Large negative PPDs, Class III depooling and buyers reblending the milk price paid to farmers in June and July could be with us through August and even September because of how wide the divergence is between the Class III and Class IV prices, based on what the CME futures markets are showing. This divergence lowers all other classes in the pool (I, II and IV), especially now with the new “averaging” method of calculating each month’s Class I Mover in effect since May of 2019.

By Sherry Bunting, Farmshine, July 3, 2020

BROWNSTOWN, Pa. – Dairy producers seek to understand record-large negative PPDs (Producer Price Differentials) for June milk, meaning the the significant gains made in cheese markets and and Class III milk price are not making it to milk checks, especially for Federal Milk Marketing Orders (FMMOs) that are not predominantly cheese markets. (See FMMO data here

The extent of these negative PPDs – ranging from -$3.00 to -$8.00 per hundredweight (cwt) – has several factors, including the new way the Class I Mover is calculated since the 2018 Farm Bill changed it from the “higher of” Class III or IV pricing factors to an average of the two with an arbitrary 74-cent add-on. (See related July 28 story on revealing milk check data here)

“Expect historically large negative PPDs in Multiple Component markets for June and July,” writes Calvin Covington, retired breed association executive secretary and milk cooperative CEO, in an email interview with Farmshine this week.

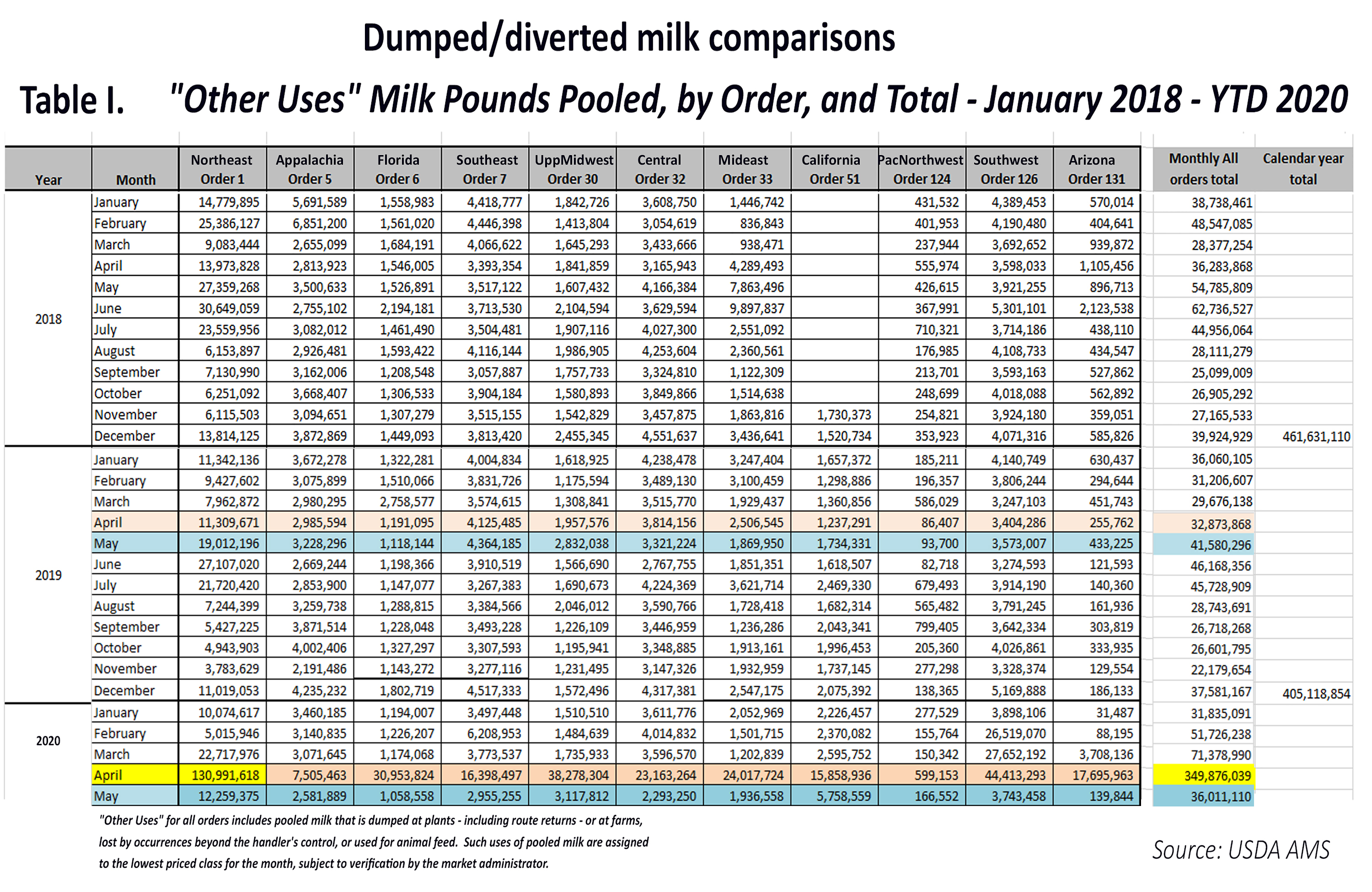

He also estimates the volume of milk depooled in June will set a record (it did), further limiting how much of the past six weeks of higher dairy product prices will even make it into their milk checks.

