By Sherry Bunting, Farmshine, July 17, 2020

BROWNSTOWN, Pa. — The negative PPDs are turning out to be whoppers as expected for June, and experts say the situation will repeat in July. In fact, by the looks of the milk futures markets, the wide spread between Class III and IV is projected to remain above the magic number of $1.48/cwt. through at least September and quite possibly through the end of the year.

That’s the big news. This divergence is messing with PPDs more than normal and changing the ‘basis’ for producers in a way that defies most risk management tools. While the Upper Midwest milk checks reflected some of the marketplace rally, other regions fell quite flat. The range in uniform prices among FMMO’s is $4 from the $13s in in California, the Southwest and Mideast (Ohio, western PA, Indiana, Michigan) to $15s in Northeast, Southeast, Appalachia to $16s in Florida and the highest uniform price in the $17s for the Upper Midwest.

In fact, depending what Federal Milk Marketing Order (FMMO) you are in, and depending upon how much of that higher Class III “marketplace” value makes it into payments by plants to co-ops and producers, this could alter how “real” the Dairy Margin Coverage margin is, as well as the workings of Dairy Revenue Protection (DRP) program insurance and other risk management options that play off Class III but settle out on an “All Milk” price USDA will calculate for June at the end of July.

Producers who purchased DRP policies and based them on components to stabilize their risk in markets that utilize a blend of classes, are realizing an indemnity they expected to receive as protein doubled from May to June is now deflated to a smaller number due to negative ‘basis’.

Experts admit — There’s no good way to manage PPD risk (or as it’s referred to in the skim/fat Orders of the South “revenues available to pay”). Interestingly, Dairy Farmers of America (DFA), at its member risk management website, is touting it has “strategies” for members to “mitigate future negative PPD risk”.

(Read to the end to learn how to participate in the Farmshine Milk Market Moos milk check survey on this issue.)

So, what changed? Other than a pandemic disrupting things.

A big change is the new way USDA calculates the Class I Mover. This was implemented in May 2019 and is currently adding on to the largeness of the inverse relationship between Class III and the uniform price in multiple component pricing orders.

In fat/skim orders of the South, producers are seeing one price on their check but then “revenues available” to pay a different price. In some cases, the “revenues available” is reference to dispensing with “overbase penalties” in June because revenues were available to pay a better price on that milk.

There are no PPDs in the four FMMOs still pricing on a fat/skim basis. But those Orders are seeing a flat-out reduction in their uniform price as announced for Florida and the Southeast FMMOs being lower than May! Meanwhile the Appalachian Order gained just 13 cents over May. (See Table I above.)

During the formation of the 2018 Farm Bill, National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) agreed on this new way to price Class I so that Class I processors could find “stability” in their costs by forward pricing without having to “guess” which manufacturing class price contract would be the “higher of.”

Farm Bureau remained neutral at the time that this was going through, and their analysis showed, historically, this new way leveled out over time for dairy producers. In fact, supporters stated that the stability of averaging Class III and IV to make the Class I Mover offered stability in input costs to milk bottlers so they could forward price, which in turn would offer stability to farmers by keeping bottlers in a position of strength to invest for the future. These are the reasons we heard, and it wasn’t much debated at the time.

No hearings were held by USDA on this major change in Federal Order pricing for the one and only class that is actually regulated. It was done in the Farm Bill, legislatively, because cooperatives and processors agreed it was what they both wanted. (More information next week on what factors Covid and non-Covid-related that are contributing to these diverse trends between Class III and IV.)

Under the current method, instead of using advance pricing factors from the “higher of” Class III or IV to calculate the Class I Mover, the two classes are averaged together and 74 cents is arbitrarily added.

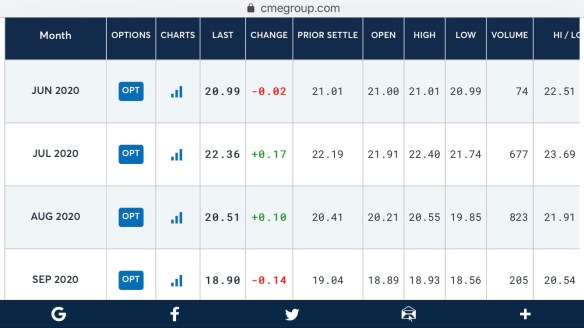

The reason this is such a big issue right now, and likely for months to come, is the size of the spread. Rapidly rising block Cheddar — which hit another record of $3.00 per pound on the CME spot market early this week – keep pushing the AMS end-product pricing higher, more than doubling the value of protein between May and June and pushing Class III milk futures further into the $20s.

