for the third week in row, fueled in part by the third round of USDA CFAP food box purchases for delivery October through December 2020.

On Wed., Sept. 9th, 40-lb block Cheddar was pegged at $2.1575/lb — up 25 cents from a week ago with a single load trading. The 500-lb barrel cheese price was pegged 10 cents higher than a week ago at $1.67/lb, with zero loads traded. The barrel price had reached $1.70 earlier in the week before backing down Wednesday, taking early week futures market gains along with it.

The block to barrel spread is at its widest level of 48 cents per pound, an indicator of cheese market vulnerability and volatility for the longer term.

Butter loses cent, powder gains cent

Spot butter lost a penny with a significant 13 loads trading Wednesday on the CME spot market, pegging the price at $1.50/lb. Nonfat dry milk gained a penny at $1.0425/lb with 3 loads trading.

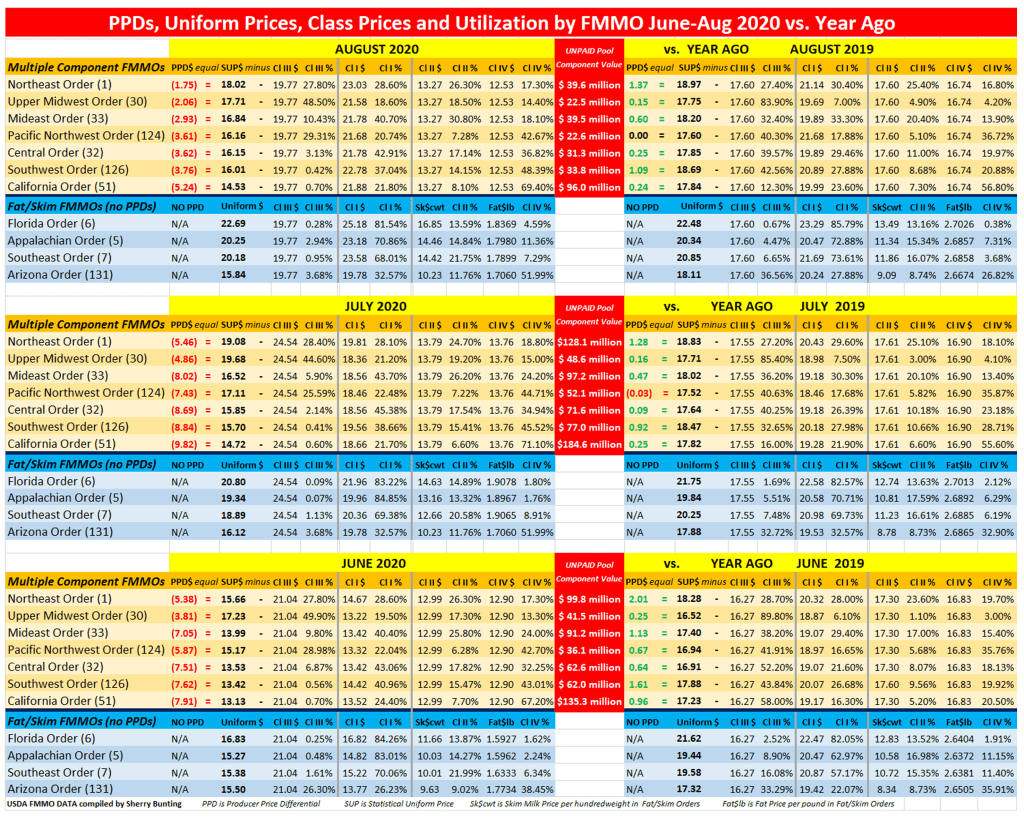

Negative PPDs persist, unpaid component value across 7 MCP Orders totals $1.47 billion for June through August milk

Look for more on this in the 9/18 Market Moos in Farmshine, but for now, here’s a chart I’ve compiled showing relevant information for August, July and June 2020 vs. same month year ago in 2019.

The bottom line is three months of significantly negative PPDs resulted in $1.47 billion in total unpaid component market value across the 7 Multiple Component Pricing Federal Milk Marketing Orders.

Losses were also incurred by the 4 Fat/Skim Pricing Orders but are not easily quantified on the FMMO pool balance sheet.

This has cost dairy producers even more who have paid to manage risk through a variety of tools because those tools only work when the milk check follows the market higher to provide the protected margin. When the market says ‘no fire here’ but the house burned down just the same, it’s a double-whammy.

Remember, fluid milk does not have a ‘market’ because it is regulated or used as a loss-leader by the nation’s largest supermarkets. Thus, the value of the components in fluid milk can only be market-valued in the other products made with milk that “sort of” have a market. When that market rallied, the value was pulled instead of pooled.

Instead of ‘band aid’ approaches to milk pricing reform, given the Class I change made in the 2018 Farm Bill has been a disaster, it’s long past time for a national hearing on milk pricing with report to Congress.

Read on, to see how other factors such as imports vs. exports affect storage anc contribute to unprecedented market misalignment.

Close-up Cl. III / IV spread widens, average for next 12 months narrows

The spread between Class III and IV milk futures widened to a $4 to $5 spread for September and October, $2 to $3 for November and December. But the average over the next 12 months for both classes in CME futures trading has narrowed this week.

The Class III futures contract for September traded at $16.62/cwt Wednesday, Sept. 9 — fully steady with a week ago while Class IV traded 15 cents lower than a week ago at $12.83.

October’s Class III futures contract traded at $18.48 Wednesday, down 54 cents from a week ago, while Class IV traded at $13.64, down 40 cents.