Covington confirms Class III milk was already being depooled in May. As reported in last week’s Farmshine, we calculated the volume of milk pooled across all Federal Orders in May was already 13% below year ago levels. For June, the depooling volume will be much more significant, in fact it is likely to be enormous.

“There is little economical reason to pool any Class III milk in June,” Covington asserts. “The only Class III milk that will be pooled in June is Class III milk going to a pool plant, and to meet any requirements to keep milk pooled in July.”

In fact, if buyers pooled Class III milk on Federal Orders in June, they would have to write a check to the settlement fund (instead of taking a draw from the fund as they do in normal conditions when the Class I bottlers are writing that check).

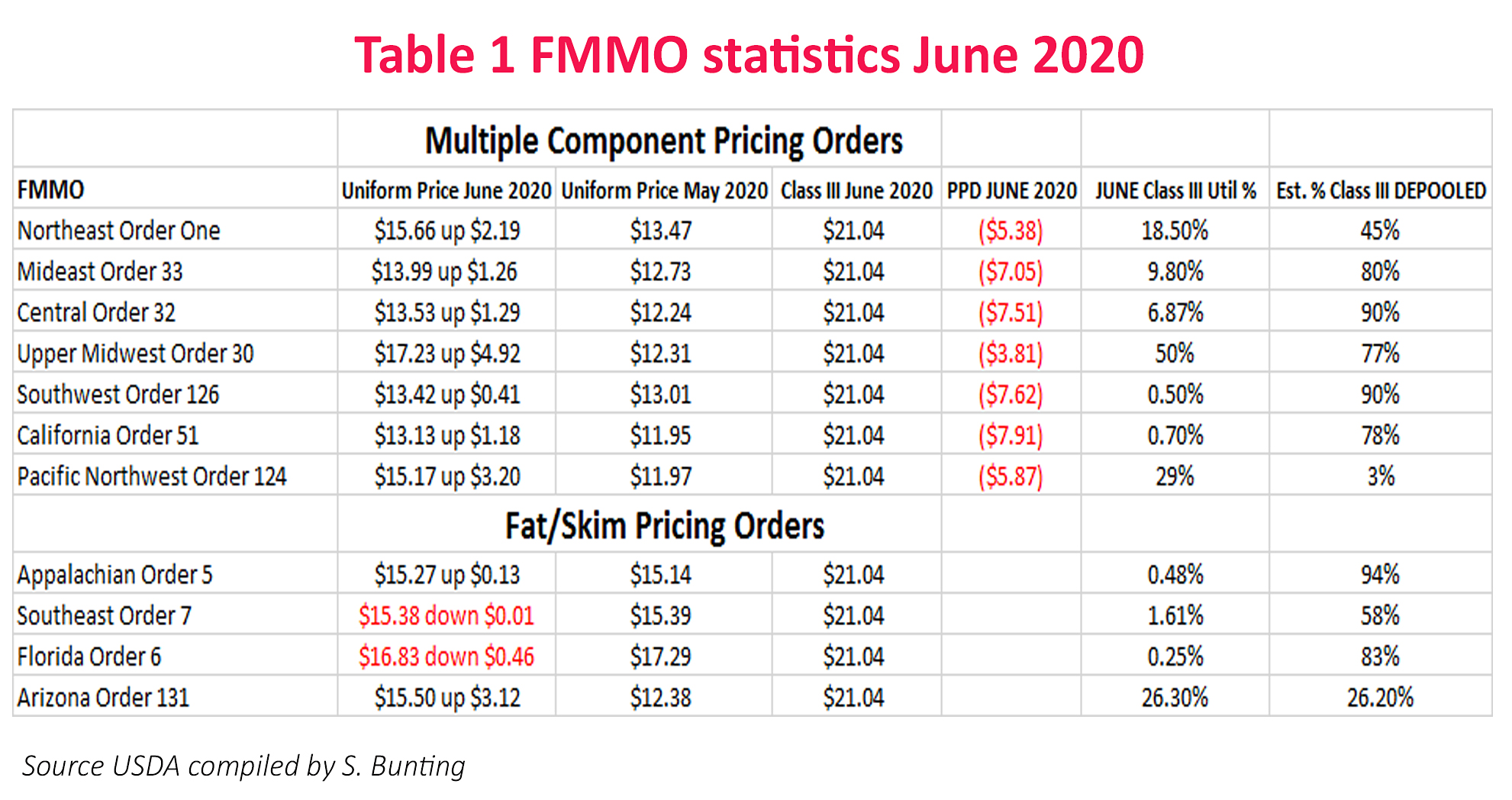

This is because the Class III price for June was announced this week at $21.04 – nearly $10 per cwt higher than the Class I Mover for June, which was set at $11.42 back in the beginning of May. The June Class I Mover is the lowest since the Great Recession while the June Class III price is the highest since 2014 — both now occurring in the same pooling month!

