Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

Potential settlement details undisclosed; Case had revealing ‘wins’ over four years, but FMMO 1 map limitations posed problems

By Sherry Bunting, Farmshine, October 2, 2020

BURLINGTON, Vt. – In an unexpected twist this week, the civil antitrust case Sitts et. al. vs. Dairy Farmers of America / Dairy Marketing Services was dismissed on the eve of the jury trial that had been set to begin Sept. 30 in the U.S. District Court of Vermont with Judge Christina Reiss presiding.

A Stipulation of Dismissal with Prejudice was accepted by attorneys for defendant DFA / DMS and the 116 dairy farmer plaintiffs that had opted out of the previously settled Northeast Class Action Antitrust lawsuit to file the civil suit.

The Stipulation of Dismissal with Prejudice docket simply states: “The parties hereby stipulate to the dismissal of the above-captioned action with prejudice,with all rights of appeal waived, and each party to bear their own costs and attorney’s fees.”

A ‘stipulation of dismissal with prejudice’ is a legal term meaning that the case is over and done with and can’t be brought back.

We have learned that the stipulation requires parties to not discuss the terms of the “dismissal”, which means that settlement details will not be disclosed as public information.

Over the four years since the civil antitrust case was filed in October of 2016, some of the 116 plaintiff dairy farmers have since exited dairy farming.

Dairy farmers who looked forward to “a day in court” with a jury hearing evidence about the increasingly concentrated and anti-competitive milk marketing environment they live every day are likely disappointed by this outcome.

But even though this case is over, some ‘wins’ happened over the four years that could accomplish transparency in smaller case filings in the future.

Throughout the four years, information about the alleged antitrust monopsony actions of defendant DFA, and the position of the plaintiffs as dairy farmers, was revealed at intervals during the proceedings.

Judge Reiss’s Opinion and Order exactly a year ago on Sept. 27, 2019 is one example.

Her Opinion and Order on this case in denying in part DFA’s request for summary judgment stated that, “Plaintiffs’ identify evidence that several of Defendants’ agreements violate a 1977 Consent Decree and Defendants’ own Antitrust Policy and Guidelines. A rational jury could find this evidence demonstrates that Defendants’ ‘acquisition of [ monopsony] power’ was through ‘predatory means.’”

In fact, this 58-page Opinion and Order, along with the amicus brief filed by the U.S. Department of Justice as a Statement of Interest in July, have provided support for others to move forward in smaller cases seeking vital financial information about the workings of DFA, the cooperative of which they are members. (More on that in the future.)

The DOJ statement filed in the Vermont antitrust case in July stated that the alleged activities fall outside of Capper-Volstead protections and that the allegations in the case “do not appear to have involved efforts to increase farmers’ bargaining power but rather efforts at monopsonization.”

The DOJ’s 15-page statement filed in July 2020 represents the first time the DOJ has really weighed-in on the monopsonization of milk markets to basically say the “heartland protections” of the Capper-Volstead Act do not apply to the activities alleged.

In fact, DOJ stated in the brief that the claims at issue fell outside the Capper-Volstead protection because “they do not involve claims that farmer cooperatives acted anticompetitively against processors and other middlemen, but rather that these were claims that farmer cooperatives through agreements with processors, middlemen and other cooperatives, acted anticompetitively against other farmers.”

Part of the issue for the plaintiffs in the Vermont antitrust case — throughout the procedural elements of four years — was that exhibits, testimony, depositions about activities just outside of the Northeast Milk Marketing Federal Order One lines on an arbitrary map were deemed outside the jurisdiction of the case.

It is interesting to note that even evidentiary exhibits at the case docket about activities in central Pennsylvania was scratched from use in the trial simply because central Pennsylvania is one of several geographies in the Northeast that are technically “unregulated” by FMMO 1 and thus not included in the FMMO 1 “map” — even though central Pennsylvania is surrounded on one side by FMMO 1’s map and on the other side by FMMO 33’s map, and the milk from these farms moves through these FMMO marketing channels, plants and cooperatives.

So many moving parts to assemble and so many challenges to use information subject to exclusion based on FMMO maps, it boggles the mind.

Similarly, ‘collaborations’ of one sort or another — revealed through exhibits, testimony, depositions and the like — that occurred in other FMMOs linked to how milk markets function in FMMO 1, or showing a pattern of behavior, were also deemed outside the jurisdiction of this case.

This, despite defendant DFA / DMS being a national footprint milk cooperative that interestingly draws its own area council maps in ways that blend geographies between FMMOs. This, despite defendant DFA / DMS in testimony before the Pa. Milk Marketing Board or in requests made to FMMO 1 market administrators often positions itself as the all-knowing one on milk flow from its birdseye view of the national, even global, dairy grid.

A basic tenet of the case was plaintiff’s claim that DFA is ’empire-building’ not bargaining on behalf of farmer members. During the four years of process on this case, information has been revealed, but DFA has continued to boldly forge its dairy dominance by aggressively bringing the Northeast regional cooperatives and independents that had been market-managed by DMS into the milk supply membership structure of DFA-proper 2017 through 2019, and then acquiring 44 of Dean Foods’ 57 fluid milk plants across the country in 2020.

DFA was listed by Rabobank last month as the largest dairy processor in the United States and third-largest dairy processor globally behind Nestle and Lactalis.

Through additional partnerships, joint ventures and marketing alliances, DFA has a hand in every pie, and no one, not even its members, really knows how the milk (and revenue) really flows.

By Sherry Bunting (Updated as published in Farmshine, Oct. 1, 2020)

Most of us don’t even know what’s being planned for our futures. Big tech, big finance, big billionaires, big NGO’s, big food, all the biggest global players are planning the Great Re-set (complete with land grab and animal product imitation game) in which globalization is the key, and climate change and ‘sustainability’ — now cleverly linked to pandemic fears — will turn the lock.

The mandatory farmer-funded dairy and beef checkoffs — and their overseer USDA and sustainability partner World Wildlife Fund (WWF) — have been at this global food system transformation table since at least 2008 when DMI’s Innovation Center for U.S. Dairy was formed and put together the Sustainability Alliance for U.S. Dairy.

DMI says there is a difference between WWF-US and WWF-EU, but it’s really one big thing connected to these same global corporations that are driving the emerging government policies of the Great Re-set — like the Green Deal in Europe and the Green New Deal in the U.S.

DMI leaders say WWF is ‘helping’ farmers by providing a seat at the table to be sure sustainability will be profitable.

More light was shed on the ‘we will pay you’ carrot-before-club concept of ‘land banks’ in the U.S., when listening to former Vice President Joe Biden answer a farmer’s question about environmental regulations during CNN’s Town Hall in Moosic, Pennsylvania Sept. 18.

More illuminating yet is the flurry of global food company press announcements in recent days as they position themselves ahead of the Sept. 30 United Nations Biodiversity Summit in New York City. That’s where global leaders and the global business community will adopt targets to “restore” (re-wild) 30% of the earth’s land as Protected Areas by 2030 and 50% by 2050.

That’s half the world’s land by mid-Century, and leading this charge is WWF, along with companies like Walmart, Amazon, Nestle, Danone, Unilever and others involved in checkoff-funded pre-competitive collaboration through DMI’s Innovation Center for U.S. Dairy.

According to Survival International, an organization defending indigenous people and smallholder farms, these 2030 and 2050 sustainability targets of the Great Re-set “will be the biggest land grab in world history and will reduce hundreds of millions of people to landless poverty.”

The new narrative is that this massive target of land transfer is needed not just to “restore a trillion trees” as carbon sinks to cool the earth, but to end the Covid-19 pandemic and prevent future pandemics by creating more separation between humans and animals to avoid zoonotic disease transfer. These land targets call for a “critical overhaul of the food production system,” according to the summit agenda.

