Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

EAST EARL, Pa. — The June 1 Federal Milk Marketing Order (FMMO) price changes delivered mixed results: modest gains in higher-Class I fluid markets, pain in manufacturing markets, and a flat national all-milk price, despite higher dairy commodity prices in June vs. May.

With more than $8 billion in new U.S. dairy processing investments, supply and demand signals are being reshaped and pool revenues impacted as handlers navigate the pricing changes, including the new and larger make allowance deductions. These are not line items on milk checks but are subtracted from the four base commodity prices — butter, cheddar, nonfat dry milk, and dry whey — used in the class and component prices, including the Class I base mover.

Dr. Chuck Nicholson of UW-Madison noted in a recent PDP Dairy Signal podcast that the changes were not designed to improve dairy farmer income but to preserve the integrity of the FMMO system — a system that is believed to be beneficial to dairy farmer income.

Nicholson expects it will take six months or more for premiums, deductions, and pooling decisions to settle out after the final piece is implemented.

The final piece is the revised skim composition standards that arrive in Dec. 2025. They are expected to be generally positive for dairy farmers, but will have ripple effects in how components are paid, how breakevens are figured for hedging, and in handler pooling strategies.

One thing is clear: The new rules make milk pricing more complicated and milk checks less transparent. Supply and demand market signals are taking a back seat as formula changes, higher make allowances, ESL adjustments, and shifts in Class I differentials reshape how pool revenues are calculated.

As buyers navigate for price advantage; dairy farmers should do the same by understanding what’s here, what’s coming, and adjusting herd, feed, and risk management strategies.

Get ready for December

The skim composition factors will increase for Class I handlers and for the ‘reported’ Class III and IV baseline prices and FMMO statistical uniform prices (SUPs). Protein increases from 3.1% to 3.3%, other solids from 5.9% to 6.0%, and nonfat solids from 9.0 to 9.3%.

Butterfat remains unchanged at 3.5% because all handlers, even Class I, pay pooled butterfat on actual pounds, whereas Class I pays skim components at standard levels.

Producers in multiple component pricing (MCP) Orders will continue to be paid on actual pounds of protein/other solids, but the reported Class III and IV baseline prices will be set higher, along with Class I, to reflect the new skim factors.

Why it matters

Skim composition updates raise the baseline prices for Class III and IV after the higher make allowances have already lowered these baselines prices. Because Dairy Revenue Protection (DRP) “trigger revenues” are tied to these prices, coverage costs and payouts will shift. Hedging breakevens will also need to be reassessed for impacts depending on the farm’s component profile.

High-protein herds above the old standard of 3.1% may see reduced premiums because more of their “extra” protein moves into the baseline Class III price at 3.3% in December, changing how hedges or DRP line up with actual milk checks.

Low-protein herds, below the new standard of 3.3% could face new deductions or discount risk.

With protein up at 3.3% and fat unchanged at 3.5%, the Class III fat-protein ratio tightens, altering potential decisions by handlers on strategic pooling or depooling of producer milk.

As Class III and IV baseline values were lowered in June (via the make allowance increases) and will be raised in December (via the skim composition changes), DRP revenue expectations may misalign unless levels are reassessed.

Nicholson explains that farmers whose milk has been consistently pooled will want to talk with their nutritionists, buyers, co-ops and risk advisors about component levels to ensure risk management strategies align with milk check revenue and consider feeding and management adjustments to minimize negatives and maximize positives.

What can farmers do?

They can’t control formulas, but they can:

Maximize components: Boosting components remains the surest way to improve milk checks.

Maintain milk quality: This secures a milk market in the face of processing disruptions and positions the farm for future premiums if they return or improve.

Scrutinize line items: Marketing or balancing deductions and re-blends may ease as processors benefit from larger make allowance credits. Remember: Class I is the only class of milk that must be pooled, and co-ops are not required to pay pooled members the FMMO minimum blend; they may re-blend with deductions.

Know your minimum price: Each farm’s FMMO-minimum depends on butterfat plus protein and other solids, making every farm’s baseline unique.

What changed in June?

June milk checks were the first to reflect the larger make allowances that muted market strength that month. This was demonstrated in USDA’s June all-milk price at $21.30/cwt, which was flat vs. May, despite higher prices for all four base commodities used in the FMMO price formulas.

Did return to higher-of help?

The return to higher-of did not help in the first two months, actually cutting the Class I base price by $1.37 and 79¢/cwt in June and July, because the spread between Class III and IV pricing factors was narrow.

For August and September, however, the higher-of method adds 30¢/cwt as Class III and IV price spreads have widened.

ESL adjustment, what is it?

Extended-shelf-life (ESL) Class I products now carry an automatic adjustment, based on a calculated rolling average historical difference between higher-of and average-of methods. This ESL adjustment is applied to the volume of skim used in Class I ultra-pasteurized, aseptic, and micro-filtered products with shelf-life of 60 days or more.

In June, the ESL adjustment at +$1.38/cwt added an estimated $2.2 million to the Northeast pool, which came out to about 9¢/cwt across all pooled milk. For the Mideast pool, it added an estimated $1 million (6¢/cwt). According to USDA, this adjustment can be positive or negative. It has already declined substantially for August at +57¢ and September +53¢/cwt, and it can swing negative.

Differentials vs. location adjustments

Class I differentials were increased nationwide, though larger negative location adjustments puzzled some farmers. The net is still positive. For example, New Holland, Pennsylvania’s Class I differential increased from $2.90 to $4.30/cwt, while its location adjustment shifted from –35¢ to –80¢, netting +95¢/cwt.

The make allowances bite

Processor credits, known as make allowances, increased by 25 to 30%. The June Class III baseline price was $18.82 — about 66¢/cwt lower than under old make allowances. Class IV lost 50¢.

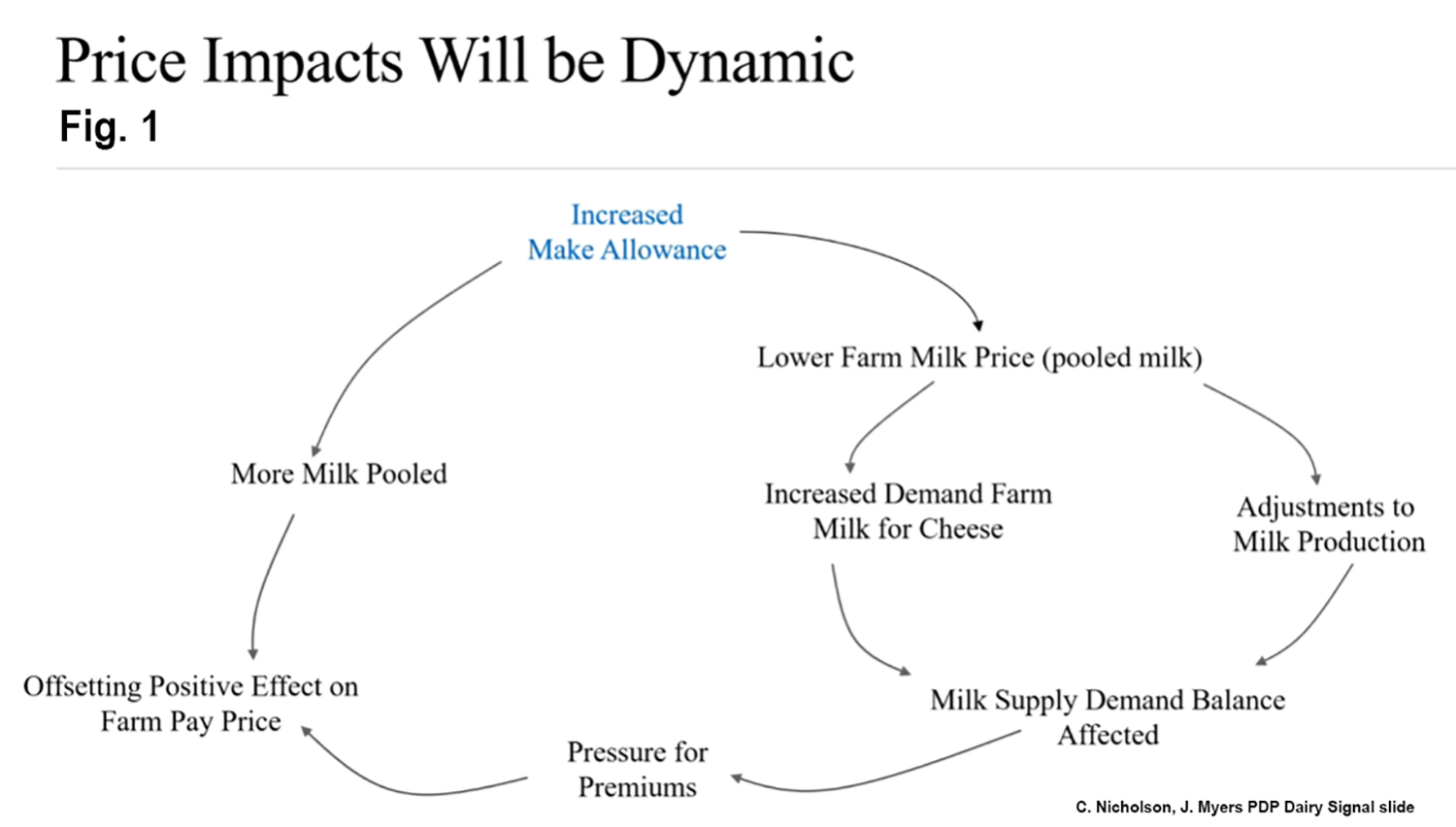

By December, when the final reform piece takes effect, Nicholson estimates pooled producers will see the difference between the old and new make allowances trim 32¢/cwt from the baseline Class III price and 91¢/cwt from Class III component pool value; while trimming 43¢/cwt from baseline Class IV and 74¢/cwt from Class IV component pool value (Table 1).

The impact on non-pooled milk or milk marketed under cooperative re-blends remains uncertain. Nicholson expects some positive offsets — eventually — as premiums return, especially outside the pool.

Nicholson and UW-Madison graduate student Jack Myers recently presented national dynamic economic modeling showing how the larger make allowances affect decisions by milk buyers and dairy farmers (Fig. 1) — resulting in a pain-before-gain offsetting effect over time.

Barrel cheese removal

Barrel cheese sales were removed from Class III and protein price formulas. Barrels often weighed down protein by trading below blocks and being adjusted for moisture levels. While seen as positive historically, new block-cheddar capacity in 2025-27 may alter future impacts. Barrels still trade on the CME, but USDA no longer reports them in the weekly National Dairy Product Sales Report (NDPSR), making comparisons impossible.

Regional blend impacts

Revised formulas and higher make allowances converged with new cheese capacity to pressure cheese-milk prices lower, boosting Class III utilization by 60% nationwide. Strategic depooling pulled blend prices lower in cheese-heavy regions.

Meanwhile, fluid-heavy regions dipped initially, despite higher Class I differentials, because advance pricing was based on May’s weaker market and the return to higher-of produced no advantage. July brought recovery.

Market volatility adds complexity

The implementation of new formulas coincides with new cheese processing in 2025, keeping U.S. cheese priced 20 to 35% below global indexes. This supports exports but pressures farm-level income.

CME trading illustrates the see-saw balancing pattern now emerging, with potential impacts for monthly checks. In August, cheese rallied to $1.88/lb by Aug. 13, and then in the next eight days from Aug. 14 through 22, the cheese price dropped to $1.77, rebounded to $1.87, then plunged to $1.75. These swings feed into the 2- to 6-week lag between Class I advance prices and manufacturing class and component announcements.