The reasons for the steep negative PPDs producers in Multiple Component Pricing (MCP) FMMOs will see for June milk, says Covington, are the high Class III price ($21.04) vs. Class IV ($12.90) and Class II ($12.99), the Class I Mover advanced pricing lag at $11.42, and the new method of calculating the Class I Mover, especially for July.

“In skim-butterfat priced markets – the Southeast Orders – blend prices will be lower than the Class III price,” Covington adds.

He explains that the PPD is paid on a hundredweight (cwt) basis, and it impacts all milk the same regardless of milk components.

“High component herds, especially in Multiple Component markets, see larger variation in milk prices,” Covington explains. “It is all due to arithmetic. Milk is paid on fat and protein. The more fat and protein in the milk, the greater the price change when fat and protein prices change.”

Covington spoke at World Dairy Expo last fall about the makeup of the milk check, and all of the factors that go into it. He reminds producers that only regulated plants are required to pay minimum class prices. Unregulated non-Class I plants choose to be associated with the pool so they can draw from it to pay a blend price to their farmers.

Now that the price for milk used to make cheese is so much higher than the price for milk used as a beverage or to make yogurt, ice cream, dips, butter, powder and all other products — cheese plants are free to disassociate themselves from the FMMO pool, and there is no regulation stating they must pay their producers even the minimum announced Class III price for components.

Under the current system, when the Class III price rises quickly to overshadow the previously-set Class I Mover, there’s no reason for those Class III plants to pool the milk, unless they want to remain “qualified” to participate in the pool (draw) in the following month.

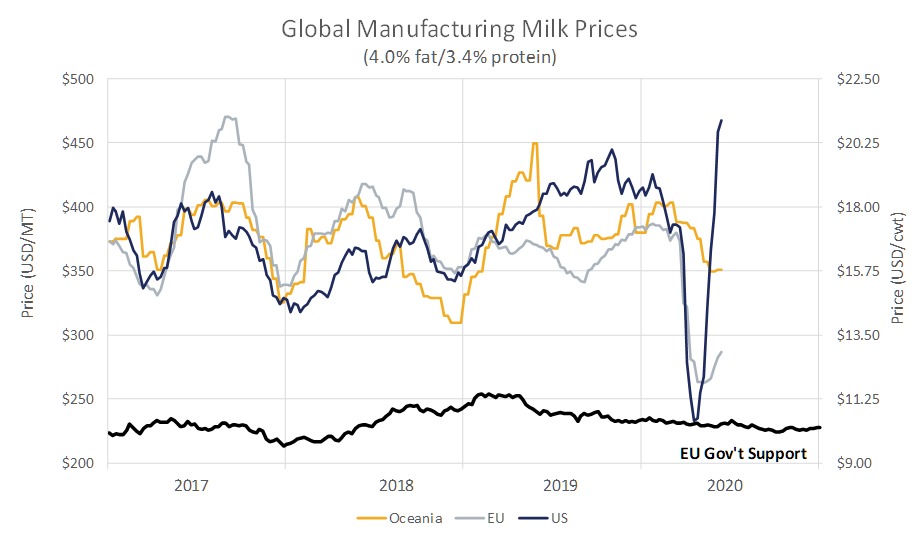

Covington observes that the upside-down pricing and negative PPDs will be with us at least through July. Dairy economists Mark Stephenson, University of Wisconsin and Andrew Novakovic, Cornell, noted in a recent Dairy Markets and Policy brief that this situation of negative PPDs, Class III depooling and buyers reblending the price paid to farmers could be with us through August and even September because of how wide the divergence is between the Class III and Class IV price via the CME futures markets.

This divergence lowers all other classes in the pool (I, II and IV), especially now with the new “averaging” method of calculating each month’s Class I Mover in effect since May of 2019.

Covington notes that it all boils down to math. The PPD is simply the difference between a Federal Order’s revenue available for producer payment (Class I, II, III and IV combined), minus the payment to producers at the Class III price based on components.

When Class III components are higher than the available revenue in the pool, the PPD is negative. When the Class III milk is depooled in that scenario, the funds aren’t there to pay the value.

