Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

CHICAGO, Ill. – On October 9, Dairy Management Inc (DMI) and Nestlé made big announcements. DMI’s Innovation Center for U.S. Dairy officially unveiled the Net Zero Initiative it calls “an industry-wide effort” to meet 2050 goals for carbon neutrality, optimized water usage and improved water quality.

On a DMI media call last week, Innovation Center chairman Mike Haddad and others discussed the Net Zero Initiative and the simultaneous announcement of a $10 million commitment and multi-year partnership by Nestlé to support the “scaling” of “access” to environmental practices and resources on farms across the country.

As clarified by Karen Scanlon, senior vice president of sustainability initiatives for DMI, this investment by Nestlé will have a “farm and field focus” and represents a five-year partnership.

Haddad suggested that other companies are looking to invest, including companies from the financial and technology sectors.

Although the press statements talk about the Net Zero Initiative (NZI) as supporting “access” for all farms of all sizes and geographies to meet the industry’s 2050 climate and environmental goals, the details are still sketchy in how this all will translate at diverse farm and industry sector levels.

California dairy producer and DMI vice president Steve Maddox noted that when times are good and producers have a good margin, they like to experiment and invest and test new ideas. He acknowledged that it’s “hard to go green when you’re in the red.”

Maddox said for 2050 goals to be met, technologies and practices have to positively impact the dairy’s bottom-line.

Krysta Harden, executive vice president of global environmental strategies for DMI and former undersecretary of agriculture under Tom Vilsack, noted that the Net Zero Initiative helps with this “affordability.” NZI will identify the pilot farms and test the ideas, the technologies and practices on those farms to show what pays.

She said Nestlé’s $10 million investment make “Nestlé our first legacy partner to come on board to really transform dairy.”

Harden explained that the funds will be used in three key areas: Foundational resources, new products (clarified as manure products), and on-farm practices.

Haddad noted that the financial and tech sectors are reaching out also, and Nestlé has pledged its expertise as well as the financial investment.

“We need capital and technology to do this,” he said. “We also need the experience and expertise of others. We believe Nestlé’s commitment is huge and hope it is the first of several.”

While the nuts and bolts are not clear, it does appear that investments, such as the $10 million from Nestlé, will help pay for the testing and development of technologies and practices on pilot farms.

What happens around that piece is called “scaling up” and “providing access” and “improving profitability,” but without a disclosed road map of how that ‘scaling’ will look to the rest of the non-pilot farms in the U.S.

“We are already talking to pilot farms,” Harden acknowledged. “We like to say that every farmer can do something, and they are already doing a lot. We talk about this at DMI board meetings to see where we are at, and the hands go up, we see that our farmers are already working on the list of things. They are already committed.”

Scanlon gave a little bit of a road map when she noted that there are three “buckets” that the Net Zero Initiative will need investment in order to address the barriers to meeting the 2050 goals:

1) Data and research gaps, the need for more dairy research with quantifiable outcomes,

2) Affordability, the need for economically viable technology and practice solutions so that farmers can make the choices that drive industry success, and

3) Accessibility, to reach scale across the diverse industry in terms of dairy size and geography, to enable farms of all sizes to access the technology and have the support to implement it successfully.

Harden explained there is “no one solution,” that technologies and practices will have to be “adapted” and “make sense.”

She listed the four areas Net Zero practices and technologies are divided into: 1) Feed production, 2) Manure handling and nutrient management, 3) Cow care and production efficiency, and 4) On-farm energy efficiency and renewable energy

According to Harden, “Net Zero is already possible on certain farms. The purpose of NZI is to expand our knowledge and adoption of policies to reduce GHG and water use.”

A bit of history

Haddad, chairman of Schreiber Foods, has been chairman of the Innovation Center for U.S. Dairy for two years and a member for 10.

He explained how the Innovation Center got started first as a “globalization initiative” followed by safety and social responsibility initiatives, but that “sustainability” was one of its main active committees from the start in 2008. Haddad said that the Sustainability Committee has operated 12 years under the continuing leadership of its chairman Dr. Mike McCloskey of Select, Fair Oaks and Fairlife.

“The Innovation Center for U.S. Dairy was created by DMI (in 2008-09) at the urging of farmers,” said Haddad.

“DMI wanted to bring together a forum of many stakeholders — dairy farmers, processors, NGOs (like WWF), retailers and foodservice — to function as a voluntary board. Farmers wanted to be connected at the middle level to collaborate with those that sell milk and milk products,” Haddad related.

Today, 27 companies have representation on this board, and over 300 companies are “engaged in the journey, along with our shoppers, citizens and neighbors around the world,” he said.

Globalization first initiative

“It started initially with a globalization initiative,” Haddad explained, adding that even though the current talk in the industry since Covid is about “re-shoring” and local, “we do not exist in an island,” he said.

According to Haddad, the original globalization initiative of the Innovation Center for U.S. Dairy back in 2008-09 started with the Bain Study. Back then, the Bain Study was touted as showing opportunities for trade.

However, Haddad said Wednesday that the Bain Study — as part of the original Innovation Center globalization initiative — “showed us that we could be informed and enlightened together and raise all boats together pre-competitively.

“The globalization study showed we need to go together. This got into our blood that we can work together on certain platforms and go farther, together than we can go alone,” he said.

By 2015-16, the Innovation Center for U.S. Dairy had evolved into a “social responsibility platform,” and Haddad said food safety was among the next pieces. Once the industry could see how to collaborate on food safety, the “pre-competitive” techniques were applied to animal care and sustainability.

In other words, the members of the Innovation Center for U.S. Dairy wanted the industry to first “go together” toward globalization, then food safety, now animal care, for which FARM is the driver, and sustainability, for which Net Zero Initiative is the driver.

“We don’t want to compete with each other in these areas,” said Haddad. “We should only compete on the attributes of our products. We should not be saying ‘mine is safer than yours’ (or more sustainable than yours), because that undermines confidence and trust in dairy.”

Haddad explained that the Innovation Center works closely with National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA).

Part two continues next week in Farmshine.

DMI integrates the dairy industry through its unified marketing plan and the various nonprofit organizations, alliances, committees and initiatives — beginning with the Innovation Center for U.S. Dairy. The IC was formed in 2008-09, launching the industry’s structural drivers beginning with the globalization initiative (Bain Study 2008), then social responsibility (FARM program 2015) and now ‘sustainability’ (Net Zero Initiative 2020). Graphic by Sherry Bunting, source USdairy.com

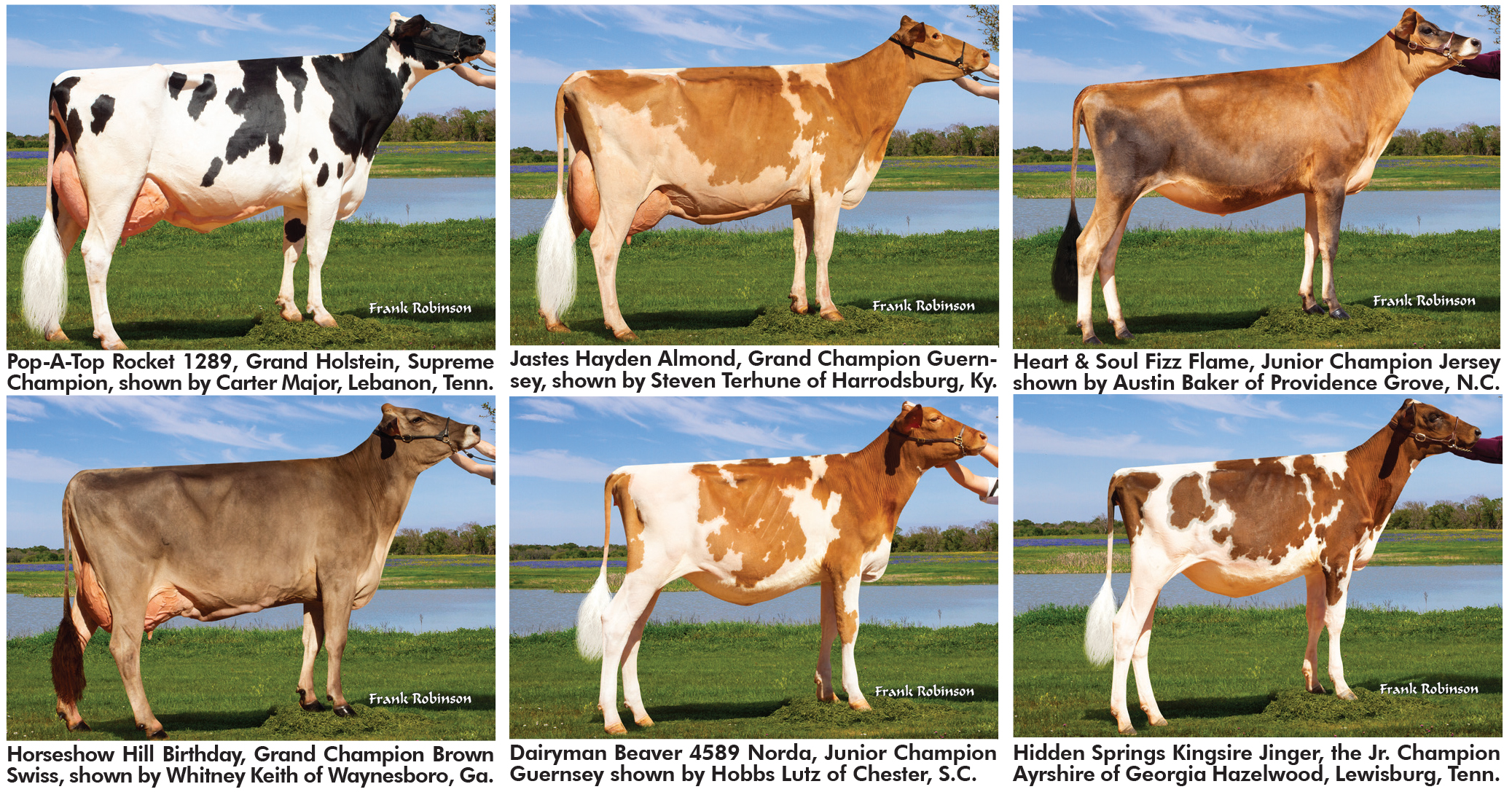

Dairyland Classic co-superintendent Jay Moon of Moon Farms (left) displays the commemorative milk can painted by Debbie Cornman, Boiling Springs, Pa. Show superintendent Carol Williams of WDairy is pictured congratulating Jacob Johns of Chapel Hill, Tenn., winner of the jackpot showmanship contest with 39 entries judged by the supreme showmanship winners. Photo by Katie Williams

By Sherry Bunting, Farmshine, October 16 and 23, 2020

MADISON, Ga. — Georgia dairy producers Carol Williams of WDairy, and Jay Moon of Moon Dairy, heard in mid-June of fall show cancellations after already losing the spring shows to Covid, they knew they had to do something. They put together a small committee with Carol serving as show superintendent and Jay as co-superintendent and started raising funds.

“The response from companies was overwhelming,” says Carol. “Once we had the funding coming in, we knew we would have the draw in premiums. The generous sponsorships included some very good premiums and prizes.”

The first annual Dairyland Classic was born in Madison, Georgia — held Sept. 30 to Oct. 3 at the Morgan County Ag Center – and dubbed by exhibitors as ‘Little Madison.’