Even as California wildfires burn out of control — collectively emitting more GHG than tens of millions of cars annually and largely influenced by environmental policies that have led to neglect of the forests in terms of land management — re-wilding of more land is big on the Great Re-set agenda.

Meanwhile, as consumers prioritize health and economics over the ‘planetary diets’ hatched by the Silicon Valley billionaires funding fake meat and fake dairy, the ‘biodiversity’ angle on these land targets is the new hook linking pandemic fears to climate action and the UN Sustainable Development Goals (SDGs) through diet.

Some of the themes are familiar in dairy industry discussions about DMI’s Sustainability Framework and Net Zero Initiative — both rooted in the Great Re-set they have been participating in planning for over a decade through alliances with WWF and its World Resources Institute doing the benchmarking for the global corporations driving it.

(Remember Starbucks’ announcement earlier this year? They are a DMI partner, and so is WWF, but after their WRI benchmarking, they announced ‘moving consumers away from dairy and toward plant-based options’ in their coffee beverages as the biggest of four areas of action! They even borrowed the ‘flat white’ name reserved for their lattes made with whole milk instead of default reduced fat milk to launch a new signature almond-‘milk’ latte. Talk about confusing the customer into making a choice desired by the diet-and-sustainability-elite-ruling-class.)

During a recent DMI ‘open mic’ call, CEO Tom Gallagher stated that these are the rules today and globalization is the world we live in. On the same call, president Barb O’Brien revealed dairy checkoff’s 13-year alliance with Walmart, a two-year partnership with Amazon, and on the Net Zero Initiative, she frequently mentioned Nestle, Unilever, Danone and Starbucks.

What do they all have in common?

They are the key global brands ramping up into plant-based and cell-based dairy and meat alternatives, and they are among the top global corporations that have set goals to ‘move consumers to planetary diets’ and to change the way food is produced.

“What we are talking about is massive transformation of societal systems — financial services, retail consumer goods, the things we bring into our home to eat or to wear or to decorate our homes with. Changing the way all of that gets produced is a massive systemic undertaking that will take business action. It will take philanthropy. It will take government action,” she said.

McLaughlin cited Danone, Nestle and Unilever as the suppliers “in the lead” on this.

livestream screenshot

“This is total ecosystem transformation,” said McLaughlin. “Our suppliers have stakeholders wanting this, and if there isn’t alignment among their stakeholders (for instance dairy), they are glad to be able to say: ‘Hey, Walmart wants us to do this so we have to do it.’ We help them figure out what to do and how to go faster on some of these things.”

She referenced Walmart’s Sept. 18 announcement that it will be net-zero by 2040 and will become a “regenerative” company “restoring” land to meet 2030 and 2050 targets.

“We will work at the landscape level with suppliers and philanthropy to restore 50 million acres of land — to change the way it gets managed, to decarbonize the supply chains, and change the way consumer products work in retail, as an industry, with traceability and transparency tools,” said McLaughlin.

She talked about Walmart having projects already for all three scopes of the Environmental, Social and Governance reporting (ESGs) that are being mainstreamed into financial markets in 2021. This is how the flow of capital will go to companies progressing toward these global targets.

McLaughlin talked about working with WWF to implement more standards and more certifications for suppliers and to move away from “segregated commodities” to “blended approaches” that use global traceability and transparency systems and document ESG reporting and progress on the SDGs each step of the way.

“It is clear we are exceeding boundaries of the planet, and as a company that sells food and apparel made of cotton, the business case is clear for the SDGs, said McLaughlin.

Asked what is Walmart’s ‘why’? McLaughlin revealed: “The benefits are clear: cost reductions, supply security, risk management, so that’s why we’re doing it.”

livestream screenshot

Speaker after speaker and company after company throughout the WEF Forum talked about how all business sectors will be collaborating on these global ESGs (capital) and SDGs (land).

Kristina Kloberdanz, Chief Sustainability Officer for MasterCard even talked about using their platform of over 3 billion customers interacting with retailers and merchants to “inform, inspire and enable consumers to take action, themselves, against their own carbon footprint.”

What is clear is that consumers will be led to where global companies want them to go. These global business leaders stated that “moving consumers” (not just suppliers) toward these goals is what they are working on.

livestream screenshot

Bank of America’s CEO Brian Moynihan (top, center), who is also chair of the International Business Council, sat with heads of the four big accounting firms in one of the WEF livestream sessions about the launch of Stakeholder Capitalism Metrics, which they affectionately refer to as “accountant as activist” or “warrior accountants.”

Moynihan said that financial accounting for the investment sector — even lending — will be predicated on progress toward carbon-neutral and carbon-negative goals.

A glimpse of how land targets would be set in the U.S. was seen in former Vice President Biden’s response to a farmer’s question at the CNN Town Hall in Pennsylvania about environmental regulation, referencing the Obama-era WOTUS rules and the Green New Deal.

“We will have land banks,” said Biden. “You will be paid to put your land in land banks to create open space and be in a position where you will be paid to grow certain crops we want you to grow to sequester carbon from the air.”

He talked about his home state of Delaware with a $4 billion poultry industry and stated that, “manure is a consequence of chickens and it is polluting the bay. But we recently found out we can pelletize the manure and remove the methane,” said Biden.

Though Biden states that his climate policy is not the Green New Deal, the overlaps are there. The Green New Deal includes such references to “land banks”, where government will purchase land from “retiring farmers” and make it available “affordably to new farmers and cooperatives that pledge certain sustainability practices.”

Analyses of the Green New Deal’s land policies suggest rented ground — which comprises up to 40% of agricultural land — would be targeted first because environmentalists assume the active farmers renting this ground don’t care as much about its stewardship because they don’t own it.

Landlords who rent ground to active farmers and ranchers for cropping and grazing are easy targets for such a plan.

However, on the production side, rented ground is incredibly important to active farmers in many dairy states, like Pennsylvania and Wisconsin, for example, and it is how new and beginning farmers get a start.

The Great Re-set driven by climate goals and sustainability linked to pandemic fears and the Covid-19 impact on the global economy holds significant impacts for food and agriculture production. The “solutions” we see discussed are things former Secretary of Agriculture and current DMI executive Tom Vilsack has worked on for at least 13 years, maybe longer.

DMI leaders tell farmers that they are the reason farmers have a voice at the table to keep regulations from coming in that are unprofitable. But more apparently, DMI leaders are at the table helping to shape the dairy re-set that mirrors the global Great Re-set as pursued by WWF and global corporations like Walmart, Amazon, Nestle, Unilever, Danone. They are driving food system transformation in the Great Re-set — a one-world-order clothed in climate goals.

DMI has longstanding alliances with these partners, including WWF. But whose interests are counted at the table where the food system transformation game is being played? The global companies that partner with checkoff through DMI’s Innovation Center for U.S. Dairy and its Sustainability Alliance? Or the farmers mandatorily funding DMI’s existence?

Are farmers and ranchers really at the table? Their powerful integrator (checkoff) and buyers (global processors) most certainly are.

Who will stand for farmers and consumers at the grassroots level? What happens when food production is fully integrated and digitized under globalized control by fewer entities? The role of USDA’s Dietary Guidelines is just the tip of the iceberg, facilitating dietary control of the masses through institutional feeding — working to move us all to the pre-ordained ‘planetary diets.’

The public at large has no idea what’s coming and how their food choices are being manipulated.

Given DMI’s alliances with the big players in food system transformation, the answers should be clear.

Time for transparency on where dairy checkoff’s partnerships are leading

By Sherry Bunting, Farmshine, August 28, 2020

Partnerships and proprietary information stop many conversations from moving forward when it comes to the direction of dairy checkoff leadership under Dairy Management Inc. (DMI).