By Sherry Bunting, Farmshine, Feb. 21, 2025 (with updates after print publication)

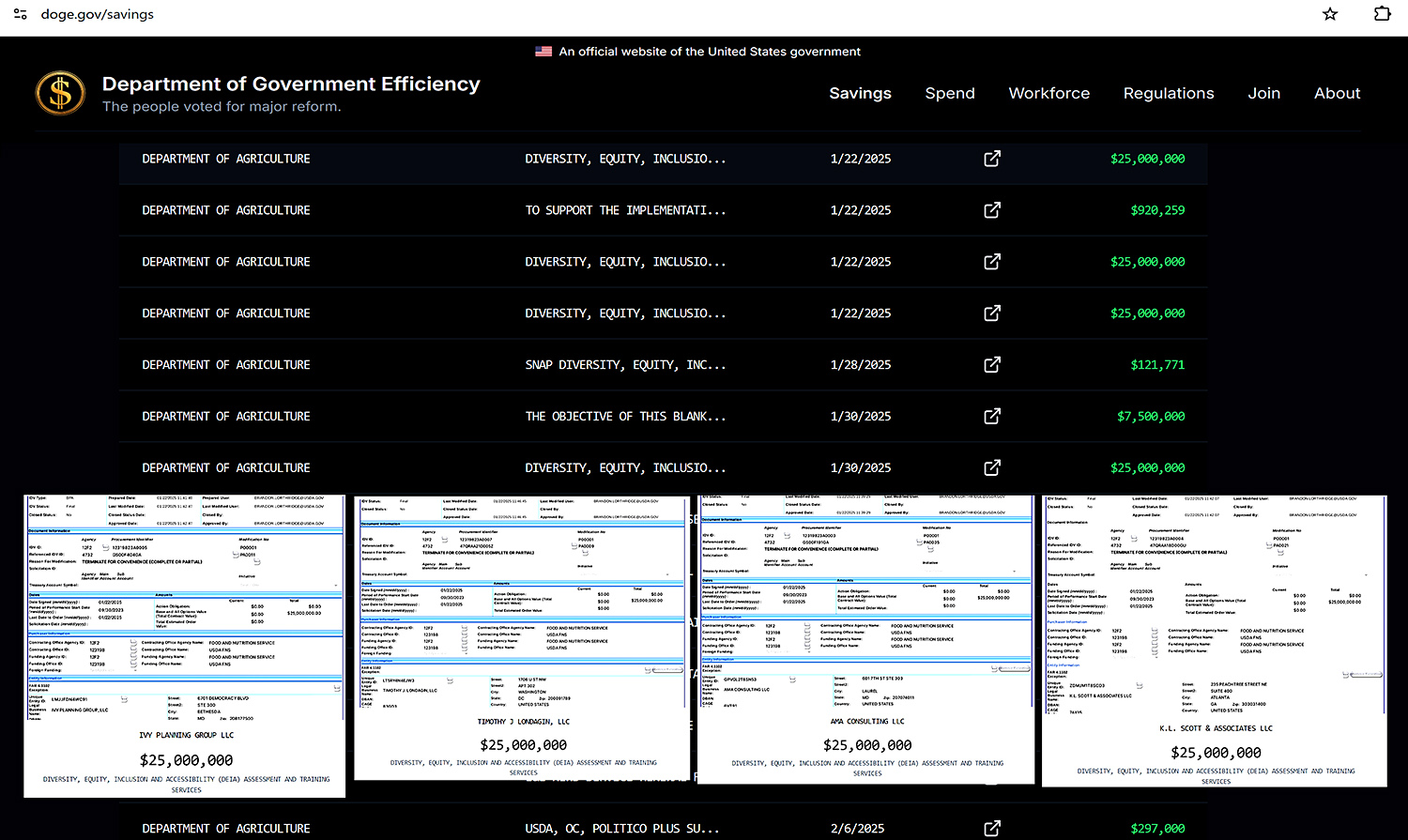

WASHINGTON – Upon reading the Feb. 14 news release about USDA’s 78 terminated contracts totaling $132 million, as identified in the ongoing review by the Department of Government Efficiency (DOGE), we noticed only 10 examples were given, totaling only $4.21 million. Reports had surfaced about Conservation Districts receiving project or program termination notices via email, and a few farmers communicated their concern about frozen funding for grant reimbursements.

So, we looked into it.

One email notice that Farmshinewas able to view, dated Feb. 14, for a project in a Colorado Conservation District, stated the reason in the subject line: “The project no longer effectuates agency priorities regarding diversity, equity, and inclusion programs and activities.”

However, the notice also clearly stated that final payments would be made on work already conducted for the terminated project — as long as the final reports and final payment requests are submitted within 120 calendar days of the notice.

We emailed the USDA press office on Feb. 18, as follows:

“A few farmers have communicated about canceled contracts or frozen funds related to conservation projects, some in which projects were started or planned, and these farmers were expecting reimbursement through grants. The news release about the $132 million in canceled contracts lists 10 things as examples outside of the core mission of USDA, but these examples only total $4.21 million, not $132 million. Where can we find a list of the balance?”

The press office turned our request over to the Freedom of Information Act (FOIA) officer at the USDA Farm Production and Conservation Business Center, who promptly responded by email on the very same day, Feb. 18, directing us to a government information specialist who could help us file an official FOIA request.

The specialist answered our call on the first try that same day (Feb. 18). Our official FOIA request was modified to seek a listing of the 78 terminated contracts referenced in the USDA press release. This experience runs contrary to what some in the mainstream media have reported about FOIA officers being “gone.”

In fact, we received a follow up email the next morning (Feb. 19) with additional information and a link to https://doge.gov/savings, where all terminated contracts throughout all federal agencies will be updated twice a week. USDA ranks 5th in the top 10 federal agencies in amount of savings as of Feb. 18.

A look at the listing shows zero terminations of any on-farm conservation project contracts.

Furthermore, $100 million of the $132 million is accounted for in the four separate $25 million contracts with four separate consulting companies, mostly located in the Capitol region, for “Diversity, Equity, Inclusion and Accessibility (DEIA) Assessment and Training Services” within the USDA’s Food and Nutrition Service, or FNS.

(Just think how much of the currently banned whole milk — which former Ag Sec. Vilsack said schools cannot afford anyway — could be purchased for the FNS-controlled National School Lunch Program with such savings!)

Also terminated was a contract with a Vermont consulting firm for “Environmental Compliance Services for the implementation of Partnership for Climate-Smart Commodities.” Even though this $8.2 million award had already been paid, the termination prevents additional orders.

While the government information specialist cannot answer abstract questions, she did indicate that conservation projects through EQIP and NRCS — that are attributed to the farm bill — are not included in the contract terminations. However, Climate Smart projects under the Inflation Reduction Act (IRA) were included in the funding that was ‘on hold’ for review.

Then USDA announced in a Feb. 20 press release that, “Secretary Rollins will honor contracts that were already made directly to farmers. Specifically, USDA is releasing approximately $20 million in contracts for the Environmental Quality Incentive Program, the Conservation Stewardship Program, and the Agricultural Conservation Easement Program.”

This is the first tranche released from the ‘pause’ as USDA continues to review IRA funding “to ensure that we honor our sacred obligation to American taxpayers—and to ensure that programs are focused on supporting farmers and ranchers, not DEIA programs or far-left climate programs,” the press release stated.

We also learned from other sources that commodity checkoff programs are part of the broader DOGE review of all USDA activities for the purpose of evaluating, and potentially reforming both spending and policy in agriculture.

The dairy promotion and research program, funded by the 15 cents per cwt checkoff, is one of 22 such mandatory commodity programs overseen by USDA AMS. According to repeated statements by dairy checkoff leaders over the past five years, this oversight involves USDA AMS reviewing all checkoff-funded activities, including for USDA staff attending all DMI meetings “even conference calls.”

This oversight comes at a cost. Of the 2022 and 2023 financial statements available for Dairy Management Inc (DMI), National Dairy Promotion and Research Board (NDB) and the consolidated United Dairy Industry Association (UDIA) and National Dairy Council (NDC), only the NDB listed USDA Oversight as a line item under its operating costs, totaling just under $1 million annually, along with a collections and compliance line item totaling just over $500,000.

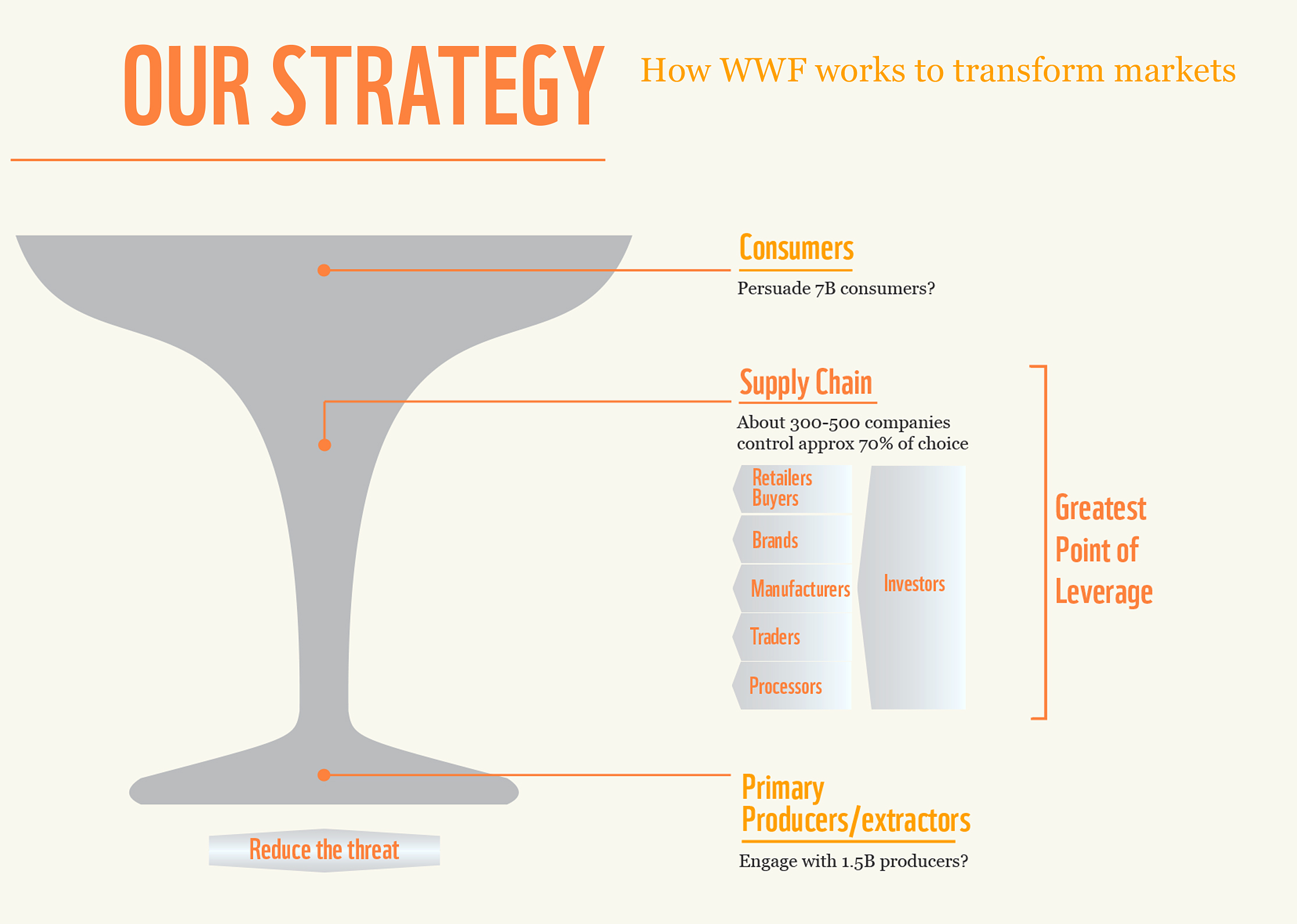

How might the DOGE algorithms decipher these costs and engagements, given both USDA and DMI have contracted with NGOs like World Wildlife Fund (WWF)?

How might it interpret WWF’s published playbook of leveraging the supply-chain of 300 to 500 companies controlling 70% of consumer food choices?

WWF’s playbook uses the consolidation in the middle (above) to move the much larger number of food producers and food consumers toward implementing their sustainability goals, the so-called ESGs (Environmental, Social, Governance) that focus on DEI, biodiversity, and their particular take (and flawed math) on the climate impact of methane emissions from cattle, disregarding the carbon cycle that is the essence of life.

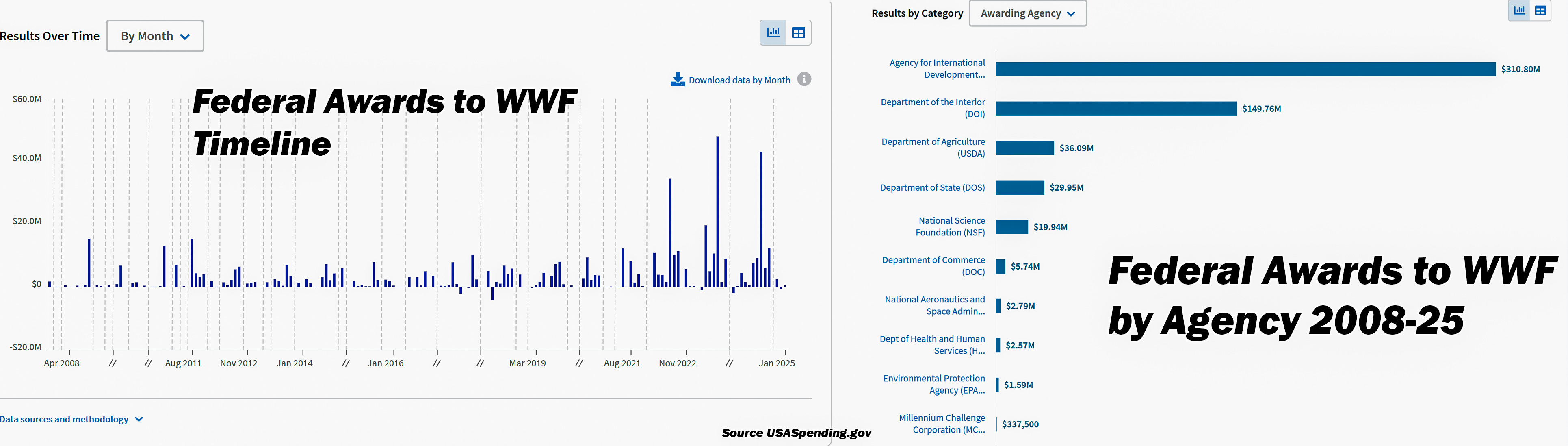

In fact, upon being provided with the link to USA Spending as part of the response we received from the current administration regarding our FOIA request, we found that the federal government has awarded the NGO World Wildlife Fund (WWF) more than $500 million since the start of the Obama administration in 2009. The bulk of the funds were awarded in 2022-24 during the Biden administration.