In addition to cash awards, companies gave semen certificates, services, halters, products… “We got money and goodies for the exhibitors,” Carol explains.

The three-months of planning turned into a big event attracting 80 exhibitors, 222 entries from 8 southeastern states clear up to Pennsylvania — many making it double as a vacation, enjoying the southern charm and historic district of Madison, Georgia with its rich agricultural history.

Carol and Jay say their committee was fortunate to bring in Kevin Lutz of Treasure Chest Jerseys, Lincolntown, North Carolina to judge five breeds — Ayrshire, Brown Swiss, Guernsey, Holstein (Black and Red combined), and Jersey.

Photo by Katie Williams

They decorated for the feel of a party, setting up tables and chairs for people to visit. They had a macaroni and cheese supper followed by an ice cream social on opening night.

“We easily fed over 150 people,” Carol relates. “The milk, cheese and ice cream were all donated by local creameries.”

Facebook comments were glowing. Participants commented that it felt like they stepped out of the truck after a long drive hauling their animals to find southern hospitality to the max.

“That’s what we wanted,” says Carol. “With the tents and the lights and the atmosphere, we had fun.”

‘Friday night lights’ under the tents at the Ag Center in Madison, Georgia. A committee of five, headed by Carol Williams and Jay Moon spent three months planning and pulling off the first annual Dairyland Classic Sept. 30-Oct. 3, attracting roughly 80 exhibitors from 8 states, 222 entries and 176 show animals arriving at the barn in five breeds for the opportunity to show and enjoy plenty of ‘southern hospitality.’ Photo by Katie Williams

The work paid off. For many of the breeders and exhibitors traveling up to 12 hours to get there, this was their first show of the year. In a normal year, they would have been to five or six shows by October. And this one was memorable.

In addition to type classes for juniors and open combined, as well as showmanship, the Dairyland Classic featured a jackpot showmanship class for youth 16 and up. They could show with their own animal or borrow one. The entry fee was $25 — winner-take-all.

“We had 39 people in the jackpot,” Jay relates. “The youth who won supreme showmanship were the jackpot judges. It was a fun event. The jackpot turned out to be $860. We turned over the whole amount, put it in a milk bottle engraved with our Dairyland Classic logo,” and it all went to the winner – Jacob Johns, a college student from Chapel Hill, Tennessee.

This first annual Dairyland Classic was held during the week that would have been World Dairy Expo in the other Madison — Wisconsin — earning it the nickname ‘Little Madison.’

“We know we’ll pick a different week for next year, but this show will go on. People enjoyed it,” Jay says. “From the planning to the actual event, it felt good to bring the dairy industry together, and know for some it might be the only show they get this year, that makes it all worthwhile.”

“Seeing the happiness on the faces of participants, the joy of getting into the show ring from little bitty kids to senior citizen showmen, some saying ‘we still got to go to Madison this year,’ that was satisfying,” Carol relates.

The Dairyland Classic was open to anyone, and early on they had entries and interest from the Midwest, but then the North American Open was moved from mid-October in western New York to Circleville, Ohio and falling then on the same week as the Classic in Georgia.

As superintendent, Carol throws her passion for youth and agriculture into everything she does. She and her husband Everett have long been involved with children and now grandchildren in 4-H, and Carol is instrumental in the family’s 1700-cow dairy farm and its growth over the years.

She serves as president of the Georgia Dairy Youth Foundation and chairman of the the Morgan County Agriculture Center Authority, to keep the dairy programs going. Serving on the board of directors for the Georgia Junior Livestock Foundation and the Georgia Cattlewomen Association, she gives the dairy industry a face and voice.

As co-superintendent of the show, Jay is instrumental on his family’s Moon Dairy, milking 120 Holsteins in a grazing operation. His youth experiences led him to University of Georgia earning a degree in Agriculture Education, and he splits his time between the home farm, managing the county agricultural center, and working in extension as 4-H AmeriCorps Service Member.

Also serving on the show committee were Kimberly Bragg, a Jersey breeder from Millen, Katelin Benkoski of Madison, and Katie Williams, Madison. Katie and Katelin did some of the show photography, and the show committee had cow photographer Frank Robinson on site to do cow portraits.

Photos by Frank Robinson

After placing all five breed shows, Judge Kevin Lutz named the Holstein grand champion, Pop-A-Top Rocket 1289, as supreme champion. The aged cow exhibited by Carter Major of Lebanon, Tenn. was also supreme bred and owned.

Carter Major of Lebanon, Tenn. with his grand champion Holstein. The aged cow was supreme champion and supreme bred and owned of the show.

Reserve grand champion Holstein was the four-year-old Archival Rae 2-ET shown by Conrad Horst, Millen, Ga. From South Carolina, Elisabeth Lark’s spring yearling Car-J Diamondback Barbie was junior champion.

Breed grand champions from left, Carter Major with his Holstein Pop-A-Top Rocket 1289, Jayme Ozburn at the halter of his brother Forest’s Jersey OBJ Applejack Julep, Stephen Terhune with his Guernsey Jastes Hayden Almond, Whitney Keith with her Brown Swiss Horseshow Hill Birthday ET and Jennifer Blankenship at the halter of Neal Smith’s Ayrshire Lazy M Gentle Lady GaGa-ET.

Showing the reserve junior champions in both Holstein and Brown Swiss competition was Caitie Collier, Harrodsburg, Ky. with her Holstein winter calf KA-Buck Bemer Crizal and Brown Swiss winter yearling Triple C Bodacious Bree.

Whitney Keith of Franks Farm, Lenox, Ga. exhibited Horseshow Hill Birthday ET, the Brown Swiss grand champion. Her winter calf, Crows Nest Posse Persnicka was junior champion. Reserve grand honors and best bred and owned went to Jacob Johns, LazyJ Farms, Chapel Hill, Tenn. for his four-year-old LIF Seamans Coll Party.

Jersey classes were the largest. Forest Ozburn, Lewisburg, Tenn. had grand champion and best bred and owned with three-year-old OBJ Applejack Julep. He also had reserve junior champion with his fall calf OBJ Mr. Swagger Pandora.

Reserve grand in the Jersey show was a fall milking yearling, South Mountain Chrome Renegade ET, shown by Hobbs Lutz of Her-Man Jerseys, Chester, S.C. The top Jersey heifer was Heart & Soul Fizz Flame, a spring yearling shown by Austin Baker, Pride Rock Farms, Staley, N.C.

A pair of four-year-olds topped the Ayrshire show. Neal Smith of Smyrna, Tenn. had the grand champion Lazy M Gentle Lady GaGa-ET, while Auburn Strange of Stell’R Genetics, Ky. showed the reserve grand JCC Dreamer Hilary.

The top two Ayrshire heifers were both bred and owned by Georgia Hazelwood, LaFollette, Tenn. The junior champion was her spring calf Hidden-Springs Kingsire Jinger also earning best bred-and-owned of the Ayrshire show. Her winter calf Hidden-Springs Kingsire Jewell was reserve heifer.

In the Guernsey show, Stephen Terhune, Locust Hill Farm, Winchester, Ky. had grand champion with his aged cow Jastes Hayden Almond. Hobbs Lutz, Chester, S.C. garnered reserve grand and best bred-and-owned with two-year-old Walnut Ridge Jackpot Stan ET. His winter calf Dairyman Beaver 4589 Norda ET was junior champion. Hickman Valleys Light Garfield, the homebred fall calf of Mike Hickman of Shelbyville, Tenn. was reserve junior champion.

Supreme showmanship honors went to Tennesseans Forest Ozburn and Carter Major, as champion and reserve, respectively. Ruth Adkins, York, S.C. placed third, Caeden and Colton Swartz, Senoia, Ga. fourth and fifth, respectively, and Jaylee Bennett, Millen, Ga. placed sixth.

Kevin Lutz of Treasure Chest Jerseys, Lincontown, North Carolina judged all five breeds at the Dairyland Classic. Photo by Katelin Benkoski

Carol and Jay say having Judge Lutz was a key to the event’s success. Lutz and his family milk 150 registered Jerseys at Treasure Chest Jersey Farms. Dairy farming and Jersey cows have been part of the Lutz family since the 1890’s, and in recent years they have exported genetics to many countries. Lutz has judged prestigious shows around the world.

Lutz twice judged The All-American, The Jersey Jug and Western National as well as over 18 state fairs and internationally in Australia, Italy, and Argentina.

Carol and Jay are also grateful to the many companies and individuals in the southeast dairy farming community for generous contributions making the Classic a successful event for cattle breeders and exhibitors from Georgia, North and South Carolina, Kentucky, Tennessee, Florida, Alabama and Pennsylvania.

Sponsors are highlighted in the show book and on the Dairyland Classic Facebook page (@GeorgiaDairylandClassic) where more photos and information can be found.

Juniors and adults competed together in one open show with Lutz placing all classes. The top three in each class by breed, follow.

AYRSHIRES:

Spring Calves: 1. Hidden Springs Kingsire Jinger (jr. champion, best bred-owned), Georgia Hazelwood, TN.

Winter Calves: 1. Hidden-Springs Kingsire Jewell (res. jr. champion), G. Hazelwood, 2. Lazy M Kingsire Tiffany, Neal Smith, TN, 3. Stell’R Hilary’s HellYeah, Auburn Strange, KY.

Fall Calves: 1. Stell’R Berkely Ziggy, A. Strange, 2. Destiny Pred Bella Sera-ET, Russell Isley, SC.

Spring Yearlings: 1. Stell’R B Zinnia, A. Strange, 2. Blue-Spruce B-King Bonnie-ET, Russell Isley, 3. Hickman Valley Raney Daisey, N. Smith.

Winter Yearlings: 1. JCC Reagan Mabel, Strange, 2. Lazy M Gentle Shantel, G. Hazelwood, 3. Hickman Valleys Raney Daffodil, N. Smith.

Two-year-olds: 1. Ollie Hilary’s Hellcat, A. Strange.

Four-year-olds: Lazy M Gentle Lady GaGa-ET (grand champion), N. Smith.

Aged Cow: 1. JCC Dreamer Hilary (res. champion), A. Strange.

Breeders Group: Auburn Strange.

BROWN SWISS:

Spring Calves: 1. Hidden Springs Victoria, G. Hazelwood, 2. Crows Nest Candie Onyx, Whitney Keith, GA.

Winter Calves: 1. Crows Nest Posse Persnicka (jr. champion), W. Keith, 2. Triple C Moonlight Dixie, Caitie Collier, KY, 3. T&T FMS Sterling Reilly, Heath McGaha, NC.

Fall Calves: 1. Crows Nest W Birthday Party, W. Keith, 2. T&T FMS Eason Saylor OCS, H. McGaha, 3. Fairdale Easton Wilma, Attie Taylor, KY.

Three-year-olds: 1. Siegerts Braiden Porsha, Carter Major, TN, 2. T&T FMS Pegasus Raelee, H. McGaha, 3. Crowsnest WF Birthdaygirl, W. Keith.

Four-year-olds: 1. LIF Seamans Coll Party (res. champion, best bred-owned), J. Johns, 2. T&T FMS Bosephus Skye, H. McGaha.

Aged Cows: Horseshow Hill Birthday ET (grand champion), W. Keith.

Breeders Group of 5: 1. Whitney Keith, 2. Heath McGaha.

