By Sherry Bunting, Farmshine, April 30, 2021

WASHINGTON, D.C. — National Milk Producers Federation (NMPF) announced Friday, Apr. 23 a Class I mover reform proposal and intention to request a USDA Federal Milk Marketing Order (FMMO) hearing that would be limited to proposed changes to the Class I mover, after which USDA would have 30 days to issue an action plan that would determine whether the department would act on an emergency basis.

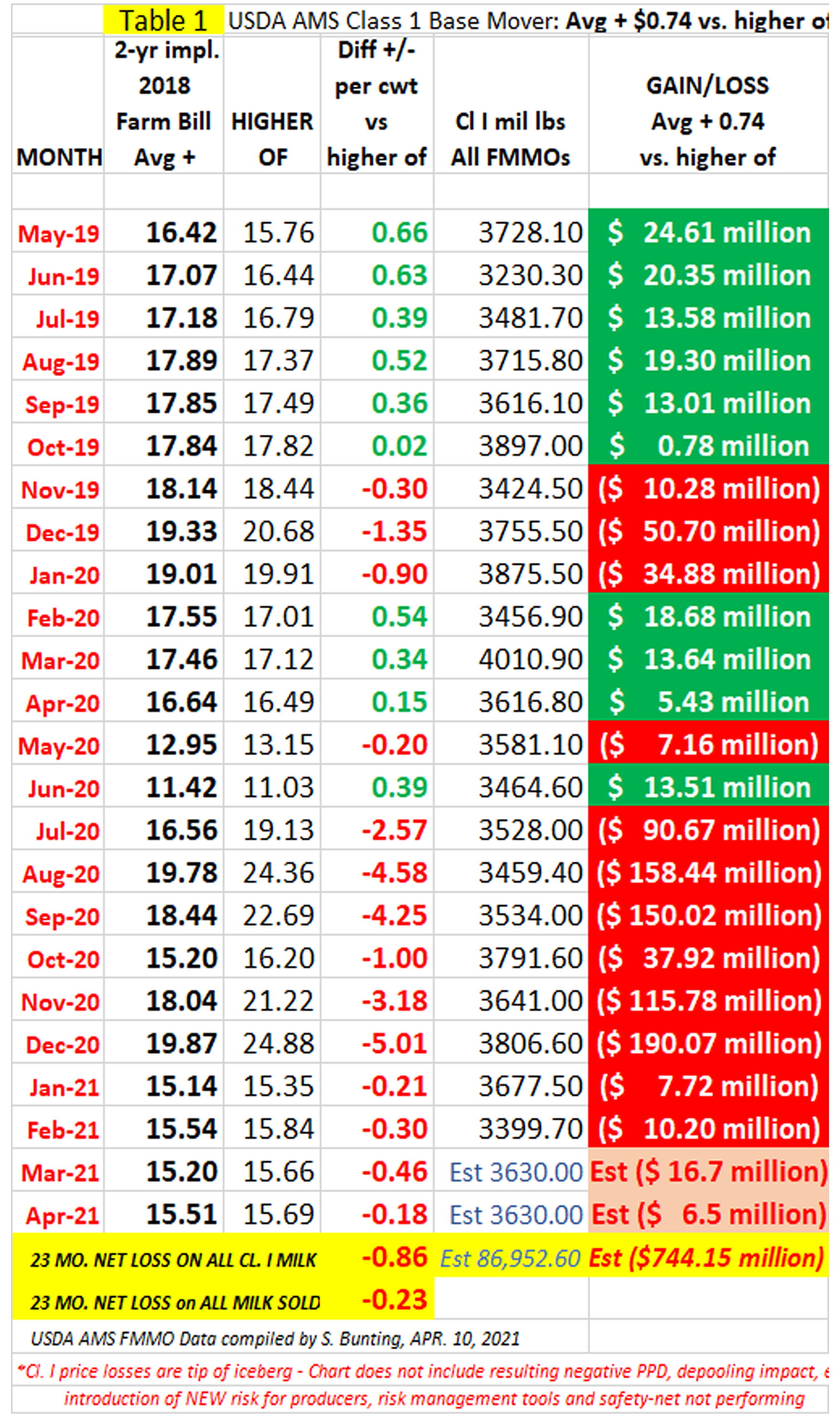

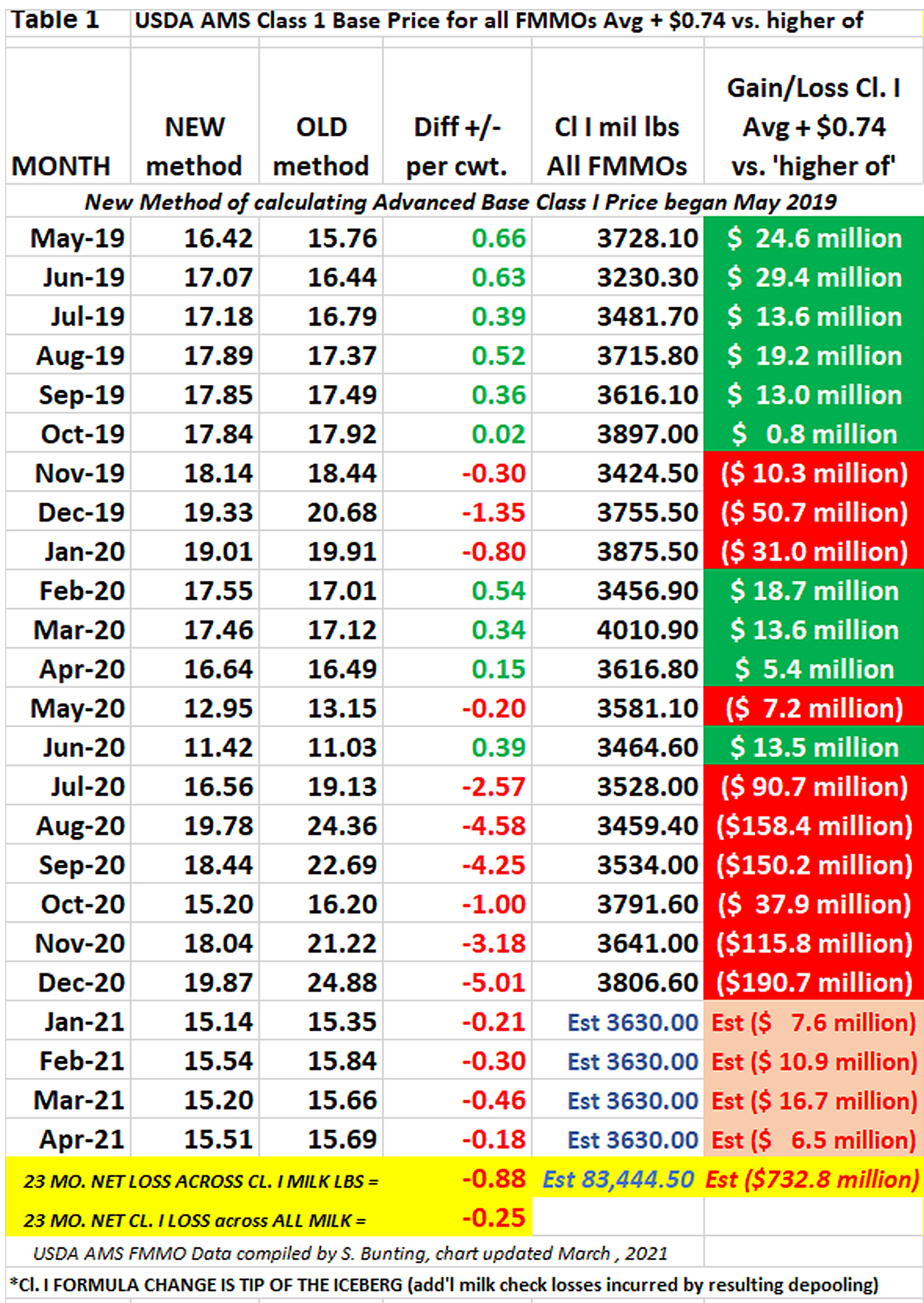

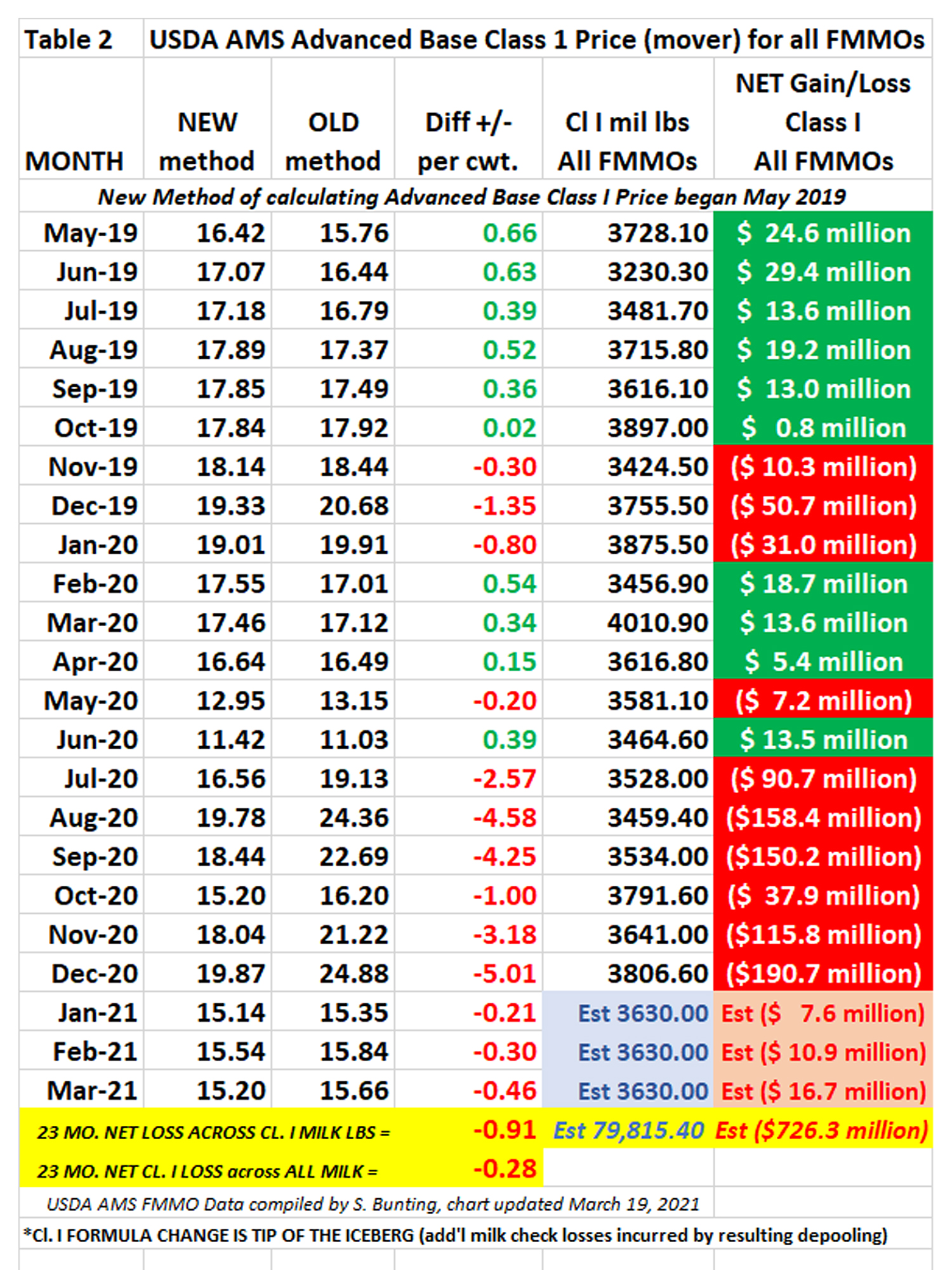

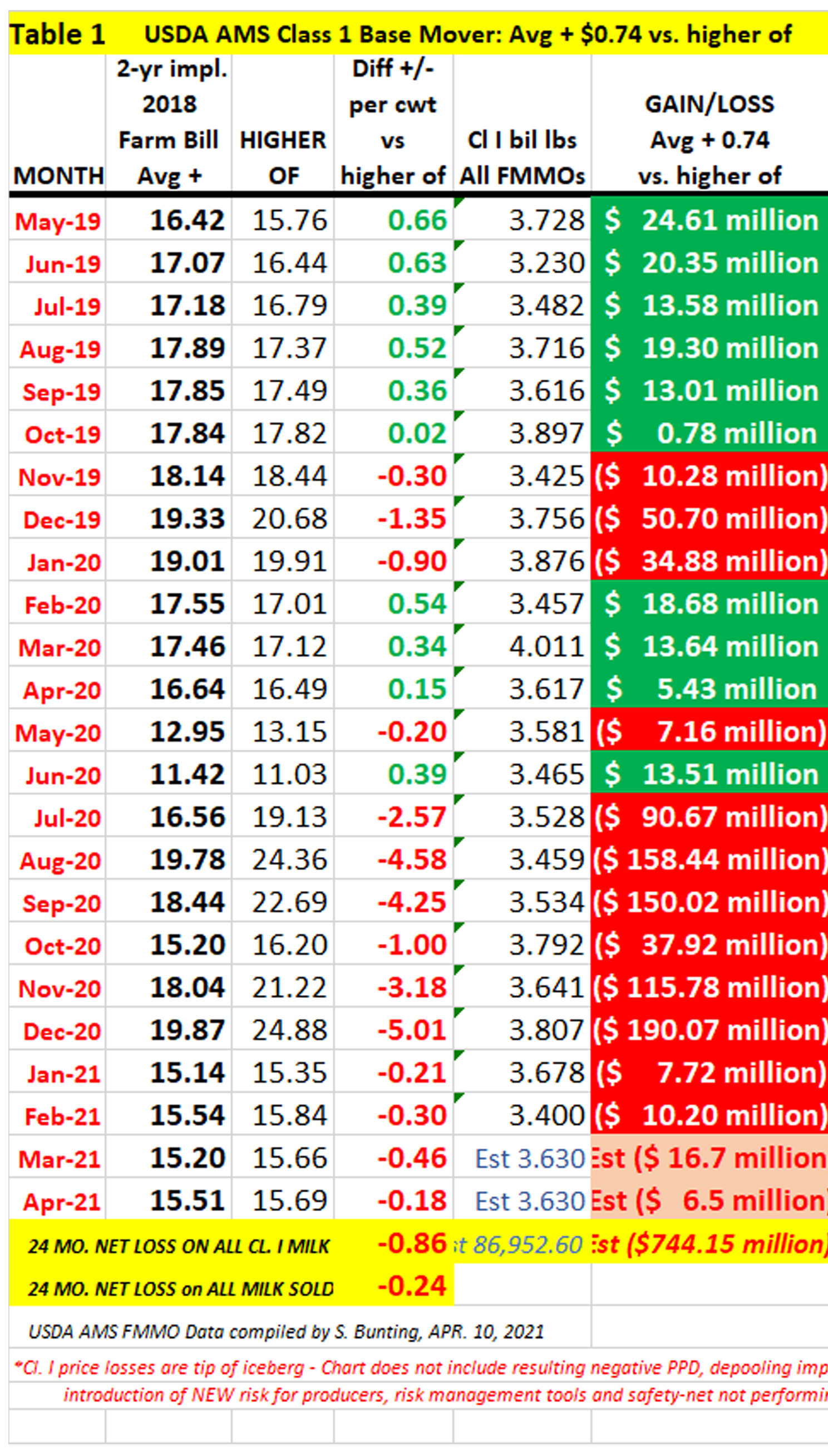

According to NMPF, their proposal would “modify the current Class I mover, which adds $0.74/cwt to the monthly average of Classes III and IV, by adjusting this amount every two years based on conditions over the prior 24 months, with the current mover remaining the floor.”

This adjuster change, if done today for the next two years, would pencil out above the current 74 cents (estimated $1.63).

The NMPF action comes after eight weeks of discussion by grassroots dairy producers and state and national dairy organizations seeking a seat at the table to address lost income and risk management disruptions influenced in part by the Class I mover change that was passed by Congress in the 2018 Farm Bill and implemented by USDA in May 2019.

