By Sherry Bunting, Farmshine, December 17, 2021

WASHINGTON, D.C. — With the announcement of the Dairy Margin Coverage (DMC) signups starting December 13, 2021 through February 18, 2022, dairy farmers saw the first glimpse of the retroactive payments passed by Congress and signed by the prior administration in December 2020. This had been followed by announcements by the current administration via Ag Secretary Tom Vilsack in August 2021.

Since that time, dairy farmers have been patiently waiting for the feed cost adjustments that are retroactive all the way back to January 2020 and waiting to update their production history for the supplemental coverage promised in 2021.

Several industry sources estimate the new alfalfa-hay price adjustment to the DMC feed cost calculation netted an average 22 cents per cwt to each payment month in 2020 and 2021 for producers enrolled at the highest margin coverage levels. Future payments will also benefit during the life of the DMC program, which is authorized by the 2018 Farm Bill through 2023.

For example, the $8.77 margin for October 2021 was recently changed to $8.54 due to the feed cost calculation upgrade — adding 23 cents per cwt. to the October DMC payment triggered for farms enrolled at the $9 and $9.50 coverage levels.

According to USDA FSA sources, the funds were released in early December, and the automatic retroactive payments to DMC-enrolled producers for the alfalfa-hay adjustment to the feed cost side of the dairy margin calculation have been sent. Producers enrolled at the higher margin levels should have received these retroactive payments by the end of 2021, and even those enrolled at lower margin levels will receive a retroactive benefit, though smaller.

Industry sources estimate the total one-time retroactive adjustment for 2020 and the first 10 months of 2021 amounts to a one-time payment of almost $3 per cwt. at 95% of a dairy farm’s tier one production history (up to 5 mil. lbs) enrolled at the $9.50 margin coverage level.

This feed cost change, alone, yields a margin benefit that exceeds the cost of the tier one premium for DMC coverage at the highest margin level of $9.50. That level of DMC coverage costs 15 cents per cwt – up to 5 million pounds of annual production history, and farms can cover up to 95% of that. To cover pounds beyond the 5-million-pound tier-one cap, the DMC premiums are more expensive and the $8 margin is the highest margin one can cover beyond the tier one, 5 million pound production history base.

In addition to the feed cost change, the Dec. 8 USDA announcement designated Dec. 13, 2021 through Feb. 18, 2022 as the signup period for both the 2021 Supplemental DMC payments on expanded production as well as the coverage level selections for 2022. The Supplemental DMC was passed by Congress in 2020 and was supposed to go into effect for 2021 forward.

Farms that have expanded production since their 2011-13 production history average was calculated will want to verify this with their USDA FSA office using a 2019 milk statement. The application for the 2021 Supplemental DMC must be submitted before doing the 2022 DMC enrollment and coverage level selections. Any farm that has a production history on record with USDA FSA under the previous MPP program — but never enrolled in DMC — will also want to go back and update their production history before enrolling in DMC for 2022.

According to the Federal Register rule, there is a formula applied to the expanded production so it’s not a pound-for-pound update.

Once the farm’s application for the new production history is approved by USDA FSA, the producer will receive the retroactive DMC payments on a percentage of that supplemental production back to January 2021.

Because of the tier-one cap, the Supplemental DMC pertains to herds around 300 cows or less with updated total production history of 5 million pounds or less annually. This cap has not been expanded.

Also, dairy farms that went through a transfer of ownership interest after Jan. 2, 2021 must have the predecessor file and verify the supplemental production history – even if the successor is the one now enrolling in the DMC program.

The DMC program has triggered payments in every month, so far, of 2021 for producers enrolled at the highest coverage level ($9.50), and there were several months of payments for producers enrolled at the $6 level. Tier one coverage at the highest margin level ($9.50) on the first 5 million pounds of annual production costs 15 cents per cwt., and the average payout so far for 2021 at that level has ranged from 96 cents in October to over $4 per cwt in July. The November and December 2021 DMC margins have not yet been announced. In addition, during 2020, payments triggered in five months and in 2019, seven months.