GUERNSEYS:

Spring Calves: 1. SC Sunny Day Beau Star, Hobbs Lutz, SC, 2. Hickman Valleys Legend Truth, Mike Hickman, TN.

Winter Calves: 1. Dairyman Beaver 4589 Norda ET (jr. champion), H. Lutz, 2. Hickman Valleys Luxury Jaycie, M. Hickman, 3. Hickman Valleys Luxury Tori, N. Smith.

Fall Calves: 1. Hickman Valleys Light Garfield (res. jr. champion), M. Hickman, 2. Kelly’s Reno Layla, Charlie Kelly, SC.

Summer Yearling: 1. Kelly’s Reno Lula, C. Kelly.

Spring Yearlings: 1. Kelly’s Ladysman Trinity, Ruthie Adkins, SC.

Winter Yearlings: 1. Jastes Randa Boo, Stephen Terhune, KY, 2. Springhill Mentor January, H. Lutz.

Fall Yearlings: 1. Kelly’s Legend Lyla, C. Kelly, 2. Twins Ridge Ladysman Maple, H. Henson.

Two-year-olds: 1.Walnut Ridge Jackpot Stan ET (res. champion and best bred-owned), H. Lutz, 2. Green Slopes A1 Brooklyn, Macy McDonald Walason, PA.

Three-year-olds: 1. Springhill GG Priceline, M. Walason, 2. Green Slopes A1 Noelle, M. Walason.

Aged Cows: 1. Jastes Hayden Almond (grand champion), S. Terhune, 2. Green Slopes Aristocrat Maybelle and 3. HI Field Big Ben Blossom, both exhibited by M. Walason

HOLSTEINS:

Spring Calves: 1. Mats Uno Beemer Vivian, Ella Gilmore, TN, 2. Hobbs Deceiver Cookie, H. Lutz, 3. Miss Liz Atwood Annie, Elisabeth Lark, SC.

Winter Calves: 1. KA-Buck Bemer Crizal (res. jr. champion), C. Collier, 2. T&T FMS Defiant Bristol-Red, H. McGaha, 3. Pop-A-Top Tattoo Tonya-ET, Carter Major.

Fall Calves: Ms-Aol Jordy Revamp-Red, by C. Collier, 2. MS Doorman Viola, E. Gilmore, 3. Crowsnest DB Rosa, W. Keith.

Summer Yearlings: 1. Pop-A-Top Jizz Sister, C. Major, 2. Ash-Go Delight Moonpie, Ashlee Godbee, GA, 3. Rocky-Tp Solomon Axle-ET, Mary Helen Coble, GA.

Spring Yearlings: 1. Car-J Diamondback Barbie (jr. champion), E. Lark, 2. Canary Crush Aplen, Charlotte Canary, NC, 3. Crows Nest A Sunny-Red ET, W. Keith.

Winter Yearlings: 1. Mats-Uno Apple Crisp Ruth-Red, E. Gilmore, 2. Pop-A-Top Diamondback Ace, C. Major, 3. Miss Liz Beemer Callie, E. Lark.

Two-year-olds: 1. Pop-A-Top Kingboy Trina, Addison Major, TN, 2. Stunning J Sundrop-Red, W. Keith, 3. Ja Bob Cuda Harmony, Reagan Britt, GA.

Fall Calves: OBJ Mr. Swagger Pandora (res. jr. champion), F. Ozburn, 2. Tierneys Victorious Lively, Jaylee Bennett, GA, 3. Her-Man Victorious Davina, Caroline Wilks, SC.

Summer Yearlings: 1. Steel-Lane Andreas Berry, Wayne Lutz, SC, 2. OmaBraggin Victorious Finish, J. Bennett, 3. Avon Road VIP Venture, M. Bond.

Spring Yearlings: 1. Heart & Soul Fizz Flame-ET (jr. champion), A. Baker, 2. Deerview Chrome Cod, W. Lutz, 3. OBJ Gentry Ava, F. Ozburn.

Winter Yearlings: 1. Her-Man Swagger Dreamy, H. Lutz, 2. OmaBraggin Showdown So Fearless, J. Bennett, 3. Heart & Soul Fizz Felicity-ET, A. Baker.

Fall Yearlings: 1. Rokey Benfer Casino Adrina-ET, C. Evans, 2. Suess Craze Reva, Noel Pickel, GA.

Fall Yearlings in Milk: 1. South Mountain Chrome Renegade ET (res. champion), H. Lutz, 2. Cherub Rockstar Plymoth, M. Bond, 3. River Valley 1801, Mackenzie Jones, GA.

Two-year-olds: 1. Her-Man Colton Fobia, H. Lutz, 2. OBJ Tequila Jacklyn, F. Ozburn, 3. Cherup Colton Naomi, M. Bond.

Three-year-olds: 1. OBJ Applejack Julep (grand champion, best bred-owned), F. Ozburn, 2. BRJ Dazzler Mint, H. Lutz, 3. Avon Road Scout Vivian-ET, M. Bond.

Four-year-olds: 1. OmaBraggin Windstar Funny, Obrien Bragg, GA, 2. TK-ENT-In Vancouver, M. Bond, 3. Peelers Megtron Trouble 1519, H. Swartz.

Does milk need reinventing for kids? USDA and dairy checkoff say yes. Meanwhile kids, parents and experts who’ve studied the issue say… not so fast… just allow the schools to provide whole milk as a choice. Istock photo by Aaron Amat

ALBANY, N.Y. – As part of the 2021 checkoff funds for Cornell dairy research approved recently by the New York State Dairy Promotion Advisory Board is the first phase (2021-22) of a two-year project to develop and build a “Kids Milk” for schools, foodservice and retail. The first phase is to complete the successful multi-step innovation process (remove lactose and add sugar), and the second phase will be to implement the “future view” (remove whey to improve shelf-stable flavor and reduce transportation cost and refrigeration).

The project was one of 12 presented by Cornell, which is one of five universities that are part of DMI’s Dairy Research Institute (DRI). The DRI was formed as a 501 c 3 non-profit by DMI’s Innovation Center for U.S. Dairy a decade ago in August of 2010.

Reading through this project’s innovation process and vision, in essence, by year two, ‘Kids Milk’ (aka ‘school milk’) could be compositionally the same as the ultrafiltered / microfiltered cheese starter milk that has the lactose and whey removed. In essence large-scale-cheese-vat-ready-milk would be positioned as ‘Kids Milk’ tested and touted as beneficial for children’s taste, tolerance and nutritional reasons, of course. (Think about this within the context of the large-scale cheese processing shifts now occurring in the dairy industry.)

According to the researchers’ slides presented to the NY Board in September, the ‘Kids Milk’ will be stripped of lactose, but then have sucrose (sugar) added in order to “achieve a higher sweetness intensity and achieve higher liking scores without increasing calories from carbohydrates in 1% fat chocolate milk,” for example. A copy of the Cornell researchers’ presentation is available online with the NY Board’s minutes at https://agriculture.ny.gov/dairy/dairy-promotion-order

The ‘Kids Milk’ would also be a high-heat pasteurized, extended shelf-life product, and the second phase talks about making it shelf-stable. In concert with this, another NY checkoff-funded Cornell project, in its second year of research, is determining how to solve off-flavors in extended shelf-life and aseptically-packaged shelf-stable milk products by removing the ‘offending’ whey — with an eye to the school foodservice applications in terms of transport and refrigeration.

The ‘Kids Milk’ research project is jointly sponsored by the NY State Dairy Promotion Advisory Board (checkoff) approving $76,269 per year for the portion conducted at Cornell, along with H.P. Hood and Dairy Management Inc. (DMI) funding the portion being conducted at North Carolina State University’s dairy research center. Hood’s contribution is $50,000 per year and DMI’s checkoff contribution is $20,000 to $30,000 per year.

In their presentation of the two-year research and innovation phase (2021-22), the Cornell researchers explained that they have proof of concept as of August 2020 for the first step in the two-step process of removing lactose and adding sugar to replace it. They explain in a power point slide that once they achieve success in the innovation research, they will move to the “view into the future” for ‘Kids Milk,’ using the microfiltration whey-removal research being done simultaneously at North Carolina State.

The “view of the future” for ‘Kids Milk’ is revealing and was described by researchers as follows:

Step 3 – “Increase the protein content by ultrafiltration to have 1% fat and 6 to 7% protein to build mouthfeel, achieve a calcium and protein per serving higher than regular milk, and bring the product to a milk solids-not-fat that would allow it to comply with standard of identity for milk and to be labeled lactose-free ultrafiltered milk.”

Step 4 – “Increase the protein content by ultrafiltration by a combination of ultrafiltration and microfiltration. Microfiltration removes milk derived whey proteins from milk. The milk derived whey proteins have been identified in our research as the ones that cause the objectionable cooked sulfur flavors in the UHT (extended shelf-life) milks. Our goal is to remove these proteins to build a milk that will taste good to children and meet nutrition guidelines while being shelf-stable. This will reduce shipping and distribution costs for milk by reducing the number of deliveries and the need to separate refrigerated delivery to schools.”

Back on August 5, 2020, DMI CEO Tom Gallagher in an ‘open mic’ call addressed the grassroots push to get whole milk back as a choice in U.S. schools. He stated to the farmers, board members and media on that Aug. 5 call that, “Farmers are great, and our product is great… but even if whole milk is eventually recommended for kids, we still need innovation to get it to the kids in a style that they like.”

Voila: ‘Kids Milk.’

Meanwhile, as reported in the August 7, 2020 edition of Farmshine, a simple trial at a middle and high school in Pennsylvania was conducted without fanfare — and anonymously due to USDA ‘milk rules’. It found that teenagers like milk the way it is, without the reinvention.

In fact, this anonymous 2019-20 trial simply offered all fat percentages of milk, and within the first month, found students choosing whole milk 3 to 1 over the lower fat options. Five months later, students responded favorably to the surveys.

But what was really significant was this: the trial resulted in middle and high school aged students – teenagers! – choosing milk over less healthful competing beverages as revealed by a 65% increase in milk consumption and a 95% decrease in the amount of milk being discarded. Instead of taking the ‘served’ low-fat and fat-free milk (per USDA), throwing it away and buying something else, the students were choosing milk and drinking it!

Whole milk is also shown to be tolerated by many who claim to be lactose-intolerant as the amount of lactose is slightly less when more of the fat is retained, and the fat slows the rate of absorption of the lactose carbohydrate. This finding is both anecdotal and referenced in an official USDA Dietary Guidelines comment by Dr. Richard Theurer, adjunct professor in the Dept. of Nutrition Sciences at North Carolina State University. In his comment (2018 and 2020-25) to the Dietary Guidelines Advisory Committee, he supports a reversal of the DGA’s misguided recommendation that children over age 2 be offered only fat-free and low-fat milk (now required at schools and daycares) instead of the healthy choice of whole milk.

Does milk need to be reinvented with farmer checkoff funds in order to “get it to the kids in a style that they like” as DMI CEO Gallagher suggested during the Aug. 5 open mic call?

Looking at year two of the checkoff-funded Cornell ‘Kids Milk’ project, the presenters own words offer a clue. They described a successful outcome “will reduce shipping and distribution costs for milk by reducing the number of deliveries and the need to separate refrigerated delivery to schools.”

