By Sherry Bunting, Farmshine, August 19, 2022

HARRISBURG, Pa. — Calls and mailings from the Pennsylvania Milk Marketing Board to small dairy farms processing and selling their very own milk — including those that are permitted by the Pennsylvania Department of Agriculture to sell raw milk — are stirring up a hornet’s nest .

The context of the communications was to get these very small processors to fill out the intrusive applications for Milk Dealer’s licenses, to pay the flat fee, and to do the ongoing monthly milk accountant reporting and calculate and further pay their 6 cents per hundredweight on sales.

To most, this made no sense, given these farms do not purchase milk from other farmers. They do their own pricing based on their expenses — always well above the state-mandated retail minimum — and many are selling raw milk, which is not a general or interstate commerce item.

In the case of raw milk, these producers operate outside of the Federal Milk Marketing Orders, so why is the Pennsylvania Milk Marketing Board (PMMB) coming after them for a Milk Dealer’s license? And why now? Could it have something to do with the bill seeking to collect over-order premium and pool it and pay it to producers directly so that the big players can’t continue to strand some of that premium?

Think about it. The PMMB doesn’t license entities doing cross-border sales of packaged milk whether it was produced in-state or out-of-state to follow the money, but they want small raw milk farms to be licensed Milk Dealers? Something isn’t right.

To their credit, however, the pushback from raw milk producers and citizens has resulted in PMMB putting this licensing effort “on hold”… for now.

Lone Oak Farm, Marion Center, Pennsylvania was one of the small producers to get a voice mail from an attorney identifying himself as a “special investigator for the Milk Marketing Board” wanting to know the name and address to send a packet to fill out.

The packet came. It was the same packet they had received two years earlier — a month before the Covid pandemic — but at that time they were only selling their raw milk and chocolate milk at the farm. They had stated in 2020 that the Milk Dealer’s license did not apply to them and never heard back from the PMMB.

That was the end of it, until August 2022.

This time, the packet included the same letter, along with an intrusive form requiring them to list all of their assets, liabilities — a complete financial statement of personal information — as part of a Milk Dealer’s License application along with monthly forms for calculating their 6 cents/cwt monthly licensing fee and the lesser fee for milk sold through products on which PMMB does not fix a price.