Of the over $500M, USAID awarded WWF $310M; the Department of Interior awarded WWF $149M; and USDA awarded WWF $36M, with other federal agencies rounding out the total. ($500M is a large sum that the mainstream media refer to as “merely a rounding error” next to the $36T (trillion) in national debt, but where else do these layers lead in terms of money and policy?)

We already know that the dairy and beef checkoffs began their alliances with WWF in the 2008 to 2010 time frame — when the work to develop their Net Zero and Sustainability platforms for dairy and beef producers began, and really ratcheted up by 2021.

Contracts with NGOs in other departments of the federal government have also been terminated through the DOGE reviews, especially via USAID, according to repeated press reports. What more may we learn from the DOGE review on potential entanglements between USDA, checkoff programs, NGO’s like WWF, and the food industry — that are not truly farmer-led but impact farmers?

To-date, there are no indications that the USDA AMS administration of the Federal Milk Marketing Orders are part of the DOGE review; however, it’s possible, depending on how these FMMO administration costs are allocated.

According to the Congressional Research Service (CRS), the 1937 Agricultural Marketing Agreement Act gives USDA several authorities in Federal Milk Marketing Orders (FMMO) that are administered through Dairy Programs under AMS. The associated costs of FMMO administration, according to the CRS “are partly covered by an assessment levied on handlers at no more than five cents per cwt., which is often passed on as deductions on farm milk checks.

WASHINGTON, D.C. – The U.S. Senate confirmed Brooke Rollins 72-28 on February 13th as the 33rd Secretary of Agriculture, and the second woman to lead the USDA. On Friday, Feb. 14, she was sworn in and addressed a gathering of over 400.

Rollins pledged to bring greater efficiency to the USDA to better serve farmers, ranchers and the agricultural community.

“We welcome the DOGE efforts because its work makes us better, stronger, faster and more efficient,” said Rollins of the review of USDA already underway by the Department of Government Efficiency (DOGE), headed by Elon Musk.

She announced an end to identity politics, pledging equal dignity.

Rollins also said the USDA will be “returned to its basic purpose,” with a focus on its core missions of supporting American farming, ranching, and forestry.

In a Feb. 14 news release, Rollins noted that the DOGE review continues to be comprehensive and announced the first tranche in a series of reforms.

USDA is currently reviewing more than 1000 contracts for possible termination. The department has already terminated 78 contracts, which totaled more than $132 million. Some of these contracts were proposed procurements that were discontinued before they went into effect, according to the news release.

The news release gave 10 examples of terminated contracts, which totaled just $4.21 million. Ending Politico subscriptions at $2.77 million, represented the bulk of the money in the examples. Other items listed ranged $30,00 to $300,000, such as Diversity, Equity and Inclusion (DEI) ‘onboarding’ specialist, Diversity Dialogue Workshops, a Brazilian Forest and Gender Consultant, a Women and Forest Carbon Initiative Mentorship Program, an international training and education for women to increase their participation in climate change adaptation, and a Central American Gender Assessment Consultant.

Rollins also rescinded all DEI programs, including 948 employee trainings focused on DEI, Environmental Justice, and gender ideology.

The Department is pursuing an aggressive plan to “optimize its workforce by eliminating positions that are no longer necessary, bringing its workforce back to the office, and relocating employees out of the National Capital region into our nation’s heartland to allow our rural communities to flourish,” she said.

On her second (Feb. 15), Rollins met with farmers at the Championship Tractor Pull in Kentucky, then traveled to southwest Kansas Monday (Feb. 17) to tour dairy and beef operations and have a producer roundtable with Senator Roger Marshall, M.D., prime sponsor of the Whole Milk for Healthy Kids Act in the U.S. Senate.

Reform of the Dietary Guidelines was mentioned in a tweet from these discussions, something Secretary Rollins will work on jointly with HHS Secretary Robert F. Kennedy Jr., also confirmed Feb. 13 in a narrow Senate vote.

At the Top Producer Summit in Kansas City, Mo., Tuesday, Feb. 18, Rollins addressed expanding trade access and cutting regulatory red tape for farmers. She also announced looking toward federal policy to prevent China from buying U.S. farmland.

USDA Secretary Rollins was also appointed this week by the Trump Administration to work together with National Economic Council Director Kevin Hassett — collaborating with scientists and global experts — to spearhead a new avian influenza strategy that moves away from mass euthanization of infected poultry flocks to prioritize enhanced biosecurity measures and medication to control spread.

Editorial Analysis: Tumultuous 2024 spills over into 2025 – Part Three

By Sherry Bunting, Farmshine, February 7, 2025(updated with additional information after print edition published)

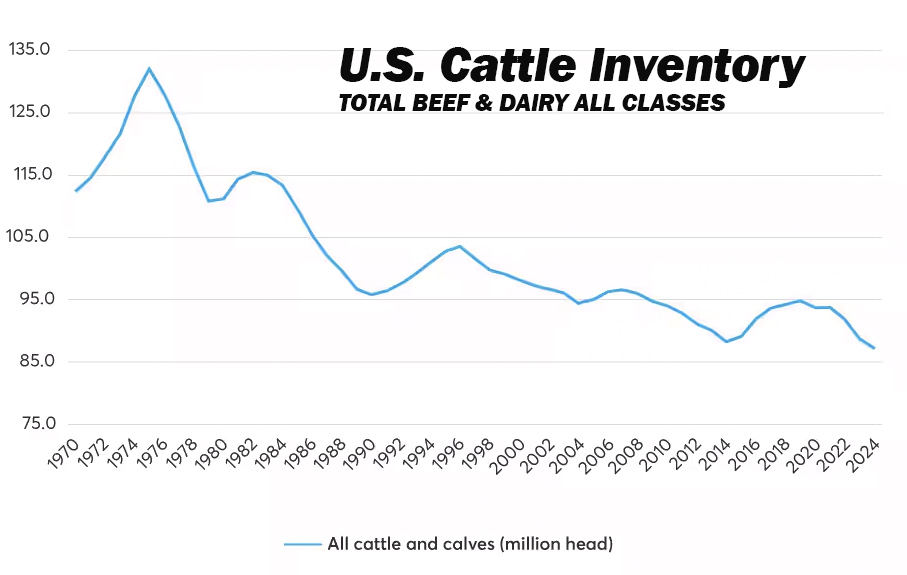

EAST EARL, Pa. – A tumultuous dairy and beef market in 2024 is bound to be even more so in 2025. The long-awaited Jan. 1 Cattle Inventory Report is in, and we all saw the kerfuffle about tariffs and trade this week.

The bottom lines are…

— The U.S. beef cow herd continues to shrink, while both the beef and dairy heifer replacement numbers are notably smaller, signaling less domestic beef production and stable, if not reduced milk production in the face of strong domestic demand for beef and dairy products.

— U.S. import volumes of live feeder cattle as well as beef and dairy products have climbed over the past five years.

— Uncertainty prevails about U.S. trade policy, but export volumes of beef and dairy have leveled off already in the past several years. Dairy exports are bound to get a boost in the short-term as U.S. prices are mostly trailing current global prices. Tariffs on Canada and Mexico and potential retaliations are paused.

— Will the dairy herd continue maintaining itself at these shrinking heifer ratios now that we are five years out from the time of plentiful heifers.

Report highlights include…

Milk cow inventory has remained relatively stable over the past five years, ranging from 9.34 million head on Jan. 1, 2020 to the 5-year high of 9.45 million head on Jan. 1, 2021, then back down to just shy of 9.35 million head on Jan. 1, 2024 and Jan. 1, 2025. However, the number of dairy replacement heifers has dropped by 16% over the past five years from 4.61 million head on Jan. 1, 2020 to 3.91 million head on Jan. 1, 2025. This number is down almost 20% — or nearly 1 million head — from the record high 4.81 million dairy replacement heifers recorded on Jan. 1, 2016.

Are milk cows milking longer? Is the average dairy cow getting 16 to 20% more productive life (an additional half lactation)? Is the age at first calving continuing to decline, and are herd culling rates also declining significantly enough to maintain the current cowherd size on 16 to 20% fewer heifers expected to calve vs. 5 and 10 years ago?

According to the Jan. 1, 2025 Cattle Inventory Report, there are not quite 27 heifers expected to calve this year for every 100 cows in the current U.S. dairy herd, and a national cull rate of 29% based on January through December 2024 dairy cow slaughter totals. Five years ago, there were just over 31 heifers expected to calve for every 100 milk cows in the similarly-sized U.S. dairy herd.

Will these trends collide at the 5-year mark this year, given the average productive life of a dairy cow based on the most recent data (2020) is not quite three lactations or roughly 5 years of age? How will the $5 to $10 billion in new processing capacity be filled, or will we see existing plant closures in their stead? Are the investor dairies that put up 10, 20, and 30,000 cow facilities each year filling new barns with milking animals raised on their own calf ranches coming in under the reporting-radar of USDA NASS? Or is the pace of dairies exiting the business on one end mirroring the growth on the other end?

One inescapable conclusion is that the milk cow herd remains relatively stable, while the dairy replacement heifer numbers have shrunk by 16% vs. five years ago and by 20% vs. 10 years ago, and the record-high prices paid for dairy replacements is proof of tight supplies.

This is part three in a four-part series. Part one was published Jan. 3, 2025; Part two on Jan. 17, 2025.

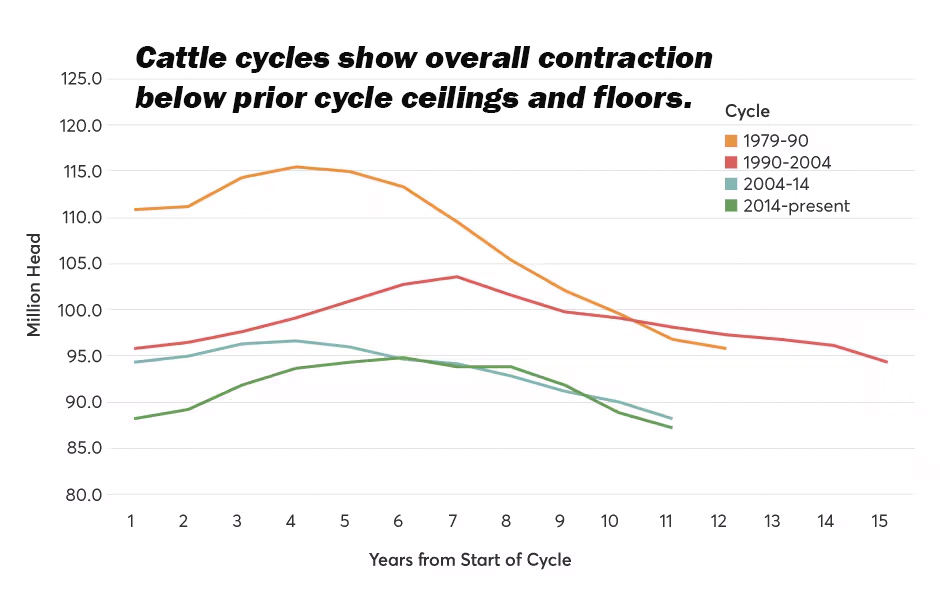

CME graph using USDA NASS Inventory data

U.S. cattle herd down… again

U.S. total cattle numbers on Jan. 1, 2025 are down 1% year-over-year (YOY), according to the All Cattle and Calf Inventory Report released by USDA on Fri., Jan. 31st.

At 86.66 million, the report counted 500,000 fewer head than last year’s total, which was already the smallest in 74 years (Jan. 1, 1951).

The total number of all cows and heifers that calved is down 0.4% YOY at 37.21 million head. That is 147,000 fewer beef and dairy cows on farms as compared with the revised-lower totals a year ago, which were already the smallest in 84 years (Jan. 1, 1941).

The total number of all heifers over 500 pounds on Jan. 1, 2025 (including heifers destined to become beef) was down 1% YOY at 18.18 million head. That’s 140,000 fewer head counted than on Jan. 1, 2024, which was already the smallest total heifer number in 34 years (Jan. 1, 1991).

In the Jan. 1, 2025 report, USDA NASS revised-lower its Jan. 1, 2024 and July 1, 2023 estimates of total animals that had calved, as well as the calf crop in those 12 to 18 month prior Inventory Reports. Statisticians went back and compared the prior estimates to the official slaughter data, the import and export data, and the relationship of this new survey information to the prior surveys.

This means the Jan. 1, 2025 numbers are now estimated at levels below the revised-lower prior reports that had already set records! (A mid-year 2024 inventory would have been helpful, but was canceled by former Ag Secretary Tom Vilsack, claiming insufficient USDA funds).