“Factors impacting the size of the PPD, positive or negative,” he says, “are Class III price relative to the other class prices, volume of Class III milk pooled and an Order’s Class I price and usage.”

The primary factor in June’s negative PPDs is the extreme rapid increase in the Class III milk price. The rising cheese markets and Class III milk futures were mostly translated into the June Class III price because it was based on four weeks of June cheese sales.

The Class I Mover, on the other hand, was calculated six weeks earlier based on what the trade was doing at the end of April and beginning of May.

In the Covid-19 market-disrupted environment this is like two different world’s colliding based on timing and calculations.

Add to this the fact that Class IV and Class II prices saw muted increases during June compared to Class III’s large and abrupt increase, and what we are left with is the scenario where Class III beats all other classes by $7 to $10 in the same pooling month.

FMMOs with larger utilization of Classes I, II and IV will not see much boost from the uptrending cheese markets in their June blend price.

FMMO’s with large Class III utilization would see that boost. But depooling, reblending and assessments will all play further roles in how even those mailbox milk checks look once June milk is paid for.

Negative PPDs are not new. Dairy producers have experienced negative PPDs on milk checks in the past. Seeing a negative number in an uptrending milk market always brings questions and frustration. In fact, the November 2019 through January 2020 period in several of the past five years produced negative PPDs.

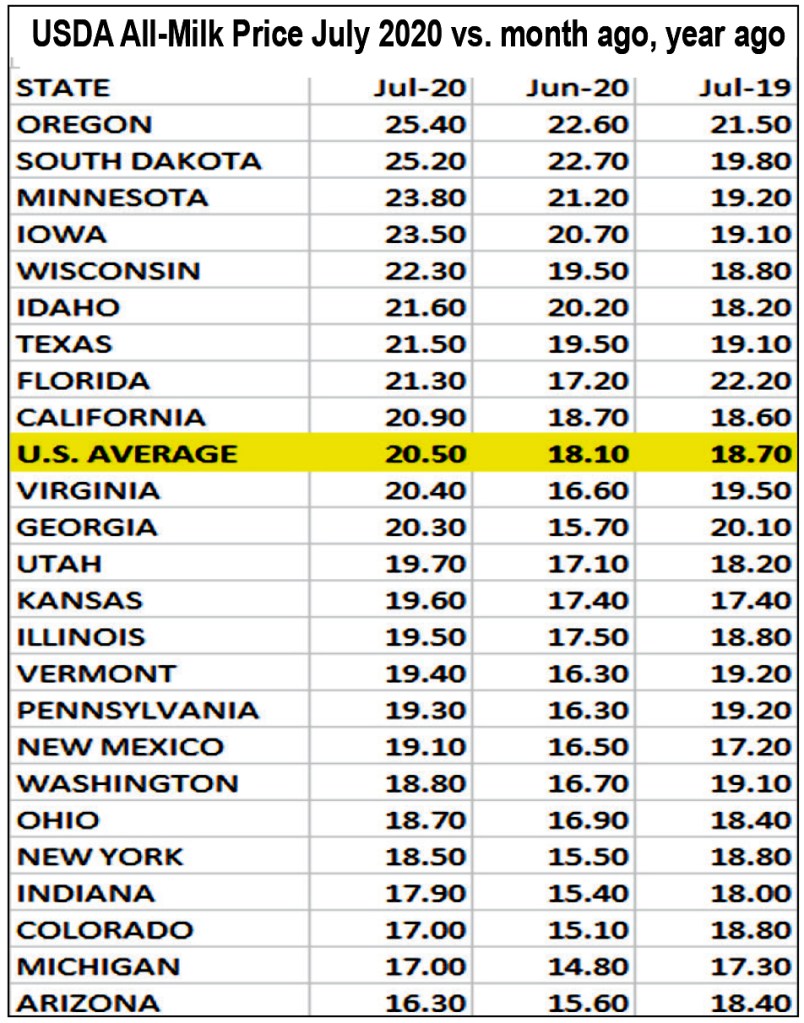

Last November, for example, the seven Multiple Component Pricing FMMOs saw a negative PPD averaging -$2 and ranging from just under -$1 to over -$3.

That pales in comparison to the negative PPDs producers will see for June, July and potentially August or September of 2020. Expect to see PPDs that are double, even triple, what was seen last November.

By now, most dairy farmers understand that a rapidly rising cheese market and corresponding Class III milk price presents the key factor putting PPDs into negative territory. When this happens, producers are reminded that a rising Class III milk price is still a positive development because it indicates milk markets are improving.

But in what some are calling a “whipsaw market” where prices turn abruptly in unexpected directions due to an unforeseen disruption like Covid-19, it’s useful to look at the other factors, for the long term.

First, when Class III milk’s component value is higher than the value of all the classes combined, the result is a negative PPD because after the Class III component values are paid, there is nothing left in the pool for the PPD draw. When the Class III milk is depooled, then that value is not available either.