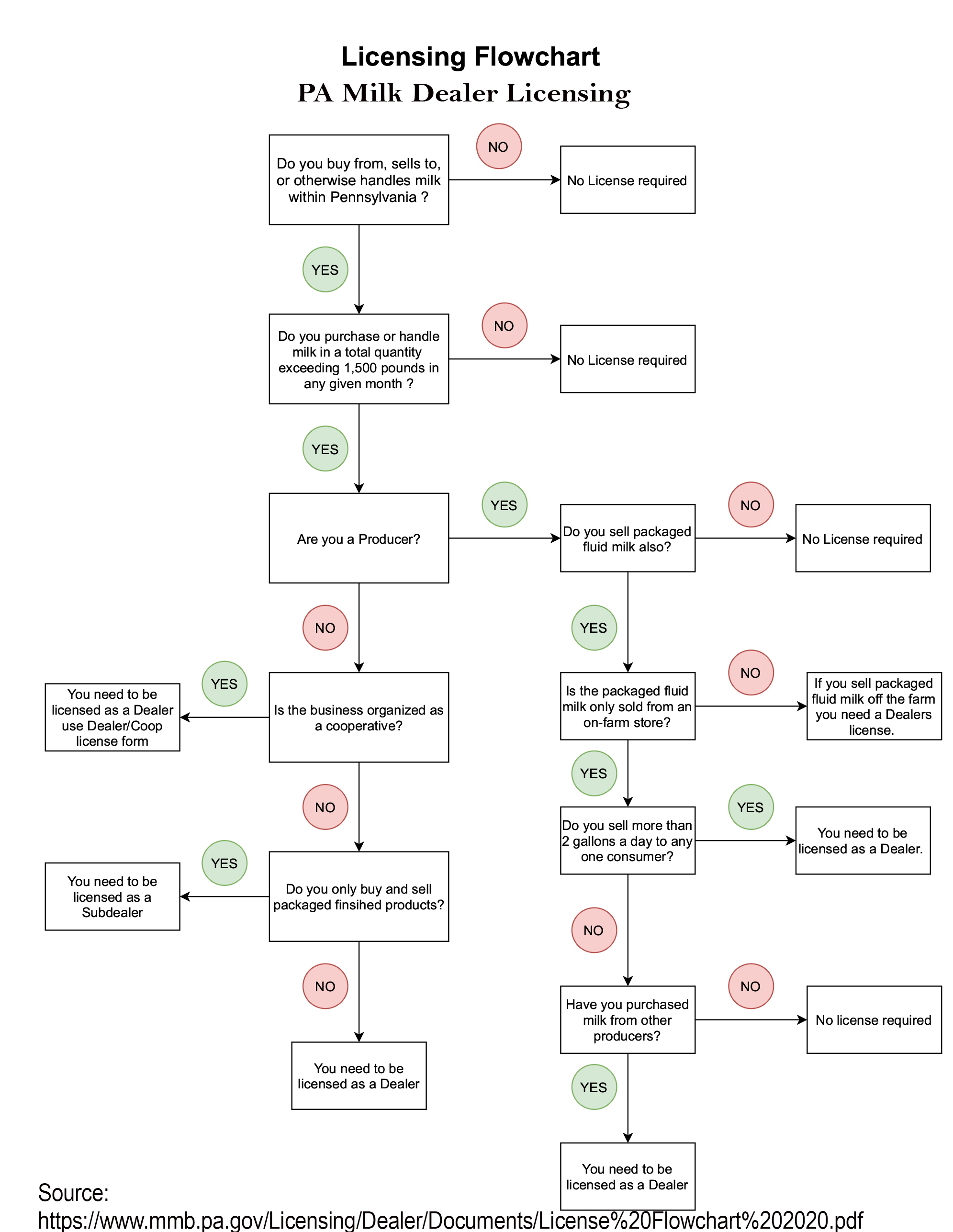

“There was no flow chart to determine if we needed to do this (like is shown below at PMMB website: https://www.mmb.pa.gov/Licensing/Dealer/Documents/License%20Flowchart%202020.pdf). My wife emailed back wanting to know why this pertained to us,” said Aaron Simpson of Lone Oak Farm in an Aug. 17 phone interview with Farmshine. “We were told it pertains to us because we were selling a small amount of milk off site at Back to Nature,” a health store in Indiana, Pennsylvania.

“Someone tipped them off,” he guesses. “We didn’t fill anything out (in the packet), and my wife responded that we would pull our small wholesale account out of Back to Nature rather than jump through these hoops.”

For Lone Oak and other small producers voicing concern, it isn’t even the 6 cents/cwt licensing fee that is the biggest problem, though they believe it is unnecessary. The real problem is the onerous and intrusive forms and the logistics and time it takes to fill out monthly milk accounting to the PMMB. Farms like Lone Oak already applied for and were granted raw milk permits by the Pennsylvania Department of Agriculture (PDA), which inspects them.

Furthermore, as a small producer, with several entities from produce to bakery to milk and more under one umbrella on the farm, the financial statement that the PMMB was requiring was information Lone Oak was not comfortable providing. Why should they? Why is it the PMMB’s business to know their personal business?

“They asked for our entire financial rundown of the farm — as a whole — right down to every asset we own, some of it not even related to the dairy. We are not willing to give that up for a (Milk Dealer’s license),” said Simpson. “This is not how it should be. The only reason we exist is because selling all of our milk conventionally has not been feasible. We are one of three dairy farms left in our township. We are down to the bits and pieces of who makes it and who doesn’t, and that’s been a failure of the dairy industry.”

Most farmers wouldn’t really choose to do customer service as they would rather focus just on farming and taking care of the cows, not running a store. Many have turned to this to preserve their livelihoods, their dairy farms.

“The whole reason we are doing this is because the Milk Marketing Board has failed the farmers, the dairy industry has failed the farmers. How many farms has Pennsylvania lost since 2015?” Simpson pondered aloud. “Within five miles of us, we have lost five or six farms since 2015, so we started selling our own milk with a permit from PDA in 2016.”