Meanwhile, contrary to DMI CEO Tom Gallagher’s assertions in the Aug. 5 ‘open mic’ call, consumers DON’T know the nutritional benefits of milk. That’s why grassroots efforts to promote milk (like the Drink Whole Milk 97% Fat Free effort) get so much action. People really know very little about milk and dairy after decades of dairy farmers spending hundreds of millions of dollars annually in promotion and education.

But that’s okay, according to Gallagher, DMI is a supply chain expander.

We keep hearing this theme that consumers will deal with fewer players, shop at fewer stores, become less brand-loyal, learn to accept pre-planned food categories and assortments, realize ‘generics’ are just as good as brands, and will focus more on how diets affect the planet, while spending more for new innovative products… We have to stop a minute and wonder:

What does all of THAT mean?

First off, the math is not adding up.

More than one report or webinar has hit on the indicators showing consumers are focused on food purchases that address their concerns about health and economic value, and they are finding comfort in traditional choices – like real milk and dairy products.

Furthermore, the food disruptions of the pandemic have created more interest among consumers in where their food comes from – is it local, regional, produced in the U.S.? They are more in touch with the importance of local and regional food systems, and less keen on global supply chains nor globalization — not just of food, but also medicine and other necessities.

While rank-and-file consumers and farmers find opportunity and security in building localized or regional food systems, that is the last thing the big players want to see happen. So what do they do? They mine consumer data, something DMI will help with, to twist consumers’ health- and value-focused concerns to fit a ‘planetary’ values system that steers consumers straight into the jaws of the global suppliers that have checked all their pre-planned criteria boxes.

They want consumers to prioritize planetary diets so supply chains can be centralized and globalized — pure and simple — and our own industry checkoff organizations are participating at best, helping them accomplish it, at worst.

In fact, the “good for the planet” mantra — as defined by World Wildlife Fund (WWF) and its World Resources Institute (WRI) is what global corporations and Silicon Valley tech food investors are all about. They are creating the boxes, checking them off, and then trying to convince consumers that this is what is important to them when making decisions about their food.

Data clouds, omnichannel marketing, digitized food, personalized experiences, purpose-driven marketing, planetary diets – these are but a few of the buzz terms and technologies driving future of food transformation.

Through GENYOUth, the dairy checkoff is actually facilitating transformation, grooming schoolchildren to make choices that will eventually pad the wallets of billionaire tech-sector food investors and give them control under the guise of planetary diets and climate change. The future-of-food players need a global ‘value-driver’. It was climate change.

Then came Covid, and people were forced home and began to turn inward to the health and economic needs of themselves and their families. They began to see the importance of communities and began to recognize that farmers are connected to their communities.

To bring them back “on-task”, WWF recently launched a campaign to link Covid-19 to the already set goals. In fact, according to its website, WWF explains that, “A big possible casualty of COVID-19 are the world’s Sustainable Development Goals (SDGs).

In a July 22 report on the pandemic and planetary health, WWF scientist Robin Naidoo states that, “In 2015, the United Nations adopted (Sustainable Development) goals to improve people’s lives and the natural world by 2030.The success of these SDGs depends on two big assumptions: sustained economic growth and globalization.

“COVID-19 has now torn both assumptions to shreds,” the WWF report states. “This has fundamental implications for how we conceive of and prioritize sustainability in a post-pandemic world.”

The report then goes on to twist the narrative on these UN SDGs (that are also part of DMI’s Net Zero Initiative) to say 30 of the targets “would help to lessen the likelihood of another global pandemic.”

Like a chameleon, the big players adapt the plan by changing the picture to shift consumer focus back onto the planetary diets and by honing in on post-Covid concerns about health and economics from a different angle. Easier to do this when people do not know much about milk and dairy.

Yes, there is a tug of war emerging from the pandemic in which consumers seek and grassroots farmers can deliver real, whole, healthful foods in regional, national and international food systems that are in direct competition with centralized global supply chains that want to streamline, limit options and control diets.

While DMI leaders are busy convincing dairy farmers to get with the program of unified marketing in order to compete – as one — in a big marketplace, what is DMI actually doing with their empowerment?

— DMI has a close working relationship with WWF to write the rules of the ‘sustainability’ and ‘net-zero GHG’ playbook – the driver.

— DMI’s marketing and public relations contractor Edelman has close ties to WWF, the EAT Lancet forums, and is developing new terms for brands in the plant-based alternative milk sectors.

— DMI partners with DFA to help launch a 50% milk 50% oat or almond juice beverage with pretty packaging and marketing that make it appear superior to the milk produced and bottled from dairy farms.

— DMI’s GENYOUth program facilitates access to schoolchildren so global corporations and other partners can groom schoolchildren into future decision-making consumers focused on “planetary diets” – their global value system.

— DMI recently hired a digital food and cellular ag proponent as its vice president of Dairy Scale for Good. Caleb Harper’s hiring has brought many questions but is merely one more cog in the supply chain wheel being built with dairy farmer checkoff money. His focus will be large dairies. His background is controlled environment horticulture through computerized plant boxes that several science publications, and even public radio, pointed out were “smoke and mirrors.” His father has ties to the early rendition of fairlife through Mike McCloskey, and both Harper and McCloskey are part of WWF’s thought leadership group

Innovation is normally something to be enthusiastic about. Technology is progressive and something farmers embrace. Competition is healthy and provides entrepreneurial opportunities.

But when it comes to mandatory promotion dollars, gone are the days of managing content that everyone can see, as it all goes digitally underground to meet proprietary consumer targets of partners. Gone are the days of education to promote the benefits of dairy to meet the needs and questions of consumers.

When farmers are forced to fund an entity with the power to set parameters on how they do business, an entity that is overseen by USDA and yet is partnered with activist groups, large multinational companies and global supply chain consolidators, and an entity that can pay for research that then becomes proprietary and could involve diluted dairy products such as butter that is mostly water, and an entity that begins to see its role as the expander of the supply chain… yes, transparency and vigilance are most definitely needed.

By Sherry Bunting, Farmshine, Sept. 11, 2020 and preview Sept. 18, 2020

Whole milk sales up 6.5% Jan through May, total milk sales flat

While consumer packaged goods (CPG) reports indicate fluid milk sales being up 4 to 5% through the Coronavirus pandemic — and flattening as of the end of August back to year ago levels — the other side of that coin is the loss of institutional, foodservice and coffee house demand. Thus, the extra CPG sales at supermarkets slightly more than covered the lost usage in foodservice and the net wholesale volume of fluid milk sales reported by milk handlers January through May 2020 was virtually unchanged (up 0.2%) compared with a year ago, according to USDA.

Within that volume are some important shifts. Conventional fluid milk sales to all uses were down 0.5% vs. year ago in the first 5 months of 2020 while organic fluid milk sales were 14% higher than a year ago.

Within the conventional milk sales, whole milk was up 6.5% and reduced fat (2%) milk was up 3.3%. Also gaining in sales January through May 2020 were “other” fluid milk sales, which includes ultrafiltered milk such as Fairlife, up 10.5% vs. year ago.

The big losers were fat free milk down 12% from year ago and flavored fat reduced milk down 22%.

These numbers were reported in the most recent USDA product sales report. Given that this included the mid-March through early May period when shortages and purchase limits were put on fluid milk in many stores throughout the country, it will be interesting to see June and July data when they are reported in the next 30 to 60 days.

Clearly, consumers are shifting even more strongly to whole and 2% milk and away from 1% and fat-free milk. With organic sales also experiencing sales increases, it is a sign that consumers are looking at health indicators, and a sense for wanting what’s real, natural and perceived to be most local when choosing milk for home. At the same time, overall sales of conventional milk are negatively impacted by the steep drop in institutional, foodservice and coffee house demand.