When the blend price is higher than the Class III price, which is the norm, those Class III plants take a draw. When the reverse is true, they would technically owe the pool.

What sets this up against a huge market-disrupting event like Covid-19 is the lag-time between the calculation of the Class I Mover based on two weeks of trade and calculated six weeks in advance compared with the calculation of the manufacturing class prices based on the current month’s market conditions weighted over four weeks.

Even in those prices, there is a one to two week lag between what happens on the CME daily spot market and its translation to the weekly USDA National Dairy Product Sales Report, on which the class and component prices are based. There is no daily reporting of actual trade, actual sales of the four main dairy commodities, just weekly surveys that are published the following week.

On the flip-side, for April, the Class I Mover was set at $16.64 based on market conditions (advance pricing factors) during the first two weeks of March, before the Covid-shutdown. The Class III price came to $13.07 for April based on the economic shutdown affecting foodservice demand while retailers had a tough time keeping dairy products in stock.

With Class I sales rising dramatically in April, and the Class I Mover sitting $3.57 higher than Class III and $5.24 higher than Class IV – there was incentive to pool everything, even the displaced milk as the industry adjusted to an unforeseeable event and the Class I Mover stood well above all other classes, especially the dumped milk that was pooled at Class IV value.

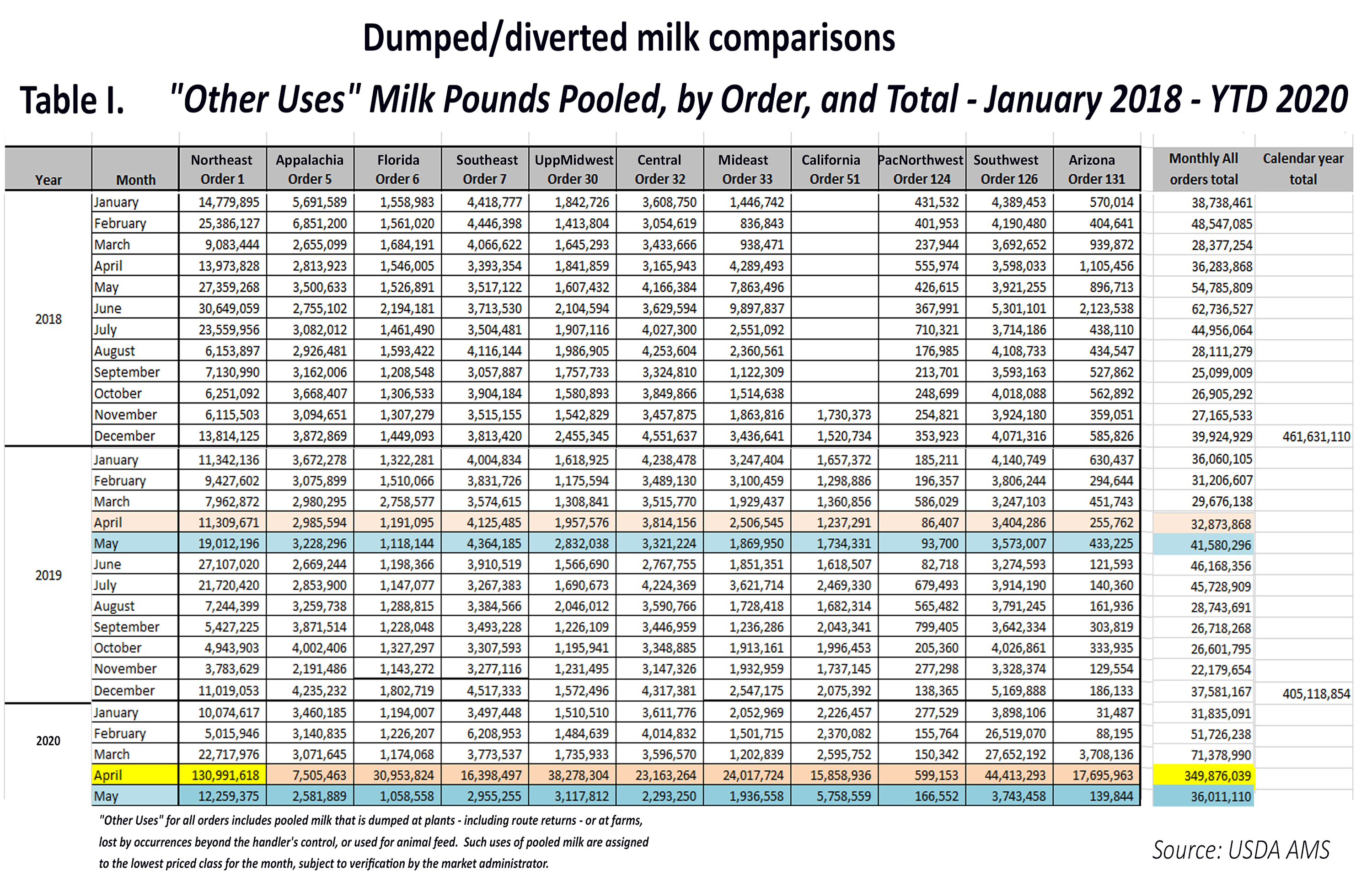

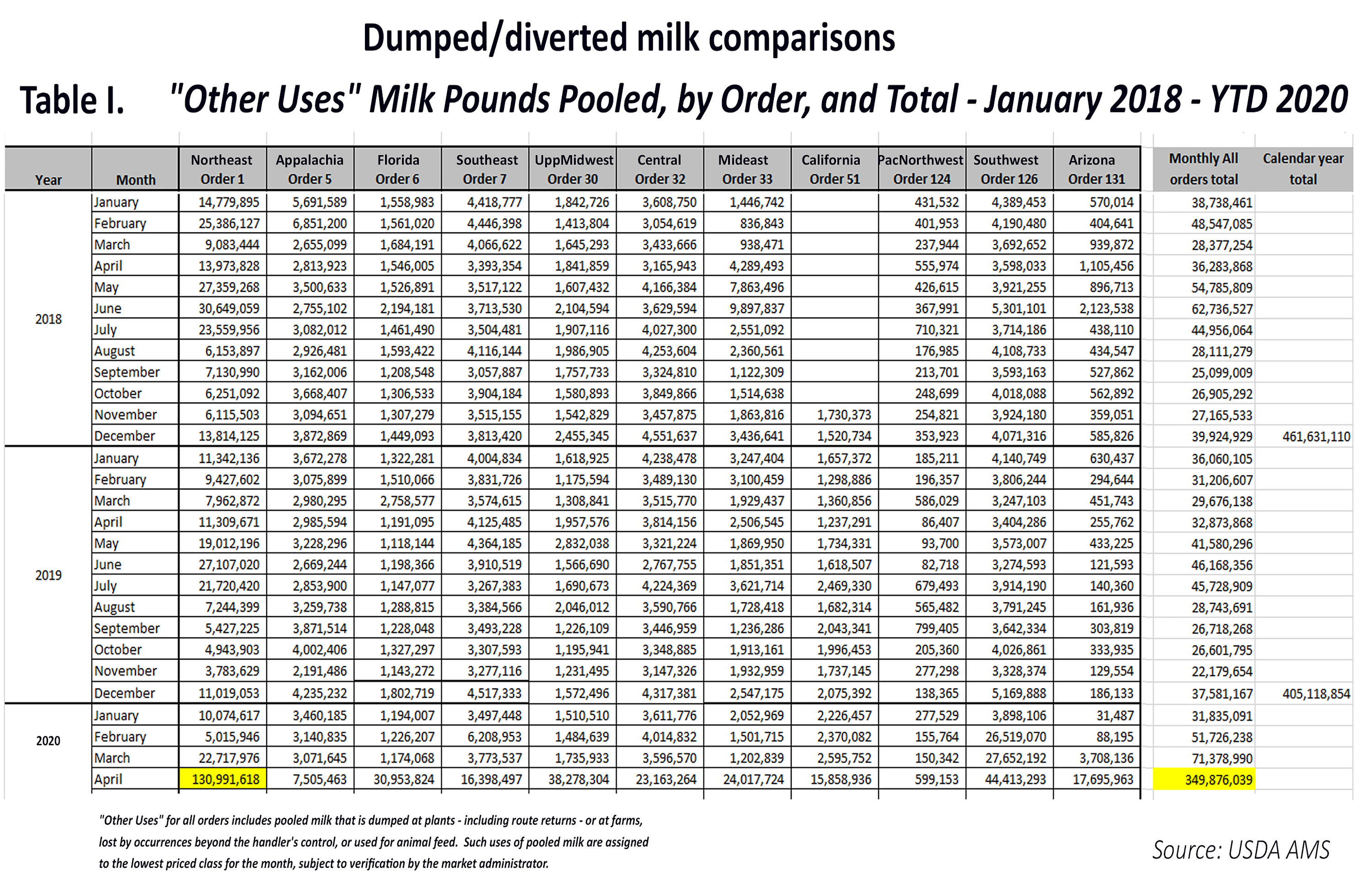

Thus, April set a record the amount of ‘other use / dumpage’ milk as 350 million pounds of displaced milk was pooled at the lowest class price across all FMMOs, nearly 10-times the amount that is normally pooled as ‘other use / dumpage’.

Now, that lag-time produces an opposite situation for June and July, and there is another wrinkle in the FMMO fabric – the new method for calculating the Class I Mover doubles the rub.