Simpson is part of the fourth generation at Lone Oak Farms, milking 40 cows in the same 1960s barn, and diversifying over the years instead of expanding the dairy herd. Now he gets calls from other farmers with all herd sizes wondering how they got started, including large farms wanting to scale back their herd size and get closer to consumers.

When Lone Oak shared their public post to customers on facebook that their raw milk and chocolate milk would no longer be available at Back to Nature, and encouraged their customers in Indiana, Pennsylvania to come the extra 20 miles to the farm in Marion Center, the response was overwhelming.

As the post was shared multiple times, PMMB executive secretary Carol Hardbarger commented that the PMMB staff was looking into what could be done, but that they had to “follow the law.”

The law, according to the flow chart found at the PMMB website (above), stipulates that any dairy farmer selling more than 1500 pounds of milk per month (less than 6 gallons per day) direct to consumers, would have to be a licensed Milk Dealer if they sold any of that milk at a site off the farm or if they sold more than two gallons per day to one customer.

This week, an official response from PMMB executive secretary Hardbarger notes that, “we have officially put licensing of small processors on hold until we decide what to do, sending a letter from me to each not licensed yet, to the ag committees with an explanation, and to PDA.”

But how did this come about and what will happen going forward?

If this requirement is truly part of the law, and if it requires small producers selling their very own milk privately in small amounts must be licensed as Milk Dealers, why have we not heard about it before?

In fact, a Penn State extension educator preparing for a value-added dairy seminar reached out to Farmshine for clarification after reading about the issue in Market Moos last week. She wanted to know why this was never brought to her attention when she asked state agencies for all of the things a small value-added dairy producer needed to know and do to sell milk and dairy products made on the farm. She wanted clarification.

According to Hardbarger, small producers, and those with raw milk permits have received packets and calls in the past, but that a list of raw milk permits was made available to PMMB recently through the online data-sharing that was set up this year between PDA and PMMB now that the weigh-sampler certification work PMMB used to help with has transferred exclusively to PDA. This put the list of raw milk permits directly into the PMMB’s hands.

This PDA list of raw milk permits has always been publicly available and updated online. So why was the action to get small producers to become licensed Milk Dealers started in earnest at this particular time? No clear answer has been given, except that the PMMB is now looking at the situation and putting it ‘on hold.’

Perhaps the biggest players in the industry — that have a stake in preserving the price-regulating and milk-accounting functions of the PMMB — are concerned about the increasing number of Pennsylvania producers going this route outside the system with some or all of their milk. Some dairy farmers are making and selling pasteurized milk and dairy products, others are selling raw milk.

In fact, at Ag Progress Days recently, a panel talked about farm transitions and how important value-added direct-to-consumer sales are for Pennsylvania’s agricultural industry. The Commonwealth has the second largest volume of direct-to-consumer sales of farm products in the U.S., and this is growing as farms are also becoming more diversified, the experts shared.

“As farmers, we don’t need another irritant to yield a pearl for PMMB. This (Milk Dealer’s license) is more administrative paperwork and a check we would need to send every month. It’s one more thing,” Simpson explained, listing all of the things they already do to sell milk through their permit with PDA and in general as dairy farmers.

“Fluid milk is breakeven across the spectrum,” he said. “We have enough irritants in a year’s time, and just that statement about irritants and pearls shows the disconnect between farmers and the PMMB.”

Farmers and dairy professionals around the state are questioning the very low 1500-pounds per month threshold on private sales of milk from farms that pushes these small producers into the category of a Milk Dealer — if any of that milk is sold at a store off the farm.

For example, Lone Oak milks just 40 cows and markets about one-third of that as direct-to-consumer sales of milk, chocolate milk, ice cream and yogurt. The rest goes to United Dairy. They are inspected four times a year for the raw milk permit and twice a year for the conventional bulk sales and federal inspection every 18 months as well. The milk tests are done twice every time they pull milk from the tank – once for the private sales and once for the conventional sales. There will also be new types of inspections coming as well, farmers are told.

Yes, small on-farm processors do not need ‘one more thing.’

“The limit for the number of gallons sold privately off the farm needs to be set drastically higher for this (Milk Dealer license),” said Simpson. “We are not even a blip on the radar, so there needs to be very large exemptions if we are to keep small farms in Pennsylvania.”

-30-