Class I milk markets get demand push from gov. purchases

At the wholesale milk handler level, USDA reports tightening milk supplies in the eastern U.S. relative to Class I usage. Specifically, the USDA Eastern Fluid Milk and Cream Report Wednesday, Sept. 9 indicated Class I sales picking up this week in the Northeast with balancing operations receiving steady to lighter milk volumes compared with recent weeks.

In the Mid-Atlantic region, milk reported to be adequate for Class I needs, and loads traveled to the Southeast for immediate needs as USDA reports Southeast milk production is tight and output is down with most milk loads clearing only to Class I plants and no loads to manufacturing.

USDA reports production of seasonal milk beverages such as pumpkin spiced flavored milk and eggnog have begun to pick up.

USDA reports that the steady to higher Class I demand is due to some schools returning to session along with government programs purchasing extra loads from manufacturers this week. In fact, reports USDA, bottlers in eastern markets are receiving milk from other regions, which is loosening up the previously tighter cream availability.

Block cheese rallies past $2/lb, but futures rally is short-lived

Cheese markets made significant gains for the third week in row, fueled in part by the third round of USDA CFAP food box purchases for delivery October through December 2020.

On Wed., Sept. 9th, 40-lb block Cheddar was pegged at $2.1575/lb — up 25 cents from a week ago with a single load trading. The 500-lb barrel cheese price was pegged 10 cents higher than a week ago at $1.67/lb, with zero loads traded. The barrel price had reached $1.70 earlier in the week before backing down Wednesday, taking early week futures market gains along with it.

The block to barrel spread is at its widest level of 48 cents per pound, an indicator of cheese market vulnerability and volatility for the longer term. Butter loses cent, powder gains cent

Spot butter lost a penny with a significant 13 loads trading Wednesday on the CME spot market, pegging the price at $1.50/lb. Nonfat dry milk gained a penny at $1.0425/lb with 3 loads trading.

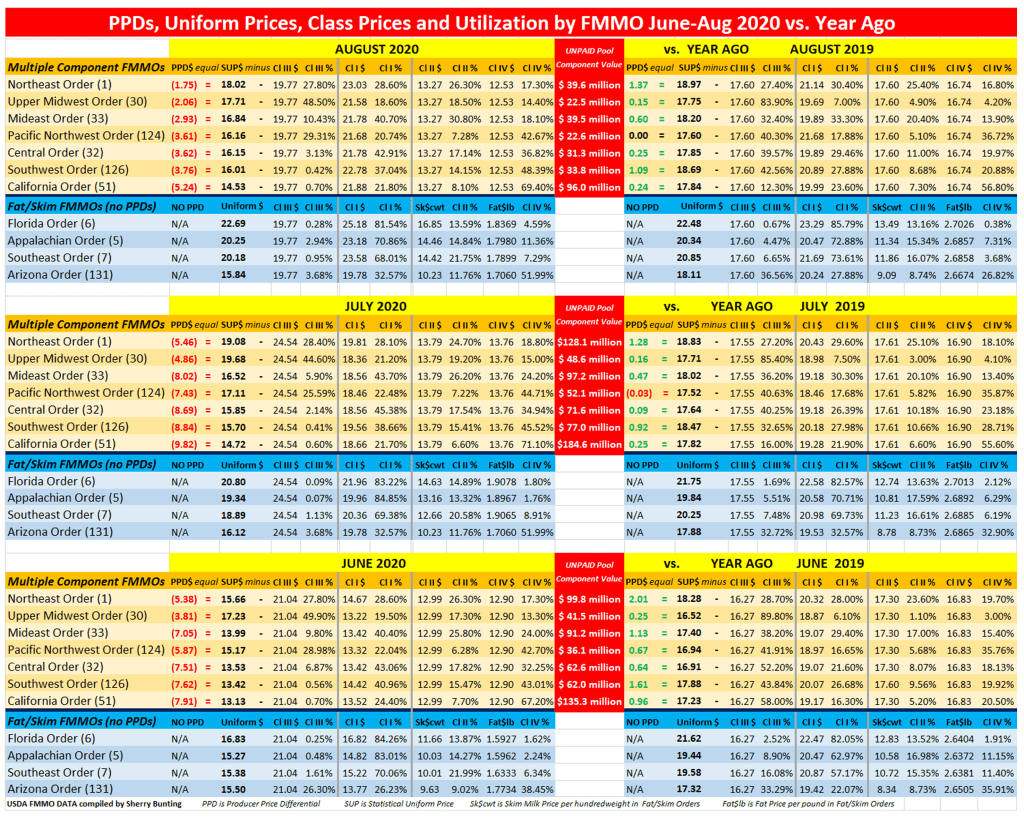

Negative PPDs persist, unpaid component value across 7 MCP Orders totals $1.47 billion for June through August milk

Look for more on this in the 9/18 Market Moos in Farmshine, but for now, here’s a chart I’ve compiled showing relevant information for August, July and June 2020 vs. same month year ago in 2019.

The bottom line is three months of significantly negative PPDs resulted in $1.47 billion in total unpaid component market value across the 7 Multiple Component Pricing Federal Milk Marketing Orders.

Losses were also incurred by the 4 Fat/Skim Pricing Orders but are not easily quantified on the FMMO pool balance sheet.

This has cost dairy producers even more who have paid to manage risk through a variety of tools because those tools only work when the milk check follows the market higher to provide the protected margin. When the market says ‘no fire here’ but the house burned down just the same, it’s a double-whammy.

Remember, fluid milk does not have a ‘market’ because it is regulated or used as a loss-leader by the nation’s largest supermarkets. Thus, the value of the components in fluid milk can only be market-valued in the other products made with milk that “sort of” have a market. When that market rallied, the value was pulled instead of pooled.

Instead of ‘band aid’ approaches to milk pricing reform, given the Class I change made in the 2018 Farm Bill has been a disaster, it’s long past time for a national hearing on milk pricing with report to Congress.

Read on, to see how other factors such as imports vs. exports affect storage anc contribute to unprecedented market misalignment.

Close-up Cl. III / IV spread widens, average for next 12 months narrows

The spread between Class III and IV milk futures widened to a $4 to $5 spread for September and October, $2 to $3 for November and December. But the average over the next 12 months for both classes in CME futures trading has narrowed this week.

The Class III futures contract for September traded at $16.62/cwt Wednesday, Sept. 9 — fully steady with a week ago while Class IV traded 15 cents lower than a week ago at $12.83.

October’s Class III futures contract traded at $18.48 Wednesday, down 54 cents from a week ago, while Class IV traded at $13.64, down 40 cents.

The next 12 months of Class III milk futures closed the Sept. 9 trading session at an average $16.68 — down 24 cents from a week ago.

The next 12 months of Class IV futures averaged $15.03 — down 4 cents from a week ago. At these midweek trading averages, the spread between Class III and IV over the next 12 months averages at $1.65/cwt — 20 cents tighter than the previous Wednesday.

Import-Export factors affect storage, which in turn affects markets

As mentioned previously, the most recent USDA Cold Storage Report showed butter stocks at the end of July were up 3% compared with June and 13% above year ago. Total natural cheese stocks were 2% less than June and up only 2% from a year ago. Bear these numbers in mind as we look at exports and imports.

According to the U.S. Dairy Export Council (USDEC), total export volume is up 16% over year ago year-to-date – January through July. For July, alone, total export volume was up 22% over year ago. Half of the 7-month export volume was skim milk powder to Southeast Asia. January through July export value is 14% above year ago.

However, butterfat export volume averaged 5% lower than a year ago year-to-date. The big butter export number for July was not enough to make up for the cumulative decline over the previous 6 months.

On the import side, the difference between cheese and butter is stark. Cheese imports are down 10% below year ago, but the U.S. imported 14% more butter and butterfat in the first 7 months of 2020 compared with a year ago.

The largest increase in butter and butterfat imports occurred in the March through June period at the height of the pandemic when retail butter sales were 46% greater than year ago.