As a result of changes made in the 2018 Farm Bill, the Class I mover is now established by averaging Class III and Class IV and then adding 74 cents to that average. It used to be calculated using the higher of Class III or Class IV. In this case, that would have made a difference as Class III and IV have significantly diverged.

The calculation change for the Class I Mover was made to help processors hedge their future milk costs on the futures markets without having to guess which futures contract to use – Class III or IV. This was said to be something that would provide stability for Class I producers by stabilizing pricing for Class I processors. However, in these very unstable ‘whipsaw market’ times, the rub on producer milk checks will sting.

When it was proposed in 2017, American Farm Bureau Federation studied this method and documented little change to the net result for dairy producers when multiple years of pricing were averaged together and evaluated. In fact, when the new method went into place, there were several months where the average-plus-74-cents made the Class I Mover higher than it would have been under the old “higher of” method.

Not so in a volatile market with a time-lag involved.

These issues of negative PPD affect disproportionately the Federal Milk Marketing Orders (FMMOs) that have more Class I and IV utilization. FMMOs with small Class I utilization and large Class III utilization are relatively untouched as those blend prices would reflect mainly the much higher Class III cheese milk component value. But with depooling and reblending, those checks may also be impacted.

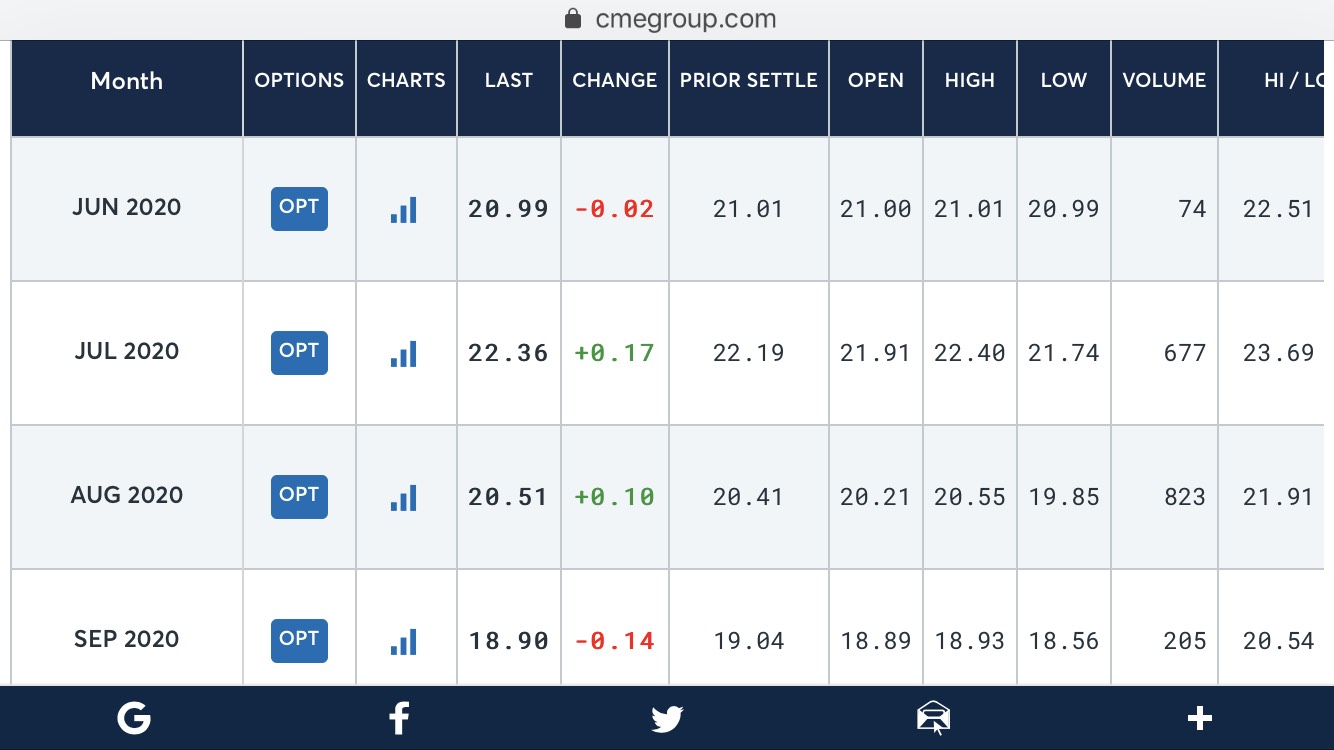

Looking ahead to July, the Class I Mover was already announced at $16.56, based on the advance pricing factors from the first two weeks of June. While July’s cheese trade is yet to be seen, the July Class III contract on the CME futures market stood at $22.85 at this writing on July 1st, which is $6.29 per cwt higher than the already set Class I Mover for July.

