By Sherry Bunting, Farmshine, July 31, 2020

CHICAGO, Ill. – A new face has “joined” Undeniably Dairy with direct ties to the effort to produce milk without cows.

Caleb Harper is the new hire for a new position via Dairy Checkoff. It was created within the DMI Innovation Center for U.S. Dairy’s Net-Zero project. His title as of May 1, 2020 is executive director of Dairy Scale for Good (DS4G).

On April 30, 2020, as reported last week in Farmshine, Harper left his position as the principle researcher at the M.I.T. Media Lab where he spearheaded the Open Agriculture Initiative, described as a “food computer” project. The lab came under scrutiny last fall for certain financial ties.

According to the May 13 New York Times, Harper’s OpenAg project “was quietly closed amid allegations that its results were exaggerated to sponsors and the public, the university confirmed. The Massachusetts Institute of Technology also announced that it would pay a $15,000 fine to the State Department of Environmental Protection because the project… improperly disposed chemicals into a well at a research center outside Boston where it conducted some experiments.”

For dairy farmers, that’s not even the worst of it. Harper has been a prolific writer and speaker touting cellular agriculture – milk, eggs and meat without animals.

According to the most recent IRS 990s (2017 and 2018) for New Harvest Inc., Harper was a New Harvest board member during those two years.

This new DMI executive will head the work of scaling up the ‘climate-friendly’ practices dairy farms will implement in the future, when his past is rooted in cell ag to replace them. His direct association with New Harvest as part of their 5-member board is troubling.

New Harvest describes its purpose as “support for education and scientific research that advance technologies that make animal products (meat, eggs, milk, etc.) without the animals in order to reduce animal suffering, improve human health, and protect the environment.”

We reached out to DMI through Scott Wallin, vice president of industry media relations and issues management. We also sent questions to the DMI chair.

— We asked whether this newly created position filled by Harper had been advertised and if other candidates had been interviewed.

— We asked what are the responsibilities and qualifications for this “executive director of Dairy Scale for Good (DS4G)”? (For his part, Mr. Harper has the following description listed on his resume at Linked-In, that he is “part of an initiative working to help U.S. Dairies pilot and integrate new technology and management practices to reach net zero emissions or better while increasing farmer livelihood.”)

— We asked whether Harper had prior connections to DMI or any member of staff or leadership before getting this position.

— We asked for confirmation of how Mr. Harper’s salary is paid, through what sub-agency of DMI or partnership?

— We asked to know his starting salary, given his listing with a speakers agency showing he charges between $30,000 to $50,000 as a speaker – a speaker who frequents events side-by-side with the executive director of New Harvest, such conferences sponsored by the United Nations, World Government Summit, EAT Forum and other entities on planetary diets, “future of food” and cellular agriculture – milk without cows, eggs without hens, beef without cows.

— We also messaged Mr. Harper to ask him how a board member of New Harvest that funds research and supports technology specifically for milk without cows gets a job paid by mandatory checkoff funds from American dairy farmers who feed, care for and milk cows?

— We asked him what are his interests and qualifications in dairy?

— We asked if he was tapped for this position by someone within the DMI organization or one of DMI’s “partners” or did he simply respond to a job posting and interview for the position?

— We asked DMI how it came to be that a person who is an obvious supporter of technology to create milk without cows became the person hired by dairy checkoff — with dairy farmer money — to help develop, scale and implement environmental practices for real dairy farmers?

So far, the only response we have received was a brief general email from DMI’s Wallin, as follows: “Caleb Harper joined on May 1 to support U.S. dairy’s growing commitment to environmental stewardship and the development of new, scalable technologies and practices to support U.S. farmers.”

Harper, who goes by the handle @CalebGrowsFood on Twitter, has deep connections to cellular agriculture, a new sector populated with Silicon Valley “tech food” startups that the largest global dairy and meat integrators and food giants are now investing in to ramp up to scale. They use false science on human health and environment, especially climate change, as the angle to push these new product investments so they take root in retail and foodservice sectors across the nation, the world.

In fact, the continuation of status-quo low-fat and fat-free diets via the Dietary Guidelines Advisory Committee’s unscientific “Scientific Report,” July 15 is a key in the cell ag arsenal. A primary vegan on the saturated fats subcommittee alluded to “making way for new foods coming” that will deliver the nutrients the government-sanctioned meal patterns leave lacking.

New Harvest has funded and supported research with donations to companies making bovine DNA-altered yeast that excrete “dairy replacement” proteins that companies claim are “interchangeable” with real dairy protein in any food processing application. Companies like Perfect Day tout their B2B model of working with large dairy companies to scale, to provide replacement dairy protein that reduce the need for real dairy protein and thus reduce the need for cows and the “pressure” on the environment.