The next 12 months of Class III milk futures closed the Sept. 9 trading session at an average $16.68 — down 24 cents from a week ago.

The next 12 months of Class IV futures averaged $15.03 — down 4 cents from a week ago.

At these midweek trading averages, the spread between Class III and IV over the next 12 months averages at $1.65/cwt — 20 cents tighter than the previous Wednesday.

Import-Export factors affect storage, which in turn affects markets

As mentioned previously, the most recent USDA Cold Storage Report showed butter stocks at the end of July were up 3% compared with June and 13% above year ago. Total natural cheese stocks were 2% less than June and up only 2% from a year ago. Bear these numbers in mind as we look at exports and imports.

According to the U.S. Dairy Export Council (USDEC), total export volume is up 16% over year ago year-to-date – January through July. For July, alone, total export volume was up 22% over year ago. Half of the 7-month export volume was skim milk powder to Southeast Asia. January through July export value is 14% above year ago.

However, butterfat export volume averaged 5% lower than a year ago year-to-date. The big butter export number for July was not enough to make up for the cumulative decline over the previous 6 months.

On the import side, the difference between cheese and butter is stark. Cheese imports are down 10% below year ago, but the U.S. imported 14% more butter and butterfat in the first 7 months of 2020 compared with a year ago.

The largest increase in butter and butterfat imports occurred in the March through June period at the height of the pandemic when retail butter sales were 46% greater than year ago.

Looking at these butter imports another way, is it any wonder butter stocks are accumulating in cold storage to levels 13% above year ago at the end of July — putting a big damper on butter prices and therefore Class IV?

The U.S. imported 14% more butter and butterfat and exported 5% less butter and butterfat year to date while storage has been running double-digits higher, up 13% at the end of July.

As accumulating supplies pressured butter prices lower, the U.S. became the low price producer and exported a whopping 80% more butter in July compared with a year ago. This was the first year over year increase in butter exports in 17 months. But the record is clear, year-to-date butter exports remain 30% below year ago and total butterfat exports are down 5% year-to-date.

Analysts suggest that butter and butterfat imports are higher because U.S. consumer demand for butterfat has been consistently higher — even before the impact of the Coronavirus pandemic stimulated butter demand for at-home cooking and baking.

This reasoning is difficult to justify — given there is 13% more butter currently stockpiled in cold storage vs. year ago keeping a lid on the wholesale prices (while retail prices rise) and undervaluing butterfat and Class IV milk price in the divergent milk pricing formula. If 14% more butter and butterfat are being imported, does this mean we need to import to serve consumer retail demand and keep larger inventory at the ready to serve that retail demand?

If so, why is the inventory considered so bearish as to hold prices back and thus amplify the Class III and IV divergence?

Does month to month cold storage inventory represent excess? Or does it simply represent a difference in how inventory is managed in today’s times, where companies are not as willing to do “just in time” and “hand to mouth” — after they dealt with empty butter cases and limits on consumer purchases at the height of the pandemic shut down this spring.

The trade has not sorted out the answers to these questions.

Meanwhile, these export, import, and government purchase factors impact the inventory levels of Class III and IV products very differently — and we see as a result the wide divergence between Class III and IV prices and between fat and protein component value.

Interestingly, USDA Dairy Programs in an email response about negative PPDs that have contributed to the wide range in “All-Milk” prices, says the higher value of components “is still in the marketplace” even if All-Milk and mailbox price calculations do not fully reflect it across more than half of the country.

Rep. Thompson and Keller want Whole Milk choice for WIC

The American Dairy Coalition, a national organization headquartered in Wisconsin, applauded Congressmen Fred Keller and G.T. Thompson, representing districts in Pennsylvania, for recently introducing a bill designed to offer an expanded variety of dairy products, including 2% and Whole fat milk, to participants of the Special Supplemental Nutrition Program for Women, Infants and Children (WIC). The bill, officially titled, “Giving Increased Variety to Ensure Milk into the Lives of Kids (GIVE MILK) Act,” would expand WIC offerings.

The Grassroots Pa. Dairy Advisory Committee joins the American Dairy Coalition in thanking Congressmen G.T. Thompson and Fred Keller for their dedication to trying to help nutritionally at-risk Americans have the ability to choose what dairy products fit the taste preferences of their families. Thompson is prime sponsor and Keller a co-sponsor along with 39 other members of Congress on another bill — the Whole Milk for Healthy Kids Act, H.R. 832 — aimed at allowing whole milk choice in schools too.

Current Dietary Guidelines have stifled Whole milk choice by recommending 1% and fat-free milk for children over 2 years of age even though Whole milk provides a nutritionally dense, affordable and accessible complete source of protein that children love.

Science shows consumption of these products promote a healthy weight in both children and adults and fends of chronic diseases.

“More initiatives such as the GIVE MILK Act are necessary to change the antiquated and unscientifically based notion that saturated fats are dangerous to public health,” states a press release from the American Dairy Coalition. “We encourage all members of the dairy industry to not only support the GIVE MILK Act, but also encourage their legislators to urge the Dietary Guidelines for Americans also be updated to remove caps on saturated fats, allowing once more the choice of whole milk in public schools. Children deserve the best — let’s give them whole milk!”

Look for more next week on what the Grassroots Pa. Dairy Advisory Committee and 97 Milk are working on to get the word out to “Vote WHOLE MILK choice in schools — Citizens for children’s immune-boosting nutrition.”

-30-

Pingback: As depooling, negative PPDs and Cl. I formula change continue stealing value from milk checks, here’s what you can do | Ag Moos

Pingback: Covington: Class I change cost producers ‘real money’ | Ag Moos