This look into the ‘Kids Milk’ future reveals the bottom line is the disassembly and extrusion of milk at finer and finer molecular levels to reinvent and build a beverage that fits the increasingly concentrated globalized supply chain of food transformation.

It’s really not about the kids, at all.

Author’s postscript: Think about this in the context of Coca Cola now owning 100% of the fairlife ultrafiltered milk brand and the potential for reducing school milk (‘kids milk’) to the equivalent of milk protein concentrate (MPC) added to sucrose or high fructose corn syrup (HFCS) for shelf-stable concentrate reconstituted in soda-style — ‘just add water’ — beverage dispensers. Get the picture?

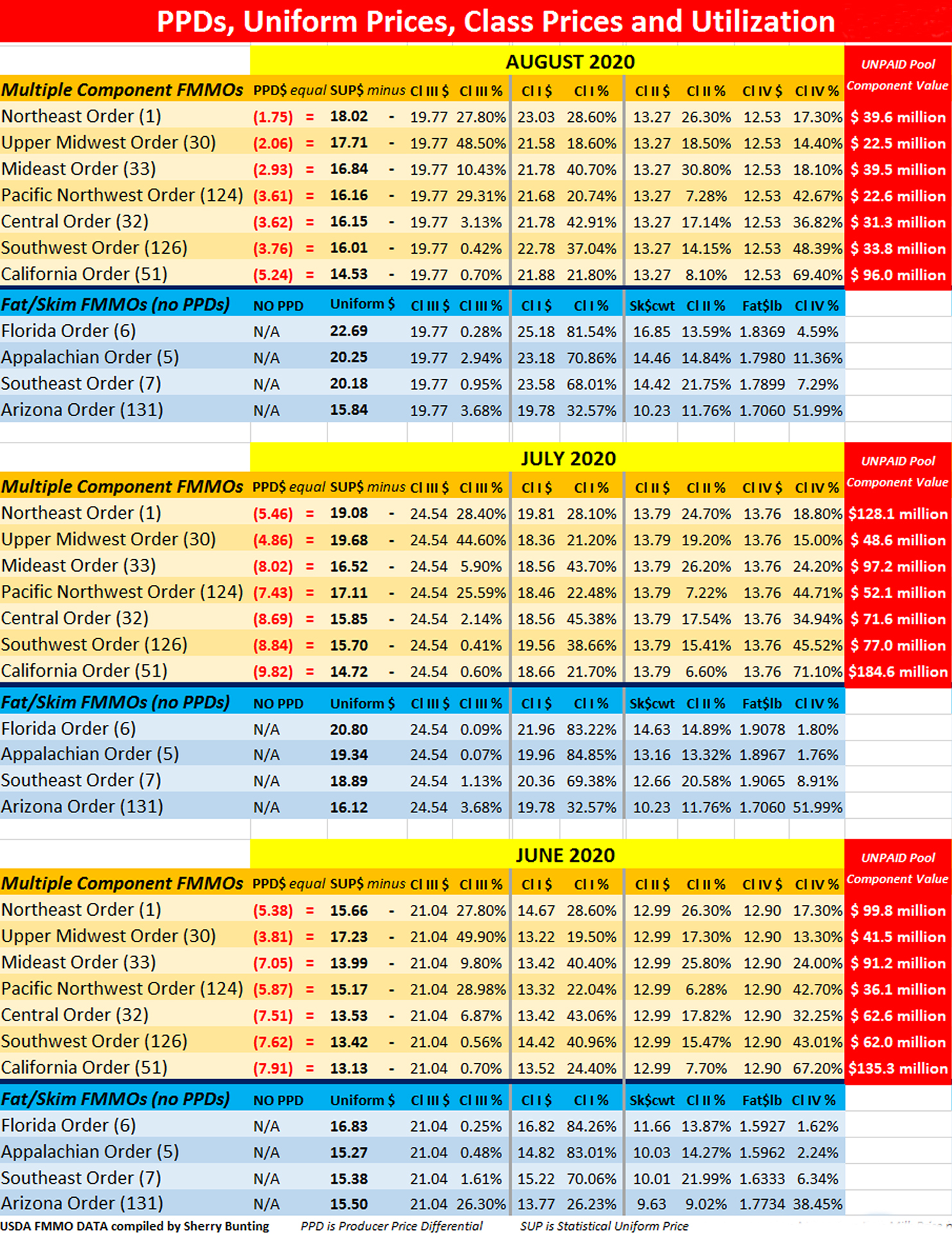

BROWNSTOWN, Pa. — The bottom line is the Federal Milk Marketing Orders are not functioning as farm-level pricing can be easily manipulated.

Negative PPDs continue to persist, and all indications are this could be the case through yearend. Several stories in Farmshine since May have covered the Producer Price Differential (PPD) situation and what it means to producer milk checks.

Now, even the American Farm Bureau Federation (AFBF) is on record evaluating the fallout from the new way of calculating the Class I advance base price as implemented May 2019 after passage of the change was made part of the 2018 Farm Bill.

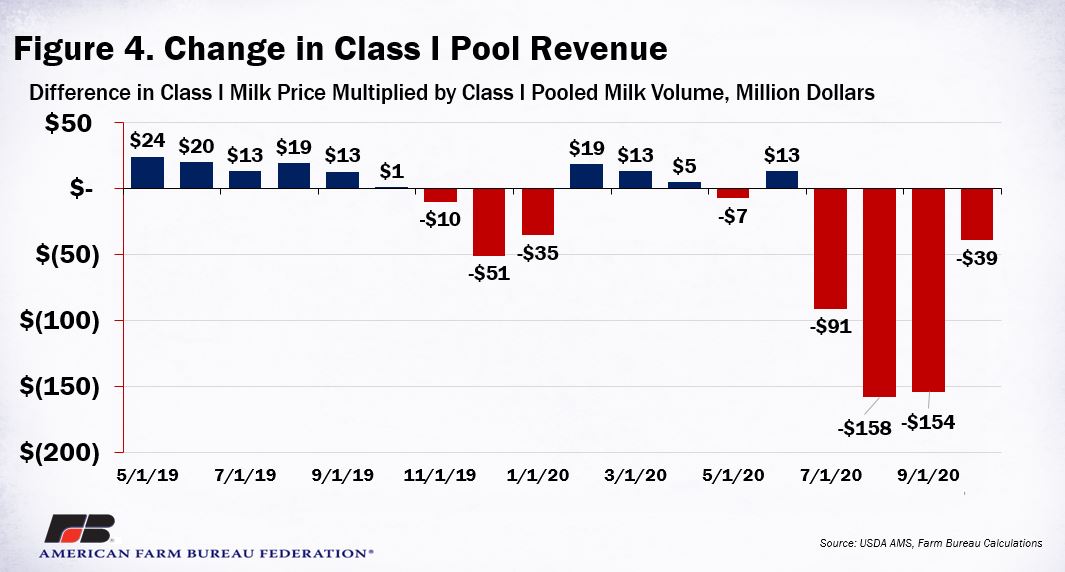

In terms of the money subtracted from Federal Milk Marketing Order (FMMO) pools, Farmshine first reported the $1.48 billion in FMMO revenue gap across 7 of the 11 FMMOs that are multiple component pricing orders. The article and above chart were published in the September 18 edition. September losses will be reflected in FMMO reports in mid-October, and so far PPDs for September milk are mixed, some positive and some negative, but all are well below what would be the case under the old Class I pricing method.

This week, AFBF dairy economist John Newton pegged the cumulative loss to Class I value, alone, at $2.00 per hundredweight or $403 million to-date, across all FMMOs just on Class I milk — money unpaid to farmers that stayed in processor pockets. That figure is about 28% of the $1.48 billion component loss figure shown in FMMO negative balance and it correlates to Class I utilization being roughly 28% of total U.S. milk volume.

The Farm Bureau summary also shows the concentrated loss of $436 million in Class I value for May through October 2020. (Interesting coincidence: DFA is today the largest Class I milk bottler with the May 2020 acquisition of 44 of Dean Foods’ 57 milk bottling plants at a bankruptcy auction price of $433 million.)

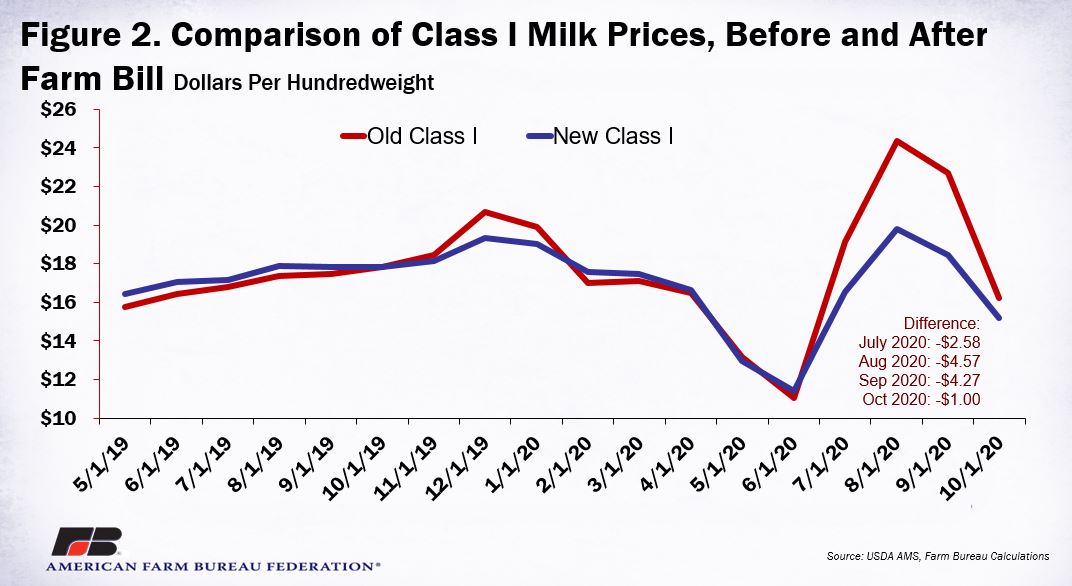

“Due to the rapid rise in Class III prices and a modest increase in Class IV prices, the spread between the two was $6.83 per hundredweight in July, $10.96 per hundredweight in August, $10.30 per hundredweight in September and (will be) $3.56 per hundredweight in October,” writes Newton this week in the Farm Bureau analysis.

“As a direct result of no longer including the higher-of in the milk price formula, the Class I milk price never fully captured the rally in Class III milk prices. Instead, the new Class I milk price was as much as $4.57 per hundredweight below the higher-of formula price in August and $4.26 lower in September,” he continues.

“As identified in Figure 2 (above), had the higher-of formula still been in place, the Class I mover would have exceeded $24 per hundredweight in August,” states Newton.

Newton cites a Class I minimum example for the Southeast, stating that these losses are “before Class I location adjustments are added. In South Florida, for example, with the $6 per hundredweight location adjustment, the Class I milk price would have been more than $30 per hundredweight in August 2020.”