While NMPF and IDFA have reportedly had conversations on the issue, IDFA has not yet publicly-announced a position.

On Tuesday (April 27), another proposal — called Class III Plus – was announced by a collaboration of state dairy groups in the Midwest. This proposal would also end Class I advance pricing factors.

Seasoned dairy policy analysts and economists suggest more proposals may be forthcoming.

USDA “will do the things it knows it can do to impact the (milk income) concern by providing better market opportunities, new market opportunities,” said U.S. Agriculture Secretary Tom Vilsack answer questions from North American Ag Journalists Monday, calling FMMO reform a “tough issue.”

On the specifics, though, the Secretary said simply that USDA would look to the industry “to work with them on the changes that need to take place.

“It’s a very very complicated issue, and not one that should be easily characterized. Anyone that tries to do that doesn’t understand the complexity of that particular topic. It’s very complex,” Vilsack explained.

He acknowledged that conversations are occurring within the dairy industry, but said: “Those conversations need to mature a bit more before anybody makes a decision that there’s going to be a significant change.”

However, in contrast to the Secretary’s observations, a “significant change” has already been made across all FMMO’s, legislatively, and it was done without hearings, without comment, without a producer referendum, without much conversation and without the knowledge of many dairy producers.

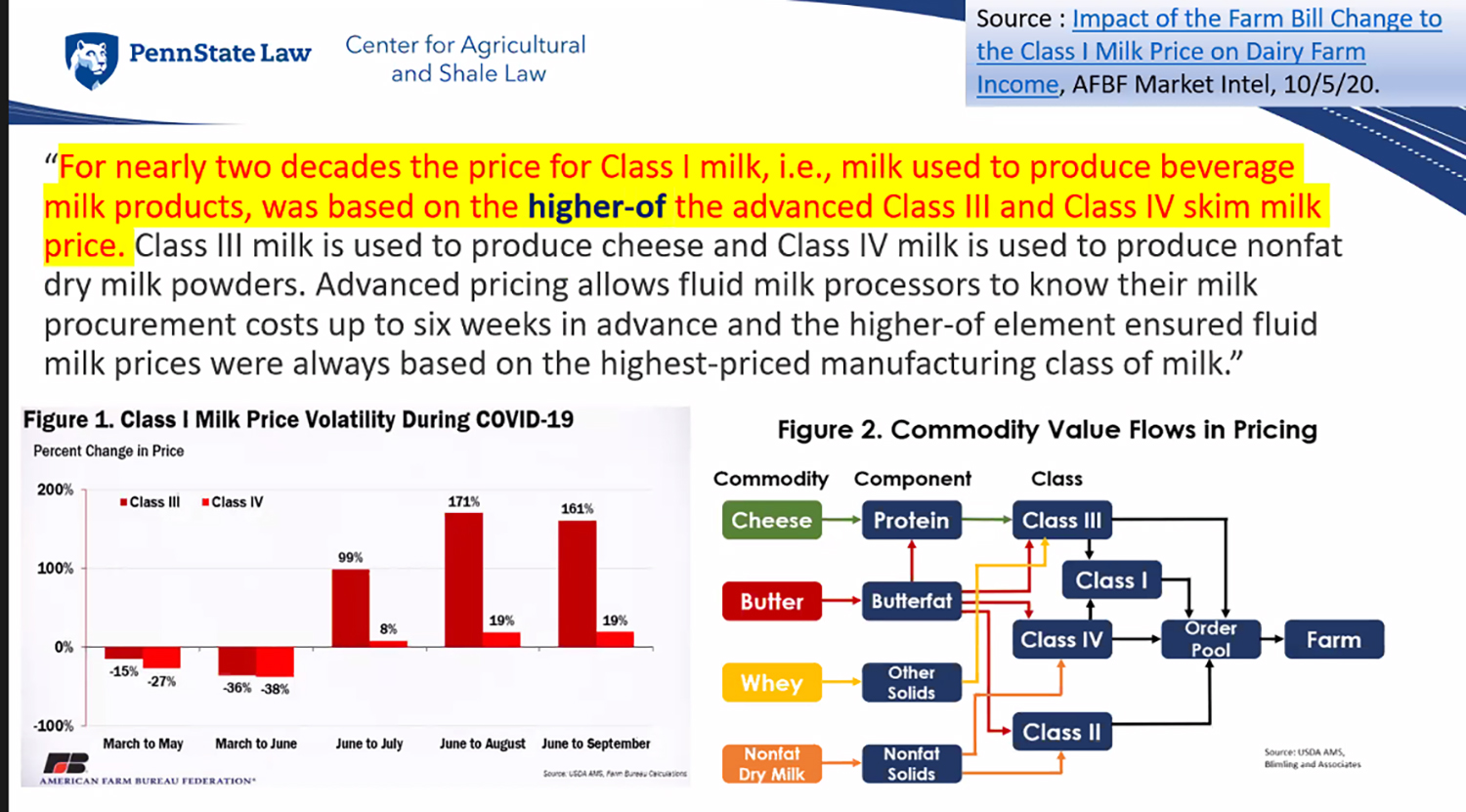

So here we are. The buck is being passed as the ball is being volleyed between industry, legislative and administrative. The volley started when NMPF and IDFA proposed the mover change in 2017-18. Congress then passed it, thereby replacing the mover that had been set by administrative hearing process 20 years ago, when USDA chose the higher of instead of an averaging method and documented disorderly marketing, negative differentials and depooling, back then.

Now, the volley is open again for what looks to be a toss from legislative to industry to administrative hearing requests.