Chart compiled by S. Bunting with USDA NASS Inventory data

Milk cows flat, heifers shrink

The number of milk cows on Jan. 1, 2025 was essentially unchanged vs. year earlier, up only 2,500 to just shy of 9.35 million head.

However, the dairy replacement heifer total is down 1% YOY at 3.91 million head. At this rate, the number of heifers heading to careers as milk cows is 16% below the 5-year comparison on Jan. 1, 2020.

At 3.91 million head, there are 37,000 fewer dairy replacement heifers than a year ago, which was already the smallest number of dairy replacement heifers in 47 years (Jan. 1, 1978).

As the graph above illustrates, milk cow numbers have held relatively stable over the past five years, while the number of dairy replacement heifers has significantly declined. Are cows experiencing longer productive life? Or are the multi-site investor dairies filling their own expansion sites via their own calf ranches, and escaping the USDA reporting radar?

According to the most recent data (2020), average dairy cow productive life in the U.S. is just shy of three lactations, roughly five years of age. With the number of dairy replacement heifers declining 16% over the past five years, will these two trends collide in the next 12 to 24 months to reduce the U.S. milking herd while escalating the already record high dairy replacement cattle prices? And, what role might HPAI H5N1 play as longer term impacts emerge?

USDA NASS reports that the average auction value of ‘average’ milking cows has increased by nearly $800 per head to $2650 for 2024 vs. $1890 for 2023; $1100 per head higher vs. the $1720 average for 2022; and double (+$1300) the average value reported at $1350 and $1300 per head four and five years ago for 2021 and 2020, respectively.

The average cost to raise dairy replacements has been estimated at $1700 to $2400 per head, which means the value of ‘average’ replacement heifers at $1720 to $2660 from 2022 to 2024 is finally starting to mirror the cost to raise them — on average.

Many dairy producers continue producing only the heifers they need, which is reducing the availability of heifers in the marketplace for those wanting to expand.

Producers continue to respond to the lure of the 3-day-old dairy-on-beef crossbred calves offering substantial margins of $800 to $1000 per head — with no investment, no rearing, no revenue-wait, and no risk.

Basically, a dairy cow can produce $800 to $1000 in revenue for the dairy as soon as she drops a live crossbred calf, no matter what the milk price or margins are doing, and with her whole lactation in front of her.

The Jan. 1 Inventory Report shows the U.S. beef herd continues to shrink, suggesting beef-on-dairy crossbreds will continue to offer bigger per-head margins than growing extra dairy heifers to sell as herd replacements — unless they are premium dairy heifers.

Expanding dairies are having to really plan ahead to raise the animals they need for growth or scramble to get them. Additional upward price momentum may be seen on dairy replacements in the next 12 to 24 months as the more abundant heifers available five years ago ‘age-out’ of the system, statistically speaking, at five years old, which is the industry average age of a milking cow in the U.S.

With the Jan. 1, 2025 U.S. milking herd holding steady at a level that is 1.1% smaller than it was in 2021, the expanding dairies are buying up the herds of the exiting dairies at high prices that make dairy farmers think about selling the cows and hanging on to the heifers, for now, if they do not have a next generation to continue the dairy.

Turnover of existing Holstein herds to include other breeds is also occurring, along with genetic improvement within the Holstein breed, as producers work to raise heifers that calve into the milking herd at younger ages, produce more component yield per hundredweight of milk, have improved productive life traits and fewer days open for a tighter average calving interval.

With a 2024 national dairy herd of 9.35 million milk cows and a 2024 national dairy cow slaughter of 2.726 million, the national culling rate last year was 29%. At that rate, even if the average age at first calving is 22-months, the U.S. dairy industry would need 28 dairy heifers to calve successfully in the next 12 months for every 100 milk cows — just to maintain the current size of the U.S. dairy herd.

According to the Jan. 1 Inventory Report, there are 2.5 million dairy heifers expected to calve in 2025 (down 0.4% or -9000 head). This calculates to 27 (actually 26.75) dairy replacement heifers expected to calve in 2025 for every 100 cows in the U.S. dairy herd as of Jan. 1st.

In 2016, when dairy replacement heifer numbers reached their peak at 4.81 million head, 3.11 million head were expected to calve that year, and the total U.S. dairy cow inventory was 9.31 million head, meaning there were 31 heifers expected to calve for every 100 cows in 2016. This has steadily eroded in part because dairy producers have stopped spending the money to grow extra heifers that were worth less than the cost to grow them until this year. They also worked to reduce age at first-calving, days open across the herd, higher component levels in the milk, reduced death loss, longevity, and began gradually re-introducing beef crossbreeding, which has become a pretty big deal over the past five years.

Some parts of the country are down significantly in heifer replacements as of Jan. 1, 2025, while others are up. For example, Pennsylvania has 15% more dairy replacement heifers on farms vs. year ago.

These estimates indicate milk production will be flat to lower for the next 12 to 24 months.

What this does not account for is the increasing milk component levels generating more dairy products per 100 pounds of milk and the increasing volume of dairy imports, particularly cheese, butter, and whole milk powder. But those increases can only do so much in the face of $5 to $10 billion in new processing assets coming online in the next 6 to 18 months.

CME graph using USDA NASS Inventory data shows continued overall contraction of total cattle inventory as new cycles mostly fail to breach prior cycle ceilings, floors, and midpoints.

Beef herd shrinks more

The Jan. 1 Inventory shows the U.S. beef herd continues to shrink. At the national level, there are no signs of rebuilding, as the total number of heifers heading to careers as beef mama cows is down 1% YOY. However, in some parts of the country, such as Virginia, more heifers were retained as beef cow replacements and fewer were earmarked for feedlots.

At 4.67 million head, there are 46,000 fewer beef replacement heifers in the U.S. vs. year ago, setting another record low as the smallest number since 1948.

Even more striking is the beef replacement heifers that are expected to calve in 2025 are down a whopping 2% YOY (-50,000) nationally.

Meanwhile, the beef-on-dairy feedlot placements, while a growing segment of the beef industry, are not enough to reverse the downward beef production trend as evidenced by declines in the number of animals over 500 pounds on Jan. 1st heading to feedlots: Steers and bulls are both down 1% (-157,000 and -21,000 head YOY, respectively). Heifers over 500 pounds heading to feedlots are down 0.6%, and the number of cattle on feed as of Jan. 1, 2025 is down 1% YOY at 14.3 million head (-130,000 head).

The Inventory Report came on the heels of the January Cattle on Feed Report, which showed 3% fewer feedlot placements as of Jan. 1, perhaps because of the Mexican border closure to the live cattle imports, due to concerns about transmission of the screw-worm parasite.

Even the total number of all calves (heifers, bulls and steers) weighing under 500 pounds dropped 1% lower YOY at 13.46 million head (-30,000).

These estimates suggest domestic beef production will decline for at least the next 12 to 24 months, maybe longer.

What this does not account for are the number of live cattle crossing the border into U.S. feedlots from Mexico and Canada and the increasing amounts of beef the U.S. imports from other countries, including from Canada, Mexico and South America.

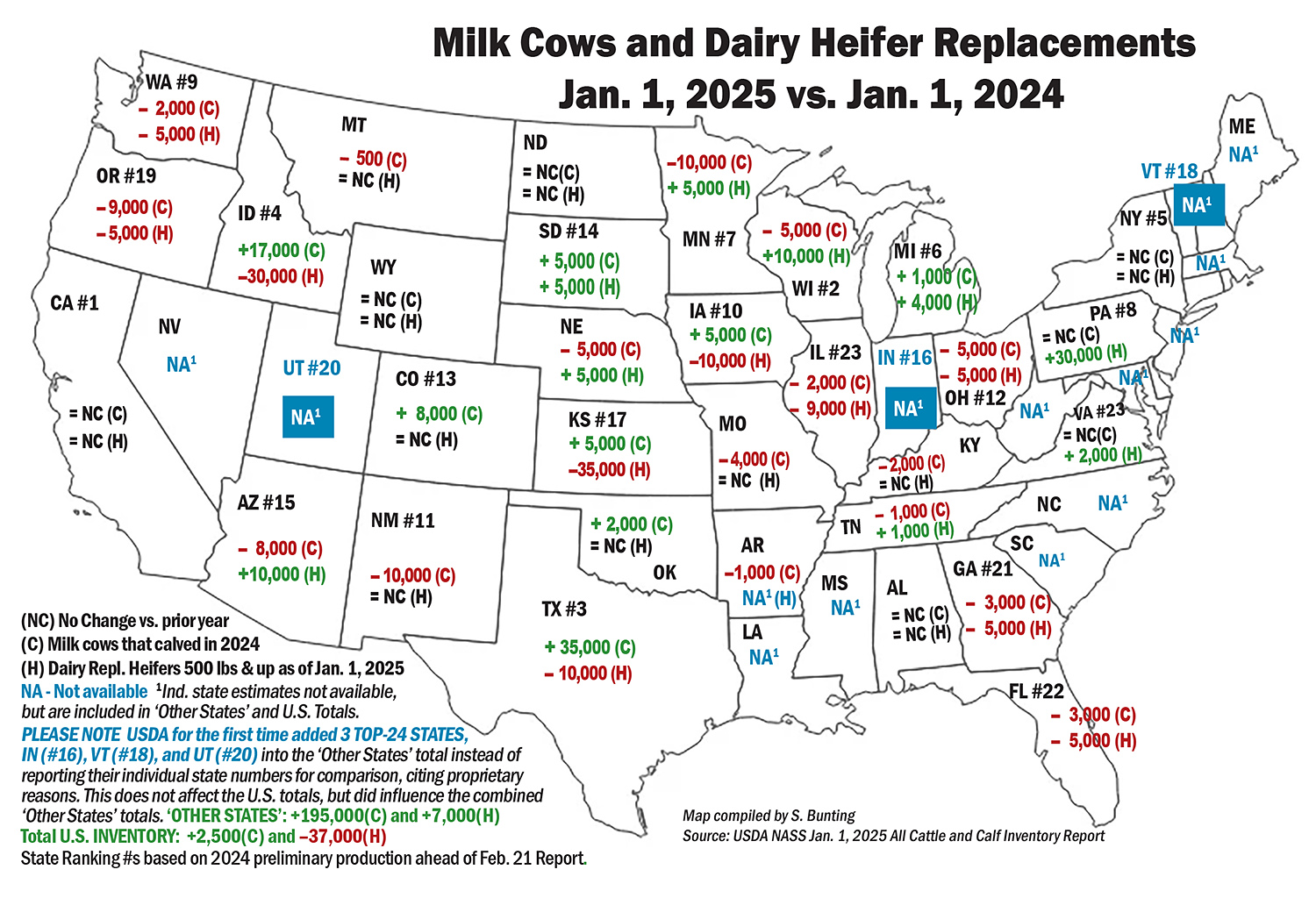

Map compiled by S. Bunting with USDA NASS Inventory data

Significant geographic dairy shifts

Breaking the dairy inventory numbers apart, we see big geographic shifts.

The West added 78,000 more milk cows in 2024 vs. 2023, except for California’s numbers being unchanged. On the other hand, the East and Upper Midwest had equal or fewer milk cows, down collectively more than 75,000 head YOY, except Michigan was up just 1000 head.

The biggest 2024 gains were tallied in Texas, up 35,000 head, and Idaho, up 17,000 head. Colorado grew by 8,000 head; Iowa, Kansas and South Dakota by 5,000 each; and Oklahoma by 2,000.

The biggest milk cow declines were in Minnesota and New Mexico, down by 10,000 head each; Oregon down by 9,000; Arizona by 8,000. Wisconsin, Ohio, and Nebraska by 5,000 each; Missouri by 4,000; Florida and Georgia by 3,000 each; Illinois, Kentucky, and Washington by 2,000 each; and Tennessee by 1,000. Smaller unranked states collectively accounted for the remainder of milk cow losses.

Interestingly, USDA pulled three Top-24 Milk Production States into the ‘Other States’ category, choosing not to report their cow and heifer numbers for proprietary reasons. They are Indiana (#16), Vermont (#18) and Utah (#20). Thus the ‘Other States’ category saw an increase of 195,000 cows simply because these three Top-24 states were included anonymously in the total.

The geographic breakdown is interesting when it comes to dairy replacement heifers as the growth is noted in the areas where the cow numbers have declined and vice versa. These shifts could reflect changes in the way heifers have tended to move across state lines for rearing, especially in light of the dairy-adapted B3.13 strain of HPAI H5N1.

Pennsylvania is the biggest outlier as the cow numbers are unchanged YOY, but farmers reported 30,000 more dairy heifers in the Commonwealth on Jan. 1, 2025 vs. year ago.

Elsewhere in the East, Virginia dairy heifer replacements are up 2,000 head; Tennessee up 1,000 head; New York and Kentucky unchanged; Georgia and Florida down 5,000 head each. Again, the ranked states of Indiana, Vermont and Utah had their replacement heifer numbers lumped into the ‘Other States’ category, which consequently showed a gain of 7,000 heifers vs. year earlier when those states were not included in that category.