Looking at these butter imports another way, is it any wonder butter stocks are accumulating in cold storage to levels 13% above year ago at the end of July — putting a big damper on butter prices and therefore Class IV?

The U.S. imported 14% more butter and butterfat and exported 5% less butter and butterfat year to date while storage has been running double-digits higher, up 13% at the end of July.

As accumulating supplies pressured butter prices lower, the U.S. became the low price producer and exported a whopping 80% more butter in July compared with a year ago. This was the first year over year increase in butter exports in 17 months. But the record is clear, year-to-date butter exports remain 30% below year ago and total butterfat exports are down 5% year-to-date.

Analysts suggest that butter and butterfat imports are higher because U.S. consumer demand for butterfat has been consistently higher — even before the impact of the Coronavirus pandemic stimulated butter demand for at-home cooking and baking.

This reasoning is difficult to justify — given there is 13% more butter currently stockpiled in cold storage vs. year ago keeping a lid on the wholesale prices (while retail prices rise) and undervaluing butterfat and Class IV milk price in the divergent milk pricing formula. If 14% more butter and butterfat are being imported, does this mean we need to import to serve consumer retail demand and keep larger inventory at the ready to serve that retail demand?

If so, why is the inventory considered so bearish as to hold prices back and thus amplify the Class III and IV divergence?

Does month to month cold storage inventory represent excess? Or does it simply represent a difference in how inventory is managed in today’s times, where companies are not as willing to do “just in time” and “hand to mouth” — after they dealt with empty butter cases and limits on consumer purchases at the height of the pandemic shut down this spring.

The trade has not sorted out the answers to these questions.

Meanwhile, these export, import, and government purchase factors impact the inventory levels of Class III and IV products very differently — and we see as a result the wide divergence between Class III and IV prices and between fat and protein component value.

Interestingly, USDA Dairy Programs in an email response about negative PPDs that have contributed to the wide range in “All-Milk” prices, says the higher value of components “is still in the marketplace” even if All-Milk and mailbox price calculations do not fully reflect it across more than half of the country.

Rep. Thompson and Keller want Whole Milk choice for WIC

The American Dairy Coalition, a national organization headquartered in Wisconsin, applauded Congressmen Fred Keller and G.T. Thompson, representing districts in Pennsylvania, for recently introducing a bill designed to offer an expanded variety of dairy products, including 2% and Whole fat milk, to participants of the Special Supplemental Nutrition Program for Women, Infants and Children (WIC). The bill, officially titled, “Giving Increased Variety to Ensure Milk into the Lives of Kids (GIVE MILK) Act,” would expand WIC offerings.

The Grassroots Pa. Dairy Advisory Committee joins the American Dairy Coalition in thanking Congressmen G.T. Thompson and Fred Keller for their dedication to trying to help nutritionally at-risk Americans have the ability to choose what dairy products fit the taste preferences of their families. Thompson is prime sponsor and Keller a co-sponsor along with 39 other members of Congress on another bill — the Whole Milk for Healthy Kids Act, H.R. 832 — aimed at allowing whole milk choice in schools too.

Current Dietary Guidelines have stifled Whole milk choice by recommending 1% and fat-free milk for children over 2 years of age even though Whole milk provides a nutritionally dense, affordable and accessible complete source of protein that children love.

Science shows consumption of these products promote a healthy weight in both children and adults and fends of chronic diseases.

“More initiatives such as the GIVE MILK Act are necessary to change the antiquated and unscientifically based notion that saturated fats are dangerous to public health,” states a press release from the American Dairy Coalition. “We encourage all members of the dairy industry to not only support the GIVE MILK Act, but also encourage their legislators to urge the Dietary Guidelines for Americans also be updated to remove caps on saturated fats, allowing once more the choice of whole milk in public schools. Children deserve the best — let’s give them whole milk!”

Look for more next week on what the Grassroots Pa. Dairy Advisory Committee and 97 Milk are working on to get the word out to “Vote WHOLE MILK choice in schools — Citizens for children’s immune-boosting nutrition.”

DMI leaders give Net Zero, ‘sustainability’ overview

By Sherry Bunting, Farmshine, September 11, 2020

CHICAGO, Ill. – A month ago, after Farmshine revealed the background of DMI’s new Vice President of Dairy Scale for Good, questions and concerns voiced by dairy farmers led DMI to announce it would have one of its monthly “open mic” calls specifically on the topic of Sustainability and Net Zero Initiative (NZI).

That was Sept. 2, but unlike previous calls, Farmshine was not included among trade media.

This is not surprising because Farmshine has obtained a copy of a communication sent to dairy checkoff board members stating in print that the DMI board has agreed not to engage with Farmshine, stating that Farmshine articles misrepresent their facts.

This position came after two well-sourced articles were published in Farmshine about Caleb Harper, of Vice President Dairy Scale for Good, who was hired by DMI to work with large farms to scale sustainability practices as part of the Net Zero Initiative. The articles revealed concerns about his background in science, funding and future of food philosophy.

Farmshine has obtained a link to the recording of the Sept. 2 open mic call on sustainability that was part of a DMI e-newsletter. However, only 35 minutes of the hour-long call were shared with farmers. The recording was cut at the end of presentations by DMI CEO Tom Gallagher, President Barb O’Brien and Vice President of Sustainability Karen Scanlon.

Thus the recording excluded the 25 minutes of questions and answers, despite Gallagher’s assertion that he would “make sure to get this information into the trade media to communicate with producers and clear up misperceptions that have been perpetrated.”

During the recorded presentations, Gallagher stated that, “The industry — as an industry — has recently made commitments to be carbon-neutral by 2050.”

While he did not get into specifics, he said he wanted dairy farmers to understand the big picture.

He said the dairy checkoff has been involved in this effort 13 years in the role of science, research, and outreach to the supply chain.

Gallagher sought to assure farmers that the first order of business is to “recognize and promote how dairy farmers have been and continue to be stewards of the environment.”

He said the next thing is to make sure consumers and thought leaders understand that sustainability must be profitable for farmers.

He said that the NZI does not mean every dairy plant or every dairy farm will achieve carbon-neutrality. “We want to say that as an industry we are carbon-neutral. That’s our perch,” said Gallagher.

Lastly, he said, “We want to avoid having farms and companies and co-ops use sustainability as a marketing advantage (in competition with each other).

“We should stick together on this, because our competition is others — cell based ag and plant-based beverages — so let’s not beat each other up on this,” said Gallagher.

(Yet DMI hired a key Net Zero employee with ties to cellular agriculture and digital agriculture and funded a new product “innovation” that is half milk and half almond or oat beverage made by DFA in pretty cardboard cartons using buzz terms like “purely perfect blend.”)

“When we went into this 12 to 13 years ago, it was still emerging what sustainability is — and it is still sometimes vague — but from a consumer standpoint, they are focused on sustainability,” said Gallagher.

Later in the call, he stressed the importance of sustainability saying 80% of consumers are focused on it, but then confirmed a bit to the contrary what various consumer surveys show for actual decision-making factors: Number One is still ‘taste,’ followed by number two ‘price,’ and even Gallagher states that nutrition and sustainability are “tied for third.”

He was vague on that nutrition and sustainability distinction and took issue with anyone claiming consumers need more education on dairy nutrition.

“We have these two great components to our story: nutrition and sustainability,” he said, “I don’t care what others are telling you, we have the data and people already do understand the nutritional value of dairy. Sure, we can remind them, but they know it.

“The piece they are not aware of is the sustainable nature of the dairy industry and dairy farming. They don’t get it, and they’ll buy into the notion that plant-based is more environmentally sound because the consumer – especially millennials and Gen-Z – have made their decision… 80% of them expect companies to invest in sustainability in the next year.”

(Or are 80% of consumers being pushed in this direction by top-down supply chain transformation?)