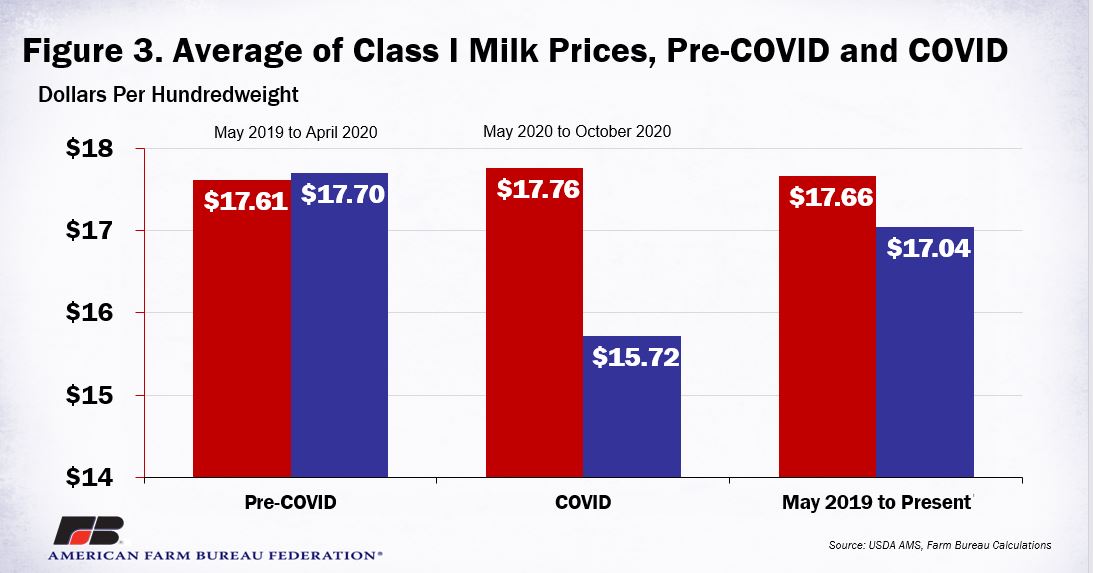

Newton notes that from May 2020 to October 2020, the average difference between the old and new Class I milk price formulas was $2.04 per hundredweight in favor of the beverage milk processor. This means that the regulated minimum prices fluid milk processors had to pay dairy farmers from May through October 2020 were an average of $2.04 lower than what they would have been if the higher-of was still in place.

Going back to May 2019 when the new Class I formula was implemented, Newton notes that the Class I milk price was 62 cents per hundredweight lower on average for the past 19 months compared with the pre-farm bill higher-of formula. (Fig. 3 above)

When looking just at the 12 months pre-Covid from May 2019 to May 2020, the new Class I calculation added 9 cents per hundredweight to Class I pooled volume.

Newton writes that the Class I volume, alone, saw a $32 million benefit in the new Class I pricing in the first 12 months May 2019 through April 2020. Post-Covid, the new Class I pricing method is reflected as a $436 million loss May to October 2020, so the cumulative loss is estimated at $403 million over 19 months of implementation.

This analysis, says Newton, was based on actual Class I pool volume as determined pre-Covid, and does not account for the impact on all milk in and out of the pool for which producers were paid at or near FMMO blend price, before deductions.

The bottom line in looking at the Farm Bureau analysis, along with our own past four months of analysis, the new way of calculating Class I – per the 2018 Farm Bill – would be a relatively benign factor in a ho-hum market if dairy product and component values were at least somewhat accurately reflected across multiple manufacturing classes.

On the other hand, it works poorly in a lopsided market where markets are disrupted, huge government purchases occur on some products and not others, and where huge imports of some products (butter) and not others (cheese) impact accumulating inventory differently for the different milk classes.

While magnified in a severe market disruption like Covid-19 has created, the dairy “market” complex has had lopsided markets in the past and will again in the future at some level. The fact that this pricing change was made without a national hearing and without a dairy producer vote and without an FMMO administrative hearing is concerning.

Some members of Congress have stated that National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) — together — agreed on and requested this Class I pricing change and that Farm Bureau took a non-position, making the change a “no-brainer” for Congress to include in the Farm Bill.

Farm Bureau had done analysis before the change was implemented showing the average over time was neutral. But neutral over time does not reflect month to month cash flow impacts and messed up risk management tools when markets diverge.

What we see in this so-called “neutral” change is the capacity for processors to manipulate the transfer of market value by playing one class against others and essentially removing ‘market value’ from producer milk checks.

Congress needs to hear the story of how dairy farms are impacted in their cash flow and use of risk management tools when a minimum of $1.48 billion in component value is simply sucked out of milk checks over a 4-month period.

Yes, CFAP payments help dairy farmers. But government payments lead dairy even farther away from establishing market value to become more reliant on government payments that, quite frankly, come with more and more strings attached.

Remember, USDA Dairy Programs responded in a Farmshine interview in August to explain that the value missing from pools is “still in the marketplace” even if it doesn’t show up in the FMMO blend prices.

Specifically, USDA stated in that August 3 email that, “The blend price (SUP) is a weighted average of the uses of milk that was pooled for the marketing period (month). If some ‘higher value’ use milk is not in the ‘pool’ then the weighted average price will be lower. It is important to note that the Class III money still exists in the marketplace. It is just that manufacturing handlers are not required to share that money through the regulated pool.

From the looks of milk checks shared in Farmshine’s Market Moos survey in June and July — and looking at the All-Milk prices reported by USDA through August — this ‘money that still exists in the marketplace’ has been largely unshared with producers.

The Class I pricing change was made, according to NMPF / IDFA to so that Class I processors could manage their price risk with forward contracting.

However, CME market brokers and analysts who were questioned about the use of forward contracting by Class I milk bottlers say that few, if any, are doing it. Part of the NMPF / IDFA push for this change was their statements that Class I bottlers would use risk management to stabilize their milk costs if the higher-of method was abandoned in favor of “averaging”.

In fact, some analysts we spoke with report there’s no incentive – even with the new formula – for processors to forward contract a perishable, quick-turnaround product like gallon jug milk. It doesn’t sit in a warehouse like cheese or butter or powder.

… Unless it is shelf-stable ultrafiltered milk — like Coca Cola’s Fairlife products. Coca Cola purchased the remaining shares of Fairlife from the Select Milk Producers cooperative on Jan. 3, 2020 — just 9 months after the new Class I pricing method was implemented.

The industry said this Class I pricing change was needed so that fluid milk processors could stabilize prices and in turn be positioned to invest in fluid milk processing and innovation, which would help dairy producers in the end by providing more Class I markets.

But what happened? Just 6 months after the new Class I pricing method was implemented, the largest fluid milk bottler, Dean Foods, filed for bankruptcy protection and sale in November 2019 with DFA waiting in the wings to buy. Then, 3 months after that, Borden filed bankruptcy and ended up selling to a consortium headed by former Dean CEO Gregg Engles.

Farm Bureau’s analysis this week estimates the impact on dairy farmer revenue from a purely Class I perspective. It does not quantify the full extent of component value removed from FMMOs in the process. Thus, the $403 million cumulative loss impact declared by Farm Bureau represents about 28% of the total loss – which is equivalent to the current nationwide Class I utilization.

This is a Class I pricing calculation change, but its impact on FMMO blend prices and farm-level mailbox prices is pervasive.

In addition, it is important to be aware in this discussion of loss impacts that there is absolutely zero method of calculating the market value of fresh fluid milk. It is not possible to determine what fresh fluid milk is worth because it is:

1) Regulated by federal and state milk marketing orders and boards,

2) Used as a loss-leader by supermarkets selling it far below its cost – especially the largest milk bottling retailers like Walmart and Kroger, and

3) Federal government restrictions on the fat level of milk children are “allowed” to consume at school or daycare.

In short, the federal government controls fluid milk through USDA in lockstep with NMPF / IDFA — and don’t forget, DMI. Dairy checkoff figures prominently in this equation with the same heavyweights at the same table — pushing fat-free, low-fat, ultrafiltered, shelf-stable products, even 50/50 plant-based blends.

Even DMI CEO Tom Gallagher is on record stating that the white gallon isn’t the future because even if children can have whole milk “innovation” is needed and admitting that his job is to “get processors to do stuff with your milk”.

For processors to “do stuff with your milk”, they have to be promised a bigger margin. This could explain why the forward-looking focus of farmer-funded checkoff efforts is on innovation (processing partner margin), not on promoting and educating consumers about fresh fluid milk. And, it might explain why this new Class I formula was needed to average the only so-called market value left in the so-called dairy market.

CFAP payments are salve on some wounds, but the larger issue is still clear: Dairy producers need a voice — apart from the organizations that claim to represent them.

By Sherry Bunting, published Sept. 14, 2020 in Farmshine

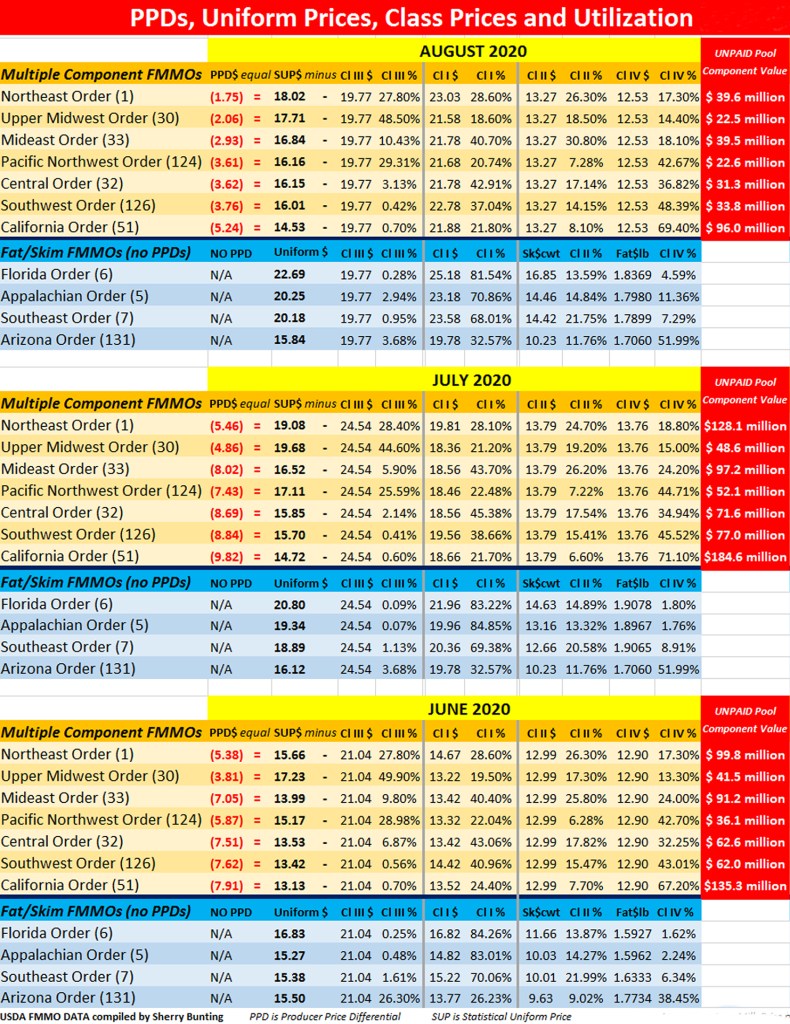

BROWNSTOWN, Pa. — The negative Producer Price Differentials (PPDs) persisted in final payments for August milk received by dairy farmers in mid-Sept., according to uniform prices announced by USDA Federal Milk Marketing Orders September 11 and 12.