Beef replacement heifers and feedlot heifers are down a combined 10,000 head in Pennsylvania, while Virginia showed signs of beef herd rebuilding, reporting 4,000 more beef replacement heifers and 4,000 fewer heifers heading to feedyards.

Looking at the Mideast, Michigan had 5,000 more dairy heifer replacements, while Indiana’s numbers were unreported. Ohio is down in dairy heifers by 5,000 head. Beef replacement heifers in that region are up by 7,000 head and feedlot heifers are up by 3,000 head.

The Upper Midwest grew their dairy replacement heifer numbers, while the West significantly decreased them. Wisconsin is up by 10,000 head YOY; while Minnesota and South Dakota grew by 5,000 head each.

In the West, the following states with significant growth in milk cow numbers had significant losses in dairy replacement heifer numbers: Kansas down a whopping 35,000 head in dairy replacement heifers; Idaho down by 30,000 head; Texas, Pacific Northwest and Iowa down 10,000 each. Dairies in Kansas, Idaho, Texas, and Iowa contended with avian influenza in 2024.

Meanwhile, in California, New Mexico, and Colorado (all three having dealt with H5N1) the number of dairy replacement heifers was reported as unchanged YOY, but Arizona, which has not had H5N1, grew its dairy heifer numbers by 10,000 head.

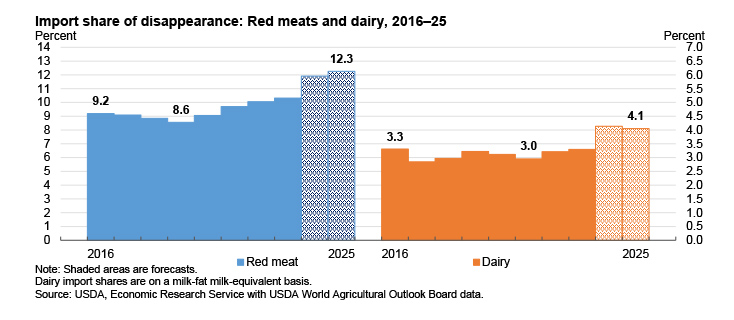

USDA Economic Research Service graph

Trade is uncertain(Imports up, Exports leveling off)

Dairy and beef imports are growing, and the industry is responding to ‘tariff talk’ with statements showing fear of trade wars harming farmers or possibly gaining concessions in the context of Agriculture’s current annual trade deficit of $45.5 billion.

On Friday, Jan. 31, the spot cheese and Class III milk futures markets plunged lower in response to U.S. tariff announcements of 25% on goods from Canada and Mexico and 10% on goods from China.

This fear was short-lived, however, because the planned tariffs on goods from Canada and Mexico were promptly paused three days later on Monday, Feb. 3, when leaders agreed to support and combine efforts on U.S. border security, while putting teams together with the pledge to work through U.S. trade issues over the next 30 days.

The announced 10% tariffs on China went into effect Feb. 4, but discussions between the U.S. and China are said to be resuming for phase one of the trade deal struck in the prior Trump Administration just before the Covid pandemic hit globally.

Meanwhile, the total volume (not value) of dairy exports has leveled off on a total solids basis in the past two to three years as the U.S. exports more cheese and less skim milk powder and much less whey – the latter because we domestically produced less commodity SMP and far less commodity dry whey in 2024. Inventories are down for both, meaning domestic demand is using what is produced.

On the flip-side, the U.S. imported more cheese, butterfat, and whole milk powder during the first 11 months of 2024 YOY.

We will take a closer look at the trends in U.S. dairy farm numbers, production, and trade after final 2024 trade and production data are released in late February, and with more information, perhaps, on how U.S. agricultural trade policy may be shaping up for 2025.

Whole Milk for Healthy Kids Act reintroduced in style!

‘Most nutritious drink known to humankind’ takes center stage at Ag Secretary confirmation hearing

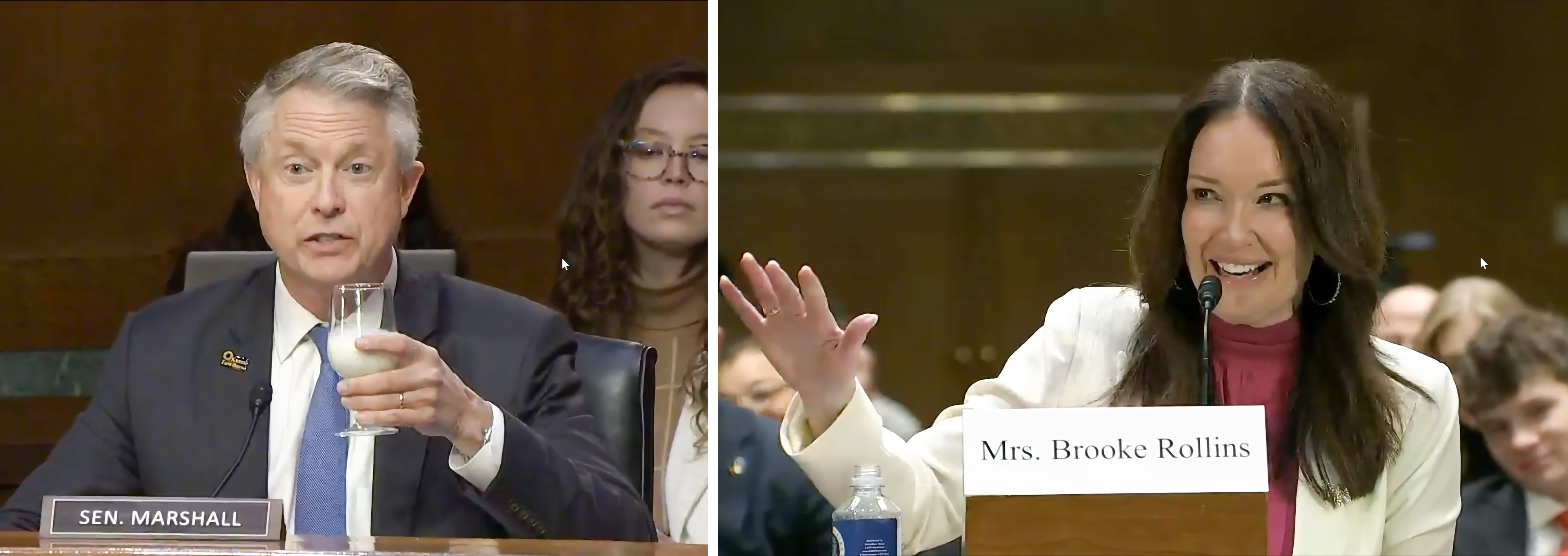

This split-screen moment captures Sen. Roger Marshall, M.D. and Agriculture Secretary Nominee Brooke Rollins during their confirmation hearing exchange on bringing whole milk choice back to schools. Sen. Marshall always comes prepared with THE MILK! Livestream screen capture by Sherry Bunting

From grassroots volunteers to halls of Congress, ‘hat’s off to 97 Milk’

WASHINGTON, D.C. – It was the high point of the four-hour confirmation hearing on Jan. 23rd for President Trump’s Ag Secretary nominee Brooke Rollins, when Senator Roger Marshall, MD (R-Kan.) poured himself a glass of whole milk in front of the television cameras, and said:

Ms. Rollins, welcome. I want to know if you agree with me that whole milk is the most nutritious drink known to humankind and belongs in our school lunches.”

He then promptly took a big swig of nature’s nutrition powerhouse that American children have been banned from consuming at school meals since 2012.

Yes, there was a ripple of good-natured laughter throughout the room at the absurdity of it all – the absurdity that this nutrition powerhouse has actually been banned for 13 years on school grounds to even be bought with one’s own money from midnight before the start of the school day to 30 minutes after the end of the school day, per the 12-years of King Vilsack that Secretary Perdue’s interruption even failed to overturn.

The new Ag Secretary nominee Rollins responded with a hand motion to her mother two rows back among the family, friends, colleagues, ag teacher, fellow former FFA state officers and current little league team she coaches in attendance for the confirmation hearing, as she replied with a hearty and all-too-knowing laugh:

“Senator, I don’t know that you have met my mom – yet. But this is all we had in our refrigerator growing up – not anything else – just whole milk. She is absolutely never going to let us forget this – the fact that this is coming up! But yes, this hits home to me very quickly,” said Rollins.

On the very same day, whole milk champion U.S. Representative Glenn ‘GT’ Thompson (R-Pa.) with prime cosponsor and pediatrician Rep. Kim Schrier (D-Wash.), along with Senator Marshall and prime cosponsoring Senators Peter Welch (D-Vt.), Dave McCormick (R-Pa.) and John Fetterman (D-Pa.) led the re-introduction of the bipartisan, bicameral Whole Milk for Healthy Kids Act of 2025, known as H.R. 649 in the House with 90 total cosponsors to-date, and S. 222 in the Senate with 12 total cosponsors to-date.

The bill in its fifth attempt will allow unflavored and flavored whole (3.25 to 3.5% fat) and reduced-fat (2%) milk to once again be offered in school cafeterias, which are currently only permitted to have fat-free and 1% milk available for growing children, much of which is shunned or thrown away.

“Federal policy, based on flawed, outdated science has kept whole milk out of school cafeterias for more than a decade,” said Rep. Thompson in a Jan. 23rd press statement. “Milk provides 13 essential nutrients for growth and health, two key factors contributing to academic success. The Whole Milk for Healthy Kids Act of 2025 provides schools the flexibility they need to offer a variety of options, while supporting students and America’s hard-working dairy farmers.”

“As a pediatrician, I know how important a balanced and nutritious diet is for children’s health, well-being, and development,” added Rep. Schrier. “A healthy diet early in life leads to proper physical growth and improved academic performance and can set the foundation for lifelong healthy eating habits. Milk contains essential nutrients… This bill simply gives schools the option of providing the types of milk most kids prefer to drink.”

Sen. Marshall was blunt, saying, “(It) should never have been excluded from the National School Lunch Program. Now, 13 years after its removal, nearly 75% of children do not receive their recommended daily dairy intake. I believe in a healthier future for America, and by increasing kids’ access to whole milk in school cafeterias, we will help prevent diet-related diseases down the road, as well as encourage nutrient-rich diets for years to come.”

“Milk provides growing kids with key nutrients they need. Dairy is also an important part of Vermont’s culture and local economy, which is why our bipartisan bill to expand access to whole milk in our schools is a win for Vermont’s students and farmers,” said Sen. Welch.

Sen. McCormick said the bill “puts milk back in schools that growing kids actually want to drink. Pennsylvania’s dairy farmers supply this country (with it)… allowing schools to serve (it) in the lunchroom is just commonsense.

“Kids need it,” said Sen. Fetterman. “Let’s give them the option to enjoy whole milk again in schools – it’s good for them, they’ll actually drink it, and it supports our farmers. This bill is a simple solution that benefits everyone.”

Both National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) rushed to the forefront singing the bill’s praises and promptly issuing press releases, something that in past attempts took a little time.

