By Sherry Bunting

Trade sentiment is mixed on how long the upward momentum in dairy markets can last as producers wait for these higher levels to land in their milk checks.

On one hand, USDA Dairy Market News reports strong pizza sales, stable to strong retail sales, and government purchases all stoking demand against reined-in supply. On the other hand, some analysts see weakness ahead as higher prices may prompt milk expansion by fall when demand may wane after CFAP food box purchases end and food-service pipelines are re-stocked. Much will depend on how the economic re-opening goes for families and food-service, as well as what happens with schools and sports. Experts suggest producers evaluate their risk management tools while markets present positive margins in a tumultuous time.

To-date, the USDA Coronavirus Food Assistance Program (CFAP) Farmers to Families Food Box Program has delivered 18.5 million boxes. The first round of May 15-June 30 fresh food purchases totaled $1.2 billion, including $317 million for milk and dairy products. Now USDA is poised to announce a second round of $1.16 billion for July 15-Aug. 30, of which dairy’s share has not yet been specified.

Also, as of June 22, USDA paid $895 million in CFAP dairy farm payments, and a total of 15,222 dairy producers (about half) have applied. The dairy payment formula equates to $6.20 per hundredweight on Q1 milk (including dumped milk). CFAP enrollment continues through August 28, 2020.

Meanwhile, milk futures continued their multi-week march higher on the heels of record-setting CME block-cheese prices through June, pegged at $2.70/lb Monday, June 22 and then $2.81/lb Tues., June 23. Barrels shared the advance, but were a record 44-cent spread behind the block trade at $2.37/lb.

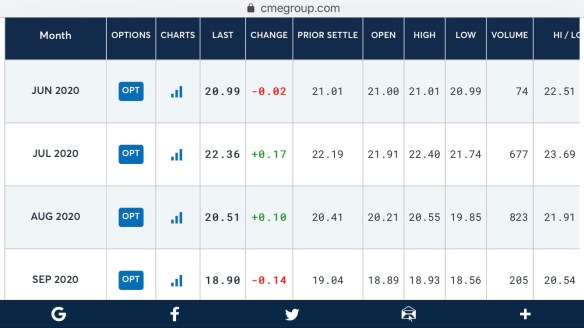

June’s Class III milk contract hit $21 Monday, up $9 from the USDA-announced May Class III price of $12.14. July’s contract topped at $22.19, and August edged into the $20s. Monday’s Class III milk futures averaged $17.98 for the next 12 months — up 69 cents from two weeks ago.

Part of the extent of Monday’s advance is attributed to new rules when higher trading surpasses the 75-cent limit, as happened Friday, the limit doubles for the next trading day, allowing more speculative activity up or down. But Monday’s spot cheese increase shored-up the gains, while after-hours trading hinted a 20-cent pull-back before another spot cheese market gain Tuesday noon narrowed the dip in fall milk futures. At mid-day Tuesday, summer 2020 front-months were another potential nickel or dime in the green, and penny to nickel gains were applied to 2021 Class III contracts.

Screenshot of June-Sept. Class III milk futures trading at Noon CDT Tuesday, June 23 — just after the spot cheese auction on the CME in Chicago saw 40-lb block cheddar trade at yet another record high of $2.81/lb with 500-lb barrels also higher at $2.36/lb — behind blocks by a new record-setting 45-cent spread.

New block cheese futures at the CME were launched in 2020, helping processors manage the risk of the wide spreads between 40-lb block and 500-lb barrel cheddar that broke records in 2019, setting new record spreads again this week.

Class IV milk futures gains into this week have been less stellar as butter had melted off a previous advance, but firmed up late last week, then pegged a 2-penny loss at $1.81/lb Tuesday. Spot powder strengthened last week in active trade after the biweekly Global Dairy Trade auction index rose 1.9%. The first two days this week, the Grade A nonfat dry milk spot price remained pegged at $1.03/lb with just two loads changing hands on the CME.

The awaited June 22 USDA Cold Storage report confirmed that accumulating cheese moved to food-service with a seasonally-unusual and record-large natural cheese inventory pull-out for the month of May. Despite this inventory pull, cheese stocks remain 5% above year ago, and butter stocks are up 21% vs. year ago. Inventory is apparently not as negative to markets as it was pre-Covid due to the retail shortages experienced in April during the height of ‘stay-at-home’ orders. Some companies report wanting to keep more inventory instead of operating ‘hand-to-mouth.’

On the farm side, USDA confirmed 1.1% less milk was produced in May vs. year ago. USDA data also showed 13% less milk was pooled on Federal Orders vs. year ago — abruptly reducing the pooling of dumped and diverted milk. At 36 million pounds, the volume of milk pooled as “other use / dumpage” in May was a fraction of April’s 350 million pounds of “other use / dumpage” milk pooled.