By Sherry Bunting, republished from Farmshine, April 9, 2021

Class III futures gain big,

Cl. IV modest, spread widens

CME Class III and IV milk futures made a strong turnaround last week and continued to rally higher this week — especially on the Class III where $19s returned to the board for May through August and new contract highs were set all the way across the board.

The big gains on Class III vs. smaller gains on Class IV widened the Class III / IV spread that is currently averaged to determine the Class I base price, which affects PPDs and de-pooling.

The spread between the 12-month averages expanded to $1.75 over the next 12 months, with May through September contracts showing the potential for a $2 to $4 spread between Class III and IV.

On Wed., April 7, Class III milk futures for the next 12 months averaged $18.43 — up 32 cents from last week and almost $1.00 higher than two weeks ago. (Additional gains were made through Fri., Apr. 9.)

Class IV milk futures for the next 12 months, on the other hand, averaged $16.68 on Wednesday — up just 8 cents from last week and 75 cents higher than two weeks ago

CME cheese, powder higher,

whey firm, butter melts off early gain

On the spot dairy product markets via the CME this week, cheese had big gains, powder put on a penny, whey stayed firm at last week’s higher levels, and butter advanced early before erasing the advance at midweek to be a fraction of a penny lower than a week ago.

By Wed., April 7, the 40-lb block cheddar price was pegged at $1.80/lb, up 6 cents from a week ago with 4 loads trading; 500-lb barrel cheddar was at $1.58/lb, up a full dime from a week ago with 3 loads changing hands.

Dry whey on the CME spot market remained firm at last week’s advance, pegged at 66 cents/lb again Wed., Apr. 7 with zero loads changing hands.

Butter gained its way to $1.83 by Tuesday before losing almost 2 pennies Wed., April 7 when 9 loads traded, and the CME spot price was pegged at $1.8150/lb — a fraction of a penny lower than the previous Wednesday’s spot butter price.

Nonfat dry milk gained a penny this week. On Wed., April 7, the spot price for Grade A NFDM was pegged at $1.1925/lb with 2 loads changing hands.

March protein question answered

Last week in this column, the March Class and Component prices announced by USDA last Wed., March 31 were reported, and the protein price at $2.6954/lb — down about 30 cents from February — seemed to be a “head-scratcher” given the fact that all end-product prices were higher, and the Class III, IV and II prices also ended up higher.

Reaching out to USDA questioning whether this was correct or a typo, here’s how a USDA source explained the interaction of the fat and skim as a sort of ‘snubber’ or offset for protein vs. fat when butter gains are larger than cheese gains in value in the wholesale market as reflected by by end-product pricing, with fat and skim yields applied. (There’s a story to this phenomena, stay tuned for another edition explaining the how and why this ‘snubber’ came to be.)

Meanwhile, USDA referred me to this formula for the protein price calculation on page 5 of the monthly Class and Components announcement:

Protein Price = ((Cheese Price – 0.2003) x 1.383) + ((((Cheese Price – 0.2003) x 1.572) – Butterfat Price x 0.9) x 1.17).

The USDA source explained in an email as follows:

“The protein price is a function of both the cheese price and the butter price. If you look at page 5 of the report ‘Announcement of Class and Component Prices’ for March 31, 2021, you will find the formula for the protein price. In that formula, you will note the use of both the cheese price, which is the weighted average of both block and barrels, and the butter price. Please note that the use of the butter price has a negative sign, i.e. as the butter price goes up everything else held the same, the protein price goes down. So, while both the cheese price and butter price went up; the increase in the butter price for March compared with the February price was much larger than the (increase for the) cheese price, so the protein price declined.”

The USDA explanation continues:

“The Class III skim milk price is down in March about 60 cents per cwt ($0.0060 per pound) when compared with February, i.e. using the lower protein price of about 30 cents per pound times 3.1 pounds plus a small increase of about 5 cents in the in the other solids price times 5.9 pounds results in the decline of about 60 cents per cwt ($0.0060) for the Class III skim milk price. The Class IV skim milk price in March is about unchanged, up 1 cent per cwt ($0.0001 per pound) as the nonfat dry milk price was up only $0.0005 per pound.

“Both the Class III and Class IV prices are equal to 96.5 pounds of skim milk times the skim milk price for each class plus 3.5 pounds of butter times the same butterfat price. So, with the Class III skim down 60 cents per cwt ($0.0060 per pound) but the butterfat price up $0.28 per pound. The Class III and Class IV prices both increase. The gain in Class IV was $0.99 per cwt while the Class III price was up 40 cents per cwt.”