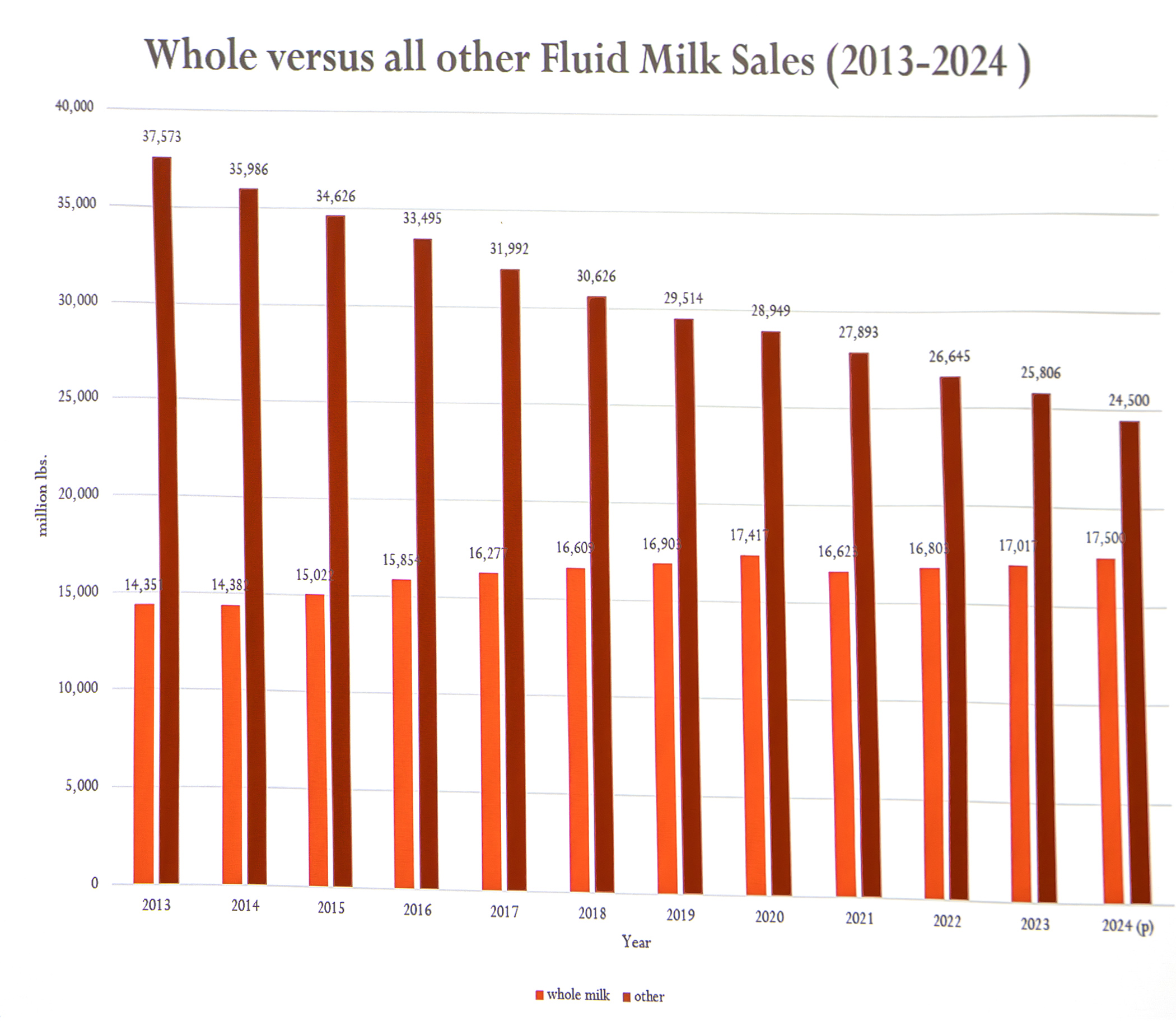

As longtime milk market guru Calvin Covington noted at the R&J Dairy Consulting seminar in eastern Lancaster County Jan. 28th, kudos go to the grassroots efforts. He showed the increase in whole milk sales nationally, while other fluid milk categories have declined. This has somewhat stabilized the steep losses the entire fluid milk category has suffered most steeply in the past 14 years.

“My hat’s off to all of you and what you have done here in Pennsylvania, throughout the state and country, in promoting whole milk. I just wish other dairy farmers would be grassroots like you are and get involved,” said Covington. “Your work has paid off. Look at this graph. In 2013, whole milk sales were a little over 14 billion pounds. Last year (2024 with 11 months of data) I’m estimating 17.5 billion pounds. Whole milk is coming up, and everything else is going down.”

Covington dug into the graph (above) further to show that in 2019, the amount of whole milk sold was 16.9 billion pounds. “But look what happened in 2020, it jumped up to 17.4 and then back down to 16.62 in 2021. That was the pandemic. People were home. Schools were closed,” he said.

“When they were home, they drank good-tasting milk, but unfortunately when the schools opened back up, they had to go back to the other stuff. But my hat’s off to what you’ve done here. We’re selling more whole milk, and one thing people forget is that 100 pounds of Class I milk sales with higher fat content — last year it averaged 2.4 in this market compared to what it was 15 years ago when it averaged less than 2% — the more fat sold in Class I milk, the more income for you as dairy farmers. Class I butterfat is worth more than butterfat in the other markets, so my hat’s off to what you’re doing.”

(Author’s Note: Yes, Covington is speaking of the good work, the hard work, of 97 Milk volunteers who formed the non-profit in 2019 after dairy farmer Nelson Troutman’s painted bales began appearing. This good work is sustained by a handful of volunteers and donations. Just think what could be accomplished with more involvement. One of those volunteers is Jackie Behr of R&J, who puts her marketing skills to work for 97 Milk. She reminded farmers that donations are needed to keep the milk education movement going. An Amish Wedding Feast fundraiser is scheduled for Feb. 8 at Solanco Fairgrounds, with sponsorships still available. The next 97 Milk meeting open to all dairy farmers is March 25 at Durlach-Mt. Airy Fire Hall near Ephrata, Pennsylvania. Check out 97milk.com to learn more about the milk education movement, and hit the donate tab to find out how you can help.)

SAVANNAH, Ga. – Flat milk production volume, but with higher components, and a more unpredictable demand are factors new to the dairy industry that make price projections more difficult for the year ahead.

Calvin Covington has spent his life in milk marketing, now retired from managing Southeast Milk Inc., and before that working with cheese processors to see (and pay) the value of higher protein and fat when he was with the American Jersey Cattle Association earlier in his career.

Covington gave his dairy outlook for 2025, with emphasis on the Southeast markets during the Georgia Dairy Conference attended by over 400 in Savannah, Jan. 20th.

“I was way low on my projections last year. 2024 ended up with prices higher than anticipated,” he said.

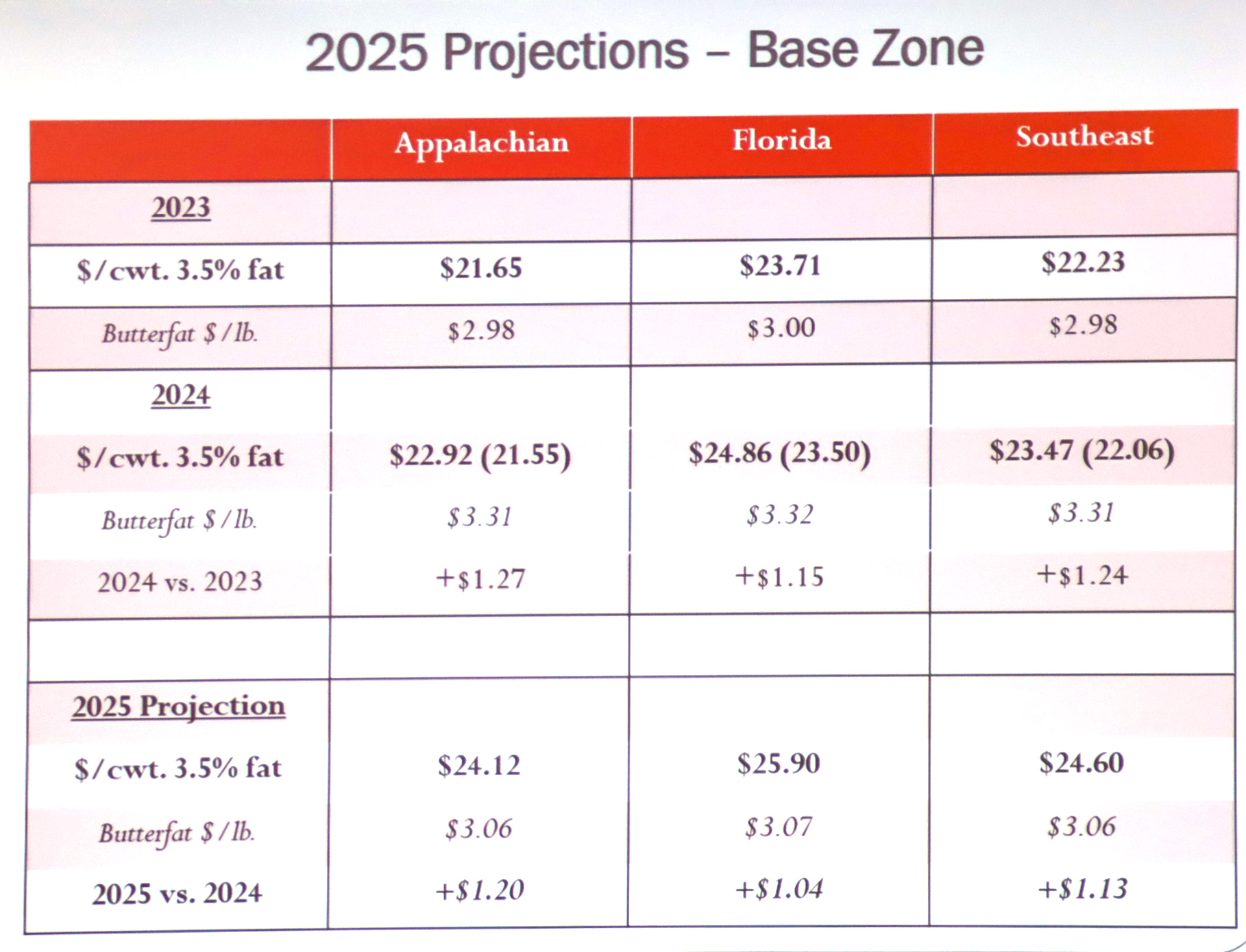

This year, he is projecting prices in the Southeast markets to rise by $1.20 per hundredweight as an average for 2025 vs. 2024 in the Appalachian region ($24.12), $1.40 in Florida ($25.90) and $1.13 in the Southeast Order ($24.60). Most of the increase will come from the skim side this year because the FMMO changes, which will be implemented in the second half of 2025, will pressure butterfat value.

Covington shared his price projections for Southeast milk markets for 2025.