In fact, even though DMI’s sustainability partner World Wildlife Fund (WWF) has been scrambling to come up with new ways to tie the globalized ‘sustainability’ agenda to pandemic prevention as a hook that gets to the “health” and “economic” concerns consumers really have…. Gallagher went so far as to say: “Covid has had an interesting impact on millennials, Gen-Z and the next generation because the majority feel that Covid is an example of why we need global, big-picture solutions with companies leading the way.

“Covid is not distracting consumers, it is heightening the stakes,” said Gallagher, right out of the most recent WWF and global re-set playbook seeking to get everything back on their track.

O’Brien mentioned the dynamics that are more at play: large global companies like Nestle, Unilever, Danone and Starbucks making sustainability even more important as a priority.

“We at checkoff are positioning U.S. Dairy as a solution to drive a unified approach,” she said. “The good news is we know dairy is and can be a solution with the growing body of research and practice-based proof and an industry-wide plan. We are ready to re-set what people think they know about dairy.”

O’Brien painted a picture of the global landscape in which U.S. dairy will have less access if it is not unified to show industry-wide measurements of sustainable impacts.

Then it became clear. O’Brien said “This is not just about consumers, but also investor groups. They are setting the criteria for measuring sustainable impacts, and they expect companies to more fully disclose impacts that are tied to their businesses.”

She said trillions of dollars are being invested in businesses that can do that, and she said many countries are making legally-binding country-wide commitments to accelerate, and they emphasize the need for the U.S. to voluntarily report its impacts.

“We see our dairy customers like Unilever, Danone, Nestle and Starbucks working to meet these global goals on carbon neutrality, water use, zero waste and hunger initiatives,” said O’Brien. “They need to know where we are at to help them meet their goals against these sustainability metrics.”

(The World Resources Institute, which is inextricably linked to WWF, along with UN benchmarks, are formulating these metrics – a work in progress since 2009 when DMI’s Innovation Center for U.S. Dairy first established its sustainability partnership with WWF, according to the WWF website.)

Gallagher said farmers have been at the table on this, and he presented an overview of the “the plan.” He took issue with dairy farmers who are “against globalization” and with strong words, stated: “My answer to that is we did not create globalization, but those are the rules, and it’s the world we are living in… with very powerful forces that are very much against dairy at play here in the U.S.”

(There is a difference between international trade and ‘globalization.’ Globalization is a more centralized order of things affecting aspects of life, health, resources and economies at an international scale.)

Gallagher confirmed that companies will drive this, and he said that consumers want corporations to drive this. He and O’Brien both talked about DMI’s sustainability partnerships began with Walmart in 2007.

Where the plan meets the farm, Gallagher said the Net Zero Initiative has three categories: Large farms, medium sized farms, and small farms.

“We’re doing something for each of those. Some staff (Caleb Harper) are focused solely on large farms looking at technologies to see if they are financially sustainable,” said Gallagher. “And we have folks working on mid-sized and small farms too. Our focus is the research, and some of our efforts will be foundational to support all farms.”

He introduced Karen Scanlon, DMI’s vice president of sustainability who said dairy’s diversity is a key in the Net Zero Initiative.

“There is no one right way, no prescription on how to achieve our environmental outcomes along with profitability,” said Scanlon. “We are focusing right now on learning what farmers are already doing, and helping to share that with more farmers, so farmers can learn from each other.

“We also want to work with farmers and supply chain partners on demonstration projects to highlight successful technologies, practices and approaches,” said Scanlon.

She mentioned two examples – one in Wisconsin and one in southeastern Pennsylvania as well as talks with producer organizations in Idaho and the Pacific Northwest – where farmers and their cooperatives and other supply chain partners are already doing things that DMI can come in and be part of to find ways to cost-share the ideas to increase adoption among more farms.

“Founded by dairy farmers 12 years ago through checkoff, the Innovation Center for U.S. Dairy put us at the table and we find common ground and set a common set of principles that is a difference maker in the supply chain,” said O’Brien.

She went back to a summit with Walmart in 2007, which led to a deepening of the relationship over time. More recently, in 2018, DMI had a similar ‘summit’ with Amazon and that partnership is underway with DMI as category captain.

“Today Walmart proactively uses the FARM program’s animal care and environmental modules. They are using our programs with farms they contract directly,” said O’Brien, adding that DMI starts with relationships and brings in other companies to align with that. She and Gallagher stressed that dairy checkoff now has a “unified Net Zero plan in place and is coordinating with other industry organizations.”

“There is one plan marching forward with each industry organization playing their own unique role,” said O’Brien. She explained that DMI is engaged in science and outreach to the supply chain and telling the dairy story; NMPF is focused on legislative and regulatory as well as on-farm environmental stewardship; Newtrient is focused on viable technologies and practices to produce new revenue streams; and US Dairy Export Council is focused on export markets and aligning targets with DMI’s thinking on measurement and progress.

“What we have created for dairy farmers over the last decade is ready as sustainability increasingly becomes a requirement for doing business,” said O’Brien. “We must continue to lead in this.”

Before opening it up to questions for the last 25 minutes of the call – which were not shared in the DMI newsletter recording – Gallagher told everyone on the open mic call that this was a 30,000-foot view and if they want more details, DMI could do another open mic call on the topic or find other ways to communicate.

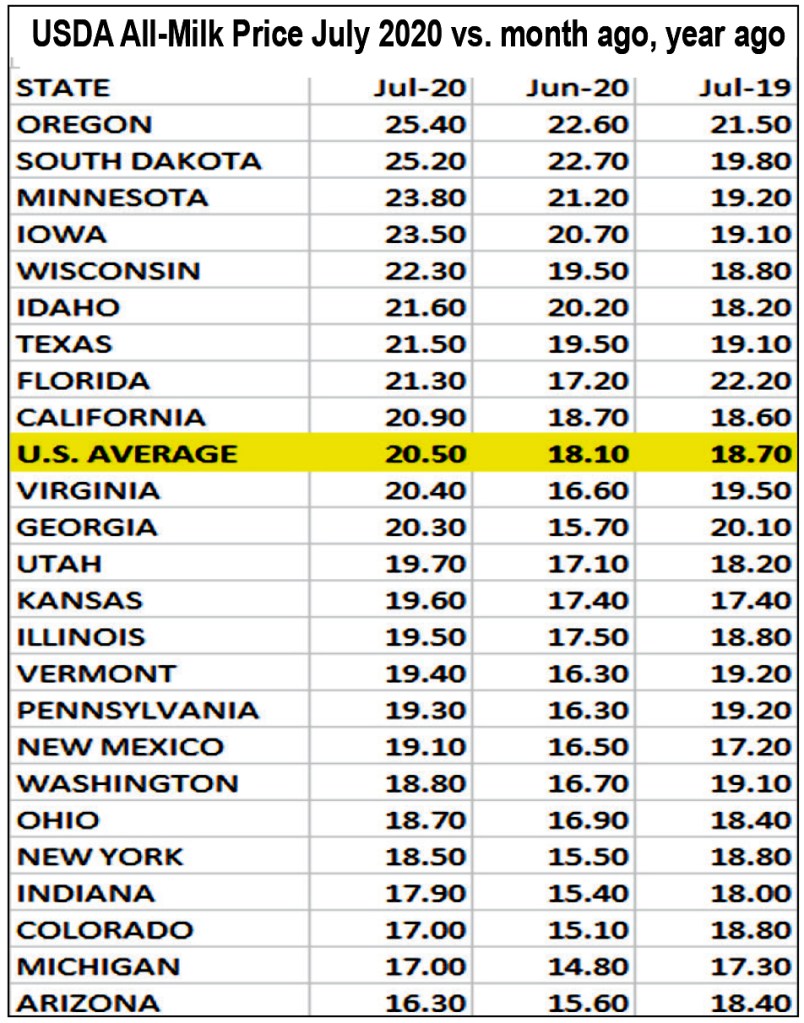

The USDA NASS Agricultural Prices report calculated a U.S. All-Milk price of $20.50 for July, up $2.40 from the June All-Milk price of $18.10 and $1.80 higher than a year ago. With this as the pegged U.S. average milk price, the July Dairy Margin Coverage (DMC) margin was calculated at $12.41, also $2.40 higher than June and $2.91 above the highest level of DMC coverage.