This pushed uniform prices lower in some Federal Orders, while others were higher. (See chart above).

The bottom line is a cumulative loss impact of $1.48 billion in UNPAID market value of milk components across the seven Multiple Component Pricing Federal Milk Marketing Orders (FMMOs) — not to mention unquantified losses in the 4 fat/skim pricing FMMOs — after three months of significantly negative PPDs for June, July and August milk as paid in July, August and September 2020.

Losses incurred by the four Fat/Skim Pricing Orders, but are not easily quantified on the FMMO pool balance sheet and were most pronounced in June for those FMMOs.

More losses will be added for September milk, paid in October, and the CME futures indicate loss impacts could continue through yearend.

This unpaid component market value — represented by negative PPDs (the difference between the uniform price and the announced Class III price) — has cost dairy producers using risk management tools even more as such tools utilize primarily the Class III price as a market indicator. When the Class III price rallies, but the milk check doesn’t mirror that, a producer can be left without the higher price in the milk check and without the coverage through the risk management at the same time.

This would be like having a fire and having the adjuster look at a neighbor’s intact house to determine no claim, instead of looking at the house that burned. When the market says ‘no fire here’ but the house burned down just the same, it’s a double-whammy.

Remember, fluid milk does not have a ‘market’ because the Class I price is both regulated at varying degrees by state and federal marketing orders, and at the same time, fluid milk is used as a loss-leader by the nation’s largest supermarkets. Thus, it is impossible to determine the “market value” of fluid milk.

Add to this the restriction of fat content in schools and other institutional feeding by the federal government, and market value of fluid milk – especially whole milk – is further impinged by non-market factors.

This means the value of the components in fluid milk can only be assigned by the value of dairy products made with milk. When that market rallied on Class III, while plummeting on Class IV, the “market” value was pulled instead of pooled.

Several factors are creating the problem.

First, Covid-19 caused disruption in markets that are now heavier on the retail side and lighter on the foodservice side. The industry is adjusting to this.

Second, a ‘band aid’ approach to milk pricing reform in the 2018 Farm Bill changed the Class I relationship to an uptrending manufacturing class market by using an averaging method instead of the “higher of” Class III or IV. This is just one reason a national hearing on milk pricing with report to Congress is long overdue.

Third, the spread between Class III and IV milk futures persists, so even when Class I and Class III were close in price for August, Class IV and II were so far behind that negative PPDs and de-pooling occurred. Current levels show a $4 to $5 spread for September and October and $2 to $3 for November and December.

Fourth, government purchases and import-export factors are affecting storage of Class III and IV products differently, which in turn affects the markets differently.

As mentioned previously in Farmshine, the most recent USDA Cold Storage Report showed butter stocks at the end of July were up 3% compared with June and 13% above year ago. On the other hand, total natural cheese stocks were 2% less than June and up only 2% from a year ago.

On the import side, the difference between cheese and butter is stark. Cheese imports are down 10% below year ago, but the U.S. imported 14% more butter and butterfat in the first seven months of 2020 compared with a year ago.

Is it any wonder butter stocks are accumulating in cold storage to levels 13% above year ago at the end of July — putting a big damper on butter prices and therefore Class IV?

Butter demand is up. Butter imports are up. But the PRICE of butter is at the lowest level since 2013.

Analysts suggest that butter and butterfat imports are higher because U.S. consumer demand for butterfat is higher. But that reasoning doesn’t make sense because the Class IV price and butterfat value is depressed because of “burdensome inventory of butter” in cold storage, holding back butter prices and amplifying the Class III and IV divergence that is at the root of the negative PPDs.

Again, a national hearing on milk pricing is long overdue. Even the risk management tools touted by USDA do not perform as expected due to inverted and divergent price relationships and reduced ability to transfer market value.

On October 5, 2020, American Farm Bureau published its analysis which evaluated a similar loss impact. Read the AFBF analysis here

Second checks under CFAP 1 delayed by enrollment extensions

By Sherry Bunting, Farmshine, Sept. 25, 2020

WASHINGTON, D.C. — President Donald Trump and U.S. Secretary of Agriculture Sonny Perdue announced an expansion of the Coronavirus Food Assistance Program (CFAP) on Sept. 17, which means a second round of $14 billion in additional CFAP payments will be made to a new list of eligible commodities, including dairy cow’s milk as a price-trigger calculation and even goat’s milk as a sales-triggered calculation.

Sign up for this second round of assistance – CFAP 2 — runs from Sept. 21 through Dec. 11, 2020.

CFAP 2 payments for dairy calculate to a little over $2.00 per hundredweight on the equivalent of April through August milk marketings. However, the calculation boils down to $1.20/cwt on actual April through August milk marketings, plus another $1.20/cwt on the estimated September through December milk marketings – a 4-month period – using the average daily milk production from the prior 5-month’s actual marketings.

Specifically, the announcement describes the CFAP 2 dairy payments as follows:

Payments for cow milk under CFAP 2 will be equal to the sum of the following:

1) The producer’s total actual milk production from April 1, 2020, to August 31, 2020, multiplied by the payment of $1.20 per hundredweight, and

2) The producer’s estimated milk production from September 1, 2020, to December 31, 2020, based on the daily average production from April 1, 2020, through August 31, 2020, multiplied by 122, multiplied by a payment rate of $1.20 per hundredweight.

This round of farm assistance, known as CFAP 2, follows in addition to CFAP 1.

The CFAP 1 payments were to be made in two stages, with enrolled producers having received most of their eligible payment in their first check. However, the second portion or balance of payments under CFAP 1 won’t be received until after all enrolled producers receive their first checks.

Producers have not yet received their second checks from CFAP 1 because the enrollment period for CFAP 1 was extended through Sept. 11.

Further complicating payment of second checks under CFAP 1 is USDA’s extension of signups for certain counties in Louisiana, Oregon and Texas that were impacted by natural disasters (fires and hurricanes). Producers in those areas have until Oct. 9, 2020 to enroll in CFAP 1.

Once all enrollments in CFAP 1 are completed by Oct. 9, and once all enrolled farms receive their first checks for all eligible commodities under CFAP 1, then the remaining funds from CFAP 1 will be disbursed in the second checks to enrolled producers for eligible commodities, including milk.

CFAP 2, on the other hand, represents a totally separate second source of funding and assistance — and a second enrollment period — to cover market disruptions and additional marketing costs for the nine months period of April through December, whereas CFAP 1 covered mainly the disruptions for the first part of the year. There is some overlap in the time period, but these are two separate enrollments and calculations under CFAP.

To-date, according to USDA, nearly $1.75 billion has been paid to dairy farmers for milk under CFAP 1. The total paid or approved for payment to-date for all commodities under CFAP 1 is $10.2 billion.

Funds for CFAP 1 and 2 are from a combination of the CARES Act and the CCC. USDA used public feedback to make improvements under CFAP 2, according to Secretary Perdue.

CFAP 2 divides commodities into three categories for compensation as 1) Price Trigger Commodities, 2) Flat-rate Crops, and 3) Sales Commodities. Each category has a different method for calculating a payment.

Eligible livestock, including beef cattle and dairy cattle destined for beef, will be based on maximum owned inventory on a date selected by the producer between April 16 and August 31, 2020. USDA FSA personnel report that it’s okay if the date selected by a producer is within the same window as the date selected for CFAP 1 livestock payments as long as the animals in inventory on that date were destined for market as meat animals, not for dairy purposes.

USDA FSA personnel indicate that cull dairy cows are not eligible livestock under CFAP 2, but bull calves and any heifers identified as market animals for beef or veal can be claimed as inventory for market impact payments under CFAP 2.

Corn silage and other forages grown as feed for dairy cattle are also eligible under the corresponding flat rate acreage crops portion of CFAP 2

A complete list of farm commodities covered under CFAP 2 is available at farmers.gov/cfap

As with CFAP 1, there is a payment limitation of $250,000 per person or entity for all commodities combined. Applicants that are corporations, LLCs and partnerships may qualify for additional payment limits when members actively provide personal labor or management to the operation.

In addition, USDA reports that this special payment limitation provision has been expanded to include trusts and estates for both CFAP 1 and 2.

Producers will also have to certify they meet the adjusted gross income limitation of $900,000 unless at least 75% or more of their income is derived from farming, ranching or forestry-related activities. Producers must also be in compliance with Highly Erodible Land and Wetland Conservation provisions to receive payments.

USDA reports that Farm Service Agency staff at local USDA Service Centers will work with producers to file CFAP 2 applications. Producers interested in one-on-one support with the CFAP 2 application can also call 877-508-8364 to speak directly with a USDA employee ready to offer assistance at the call center.

Farmers can also visit farmers.gov/cfap for additional information.

Huge new cheese processing capacity is negative, a somewhat ‘balanced’ global powder inventory is positive