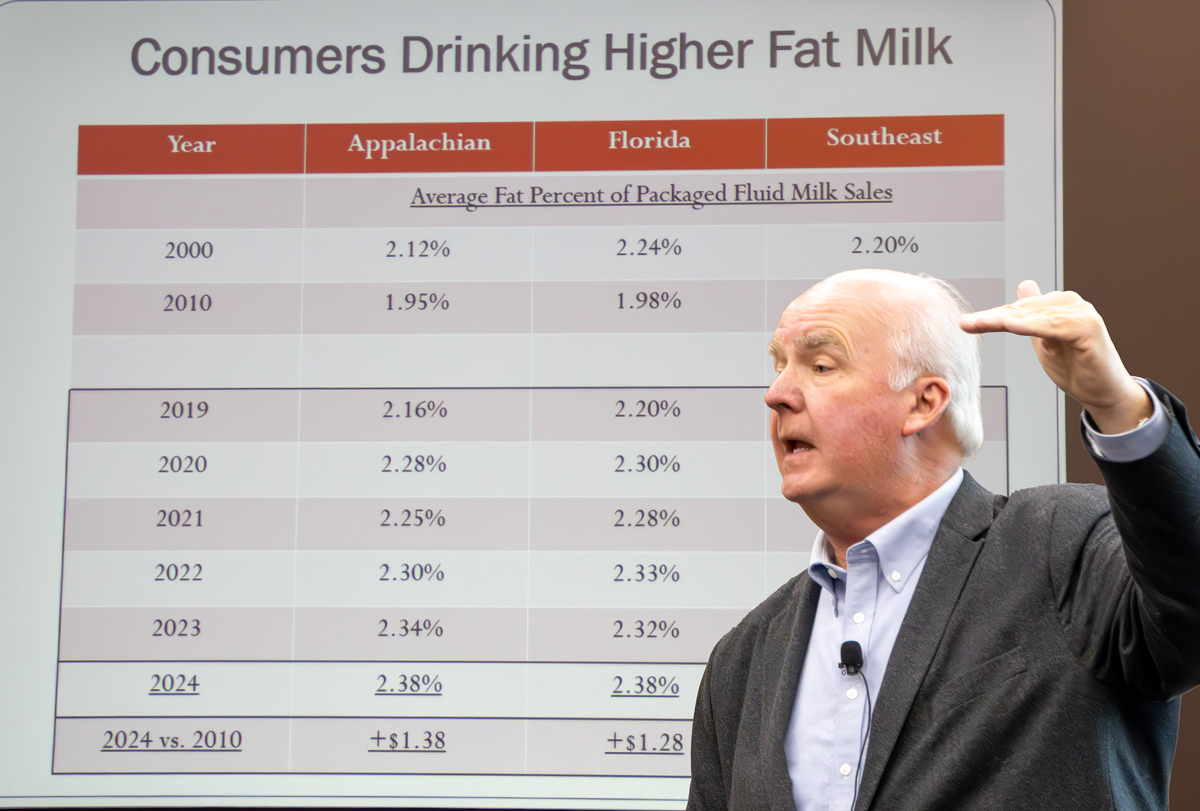

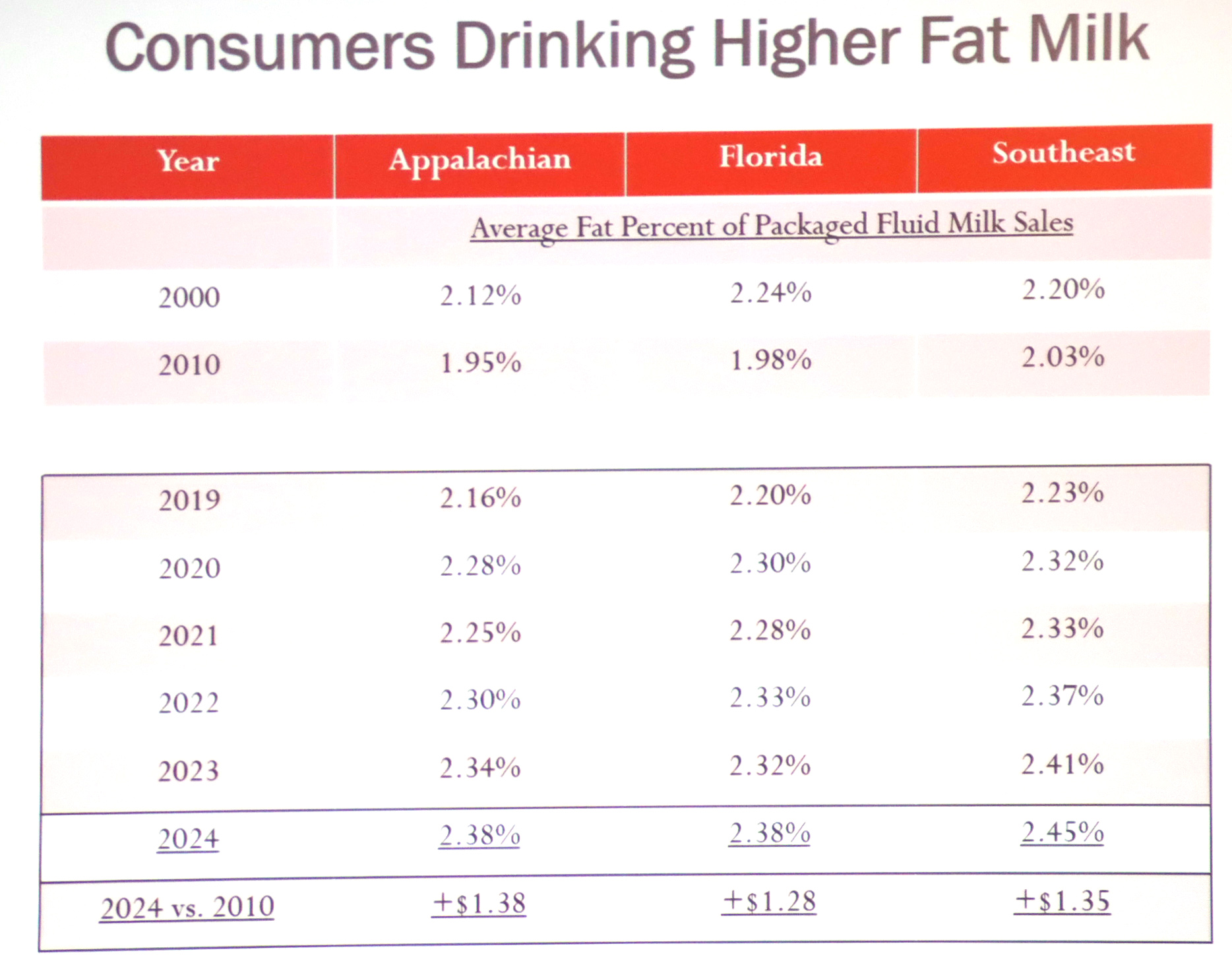

Producers are making higher butterfat milk, averaging well over 4.0% across the three Southeast Orders at 4.06 in Appalachian, 3.92 in Florida, and 4.11 in the Southeast. This compares with 3.65% across the three Orders in 2010.

“Additionally, consumers are also drinking higher fat milk,” said Covington, calculating the average fat percentage of Class I sales in the three Southeast Orders rose from 1.95% in 2010 to 2.4% in 2024.

Covington calculated that fat percentage in milk sales showing the change in consumer preference for higher fat milk puts more money in producer milk checks.

“In 100 pounds of Class I milk in the Appalachian Order, for example, that 2.38% fat made the milk worth more money, $1.38 per cwt more,” he said, with a chart showing Southeast producers saw a $1.28 benefit; Florida $1.35.

“There has been a big change in consumer preference, and that has raised your Class I price,” he said.

He commended dairy producers for improving their components, which has also improved their milk price.

“You’ve done this through genetics and feeding and nutrition programs, and it’s not going to stop. We are moving quickly to Holsteins making milk like Holsteins and testing like Jerseys.”

Other good news heading into 2025 is dairy product inventories are in good shape, he said. Cheese stocks are down, powder is up just a small amount, dry whey inventory is way down and butter inventory is flat.

Dairy product demand is up, but Covington sees a bit of a challenge looking at demand on a total solids basis because “we are exporting more cheese and less powder.”

Looking ahead, he gave attendees a lot to think about on the changing structure and markets in the dairy industry.

Covington observed that 10% (140) of the 1408 dairy farms that were counted in the 2022 Census of Agriculture in the Southeast had 64% of the region’s milk sales.

Of that 140, there were 22 farms with 2500 cows or more, producing 32% of the region’s milk.

“This is happening all over the country,” said Covington. “We are getting more concentrated.”

This year the milk production advantage flipped back to Florida by slightly more than Georgia, but the two states together have reached 50% of Southeast milk sales. Covington thinks by 2030, “we will see 60% of the milk produced in the Southeast coming from Georgia and Florida.”

When asked what has led to Georgia’s rapid increase in production over the past few years, Covington said “Georgia dairy farmers want to expand and they have the ability to expand. They are progressively making more milk per cow and have the land mass and support.”

His “demand and supply” summary for the Southeast region shows 1160 dairy farms at the end of 2024, producing 8 billion pounds of milk with 32 regulated milk plants. The region had 8.3 billion pounds of Class I fluid milk disposition, and 0.9 billion pounds of Class II products processed.

Against those numbers, the amount of packaged fluid milk products sold in the Southeast was 10 billion pounds. “The Southeast is still a deficit area, and there is room for growth,” he said.

As for total U.S. milk production, Covington doesn’t see it rebounding any time soon. Cow numbers are moving lower and milk per cow is simply not making the year over year gains seen in the past.

“Milk production has been pretty constant for the last three years,” he said. “We have to go way back to see where that has happened before.”

But he also wanted producers to think differently about production, to realize that in making more components, their milk is generating more products. He calculates that today’s hundredweights of milk, nationwide, yield a half pound more cheese. That adds up.

“You as dairy farmers are doing this. By getting your components up, you are also improving sustainability over time. You are making more products from the same volume of milk,” Covington explained.

“Based on average component level changes, if a plant is making one million pounds of cheese a day, they now need 177 loads instead of 185 loads a day for that same output,” he said.

Brooke Rollins, photo courtesy America First Policy Institute

Bringing whole milk choice back to schools could align with Rollins’ and Kennedy’s priorities

By Sherry Bunting, Farmshine, November 29, 2024

WASHINGTON, D.C. – President Elect Donald Trump has nominated Brooke Rollins of Fort Worth, Texas to be the 33rd U.S. Secretary of Agriculture. She would be the second woman to serve in the top USDA post, the first being Ann Veneman in 2001 under President George W. Bush.

Trump’s announcement Saturday, Nov. 23 brought ripples of surprise across ag media outlets after many had floated a long list of other names under consideration.

In the end, it came down to Rollins, a lawyer and trusted advisor who previously served on Trump’s 2016 Economic Advisory Council as well as Director of Domestic Policy Council and Assistant to the President for Strategic Initiatives in Trump’s first term.

Rollins has spent the past four years as founder and CEO of the America First Policy Institute (AFPI). Trump highlighted her commitment to American farmers, food self-sufficiency, and rural small-town restoration.

The AFPI has not had much to say on agriculture, specifically, but has advocated for a ban on China’s ownership of American farmland. Rollins also spoke out against any sort of carbon or methane tax in a 2018 Texas Public Policy Foundation broadcast.

“As our next Secretary of Agriculture, Brooke will spearhead the effort to protect American farmers who are truly the backbone of our country,” Trump stated.

Raised with a generational ranching background in the small town of Glen Rose, Texas, Rollins was involved in 4-H and FFA leadership and credits her high school ag teacher for “changing her life.”

She earned her B.S. in agriculture development at Texas A&M and spent her public policy career in nonprofit and governmental leadership at the state and federal levels.

She and her husband Mark have four teenage children, who avidly show cattle.

While searches for paper or interview trails on her agriculture policy positions come up mostly empty, what can be gleaned is that Rollins has the President-Elect’s ear and a penchant for analyzing issues with an ear to those affected, not just the ‘experts.’

In a post on X (formerly twitter), Rollins thanked Trump for “the opportunity to serve… It will be the honor of my life to fight for America’s farmers and our Nation’s agricultural communities. This is big stuff for a small-town ag girl from Glen Rose, Texas… Who’s ready to Make Agriculture Great Again?”

Ag and dairy organizations responded. Several took the opportunity to also weigh-in on Trump’s nomination of Robert F. Kennedy Jr. a week earlier for Secretary of Health and Human Services with the Make America Healthy Again agenda.

The two departments jointly issue the Dietary Guidelines for Americans (DGAs) every five years, which USDA uses to regulate meals (and milk) served at schools, daycares, and senior centers. A large chunk of USDA’s massive budget and staff administer and regulate nutrition programs.

The next cycle of DGAs is already in process with the two new USDA and HHS secretaries tasked with finalizing the 2025-30 DGAs by the end of next year that will set the rules for schools and other nutrition programs for years to come.

American Dairy Coalition CEO Laurie Fischer observed in a statement that the incoming secretaries will have the opportunity “to fix food nutrition policy, such as a long overdue reform of the Dietary Guidelines that govern school meals where children have been prohibited from choosing whole milk and 2% milk since 2010.”

Grassroots Pennsylvania Dairy Advisory Committee chairman Bernie Morrissey also expressed hope that Rollins and Kennedy, if confirmed by the Senate, will work together to bring the choice of whole milk back to schools.

“For far too long, America’s children have been deprived of the choice of delicious, nutrient-dense whole milk. USDA requires schools to only offer fat-free and 1% low-fat milk. Many children throw that milk away, so they are missing nature’s nutrition powerhouse. Now, more than ever, we need to offer the “good stuff,’” Morrissey stated, adding that “Rollins is a mother, and that helps. We have mothers on our committee and they really get it.”

He explained that his committee includes dairy farmers, allied industry representation, a recently retired internal medicine doctor, school nurse, school foodservice director, and former school board director who have worked on this issue over more than a decade. He wants the incoming secretaries to understand the problem so they can unwind the decades of worsening low-fat rules that pave the way for more ultra-processing leaving children with less nutrient-dense choices and unfavorable nutrition and health outcomes.

“We look forward to working with the next Administration on reforms that allow dairy farmers to market the whole milk they produce and allow children the opportunity to choose milk they will love,” Morrissey added. “Our friends at the 97 Milk organization are doing a wonderful job educating the public. Now, we just need real leaders willing to stand up and roll back the federal ban on whole milk in schools. We are eager to help Make America Healthy Again and Make Agriculture Great Again.”

The International Dairy Foods Association (IDFA) has conducted surveys showing the vast majority of parents want their kids to have the choice of whole milk at school.

In his response to the Rollins and Kennedy nominations, IDFA CEO Michael Dykes, DVM also highlighted the joint nutrition roles of USDA and HHS, citing the need to “enhance the diet quality of Americans, protect the integrity of food production and processing, and establish a regulatory environment that drives innovation and efficiency… to continue leading the world in the production of high-quality dairy nutrition.”

In a follow up interview with ADC, Fischer said dairy labeling integrity is another big issue for dairy farmers in the wheelhouse of both USDA and HHS. “We hope to see the restoration of labeling integrity in the dairy case when it comes to plant-based lookalikes that don’t even come close to real dairy’s nutrition. That includes the regulation and clear labeling of these novel bioengineered fake ‘dairy’ and ‘meat’ lab-created proteins.”

More broadly, she cited the need for real world application of sound farmer-led policy and innovation that meet the realities farmers face daily.

“ADC looks forward to working with the next Secretary on ways to reduce redundancies and wasteful spending to improve efficiency so more of the dollars intended to support farms get to the actual farmers. We are encouraged by Rollins’ history with the Office of American Innovation in Trump’s first term because our farmers are key innovators and lifelong stewards of natural resources,” she said.

As of Nov. 26, National Milk Producers Federation (NMPF) had not yet released a public statement to the media on the nominations of either Rollins or Kennedy, stating simply in a social media post on X: “Congratulations to Brooke Rollins on her nomination to become the next USDA Secretary. Dairy farmers are ready to hit the ground running in 2025!”

National Cattlemen’s Beef Association VP of government affairs, Ethan Lane touted Rollins’ “history of fighting for Main Street and Rural America. America’s cattle producers need a secretary of agriculture who will protect family farms and ranches, roll back crushing regulations, and stand up for rural values.”

American Farm Bureau president Zippy Duvall weighed in, noting the “good relationship” Rollins has with the Texas Farm Bureau: “We hope to build on that. We’re encouraged by her statement that she’d ‘fight for America’s farmers and our nation’s agricultural communities.’ Effective leadership at USDA is more important than ever as farmers and ranchers face a struggling agricultural economy.”

Trump’s cabinet nominations are now complete and require confirmation by the U.S. Senate.

Check out some other interesting perspectives on the next USDA Secretary, pending Senate confirmation.

HARRISBURG, Pa. – Innovation on the dairy farm isn’t just the big investments that come to mind, but a mix of changes and a mindset to improve. Three distinctly different Pennsylvania dairy farms were showcased in a producer panel during the 2024 Dairy Financial and Risk Management Conference hosted by the Center for Dairy Excellence recently.