These July USDA numbers are welcome, but tell half the story.

The chart above lists the July 2020 USDA All-Milk price calculations for the top 24 milk-producing states in descending order with the U.S. average highlighted.

What stands out is the range from top to bottom. It has doubled from a more typical $3 to $4 spread to an $8 to $9 spread in June and July 2020. This is the widest we could find on record — with the U.S. average All-Milk price standing fully $4.00 higher than the state with the lowest All-Milk price in June and July 2020 compared with a more typical $1.50 difference a year ago.

A year ago, 7 of the 24 USDA milk production report states were below the U.S. average, a more typical occurrence. In June and July 2020, 15 of the 24 states were below the U.S. average All-Milk price.

On the up-side of the chart, we see that the highest states are $4 to $5 above the U.S. average, when normally that difference would be less than $3.00.

Actual mailbox price calculations won’t be released for five months, and when they are released, the range will likely be even wider from top to bottom than the $8 to $9 spread we see in All-Milk prices the past two months.

Unofficial milk check surveys of volunteered data from dairy producers in six federal orders for June and July show a whopping $14.00 per hundredweight range from top to bottom in gross pay and mailbox net pay.

As for the August All-Milk price, USDA won’t report that until the end of September. We will get Federal Order uniform price announcements for payment of August milk in mid-September. On Sept. 2, USDA did announce August Class and Component prices with Class III (cheese) milk at $19.77, which is $7.24 above the Class IV (butter / powder) price of $12.53. Class II was announced at $13.27. The August protein price was pegged at $4.44 and butterfat $1.63.

Margin ‘equity’ affected by wide spreads

For dairy producers enrolled in DMC — but in regions receiving the lower end of these All-Milk prices in June and July — the safety net program thresholds were not met by the ‘average’ margin even as that margin did not reflect their reality. For dairy producers using a variety of risk management options, new challenges have also emerged in the current market dynamic due to de-pooling of milk making negative producer price differentials (PPD) more negative in some areas.

While the spread between Class III and IV looked like it would narrow this fall, an upswing in Class III futures for October through December contracts this week — and lackluster performance on Class IV — show spreads in manufacturing class values could widen again, which tends to be an incentive for de-pooling in Federal Orders where a mix of products, including Class I beverage milk, are produced.

There are tools to navigate these challenges, say the experts, but a deeper concern is how closely the divergence can be related to the product mix of the CFAP food box government purchase rounds — and changes in U.S. dairy imports.

As the third round of CFAP Farmers to Families Food Box purchases are underway for fourth quarter 2020 delivery, USDA this time set parameters for food box dairy products to be more representative of Class II and IV products, along with the Class III cheese products. In addition, the third round defines the fluid milk in several solicitations to be 2% or whole milk. This will also help with fat value that has plummeted this year.

Still, the majority of government food box purchases continue to be cheese, and the markets responded last week as spot cheddar rallied back above $2.

CME spot cheese pushes higher — past $2/lb, butter and powder steady-ish

Cheese markets gained more than a dime in CME spot trade on Wed., Sept. 2 with 40 lb blocks pegged at $1.91/lb. From there, the market continued to move higher at $2.12 by Friday, Sept. 4, up 30 cents from the previous Friday with zero loads trading; 500-lb barrels were pegged at $1.70/lb, up 27 cents with a single load trading.

Spot butter managed to gain through midweek before losing some of that advance at the end of the week. On Friday, Sept. 4, a whopping 12 loads were traded on the CME spot market with the price pegged at $1.4925/lb — up a nickel from the previous Friday. Nonfat dry milk on the CME spot market gained a penny at 1.03/lb with 6 loads trading Friday.

Milk futures are improving again, divergence continues

Class III and IV milk futures for the next 12 months came a bit closer together, on average, but the fourth quarter 2020 contracts are still divergent as Class III milk futures rallied Wednesday while Class IV was stagnant through yearend.

Trade on Sept. 4 closed with the September Class III contract up $1.37 from previous week at $17.06, October up $1.27 at $18.89, November up 21 cents at $17.55, and December down 12 cents at $16.65. On Friday, Sept. 4, the next 12 months averaged $16.82.

Conversely, yearend Class IV futures closed with the September Class IV contract down 14 cents from a week ago at $12.82, October down a penny at $13.86, November down a dime at $14.39, and December down 9 cents at $14.69. The next 12 months (Sept. 2020 through Aug. 2021) averaged $15.03 on Sept. 4.

The average spread between III and IV over the next 12 months was $1.79/cwt.

Imports/export factors affect storage, which in turn affects markets

The USDA Cold Storage Report released at the end of August showed butter stocks at the end of July were up 3% compared with June and 13% above year ago. Total natural cheese stocks were 2% less than June and up only 2% from a year ago. Bear these numbers in mind as we look at exports and imports.

According to the U.S. Dairy Export Council (USDEC), total export volume is up 16% over year ago year-to-date – January through July – and July, alone, was up 22% over year ago. Half of the 7-month export volume was skim milk powder to Southeast Asia. January through July export value is 14% above year ago.

However, butterfat exports are down 5% year-to-date. The big butter export number for July was not enough to make up for the cumulative decline over the previous 6 months.

On the import side, the difference between cheese and butter is stark. Cheese imports are down 10% below year ago, but the U.S. imported 13% more butter in the first 7 months of 2020 compared with a year ago.

When butterfat and butteroil as well as butter substitutes containing more than 45% butterfat are included in the total, the volume of imports is 14% higher than a year ago with the largest increases over year ago seen from March through June at the height of the pandemic when retail butter sales were 46% greater than year ago.

Looking at these butter imports another way, is it any wonder butter stocks are accumulating in cold storage to levels 13% above year ago at the end of July — putting a big damper on butter prices and therefore Class IV? The U.S. imported 13% more butter and 14% more butter and butterfat combined, plus exported 5% less butter and butterfat year to date.

As accumulating supplies pressured butter prices lower, the U.S. became the low price producer and exported a whopping 80% more butter in July compared with a year ago. This was the first year over year increase in butter exports in 17 months. Still, the record is clear, year-to-date butter exports remain 30% below year ago and total butterfat exports are down 5% year-to-date.

Experts suggest that butter and butterfat imports are higher because U.S. consumer demand for butterfat has been consistently higher even before the impact of the Coronavirus pandemic stimulated a run on butter at stores for at-home cooking and baking. This seems to be a difficult reasoning to justify — given there is 13% more butter currently stockpiled in cold storage vs. year ago.

If 14% more butter and butterfat are being imported, does this mean we need to import to serve consumer retail demand and keep larger inventory to serve that retail demand? If so, why is the inventory considered so bearish as to hold prices back so far as to amplify the Class III and IV divergence? Does month to month cold storage inventory represent excess or simply a difference in how inventory is managed in today’s times, where companies are not as willing to do “just in time” and “hand to mouth” — after having dealt with empty butter cases and limits on consumer purchases at the height of the pandemic shut down.

The trade has not sorted out the answers to these questions.

Meanwhile, these export, import, and government purchase factors impact the inventory levels of Class III and IV products very differently — and we see as a result the wide divergence between Class III and IV prices and between fat and protein component value.