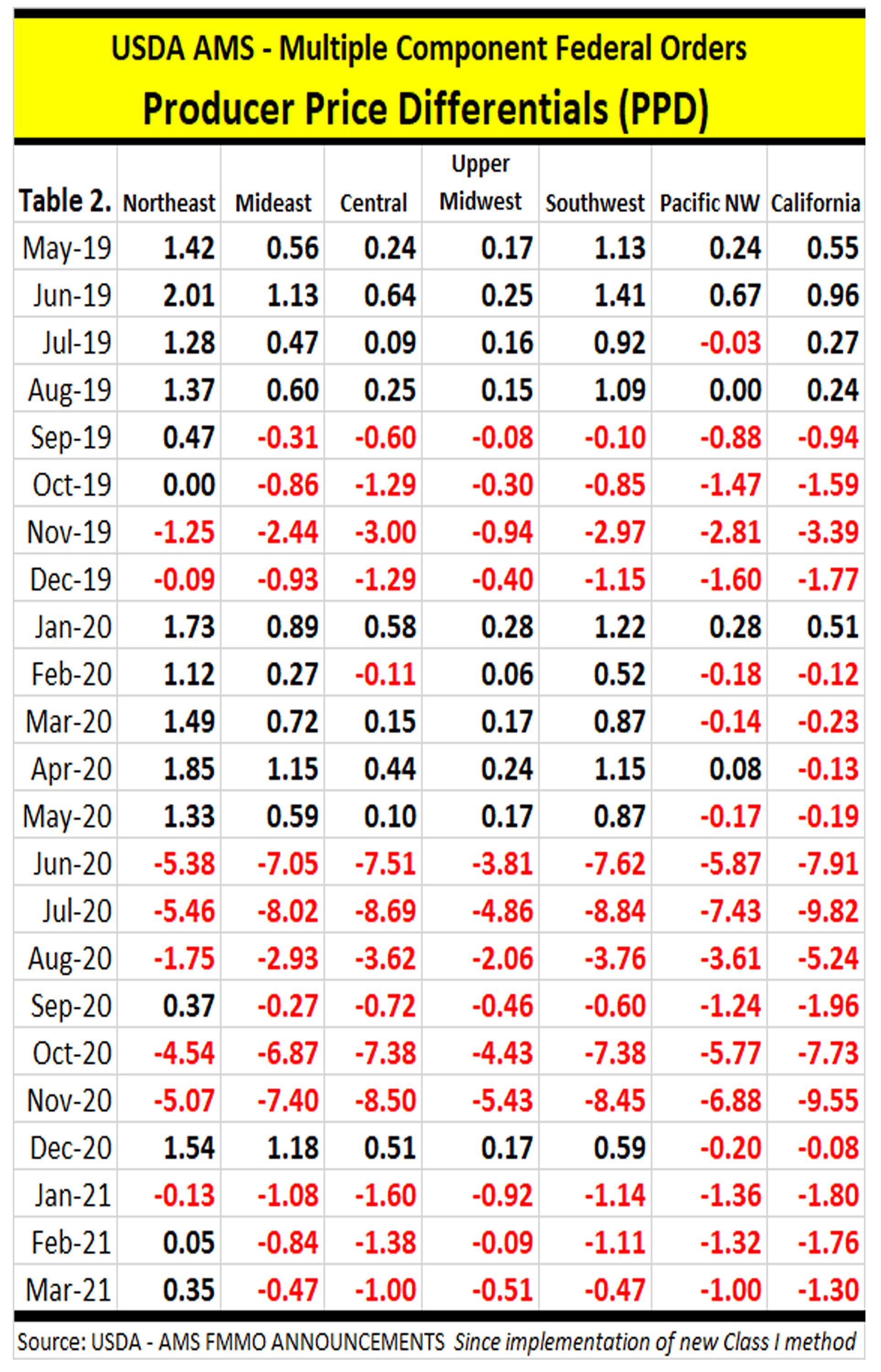

For its part, NMPF states that the current mover was “intended to be revenue neutral while facilitating increased price risk management by fluid milk bottlers. The new Class I mover contributed to disorderly marketing conditions last year during the height of the pandemic and cost dairy farmers over $725 million in lost income.”