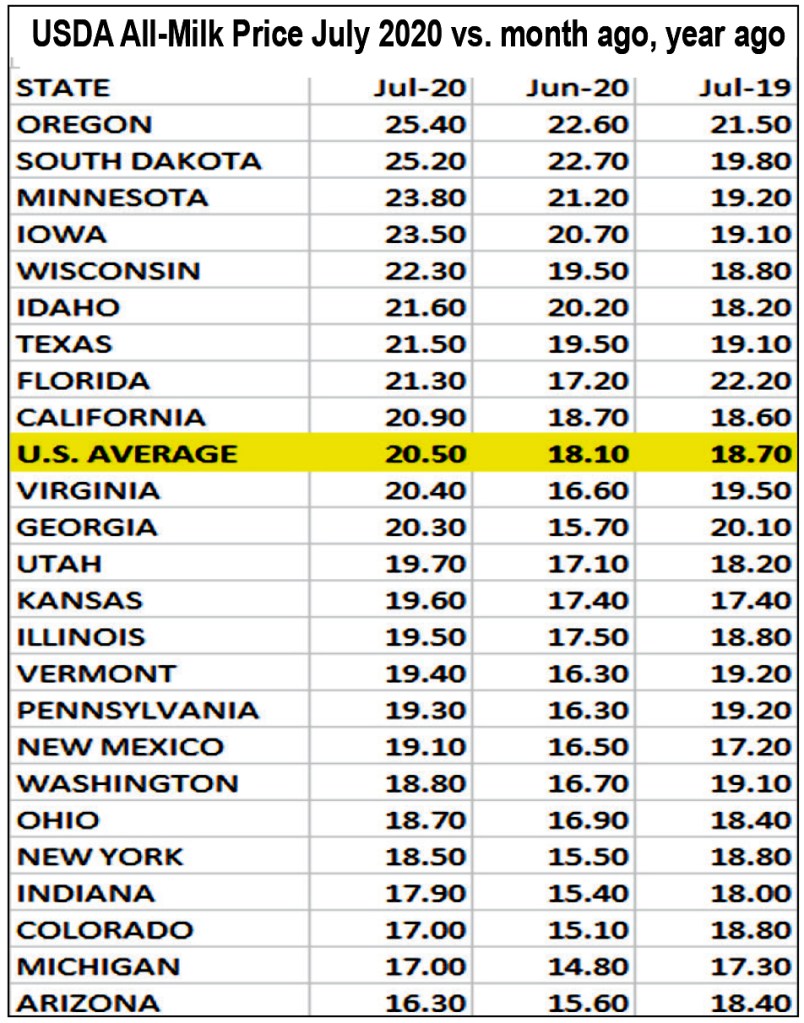

USDA reports Feb. All Milk price at $17.10, DMC margin $6.22

February’s All Milk price was announced last week at $17.10 and based on an national average butterfat of 4.10%. This was 40 cents lower than the January All Milk price at the same time that feed costs went higher.

The combined result was a Dairy Margin Coverage (DMC) margin for February announced this week at $6.22/cwt, the lowest since April and May 2020 when at the height of the Coronavirus pandemic shut down, the DMC margin was calculated at $6.03 and $5.37, respectively.

Letter signed by producers, groups, seeking remedy for failed Cl. I formula makes its way to NMPF / IDFA

On Federal Milk Market Order pricing — namely the failed change in how the base Class I price is formulated — National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) are at the table, according to U.S. House Ag Committee Ranking Member G.T. Thompson.

Sources indicate they are discussing various proposals and approaches. Meanwhile grassroots organizations representing dairy producers are continuing their almost weekly group conference calls and seeking a seat at that table.

Farmshine readers are aware that dairy producers from across the U.S., along with many state dairy associations and the American Dairy Coalition, came together in early March to compose a letter to NMPF and IDFA, addressing the impact of massive depooling in relation to large negative PPDs for dairy farmers across the U.S.

The letter specifically identifies the change in how the Class I base price is calculated, which NMPF and IDFA put forward, Congress passed in the 2018 Farm Bill, and USDA implemented in May 2019. The letter, signed by hundreds of producers and many producer organizations, will be officially sent to NMPF and IDFA by the end of this week (April 9), according to the ADC.

Specifically, the Farm Bill language states that the Class III / IV averaging method + 74 cents – instead of the previous “higher of” method – was to be implemented in 2-year periods. This suggests we are now at the point in time where something can be done to adjust this formula before the next 2-year period of implementation begins.

Meanwhile, dairy economists are being featured in webinars, zoom conferences and other venues to explain and ‘educate’ producers on PPDs, what impacts them, and how other aspects of Federal Milk Marketing Order pricing formulas, rules and provisions all work. All of it has become a hot topic since the new Class I formula implemented May 2019 leaves in its wake over $700 million in NET losses on Class I value, alone over 23 months, and upwards of $3 billion when negative PPDs and depooling are factored in.

While the change assisted in the idea of risk management for milk buyers, it has introduced significant and costly basis risk for milk producers, interfering with producer risk management tools, and has led to staggering net value losses by most dairy producers over 23 months since implementation, also undermining the purpose of the FMMOs with regard to the orderly marketing to assure milk moves to Class I fluid milk use.

Education is good. Solutions are better. Remember, the selling point to Congress for making the Class I formula change from ‘higher of’ to average + 74 cents in the 2018 Farm Bill was that dairy producers would be “held harmless”… Instead, they are being robbed. Stay tuned.

-30-