In fact, Class III milk futures settled Tues., July 14 at $24.34 for July, $23.09 August, $20.23 September, $18.40 October, $17.44 November and $16.35 December. Meanwhile those months for Class IV milk futures settled Tuesday at $14.03 for July, $14.51 August, $14.85 September, $15.07 October, $15.31 November and $15.53 December. Not until December is the spread within the $1.48/cwt range where the new way of averaging the two classes returns from being so out of kilter to Class III.

Remember, these negative PPDs are the result of Class III being larger than the uniform blend price, and the large amount of depooling that resulted keeps that higher value from being shared in the pool. Class III handlers are accustomed to taking a draw, not writing a check, and there’s no requirement to be pooled unless a plant is a pool supplier or wants to stay qualified for the next month in most FMMOs.

A Farmshine article two weeks ago explained these price relationships in more detail.

Now the numbers are coming in. The recently announced uniform prices and PPDs range from nearly $4 to near $8 — just as leading dairy economists had estimated.

The least negative was the Upper Midwest FMMO 30, at minus-$3.81, where 50% of the milk utilization was Class III, and the uniform price gained a whopping $4.92 at $17.23 for June. In fact, producers in Wisconsin and Minnesota report $20 milk checks for June.

The most negative PPD was minus-$7.91 in California, where less than half of one percent of the milk utilization was Class III, and the uniform price gained just $1.18 at $13.13 for June.

The Southwest FMMO 126 wasn’t far from that at minus-$7.62 with a uniform price announced at $13.42 — up 41 cents from May.

In the Northeast FMMO One had a minus-$5.38 average marketwide PPD, but the uniform price gained $2.19 over May at $15.66 with 18.5% Class III milk utilization.

The Mideast Order PPD is minus-$7.05, and the uniform price gained $1.26 at $13.99 with just over 9% Class III utilization.

In the southern FMMOs, pricing is still on a fat/skim basis, not multiple components, but the inverse relationship of the Class I Mover to Class III pricing is keeping June uniform prices flat or lower compared with May. The Southeast FMMO 7 saw a penny decline in the uniform price to $15.38 in June, and Florida Order 6 uniform price fell 46 cents from $17.29 in May to $16.83 for June. The Appalachian FMMO 5 gained just 13 cents at $15.27 for June.

Nationwide, just over 9.5 billion pounds of milk was pooled across all Federal Orders in June, down 36% from 14.4 billion pounds a year ago and down 28% from the 13.2 billion pounds last month.

May milk production was down 1.5% compared with a year ago, but the pooling volume nationwide was already 13% lower than a year ago in May.

USDA confirms that handlers making just Class II, III or IV products are not required to pool the milk, and therefore, due to “expected price relationships,” some handlers decided to not pool some of their milk receipts in May, and most definitely elected not to pool in June.

“Only Class I handlers are required to pool all of their milk receipts no matter how it was used,” USDA Dairy Programs explained in an email response to Farmshine this week.

In Table I are the marketwide FMMO data for June from Market Administrator announcements on different dates over the past several days. Comparing Class III volumes reported to month ago and year ago, an estimated 45 to 94% of Class III milk was depooled in various FMMOs, with the exceptions of Arizona and the Pacific Northwest where depooling was less of a factor.

Looking at the Northeast FMMO, alone, the estimated 45% less Class III volume in the pool in June vs. May, kept just over $110 million in collective component value out of the Northeast pool.

The question is, since USDA confirms that money is “in the marketplace”, will that “marketplace money” make it to farm-level milk checks, 13th checks, reduced retains? And will the “Covid assessments” and “marketing or balancing fees” and “overbase penalties” be adjusted or eliminated in June?

Others wonder how this will affect the All Milk price for June as calculated by USDA NASS at the end of July. Will the erraticness of how this “value in the marketplace” could be handled make winners and losers in terms of the Dairy Margin Coverage? How will this situation translate to those margins as a national average?

USDA AMS Dairy Programs defined the NASS All Milk price in an email as follows: “The NASS U.S. All Milk Price is a measurement of what plants paid the non-members and cooperatives for milk delivered to the plant before deduction for hauling, and this includes quality, quantity and other premiums and is at test. The NASS price should include the amount paid for the “not pooled milk.”

USDA explained that, “The blend price (Statistical Uniform Price, or SUP) is a weighted average of the uses of milk that was pooled for the marketing period (month). If some ‘higher value’ use milk is not in the ‘pool’, then the weighted average price will be lower.”

However, the USDA response also points out that, “It is important to note that the Class III money still exists in the marketplace. It is just that manufacturing handlers are not required to share that money through the regulated pool.”

So, will it be shared at the producer level outside of the pool? From the looks of a few June milk check settlements that have been reported to Farmshine on the morning of July 15, it’s not looking like the higher Class III value is helping checks shared from the Southeast FMMO at this writing. How will that stack up to a margin that gets figured also looking at the Upper Midwest where the uniform price saw almost a $5 gain?