Even though the July Class I Mover stands $5.14 per cwt above the June Class I Mover, not even July’s Class I had the benefit of the full advance in June cheese trade because it was based on just the first two weeks of the June rally.

According to John Newton American Farm Bureau chief economist , there is currently, no mechanism to prevent negative PPDs. Newton writes in a recent ‘market intel’ piece:

“Historically, negative PPDs occur less than 15% of the time. Methods to prevent or mitigate negative PPDs — such as eliminating the advanced pricing component, reconsidering the higher-of pricing formula (but with forward contracting of Class I milk), requiring mandatory pooling of milk in all Classes or consideration of decoupling the Class I milk from the price of manufactured milk products – could be explored.”

UPDATE: Negative PPDs will be here for a while. Looking at these price spreads does not bode well for the continued inverted relationship between Class III and the Class I Mover — or what milk market analysts call “unorthodox pricing arrangements” — that will lead to continued negative PPDs and de-pooling of the higher Class III value milk from Federal Milk Marketing Order pools. In fact, the discussion of this issue has many twists and turns, a few questions have been forwarded to USDA Dairy Programs for some explanations, and June pooling data and blend price / PPD information is anticipated after the 14th.

Here’s the problem. Even when the ‘advanced pricing’ method gets caught up, the real problem is the way the Mover is now calculated. The 2018 Farm Bill made a huge change without a USDA administrative hearing and without a producer (bloc) vote.

Fluid milk processors wanted stability. They wanted to be able to forward-contract their milk costs and not have to deliberate over which futures contract to use — Class III or IV — since the Class I Mover used to be based on the “higher of” the two classes. Now, the futures markets are showing us that the spread between Class III and IV is going to be well above $1.48/cwt through November. That’s the significant number because the new Class I Mover method is calculated by averaging Class III and IV and adding 74 cents to that average. Once the III / IV spread hits $1.48/cwt, the 74 cents no

longer covers the difference.

Once we get to 2021, the spread narrows through those months, according to what the futures show now, but the Class III / IV spread looked reasonable and well within that $1.48/cwt for this current period back when viewed on the futures markets six months ago. If Congress can make a big change like this to Federal Order pricing formulas based on NMPF and IDFA agreeing on such while the Farm Bureau took a neutral position

— other than to review it and show it to be a wash when averaged over time — why can’t the Congress require a USDA National Hearing on milk pricing with Report to Congress?

Previous Farm Bills had such language, but the National Hearing “cost” was never funded. Now, the idea of a National Hearing on milk pricing, and a producer vote on Federal Orders, is seldom discussed. What we see from this Class I Mover example that a big changes can be made and implemented quite readily at the legislative level — no hearing or vote required — as long as the cooperative processors and proprietary processors agree on the change in advance. If milk is substantially depooled to keep higher end product values in hand, hopefully through the reblending process, plants and cooperatives will pay the marketplace value to dairy farmers, given the sacrifices producers have made to bring production into line with demand.

FYI: The Pennsylvania Milk Marketing Board (PMMB) successfully “decoupled” and stabilized the Class I milk price for two months by setting a Class I floor of $15 through the state’s over-order premium authority. The Federal Milk Marketing Orders were going to have a national hearing on this in April, but chose not to after economists and organizations in the Upper Midwest cheese region complained. The PMMB action was limited only to Pennsylvania, so for two months (the limit of the Order), when the Class I beverage milk price for milk produced, processed and sold in Pennsylvania fell below $15, the current over-order premium of around $1.00 per cwt was expanded automatically to bring the price back up to $15 for May-July 2020 for this very reason.

Trouble is, with the FMMOs not considering a similar move, this PA ‘premium’ only pertains to bottling plants paying milk suppliers for milk produced on PA farms (and they are free to take milk from other farms outside of PA). This price was built into the PA minimum retail milk price for May and June, but retailers, processors and cooperatives are not required to pass these state-mandated premium funds paid by PA consumers back to PA farms — unless the milk meets all three of these criteria: produced, processed and sold in Pennsylvania.

Author’s Opinion: There is one other thing worthy of consideration. A national hearing on milk pricing, period, to look at options, updates, simplification, transparency, daily reporting, producer voting, consolidation, transportation and deductions. Some grassroots groups have been asking for a national hearing with report to Congress for nearly 10 years as there is no other way for farmers to access the FMMO system run by market administrators, and they don’t even get a vote because cooperatives bloc-vote changes on behalf of their members. Previous Farm Bills included language for such a national hearing, but they were never conducted. At some point, the complexities at play here need to be evaluated from both regional and national perspectives in terms of “orderly marketing” and how farm viability and farm and food security in regions are affected and in terms of fulfilling the desire of many consumers wanting fresh, local milk.

-30-