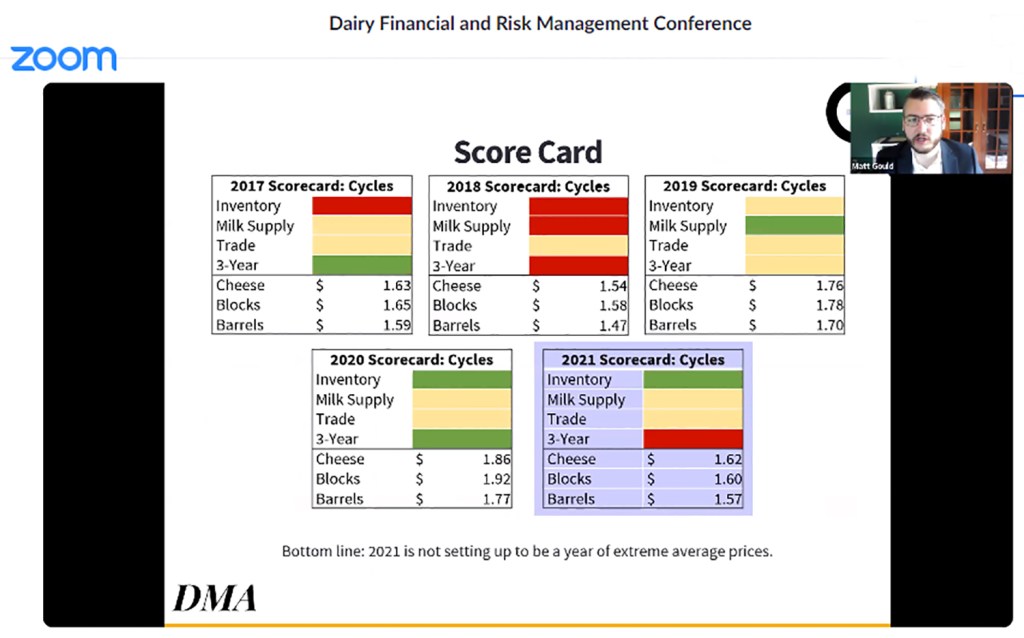

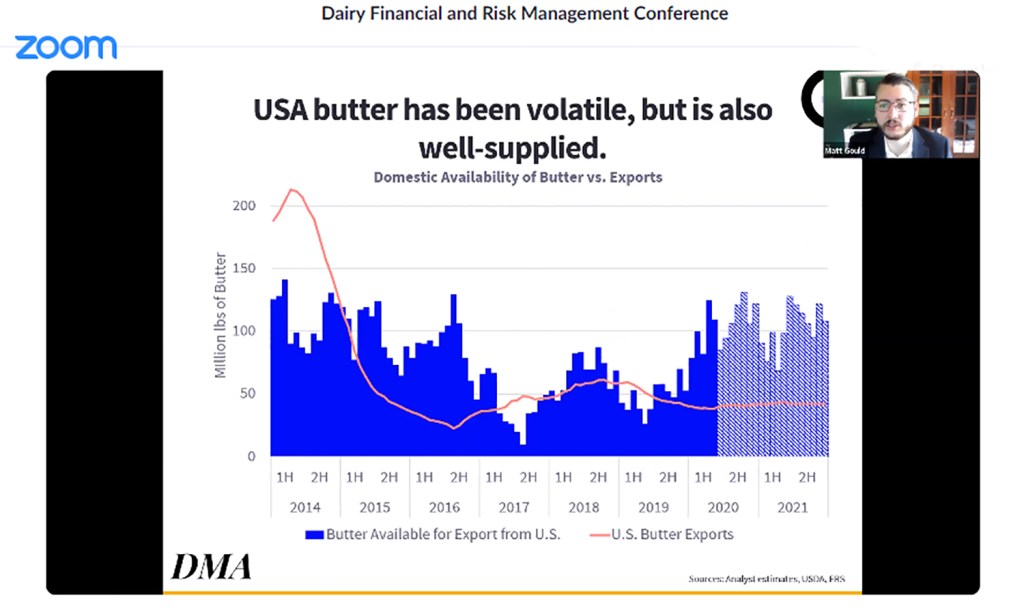

During the Dairy Financial and Risk Management Conference held virtually by Center for Dairy Excellence via Zoom, Matt Gould of Dairy Market Analyst Inc. showed how four long-term global dairy cycles were anticipated for 2017 through 2020 and are forecasted to be mostly neutral or “mediocre” for 2021. Zoom conference screenshot

By Sherry Bunting

HARRISBURG, Pa. — Back in December of 2019, “No one thought 2020 would be a bad year. What wallops you over the head are the unknowns,” said Matt Gould, president of Dairy & Food Analyst Inc. last Wednesday during the Center for Dairy Excellence Risk Management Conference held virtually. The list of over 100 attendees was a v‘who’s who’ of dairy market analysts, brokers, cooperative marketers, consultants and lenders with a sprinkling of farmers.

As for the 2021 outlook sitting here in September with so many unknowns, Gould said the consensus is next year will be a “mediocre” year for dairy markets.

“We can only talk about the known-knowns, with plenty of room for surprises,” he said, focusing on four long-term trends through forecasting models.

From a high level view, Gould said the conflict between indicators that are price-supportive and indicators that are price-negative will temper each other to be more-or-less “a wash in terms of market direction” – except for the influence of surprises one way or the other.

He discussed these trends within the context of how a producer’s milk check is figured, looking at cheese and whey setting the Class III price and butter and nonfat dry milk setting Class IV.

Putting some emphasis on the huge new cheese production facilities coming into operation at the end of 2020 and first quarter of 2021 in both the U.S. and Europe, Gould’s forecast for product prices included low cheese prices next year, stable butter prices, and the highest skim milk powder prices the world has seen in a long time.

The 3-year cycle

The 3-year cycle is still one of the four patterns that most people are familiar with. Historically, it has done a good job of reliably nailing the highs and lows, but not how high or how low, said Gould.

It is also the simplest of the four major patterns. If 2018 was the low in a 3-year cycle, then 2021 will be the next low – 2006, 2009, 2012, 2015, 2018…. 2021.

The global milk supply cycle

The second cycle Gould talked about was the global milk supply cycle, and this cycle is “neutral-ish” for 2021.

Globally, there is milk production growth, but it is not surging, said Gould.

“That’s the good news. We don’t have this wall of milk coming at us, but the flip side is that we don’t have a big contraction either to set us up for really good milk prices like in 2014,” he explained.

Globally, farmers have grown milk production through June, but only by 1 billion pounds per month. “When we cross that 1.5 to 2 billion pounds per month threshold, that’s the guard rail. That would be excessive over-supply territory,” said Gould. “We want some growth to keep balance with demand. There is rising dairy demand as the population grows and the middle class rises, but if we get over that guard rail, then growth becomes inventory.”

So, on global supply as a cycle, 2021 is neutral because global production is growing, but at a pace that should mirror demand growth.

The inventory cycle

On the global dairy inventory side, Gould said the set up into 2021 is “more price supportive.” Mainly because the global supply of the world’s balancing product – milk powder – is on the tight side of adequate.

“When we have big powder inventory, it overhangs the market and prices tend to be lower. Spikes happen when the trade is drawing down supply or when there is no overhang,” said Gould.

Heading into 2021, he said the dairy market with respect to global milk powder inventory “is in a price inflationary zone. We don’t have big inventory and we’re not setting up to build big inventories, so the risk of a good year for milk prices is still in there within this inventory cycle.”

The inventory cycle is setting up to be a price supportive one for 2021.

The trade cycle

Over the past 20 years, the world has gone through a period of booking trade agreements rapidly and aggressively. “We got new customers, grew exports, saw new opportunities and new demand,” said Gould. “The bad news is we have not booked any new WTO-style agreements in a long time.”

Gould explained that WTO-style agreements are the kind that give dairy access to new markets that grow quickly as opposed to more sales within existing markets that grow slowly.

Those WTO-style agreements of the past presented a “trade tailwind” fueling rapid market growth. “This lack of a trade tail wind is price negative for 2021,” said Gould. “The long-term view shows a lack of new global demand growth, which will hurt us.”

Gould acknowledged that the U.S. is getting a new style of trade agreement. “We have trade negotiations ongoing with several countries and we have taken existing agreements and negotiated new ones with the same customers. So, we are seeing new market access but not the advantages of WTO-style access.”

Gould sees the change from rapid growth to steady access in this trade cycle as setting up to be price negative.

Taken together, these four cycles show 2021 setting up with two neutrals, one negative and one positive.

Class III and IV expected to flip

As the indicators will be mixed, so will dairy product markets.

Gould’s cheese forecast is for an average $1.62/lb and his forecast for nonfat dry milk is that prices could reach $1.23/lb.

In farm milk checks, said Gould, it’s no simple task how milk prices get determined. “We use end products so it’s not a question of what the milk is worth, but what these products are worth, and it subtracts-out the cost of making the products and a yield factor too.”

Ostensibly, the Class II prices uses Class IV and the Class I price uses all the classes.

With Class III so much higher presently than the other classes, Gould noted the switch is setting up to flip for 2021.

Milk powder prices are expected to rise into and through 2021 because the big surpluses are gone and 2019 production kept pace with demand, which ended up drawing down on global powder supplies even further, with 2020 being more in balance heading into the first half of 2021.

While a penny change in nonfat dry milk price brings 8 cents to Class IV price a penny change in butter equates to 4 cents change in the Class IV price. Powder will be the more positive side of the 2021 setup compared with butter, according to Gould.

“The global butter market in 2020 saw big destruction of food service demand, which affected cheese, so processors (globally) made more butter, and foodservice is not using as much butter,” said Gould.

“In the short-term, there is an overhang of butter inventory, especially in the U.S., where we had big destruction of demand and the lowest butter price since 2013,” said Gould. “But people call me and say they can’t find butter on the shelf at the store, so how can this be?”

How can we have the lowest wholesale butter price and not be keeping up with retail demand?”

Gould explains that 55% of U.S. butter consumption pre-Covid was foodservice – going out to eat. In this pandemic environment, the foodservice industry has been devastated. Open Table, a company that books restaurant reservations estimates foodservice is still down by half and full-service restaurants are decimated.

“On the flipside, retail butter sales have been extraordinary at times, with some weeks more than doubled over year ago,” said Gould. But plants in the U.S. are specialized moreso than in Europe where dairy plants are more flexible making more different products instead of specialized for high volume and efficiency.

Matt Gould, Dairy Market Analyst Inc. talked about the differing market and inventory conditions for dairy products into the end of 2020. U.S. butter exports are down, imports are up, and U.S. butter inventory has been built up. Globally, butter is well supplied as more versatile plants in Europe switched from cheesemaking to butter when Covid-19 shut down the restaurant trade. Zoom conference screenshot

“Where we have the bottleneck in the U.S. is turning bulk butter into quarter pound sticks for retail,” he said, adding that in the past21 days, retail butter sales have slowed to show smaller growth rates over year ago.

In short, while holiday sales will help boost fourth quarter, it won’t make much difference in the overall butter picture because “we’ve already gone through the demand destruction and the inventory is already built. We have more butter in stock than we have domestic sales so we are in surplus,” said Gould.

Gould did not specifically mention the large imports of butter and butterfat into the U.S. from March through July, but he did reference the bottleneck in turning enough bulk butter into sticks for retail. As this pushed retail butter prices higher, Gould noted that importing was incentivized.

Cheese is where some “known surprises” come into play.

The U.S. will see significant new cheese production capacity becoming operational in November (Michigan) and the beginning of 2021 (Minnesota).

“Every one penny in cheese price change is 10 cents of change on the milk check,” Gould pointed out. “As a globe, we are in relatively balanced to tight supply on cheese in the second half of 2020, but the forecast heading into 2021 is driven by the factories and capacity being built.”

He said the long-term export trend for cheese is positive. It has been a “winner” during Covid because the big cheese purveyors are pizza companies that were the first to adopt low and no-contact delivery and saw their sales surge 20% higher.

But new cheese processing capacity in the U.S. and in Europe will present short-term concerns.

“We will see huge growth in cheese processing,” said Gould. The plant in St. John’s Michigan as a joint venture of DFA, Select and Glanbia will be the sixth largest in the country.

“We have never opened a plant in the U.S. that big – that fast – in history. This is a first, and these types of plants have to be run full, or you will lose your tail,” he said, noting these types of plants in the American cheese business operate on margins of 0.5% (one half of one percent). “They’ll make a penny on a $2/lb cheddar price. That’s why they fill full and build to scale and magnitude to make volume.

“The consequence of that is a shock increase in supply,” said Gould. “Demand doesn’t grow that same way. We don’t wake up and see new demand present itself as a shock-increase like that.”

Some wild cards do exist, including government intervention. What we’ve seen already this year in dairy purchases is greater than dairy has seen in a long time.

“Government purchases (CFAP) are using 2.5 to 3% of the U.S. milk supply,” said Gould. “Normally we forecast within 1% to say a year will be good or bad, but when those purchases end, we are talking about 2.5 to 3%. That’s a huge number. That’s a price negative thing if all of a sudden there’s 2% more milk on the market without government purchases.”

The flip side, he said, is “We are going through a crisis, and people are hungry. When you have hungry people, the prescription is to get them food.”

In this way, government purchase could be a positive wild card if they continue under circumstances where economic slowdown impacts domestic demand.

Other wild cards of course include the progress on a vaccine for Covid, and the status of the economy and foodservice. Positives in those areas could unleash demand for products that can be made quickly in bulk without the bottlenecks of serving retail demand.

— Previously published in Farmshine, Sept. 25, 2020

Producers share priorities, experiences during risk management conference

A panel of producers during the Center for Dairy Excellence Risk Management Conference last week agreed their top priority is stabilizing input costs, especially feed, is the first component to any dairy risk management strategy.