We’ll look at that more closely next week.

Dairy producers who want to participate in my Milk Market Moos survey of June milk checks, please email, call or text your June milk price, fat test and PPD, and the list of deduct line items, especially any “Covid-deducts,” and include any overbase penalties. Also, provide your location or in what FMMO your milk is marketed. All the information will be anonymously aggregated. Email agrite2011@gmail.com or call or text 717.587.3706.

The Jersey Cattle Association is doing a similar June milk check survey sampling across the country.

This is a big topic when risk management is based largely on components and Class III, even though Class III use is not regulated unless processors want it to be, and certainly not in a pricing scheme that no longer prices the higher of two divergent manufacturing price trends into the only truly regulated class — Class I fluid milk.

-30-

Emotional town hall meeting in Lebanon, Pa. draws over 200 people urging contract extensions for Dean’s dropped dairies

Emotional town hall meeting in Lebanon, Pa. draws over 200 people urging contract extensions for Dean’s dropped dairies Indeed, a legacy is on the line in Lebanon and Lancaster Counties, as in other communities similarly affected.

Indeed, a legacy is on the line in Lebanon and Lancaster Counties, as in other communities similarly affected. Rick Stehr, a nutritionist and owner of R&J Consulting, directed some of his comments to the significant number of youth in the audience, saying that these farms are where the next generation learns morals, values, work ethic and the joys and failures of life.

Rick Stehr, a nutritionist and owner of R&J Consulting, directed some of his comments to the significant number of youth in the audience, saying that these farms are where the next generation learns morals, values, work ethic and the joys and failures of life. Brent Hostetter, Lebanon County dairy producer: “I am not sure how we are going to handle this going forward. We have put all we have into the farm. Nothing will settle like it should.”

Brent Hostetter, Lebanon County dairy producer: “I am not sure how we are going to handle this going forward. We have put all we have into the farm. Nothing will settle like it should.” Alisha Risser, Lebanon County dairy producer: “We are proud of our milk that we produce on our farm, and we are proud of the Swiss Premium milk in our community. We are just asking the community to support us with letters to Dean Foods to provide a contract extension until fall or winter.”

Alisha Risser, Lebanon County dairy producer: “We are proud of our milk that we produce on our farm, and we are proud of the Swiss Premium milk in our community. We are just asking the community to support us with letters to Dean Foods to provide a contract extension until fall or winter.” Kirby Horst, Lebanon County dairy producer: “The thought of looking out at the pastures and not seeing the cows … I don’t know if I can handle that.”

Kirby Horst, Lebanon County dairy producer: “The thought of looking out at the pastures and not seeing the cows … I don’t know if I can handle that.” Dr. Bruce Keck, Annville-Cleona Veterinary Service: “Without a contract extension…This is like asking a loaded tractor trailer to turn as fast as a speeding car. It’s not enough time.”

Dr. Bruce Keck, Annville-Cleona Veterinary Service: “Without a contract extension…This is like asking a loaded tractor trailer to turn as fast as a speeding car. It’s not enough time.” Rick Stehr, R&J Consulting: “This is worth fighting for…worth fighting all together for.”

Rick Stehr, R&J Consulting: “This is worth fighting for…worth fighting all together for.”

Rep. Sue Helm: “A group of representatives are writing a letter Dean Foods. We want farmers to stay in contact with us.”

Rep. Sue Helm: “A group of representatives are writing a letter Dean Foods. We want farmers to stay in contact with us.” Rep. Russ Diamond: “We wanted to get Pennsylvania milk into Pennsylvania schools but have been told that with the product stream in Pennsylvania, this is hard to do. This Pa. Milk Marketing Board issue is a hard issue to get to the bottom, and people get very protective of it.”

Rep. Russ Diamond: “We wanted to get Pennsylvania milk into Pennsylvania schools but have been told that with the product stream in Pennsylvania, this is hard to do. This Pa. Milk Marketing Board issue is a hard issue to get to the bottom, and people get very protective of it.” Rep. Frank Ryan: “Keep faith first and foremost and your sense of humor and talk with your bankers. This is emotionally draining and people want to run from it. There is a solution and we need to work together to find it.”

Rep. Frank Ryan: “Keep faith first and foremost and your sense of humor and talk with your bankers. This is emotionally draining and people want to run from it. There is a solution and we need to work together to find it.”

Mike Eby, chairman National Dairy Producers Organization and former Lancaster County dairy farmer: “The media are our friends. We can work with the media to advertise our product in ways the (check off) promotion programs can’t.”

Mike Eby, chairman National Dairy Producers Organization and former Lancaster County dairy farmer: “The media are our friends. We can work with the media to advertise our product in ways the (check off) promotion programs can’t.”