The audience of mainly ag lenders and industry representatives along with some fellow dairy farmers, had the opportunity to see how producers think through the challenges, progress, and investments, and how they manage their risk in areas such as herd health, feed and nutrition, as well as adversities they can’t control like weather, markets, and labor.

Automation at Oakleigh

For Matt Brake of Oakleigh Farm, Mercersburg, the five-year plan was accelerated in a different direction after a barn fire in December of 2019 forced the family to ask the question whether they would even continue in dairy. No animals were lost, and the 1950s parlor was saved, but they had big decisions to make about the future without a facility.

“We did a lot of praying and had a lot of difficult conversations,” he recalls.

By July 2020, they were milking 120 registered Holsteins with two Lely robots, automated feeding, automated bedding, and retained their preference for a bedded pack barn rebuilt within the existing footprint.

“We really appreciate the cow comfort we get from a bedded pack, and the longevity, which is something we are really seeing now, more than ever,” Brake explains.

They didn’t know — at first – that they would go robotic, but they did know the Lely Vector feeding system would be used for feeding in place of buying a new tractor and mixer and firing it up twice a day.

“It’s amazing to see how all these different pieces of technology play together,” says Brake.

The curtains and fans are all automated and integrated. All data points for the herd are displayed on every single milking. The system ranks cows from zero to 100 on percentage chance of illness, and the automatic sorting for individual attention is based on things like activity, rumination, production, and intakes.

“Everything just plays together in real time, without guessing. We’re still involved as managers, but the data and automation are the tools we didn’t have before. We saw an increase in production, but farming is still farming,” Brake relates, giving examples of ration changes that had to be made with a forage quality issue, and how data systems helped with early detection.

Overall, the animals are doing better in this system, and they are treating fewer cows because they are getting to them earlier.

“It’s really true that an ounce of protection is better than a pound of cure. The quicker we can give those cows the attention, the less likely they are to really nosedive on us,” he says.

Brake sees how automation saves labor in some respects, but it’s more accurate to say that, “With automation, we are better utilizing our skills. We’re able to spend our time better with the cows or focusing on priorities – like chopping corn or getting the alfalfa harvested at the right time.

“We don’t have to stop those activities two times a day or worry about if we have enough help in the parlor, and do we trust that person to stand in the parlor. The robot might ‘call in sick’ temporarily here and there, but in general, compared with some of the employees we’ve had, it’s reliable.”

Moving from just the paper DHIA to incorporating this into the electronic records, changes how they manage culling to be more voluntary than involuntary.

“We can look at space and overcrowding and begin to evaluate cows not just on milk but how efficient they are in the robots looking at deviation from the average with rankings on everything from performance in the robot to reproductive performance and past treatments and other metrics,” he explains.

Better management of the culling decisions also gives them the ability to plan how many heifers to raise. “One of the things we are doing is using more beef semen and using the system to decide who to use it on,” he says.

Renovation at Mount Rock

For Alan Waybright, innovation was the focus when he purchased Mount Rock Dairy from the Mains five years ago near Newville.

A building project was in order to update the over 30-year-old milking systems. About a year ago, they began milking in a 50-stall rotary, which changed the milking time on 2.5 times a day with each milking in a double-12 taking 9 hours, to now milking 4 times a day with each milking taking 3 hours and 45 minutes.

Waybright has been expanding from the 650 cows and 150 bred heifers he brought to Mount Rock from his prior home farm involvement at Mason Dixon, to milking 940 cows today with a 92-pound average, 4.2F and 3.3P.

Automation features were part of the rotary to reduce labor, and the calf barns include the wet barn to get them started before grouping for automatic feeders where they receive four to five feedings a day, resulting in healthier, better growing calves.

With the automated pre- and post-dipper, Waybright says the milking procedure in the DeLaval 50-stall rotary is very consistent, requiring just two employees, the first to wipe and forestrip and the second to dry and attach.

“This is a labor savings, yes, but there have been other benefits for udder health too,” Waybright reports. “When we went from the double-12 where we were hand dipping to the sprayer, a 50-gallon drum used to last seven days, now it’s three days.”

One of the innovative things he has worked on is the use of manure solids for bedding while keeping somatic cell counts low. His system uses two screw-presses dropping manure into the drum, leaving about two days’ worth of bedding at the other end with moisture levels around 50%.

They bed stalls every day during the week to use the solids as they come right out of the separator drum, adding acidifying ag lime to control mastitis.

Diversity key at Slate Ridge

“For us the secret weapon is diversity,” says Ben Peckman of Slate Ridge Dairy, Thomasville. He and his wife and high-school aged children milk 150 cows and raise 100 heifers, also feeding out all bull calves as steers.

He says there’s not one multi-million-dollar investment here, just the things that altogether add up to make a large impact.

At the dairy, he looks for ways to streamline, like ovsynch for repro. “It’s the little pieces here and there, he says, mentioning the machine with a smart phone app he purchased to do daily dry matter analysis on feedstuffs before mixing.

“Instead of always looking at the past for those adjustments, I can go out and see what the DM is right now,” says Peckman.

He fills the small sampler with three samples to get an average. “I have feed charts on my phone, pop in that number, and it changes out what I put in the mixer to get the same DM pounds,” he explains.

With feed stored in drive over piles, this is even more important to get the accurate measures each day, according to Peckman, who sees how it changes daily, firsthand.

“On a rainy day, it goes up, and on a dry, hot day, it goes down,” he says. “When changes happen day to day, testing every two weeks is not enough. My spreadsheet smooths out the changes by using the average of the past three days. When we started doing this we saw better production and components.”

A robotic feed pusher is another feed technology that’s made a difference. “We see higher intakes, fresher feed, labor savings and the ability to do this when I’m not there,” Peckman relates.

Bankers asked what ‘calculus’ goes into making such investments. For Peckman, the answer was blunt. “It’s something that improves how my herd performs but the robotic pusher does something I’m not willing to do. I’m not getting out of bed at 2:30 a.m. to push up feed.”

Other barn updates include ventilation controls and ceiling fans above bed pack areas. It’s better for cow comfort but there’s also a cost savings. “We use half as much straw and bedding with the new fans drying the air.”

His wife’s mobile milk pasteurizer is another innovation. They always fed whole milk and had a few problems when they fed it unpasteurized.

With the mobile pasteurizer, it’s two-fold: “the milk is better, but also the temperature is much better. It keeps the milk warmer, and we have healthier, better growing calves.”

Peckman really enjoys the cropping side, farming 1100 acres of diversified crops to feed the cowherd and take advantage of other markets.

“Diversity is how I mitigate risk. It’s my key technology. Diversity can’t be bought, but it pays. It helps me combat weather, combat markets, and combat other adversities in general,” he says, adding that it’s “not rocket science,” just looking at things other farmers are doing and adapting.

He does use GPS guidance for his tractors for planting and spraying, which saves seed and inputs and work off field monitoring with yield maps.

In addition to traditional corn for grain and silage and alfalfa haylage, they grows high oleic soybeans at Slate Ridge Dairy. “We saw a drastic increase in butterfat percentage,” Peckman reports.

On his silage ground, small grains are grown — triticale, wheat, and barley. The barley he harvests after it gets the head, two weeks before it would be a grain harvest, as silage for feeding heifers.

One “big new innovation” he’s excited about is male sterile forage sorghum.

“It puts a head on without developing grain in the head,” Peckman explains. “This allows the plant to concentrate on putting energy into a plant that is a high sugar crop not a high starch crop. It’s very comparable to corn silage. I take a pound of corn silage out of the ration and put a pound of this stuff right in.”

He has replaced up to 40% of his corn silage with this particular sorghum silage and would like to get to 50% because “it’s a very economical feed to grow, the seed is cheap and inputs are less. It’s working well for me, but you have to have a way to harvest it as the BMR forage sorghums don’t ‘stand’ all the way to harvest.

“We started feeding this two years ago, and our components are up.”

Another newer crop in Peckman’s diversified portfolio is milo, or grain sorghum. He says it’s economical to grow and drought resistant, and they have a market for bird seed.

The wheat is grown as a cash crop but it has been fed too. The barley he harvests is a supplement for dry corn, depending on the year. He likes to grow these crops because they make good straw to bed the cows.

Peckman is a big believer in keeping his soil covered at all times, so some of the decisions and rotations are tweaked with weather and calendar. Over the past couple years, he has added a few acres of sunflowers to the crop rotations.

“We can double crop sunflowers after wheat, and there is a viable bird seed market for those,” he says.

“Mainly, they are beautiful, and I see people enjoying them. Nobody is paying me for that part of it, but it warms my heart to see neighbors stopping with the families, taking pictures and looking at my flowers. With everything going on in the world today, if I can see someone go out and smile a little, it’s worth it.”

As bird flu detections escalate among California dairy and poultry operations, Pennsylvania’s State Vet urges early detection to ‘stamp it out’

By Sherry Bunting, Farmshine, Nov. 15, 2024

HARRISBURG, Pa. – USDA is set to amend the spring order on transportation testing to include a new National Bulk Milk Testing (NBMT) program for H5N1 in dairy cattle, which will be patterned off the former Brucellosis strategy.

This will be a regionally tiered approach, testing samples from processing plants, to assess where the virus is at this time, according to Dr. Kellie Hough, USDA District Emergency Coordinator.

“Depending on the results, we will then drill down to the state level and to the farm level, if necessary, to attempt to eradicate this,” she said.

Federal and state agencies will work with affected facilities to enhance their biosecurity levels and restrict animal movements, but also to ensure their business continuity.

The federal action is in addition to the ongoing voluntary multi-state silo milk testing surveillance program that Pennsylvania is participating in already. In that program, processors provide blinded samples from bulk milk silos, according to their own cadence of frequency, said Pennsylvania State Veterinarian Alex Hamberg.

Hough and Hamberg gave updates on the Center for Dairy Excellence monthly industry call Nov. 13.

“We supply processors with everything they need to send these samples, and the only information going to the NVSL network laboratory is the date of sample collection and the states represented by the milk in the silo at the time of the sample collection. This helps show we are clear of the virus and helps build a baseline,” said Hamberg.

He said states are having ongoing discussions with USDA about what federal surveillance will look like under the NBMT.

He stressed that the virus can be found in milk samples two to three weeks before clinical infection.

“If we can identify every farm infected right now, then we can contain this thing right now and make this virus extinct to never be seen again,” Hamberg urged. “But if we continue to avoid early identification, we could be stuck with it for as long as it wants to stick around.”

Dairy farmers have been slow to sign on to voluntary bulk tank testing at the farm level, with only 69 herds enrolled nationally, six in Pennsylvania.

Mandatory testing is currently being done in Massachusetts, Colorado, Oklahoma, Arkansas, and California. For the latter, it only began after the spread of H5N1 had escalated among dairy herds and poultry flocks in California.

During the past 30 days, as of Nov. 14, there are 201 new herd detections of H5N1 nationally. Of those, 186 were in California, two in Idaho, and 13 in Utah. The Golden State has had H5N1 detections in 291 dairies to-date, with more tests pending, and this represents more than half of the 505 cases across 15 states since the start of the outbreak in Texas last March.

Hamberg said dairies saw a 50% herd turnover within three months of infection in states that have contended with H5N1 in cattle. This is presumed to be a combination of cattle culling as well as some mortalities. Owners of infected herds also report struggling to regain their prior herd production per cow and seeing prolonged elevation in somatic cell counts.

“They are getting slammed in California,” said Hamberg. “It is not a good situation. The dairy industry is suffering, and the poultry industry is suffering. If they had had good participation in voluntary testing beforehand, they may have been able to stamp it out before it spread like this.”

He sees this as particularly important for dairies to consider the voluntary bulk tank testing that gives them ‘monitored herd status’ in Pennsylvania. “Our state is more dense than California, where it is spreading like wildfire,” he said. “In Lancaster County we have dairy on top of dairy on top of poultry on top of pigs. If we find this in an early stage, we can stamp it out quickly and contain it before it spreads all over the place.”

There is no evidence yet that the dairy variant of H5N1 has taken up residence in migratory bird populations or any other wildlife reservoir, but the cattle strain is being found in domestic poultry flocks.

On the human side, Dr. Miriam Wamsley, Pennsylvania Department of Health Epidemiologist reported there have been 36 confirmed human cases across the U.S. of the H5N1 strain found in cattle. Some have been dairy workers, others poultry workers. The cases have been mild, marked by conjunctivitis (pinkeye).

Blood samples collected from workers recently in Michigan and Colorado showed employees previously had it without knowing it.

Wamsley, urged seasonal flu shots, especially for anyone exposed to cattle and poultry: “Flu season is here. If you would contract them simultaneously, there is the possibility of the two (viruses) mixing in the human body to create a new strain, and at the same time, the combination can make a person very sick.”

The recent news of a teenager in British Columbia, Canada, hospitalized in critical condition, as well as the first pig detected with bird flu in Oregon, were confirmed to have the strain that is active in migratory bird populations, not the dairy variant.