HARRISBURG, Pa. — How are dairy producers navigating the rapidly changing dairy markets? A panel of Pennsylvania producers shared during the 11th annual Center for Dairy Excellence Risk Management and Financial Conference, conducted ‘virtually’ by Zoom in September with an audience each day of over 100 people, most of them dairy lenders and consultants.

“Risk management is important, but it takes planning,” said Mike Hosterman of AgChoice Farm Credit, moderating the panel comprised of Mark Mosemann, who farms with his father and brother milking 450 cows at Misty Mountain Dairy, Fulton County; Glenn Kline, who farms with his two sons milking 600 cows at Y-Run Farms in Bradford County; and Rod Hissong, who farms with his brother milking 1600 cows at Mercer Vu Farms in Franklin County, Pa. and 1200 cows at their satellite dairy 65 miles south in Whitepost, Virginia.

Polling the audience, Hosterman revealed a low percentage of lenders see a risk management or marketing plan from clients.

All three producers put a big emphasis on the input side of the margin since 2012. Some common themes and priorities emerged.

Stabilize feed costs

The 2012 margin squeeze caught many producers by surprise as milk prices skyrocketed and feed prices went wild.

After that happened, all three panelists aimed to expand their land base through ownership and especially rented ground to produce all of their own forages and a portion of energy and protein.

They also increased inventory capacity to buy and store feed commodities and do risk management with local feed mills.

By stabilizing feed costs – the largest input cost on the dairy – they are positioned to operate the business, plan for the future and think about risk management opportunities on the milk side.

Hissong noted that their expansion with a satellite farm in Virginia was also a hedge on the future in terms of the next generation. The brothers will be able to downsize or upsize depending on how the future shapes up for sons, daughters, nieces and nephews because they invested in two sites, not expanding into one larger site.

Value of networking

“Don’t underestimate your networking capability,” said Mosemann, who described how this enabled his family to acquire rented ground and work with others in custom harvesting and feed inventory.

For Hissong, relationships on buying forage changed to relationships in acquiring ground.

They also brought more pieces under their own management, now raising their own dairy replacements and hauling their own milk.

The satellite dairy allows the Hissongs to manage weather risk on the feed side and to set up their cow flows to gain labor efficiencies in operating the dairy. Baby calves are raised at the home farm and go to the Virginia site when bred. They stay there through gestation and calving and for milking through first, sometimes second, lactation.

Kline and Mosemann both purchase some inputs collectively with other farms, which is a risk management strategy more producers are using to stabilize costs today. They also work with other farms in custom harvesting and trucking.

Relationships with feed mills offer additional opportunities to manage risk, and relationships with the nutritionists, veterinarians, and financial advisors bring ideas to the farm.

Two ways to breakeven

All three producers use their farm accountants to do both a cost of production analysis as well as cash flow analysis to come up with a Class III price that meets their farm’s breakeven price in both scenarios, including the cost of the risk management.

That’s essential because producers can’t afford to pay for risk management that doesn’t secure breakeven or better.

“We take the COP analysis and come up with a gross milk price. We calculate our basis into that and look at the Class III price that is required for us to break even,” said Mosemann, explaining that a separate cash flow analysis, with net income offsets, calculates a final Class III price target. “That’s what we use to measure against when deciding what to buy, and our goal is to come out of it with a net price above the net breakeven.”

Even armed with this knowledge, relying on the Class III breakeven method has become a challenge today with the inverted basis from negative PPDs.

While the basis on milk in the East has declined rapidly along with the declining Class I milk utilization over the past decade, at least it has been relatively stable and could be plugged into a Class III breakeven strategy at an approximate level.

However, in the current market, a “Class III breakeven” is much more difficult to calculate because the basis is all over the place and mostly negative. Looking out at risk management for the next six to 12 months is frustrating even for those who have been doing this for a while.

Hissong observed that their strategy changes with conditions, but a key to making it work is to keep their variable costs “fairly flat” from one quarter to the next.

“We are not trying to ‘guess the market,’” he explained. “We are trying to gather information and make an educated decision. We are trying to protect the breakeven.”

Watching it daily allows him to adjust using other tools through the cooperative. Forward contracting through the cooperative means no margin calls, but Hissong noted that, “Once you take a position, you are locked into that position.”

Having both Class III and IV contracts helped because where they lost on Class III because it went higher, they gained on Class IV because it went lower.

Layered approach

All three producers use a layered approach. They don’t put all their milk in one basket and they don’t necessarily cover all of their milk.

They start by using the Dairy Margin Coverage (DMC) on the first 5 million pounds of annual production.

Each farm on the panel also forward contracts with their respective cooperatives, and they use more than one tool offered by the cooperative. They have also used Dairy Revenue Protection (DRP) on a portion of their milk in a few quarters where it made sense.

Dedicated person

It is essential to have someone within the farm ownership core who manages the strategy and is looking at it every day, the panelists said. This is not something they do and then forget about, or hand off to someone else.

“You’ve got to be passionate about it. It takes a lot of time, and you’ve got to look at it every day. So that means someone has to have the time to do it, and enjoy doing it,” said Kline, who does the risk management at Y-Run.

For Mercer Vu, that person is Rod, and at Misty Mountain, it is Mark’s father.

Kline says he is able to do it because his two sons are doing the other things in the operation. “This gives me another perspective in the operation of the business to work on,” he explained.

“This is such an important part of our bottom line, so we believe we have to be more involved in it,” Hissong said. “The first thing to know is COP, so we know what price to protect. We have to know what is a profit. We do cash flows and budgets with Mike Hosterman and work with Acuity to do quarterly accrual-based accounting so we can calculate-back our breakeven through Class III and basis.”

“Risk management is not always successful,” Mosemann acknowledged. “But our strategy is to get base-hits, not a grand-slam homerun. If we can get on base and stabilize things, then we can plan. Risk management is now a cost of doing business for us to protect against the volatility we see.”

All three producers said they tap other resources for information in addition to those they work with on risk management.

Difficult environment

The current market environment is a difficult one in which to execute a risk management plan.

These producers do their homework, develop their strategies, layer their tools, know their breakevens, know their goals, watch the markets, work with their team — but still find it difficult to know over the next six to 12 months when to pull the trigger at what looks like a breakeven forward contract or price floor due to the unknown and negative basis relative to Class III.

Each producer said they would participate in more risk management right now, but it’s difficult to assess a breakeven level because the tools based on CME futures do not match up with how their farms could ultimately be paid for the milk in those future months.

Without knowing how their cash price will perform in relation to the futures price, it’s hard to commit to a strategy that worked in the past, so new thinking is needed. The producer needs to have a handle on what to do about basis. Will the farm’s cash price move in the same direction as the futures, and by what margin of premium or discount will the cash price move? This is part of the decision making when working through a plan.

Using advisors

All three producers mentioned working with their farm and financial advisors as a key to risk management. They see lenders starting to require some level of risk management and foresee this being part of lending packages in the future.

A little bit of everything

From renting more ground and networking with others, to contracting feed, creating inventory, running cost of production, budget and cash flow analyses and using multiple tools from DMC and DRP to forward contracting, these dairy producers say a little bit of everything adds up to some base-hits to keep margins in a zone where they can operate the business and plan for the future.

“With the way the last four to five years have been, and seeing how politics and a global pandemic can turn everything on its head, if we are looking to purchase land or expand for the next generation, we better have risk management in place even if the lender doesn’t require it,” said Kline.

Hissong added that, “We continue to see our industry change. For those actively wanting to be in it and see a future in it, or if they have to work with someone to make a go of it, risk management will almost become mandatory.”

At the same time, he observed that the government CFAP payments and dairy product purchases add another ripple.

“The CFAP payments changed the balance sheet for us, and they were definitely needed from the perspective of our dairies coming out of a rough spot and scary time,” said Mosemann.

At the same time, noted Hissong, the government involvement has an effect on the market “when trying to figure out market signals and trying to figure out what to do in 2021.”

With milk class and component pricing relationships in turmoil from pandemic disruptions and government intervention, risk management is more difficult to do right now.

Even so, these producers would encourage others to take this time to learn more about it, to work through their numbers and work through some scenarios to be prepared to implement risk management at some level in the future.

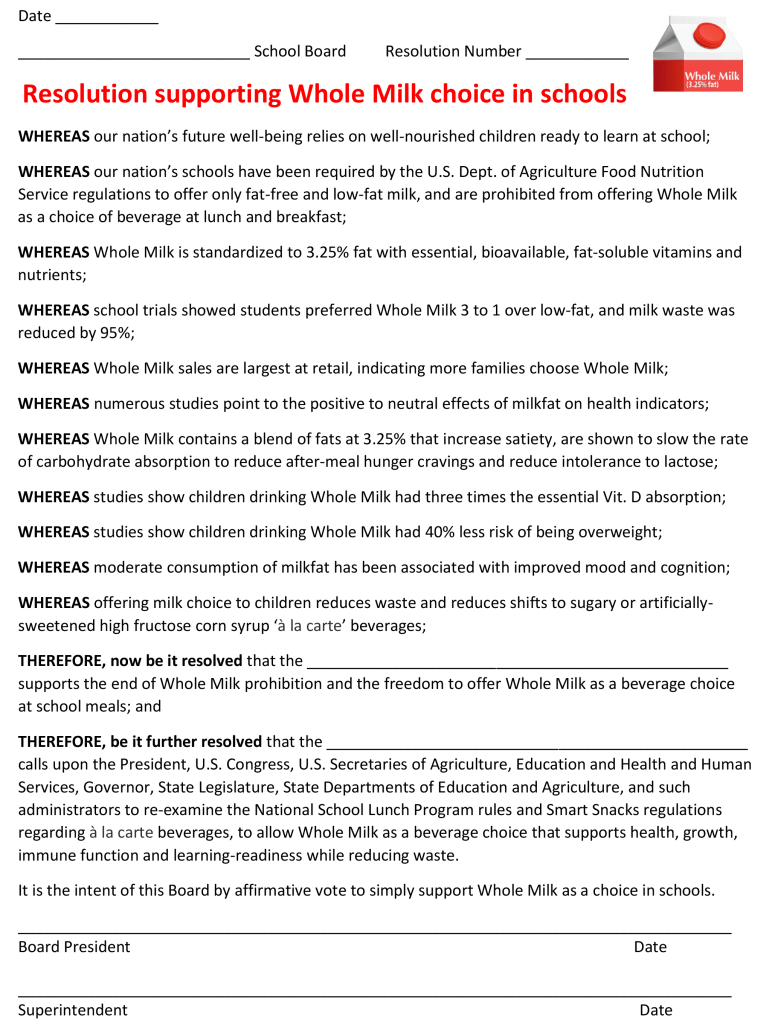

Nelson Troutman, a dairy farmer in Berks County who started the “Drink Whole Milk 97% Fat Free” round bale painting in January 2019 that led to the 97 whole milk education effort, was the first to get a “Vote Whole Milk — School Lunch Choice” yard sign. He’s pictured here with grandchildren (l-r) Jase, Emma, Evelyn, Carolyn, Jocelyn, Nolan, Madalyn. Photo submitted

EPHRATA, Pa. — It’s campaign season, and here’s a campaign everyone should be able to get behind: “Vote WHOLE MILK — School Lunch Choice — Citizens for Immune Boosting Nutrition.”