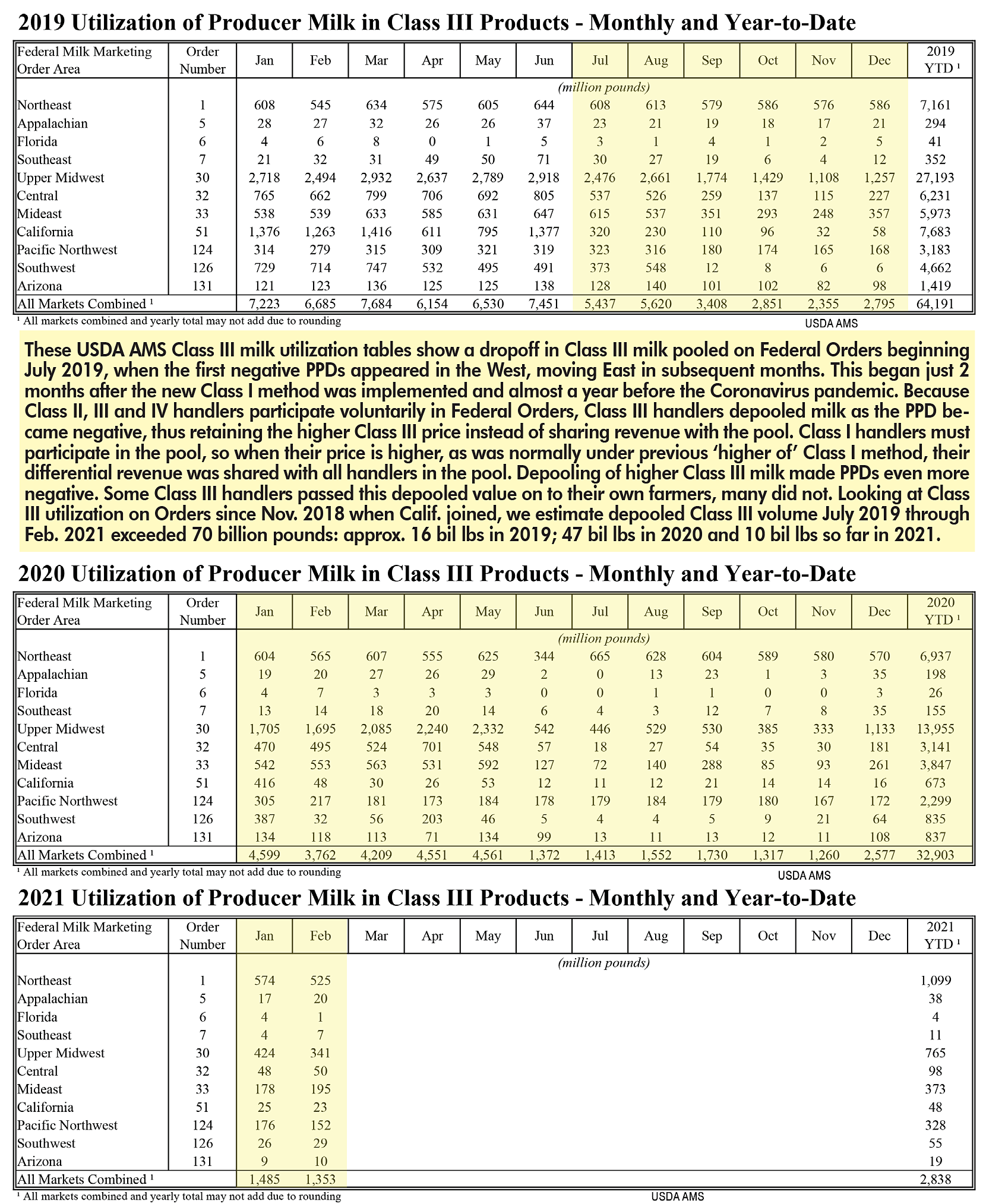

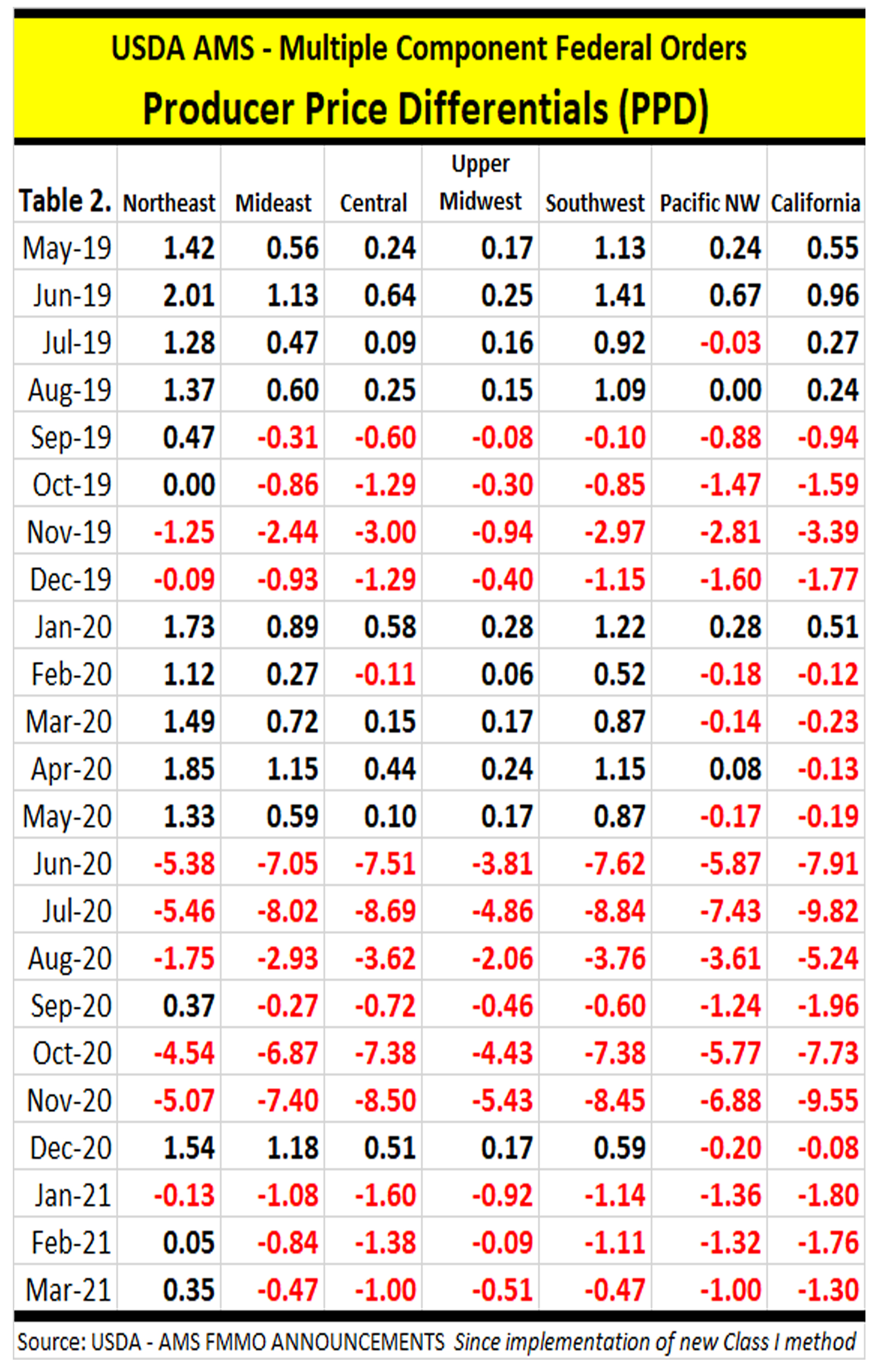

Analysis by various industry experts, including Farm Bureau’s Market Intel, peg the broader net farm losses at $3 billion when the change influenced a domino-effect of negative producer price differentials (PPDs) and massive depooling.

In the three fat/skim pricing FMMOs of the Southeast U.S. where PPDs are not shown, Calvin Covington calculates dairy farmers in FMMO 5, 6 and 7 collectively had net loss of $1/cwt off the blend price for 23 months due to the mover change from higher of to average-plus.

NMPF’s proposal is described as helping “recoup the lost revenue and ensure that neither farmers nor processors are disproportionately harmed by future significant price disruptions.”

A Penn State Ag Law Center webinar already planned on FMMOs this week, turned into a hot topic. Brook Duer, staff attorney for the center and moderator asked webinar guest Dr. Andrew Novakovic, Cornell professor emeritus about the specifics of the NMPF proposal.

“This proposal would recalculate the adjuster every two years, except the adjuster can never be less than 74 cents,” Novakovic said. “They are not talking about changing the ‘average of’ back to the ‘higher of.’”