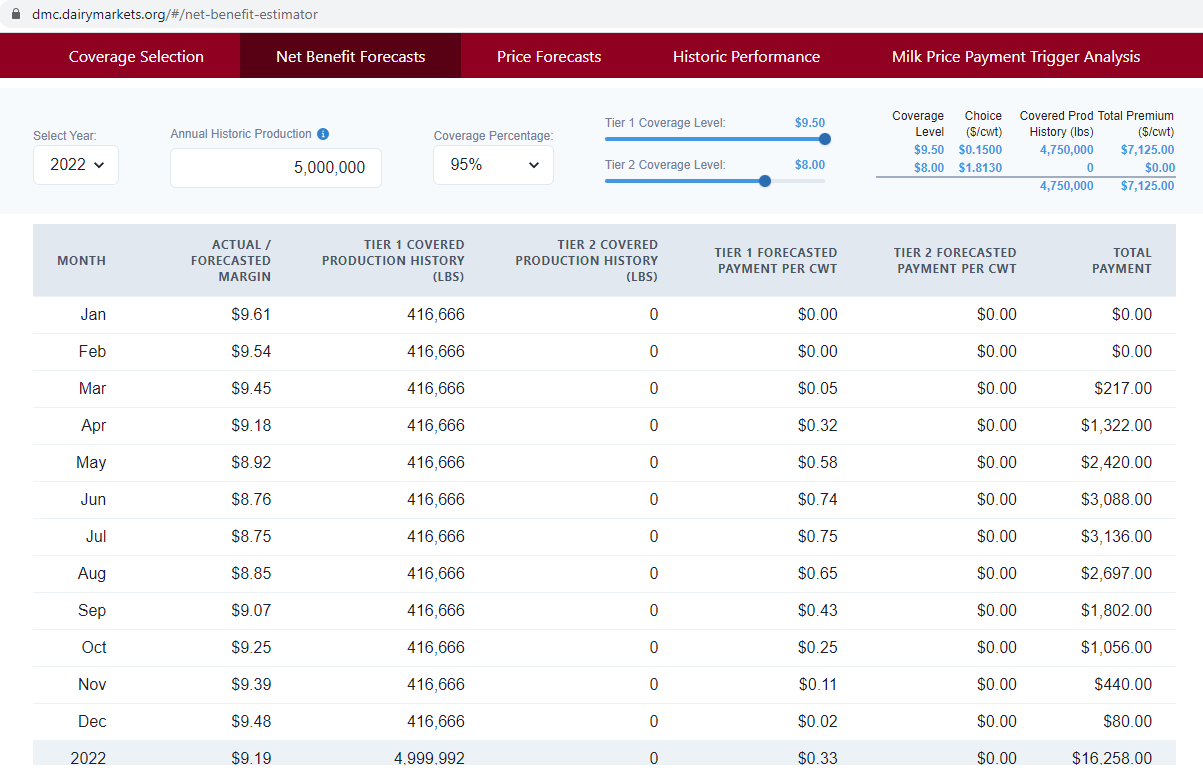

Herds of all sizes can cover their first 5 million pounds at the tier-one rate of 15 cents per cwt., which comes out to $7,125 premium cost for the year. As of December 30, 2021, with both milk prices and feed costs trending higher, the net benefit is forecast at over $16,000 on the first 5 million pounds of production history. In 2021, the 10-month average payout, so far, across herd sizes is almost $60,000. Find the net benefit forecaster in the online DMC decision tool here and be sure to select the year you are looking at in the upper left hand corner.

https://dmc.dairymarkets.org/#/

Other information about DMC can be found at

https://www.fsa.usda.gov/programs-and-services/dairy-margin-coverage-program/index

Feb. 18, 2022 is the deadline to update retroactive production history and to enroll coverages for 2022. Be sure to update production history with FSA using your 2019 final milk check statement before enrolling for 2022 DMC coverage

-30-