These “cell ag” companies and non-profits work together to seek from FDA the ability to label their creations as the dairy and meat they replace because they declare them to be biological replicas — achieved through gene-editing and modifying.

They seek the new “healthy” icon FDA is creating with its ongoing development of a Nutrition Innovation Strategy to meet dietary goals, such as low-fat. They say their replacements are superior because they reduce the impact of livestock on the planet and can be genetically customized to meet goals for the low-fat DGA recommendations.

Even the USDA bio-engineered (BE) labeling implemented in January is all set and ready for this, and guess what? Dairy producers helped lobby for it, thinking it applied to the crops they grow. Our industry leaders used producer reactions to non-GMO labeling to get grassroots support for label language that now does not require bio-engineered replacements to be labeled as such unless the engineered DNA is detectable within the final edible food.

A visit to the New Harvest web page at new-harvest.org will make your hair stand on end. Seeing the motto so boldly proclaiming: “Milk without cows. Eggs without Hens. Beef without Cows,” offers the realization that their goal – in concert with World Wildlife Fund (WWF), DMI’s “sustainability partner” — is the end of animal agriculture through cell agriculture.

Don’t get angry and don’t be depressed. Have hope. Be bold.

If every Farmshine reader does some of the suggestions below, maybe the Titanic can be steered away from the iceberg:

1) Send this article to your Congressional representatives with a short note stating that this is just one example of how your rights as an American dairy farmer are being violated by the 15-cent mandatory dairy checkoff. Ask for his or her help in getting you an exemption from paying the checkoff, or in allowing you to assign your checkoff “tax” to another promotion, research and education entity.

2) Call, email, or write to the cooperative director who represents you and ask what your cooperative is doing to protect its members from even more FARM requirements, considering an obvious supporter of “milk without cows” will be implementing the “Undeniably Dairy” environmental piece as executive director of DS4G.

3) Call your state or regional dairy promotion representative or CEO and ask them to keep all of your dime in regional promotion instead of sending those 2.5 to 3 extra cents to DMI’s Unified Marketing Plan. They have the nickel. That’s enough.

4) Watch for opportunities to support a dairy checkoff referendum. The law states that when 10% or more of the dairy producers and importers subject to the checkoff request a referendum, the Secretary of Agriculture must oblige.

At best, DMI did not do its homework on this, and other decisions that have influence over the future of rank-and-file dairy producers footing the bill.

At worst, DMI’s “pre-competitive” alliances with global food giants and WWF are steering efforts toward dilution in order to meet some ethereal environmental goal.

Meanwhile hard working, conscientious dairy farmers have done and are already doing more good for health, climate, water and soil than the combined efforts of billionaire Silicon Valley ‘tech-food’ startup investors, multinational food corporations, gene-altering animal replacers, plant-based imitators, high-paid future food fast-talkers, sly and cunning dietary do-gooders, cows-and-climate catastrophe exaggerators, and so-called ‘sustainability’ WWFers.

In times like these, dairy checkoff unity could mean circling the wagons to protect dairy farmers with a locked-and-loaded promotion, education and research front that keeps the cunning wolves from getting in, but instead it gives them an opening and some leverage to devour.

Business is business. But dairy farmers should not be forced to fund their own dilution and demise.

-30-

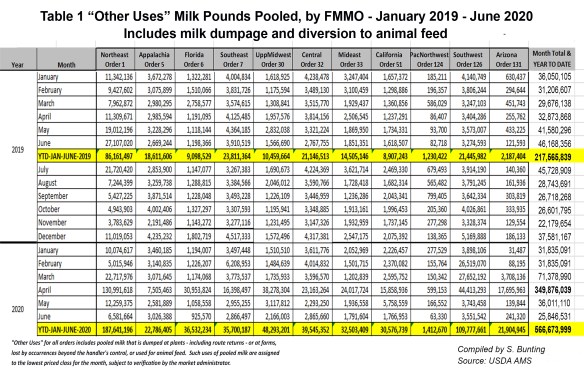

Table 1 (above) shows the “other use / milk dumpage” pooling data. What is mind-boggling is that year-to-date milk dumped totals at 566.7 million pounds for just the first 6 months of 2020, is 125 to 150 million pounds greater than the 12-month annual totals for each of the past five years.

Table 1 (above) shows the “other use / milk dumpage” pooling data. What is mind-boggling is that year-to-date milk dumped totals at 566.7 million pounds for just the first 6 months of 2020, is 125 to 150 million pounds greater than the 12-month annual totals for each of the past five years.

")

")

")

")

")

(1)")

")

")

")