In weekly producer conference calls facilitated by American Dairy Coalition after a letter was sent to NMPF and IDFA signed by hundreds of dairy farmers and organizations, a return to the higher of was identified as a short-term option while long-term proposals are vetted. American Dairy Coalition, and the grassroots groups who have been part of the conversation since February, sent emails with talking points, urging producers to contact key lawmakers and talk to them about the situation.

Proponents of a return to the higher of point out it was already vetted by USDA hearings, whereas the current average plus 74 cents was not.

“As the COVID-19 experience has shown, market stresses can shift the mover in ways that affect dairy farmers much more than processors. This was not the intent of the Class I mover formula negotiated within the industry,” noted Randy Mooney, chairman of NMPF’s Board of Directors in a press release. “The current mover was explicitly developed to be a revenue-neutral solution to the concerns of fluid milk processors about hedging their price risk.

“Dairy farmers were pleased with the previous method of determining Class I prices and had no need to change it, but we tried to accommodate the concerns of fluid processors for better risk management,” Mooney stated further.

“Unfortunately, the severe imbalances we’ve seen in the past year plainly show that a modified approach is necessary. We will urge USDA to adopt our plan to restore equity and create more orderly marketing conditions.”

Modifying the adjuster every two years is backward-looking for forward-adjustments.