Interestingly, USDA Dairy Programs in an email response about negative PPDs that have contributed to the wide range in “All-Milk” prices, says the higher value of components “is still in the marketplace” even if All-Milk and mailbox price calculations do not fully reflect it across more than half of the country.

BROWNSTOWN, Pa. — For dairy producers managing their market risk, current divergent dairy classes are a problem. Those with Dairy Revenue Protection (DRP) policies in the second quarter of 2020 (April through June) saw the sudden, singular and dramatic rise in Class III — and the negative PPD’s that showed how much of that higher price did not make it into their milk checks — evaporate their DRP claims just the same.

Professionals speaking off the record explain that when Class III milk dropped down to $12 to $13 in April and May, it looked like Class III DRP policies would have “enormous losses” and corresponding claims. But then June hit, and those coverages were wiped out because the policy price, in this case the higher Class III, was averaged over the three months of the policy quarter – even if the policyholder never saw that Class III price in their actual milk check.

DRP policies are purchased to protect a milk price floor on a quarterly, not monthly, basis.

For those producers locking in a price floor with Class IV DRP policies, or a combination of III and IV, high payouts on Class IV policies were realized. In those cases, the DRP offered some coverage and even helped some producers cover at least a portion of big losses in their Class III futures market hedges.

Digging into the complexities, the real crux of the problem is that the movement of the Class III futures market and the USDA-announced Class III price do not reflect the milk check realities of most producers who purchased these risk management policies. That’s a problem.

We’ve all heard the line: “You don’t buy insurance hoping your house will burn down.” This analogy does not apply today. There was a fire, but the market indicators on most types of policies do not recognize the damage.

Professionals who sell DRP indicate they have looked at milk settlement sheets from clients. They have seen all the PPDs for June, and they understand the shortfall projections that could be made worse by massive de-pooling for July milk. They have seen the market realities for their customers.

“What kind of risk management is this if it doesn’t account for how their milk is actually priced?” asks one professional.

In fact, several noted their belief that the USDA and Farm Bureau should look at these disparities, that if PPD is part of the mailbox milk price — as it is actually paid to farmers — then it should be accounted for in the DRP.

One concern shared in several Farmshine interviews is that ag lenders and some feed companies are urging customers to manage risk with DRP to protect their cash flow.

This is hard to do right now as the premiums to purchase DRP have skyrocketed due to the current level of volatility. This is further complicated, say insurers, by the way the Federal Order Milk Marketing system has failed to facilitate the transfer of “value in the marketplace” (according to USDA) to farmers who produced the milk.

In the very time when risk management is most essential, seeing coverages evaporate because the market did not translate value to reality is a double-whammy for those who paid to manage their risk.

Outcomes were also negatively affected for producers who based their DRP policies on components because those PPD levels are reflective of the significant discount between what farmers were paid for their components as compared with how the market valued those components — what USDA states is “value in the marketplace.”

American Farm Bureau Federation’s John Newton explains that, “In multiple component pricing Orders, proceeds from the pool are based on the difference between the classified value of the milk and the component value of the milk — which is effectively the Class III price. When the component value exceeds the classified value, the proceeds from the pool are negative and result in a negative producer price differential (PPD).”

The loss reflected by these PPDs was evident in the performance of second quarter DRP policies based on components. At one point in time, producers saw they had an indemnity coming to cover their milk check losses, the money they expected not to be paid for components because of the market downturn. But then that indemnity evaporated as June components settled higher, wiping out market losses in April and May and simply ignoring milk check losses for June when “the market” failed to pass along the higher component values to most producers in most of the U.S.

Results also varied from farm to farm, depending upon what point in time they purchased their component-based policies. Some component policies for second quarter 2020 paid something. Others did not pay much, if anything, based almost entirely upon what day a producer purchased the policy. In short, these policies did not perform as expected because the cash price paid to producers did not perform according to the “market”.

Another concern shared is farms facing sudden quotas, with little advance planning. Some cooperatives paid their co-op blend price only on 85% of a producer member’s March 2020 level of production for May, June, July, and until further notice. While DRP allows production to be 85% of the insured amount, a producer’s coverage, in many cases, can be negatively affected by what USDA reports as production change for a state or region.

In first quarter 2020 (January through March), for example, Pennsylvania’s higher production almost wiped out some claims.

In figuring milk production by state, USDA NASS looks at Federal Milk Marketing Order pool summaries as part of the production calculation, along with farm surveys. This can be problematic in a time when milk moves farther and more erratically due to supply-chain impacts, volatile futures markets and incentive to de-pool.

If production shows a decline for a producer’s state or region, it can help a claim, and if it shows an increase, this can reduce or eliminate a claim — even if that producer with that policy actually made less milk, not more.

Livestock Gross Margin (LGM), another risk management tool that is available through USDA Risk Management Agency, is seldom used today due to limits on available funding. This product is also affected by the difference between Class III and Class IV in how LGM policies reflect the settlement price, the actual milk income losses.

Newton at Farm Bureau writes that the price risk associated with PPD can only be managed through the terms of a forward contract. The PPD is not “exchange traded” so the risk in this portion of milk pricing is not covered.

Furthermore, according to Newton, DRP and LGM are federal crop insurance policies based on the announced USDA prices, which does not include the PPD because this difference between class and component value and the de-pooling risk that affects it is not a publicly-traded instrument.

While producers report some coverage from DRP by locking in a milk price floor using Class IV, especially at a point in time when Class IV was higher than Class III, this has not been the case when III is higher than IV.

Since DRP is a program that changes each year with some new elements having been implemented to it so far, those working with the program have a variety of suggestions for USDA and Farm Bureau to look at making it a better and more usable product for dairy producers:

1) Address the PPD risk – something should be done about this if it is part of how mailbox milk prices are calculated to producers.

2) Look at making the policies monthly instead of quarterly to reduce the risk of uncovered losses to policyholders and to get them paid sooner.

3) Increase the highest level of coverage to 98 or 99% instead of 95%. A 5% deductible in this market makes DRP unaffordable. For example, at current premium levels, a Class III price of $17.09, insured at 95%, comes out to $16.24 floor. Already this means there is an 85-cent deduction, on average. At a much higher current premium cost of 43 cents, that’s $1.28 to $1.30 before the producer collects anything on a 3-month average. So the combination of production percentage and higher premiums makes for a large deductibl

In short, the problem right now with dairy risk management through federal crop insurance tools and futures markets is the policies and programs and “markets” have so many nuances that are juxtaposed with a Federal Milk Marketing Order system that is inconsistent, not transparent and full of loopholes.

Simplifying both would be helpful, some say. For example, what if insurance products had one sales period and one price discovery period each month to set the deal instead of so many chances to pick the wrong times?

As one professional explained, “If part of the problem is the pricing model, then we can’t throw risk management at that problem… We need to fix the root of the problem. This is not like home-owner’s insurance. There are a lot of factors that go into this.”

When producers pay for risk management, then suffer a loss, but have no or little indemnity because the market indicators say the milk was worth more than what was paid… it’s like having home owner’s insurance when a tornado hits. Your agent looks at your flattened house (milk price settlement sheet), but then has to say he or she is sorry, the adjuster looked at your neighbor’s house as the indicator for tornado damage to your house and his house is still standing.

Dairy farmers are encouraged to learn about DRP, understand it, and decide what application it has to their business in a multi-faceted approach to risk management. Some agents handling the product are not even advertising it because of the current premium cost and these unreconciled “market” issues.

As with any risk management tool, there are critical factors to consider:

1) Know your cost of production,

2) Know your operation’s risk tolerance,

3) Work with an advisor you trust, who understands the tools and communicates with you about them,

4) Consider a blended approach, don’t look at Class III as ‘the market’,

5) Have others in the business to talk to as a sounding board,

6) Take a long-term approach, don’t look just at the short-term,

7) Learn all you can to understand how these tools perform in relation to how your milk price is calculated in your milk market.