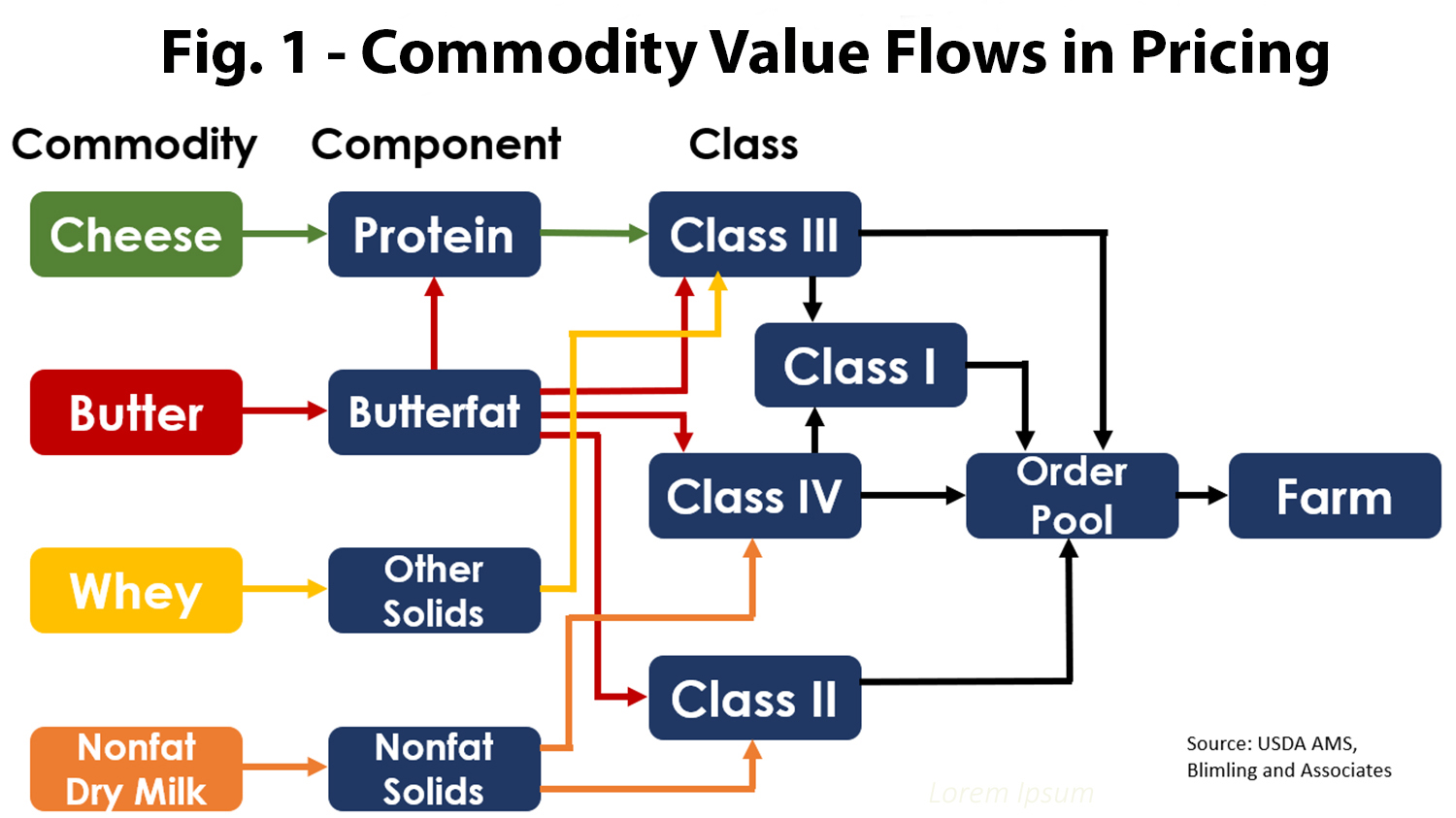

The current mover is already challenged by timing between Class I advance-pricing and Class II, III, IV announced prices as well as the higher protein production on farms in a system that prices protein in manufacturing classes but prices fat and skim solids in the fluid class.

In the Class III Plus proposal jointly announced by Wisconsin Dairy Business Association, Edge Dairy Farmer Cooperative, Minnesota Milk Producers Association and Nebraska State Dairy Association, advance pricing of Class I would also be ended.

The mover would be linked to the Class III announced skim price, not the advance skim pricing factor. The proposal includes an adjuster that would be revised annually in September by USDA for the forthcoming calendar year. It would equal the average of the monthly differences between the higher of Class III and IV skim milk prices, and the Class III skim milk price during the prior 26 months.

This adjuster would be floored at 36 cents just for the 2021-25 period “to facilitate faster convergence toward revenue-neutrality after COVID-19,” according to the announcement.

For its part, NMPF states that, “The significant gaps between Class III and IV prices that developed during the pandemic exposed dairy farmers to losses that were not experienced by processors, showing the need for a formula that better accounts for disorderly market conditions.”

To be sure, all FMMOs also saw gaps and inversion for three to six months in the pre-pandemic summer and fall of 2019.

When asked about the FMMO purpose and the ‘mover’ being set at the higher of to move milk to Class I use, Novakovic said USDA would have to look at the actual effect of the ‘average of’ on that purpose.

“Do we see any problem getting milk into Class I markets? Are they complaining there is not enough milk going to Class I?” he asks. “Probably the opposite direction is more true.”

Moving milk to Class I may be more of a discussion for the high fluid utilization areas of the Southeast, where producers end up indirectly ‘paying’ to bring milk in during deficient times of the year. This can be costly when there are price gaps and inversions as documented in the fall months of both 2019 and 2020.

When asked what recourse dairy producers may have in this, Novakovic indicated that lobbying the legislature is “theoretically possible” but that a legislative change is not likely apart from the next Farm Bill, which is three years away.

He also speculated that if someone put forward a proposal to return to the higher of for the next two years — and referred to the reasons given by USDA in its 2000 hearing decision – it’s “not inconceivable” that USDA could say they like what they had better than what Congress made them do, and perhaps like it better than changing adjusters or other ‘new’ proposals that would require a more lengthy hearing process if the industry is divided.

Novakovic was also asked how the Class III Plus proposal from the Midwest would affect Pennsylvania, given the state’s mostly Class I and IV utilization.

He responded to say Pennsylvania is part of FMMOs that include Class III (Northeast Order 1 and Mideast Order 33). He did not see any particular effect for the Northeast markets.

“Class IV would still be Class IV and II will be driven by IV values, and III would be unaffected, so the only question is what you would see happening with Class I,” said Novakovic. “The only way I see this proposal being viewed as a surprise is on the occasions when IV is higher than III, and that has occurred with some frequency in the past.”

The Northeast FMMO has seen a decline in Class III percentage relative to increase in Class IV and II over time. Class I sales also declined precipitously over the past decade but stabilized in 2019 and 2020 with rising sales of whole and 2% milk.

Novakovic confirmed that part of the problem in pricing Class I is the lack of beverage milk market indicators to do so.

As mentioned previously in Farmshine, Class I is required to participate in FMMO pooling, other classes are voluntary. Class I also has regulation at some state levels. On the other hand, in most states, beverage milk is used as a loss-leader in supermarkets, especially as large processing retailers dramatically cut the gallon price to compete for shoppers.

Under these factors, there is no way to gauge a ‘market value’ for Class I beverage milk apart from piggy-backing the other classes that value milk’s components in the manufacture of cheddar, butter, nonfat dry milk and dry whey.

The issue at hand is how to do that, now, in hindsight, after a significant surgical change was quietly made, and failed, and in the future within the context of FMMO reform.

-30-