Huge new cheese processing capacity is negative, a somewhat ‘balanced’ global powder inventory is positive

By Sherry Bunting

HARRISBURG, Pa. — Back in December of 2019, “No one thought 2020 would be a bad year. What wallops you over the head are the unknowns,” said Matt Gould, president of Dairy & Food Analyst Inc. last Wednesday during the Center for Dairy Excellence Risk Management Conference held virtually. The list of over 100 attendees was a v‘who’s who’ of dairy market analysts, brokers, cooperative marketers, consultants and lenders with a sprinkling of farmers.

As for the 2021 outlook sitting here in September with so many unknowns, Gould said the consensus is next year will be a “mediocre” year for dairy markets.

“We can only talk about the known-knowns, with plenty of room for surprises,” he said, focusing on four long-term trends through forecasting models.

From a high level view, Gould said the conflict between indicators that are price-supportive and indicators that are price-negative will temper each other to be more-or-less “a wash in terms of market direction” – except for the influence of surprises one way or the other.

He discussed these trends within the context of how a producer’s milk check is figured, looking at cheese and whey setting the Class III price and butter and nonfat dry milk setting Class IV.

Putting some emphasis on the huge new cheese production facilities coming into operation at the end of 2020 and first quarter of 2021 in both the U.S. and Europe, Gould’s forecast for product prices included low cheese prices next year, stable butter prices, and the highest skim milk powder prices the world has seen in a long time.

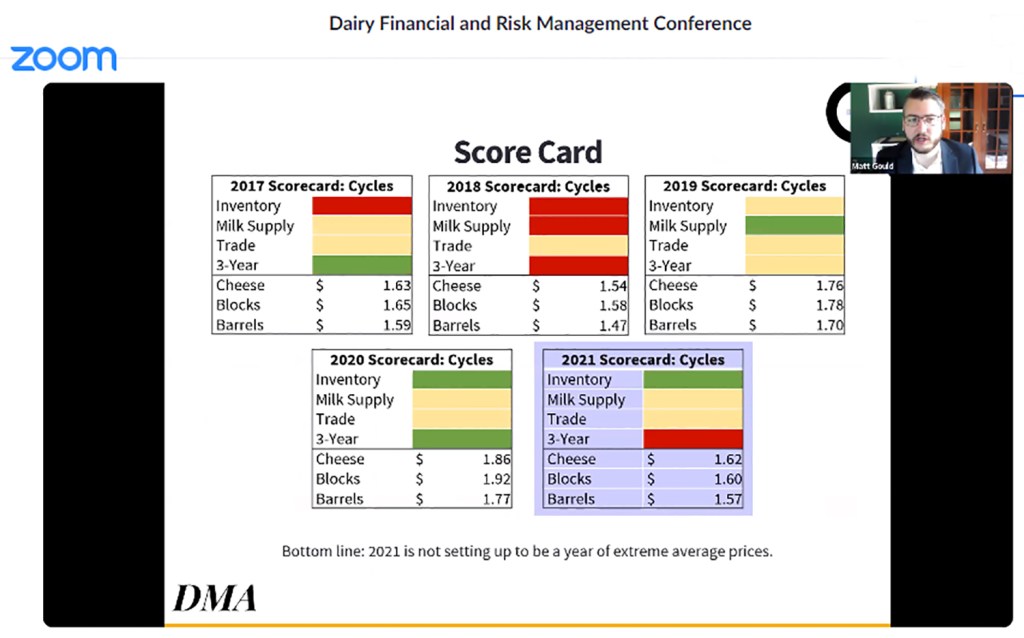

The 3-year cycle

The 3-year cycle is still one of the four patterns that most people are familiar with. Historically, it has done a good job of reliably nailing the highs and lows, but not how high or how low, said Gould.

It is also the simplest of the four major patterns. If 2018 was the low in a 3-year cycle, then 2021 will be the next low – 2006, 2009, 2012, 2015, 2018…. 2021.

The global milk supply cycle

The second cycle Gould talked about was the global milk supply cycle, and this cycle is “neutral-ish” for 2021.

Globally, there is milk production growth, but it is not surging, said Gould.

“That’s the good news. We don’t have this wall of milk coming at us, but the flip side is that we don’t have a big contraction either to set us up for really good milk prices like in 2014,” he explained.

Globally, farmers have grown milk production through June, but only by 1 billion pounds per month. “When we cross that 1.5 to 2 billion pounds per month threshold, that’s the guard rail. That would be excessive over-supply territory,” said Gould. “We want some growth to keep balance with demand. There is rising dairy demand as the population grows and the middle class rises, but if we get over that guard rail, then growth becomes inventory.”

So, on global supply as a cycle, 2021 is neutral because global production is growing, but at a pace that should mirror demand growth.

The inventory cycle

On the global dairy inventory side, Gould said the set up into 2021 is “more price supportive.” Mainly because the global supply of the world’s balancing product – milk powder – is on the tight side of adequate.

“When we have big powder inventory, it overhangs the market and prices tend to be lower. Spikes happen when the trade is drawing down supply or when there is no overhang,” said Gould.

Heading into 2021, he said the dairy market with respect to global milk powder inventory “is in a price inflationary zone. We don’t have big inventory and we’re not setting up to build big inventories, so the risk of a good year for milk prices is still in there within this inventory cycle.”

The inventory cycle is setting up to be a price supportive one for 2021.

The trade cycle

Over the past 20 years, the world has gone through a period of booking trade agreements rapidly and aggressively. “We got new customers, grew exports, saw new opportunities and new demand,” said Gould. “The bad news is we have not booked any new WTO-style agreements in a long time.”

Gould explained that WTO-style agreements are the kind that give dairy access to new markets that grow quickly as opposed to more sales within existing markets that grow slowly.

Those WTO-style agreements of the past presented a “trade tailwind” fueling rapid market growth. “This lack of a trade tail wind is price negative for 2021,” said Gould. “The long-term view shows a lack of new global demand growth, which will hurt us.”

Gould acknowledged that the U.S. is getting a new style of trade agreement. “We have trade negotiations ongoing with several countries and we have taken existing agreements and negotiated new ones with the same customers. So, we are seeing new market access but not the advantages of WTO-style access.”

Gould sees the change from rapid growth to steady access in this trade cycle as setting up to be price negative.

Taken together, these four cycles show 2021 setting up with two neutrals, one negative and one positive.

Class III and IV expected to flip

As the indicators will be mixed, so will dairy product markets.

Gould’s cheese forecast is for an average $1.62/lb and his forecast for nonfat dry milk is that prices could reach $1.23/lb.

In farm milk checks, said Gould, it’s no simple task how milk prices get determined. “We use end products so it’s not a question of what the milk is worth, but what these products are worth, and it subtracts-out the cost of making the products and a yield factor too.”

Ostensibly, the Class II prices uses Class IV and the Class I price uses all the classes.

With Class III so much higher presently than the other classes, Gould noted the switch is setting up to flip for 2021.

Milk powder prices are expected to rise into and through 2021 because the big surpluses are gone and 2019 production kept pace with demand, which ended up drawing down on global powder supplies even further, with 2020 being more in balance heading into the first half of 2021.

While a penny change in nonfat dry milk price brings 8 cents to Class IV price a penny change in butter equates to 4 cents change in the Class IV price. Powder will be the more positive side of the 2021 setup compared with butter, according to Gould.

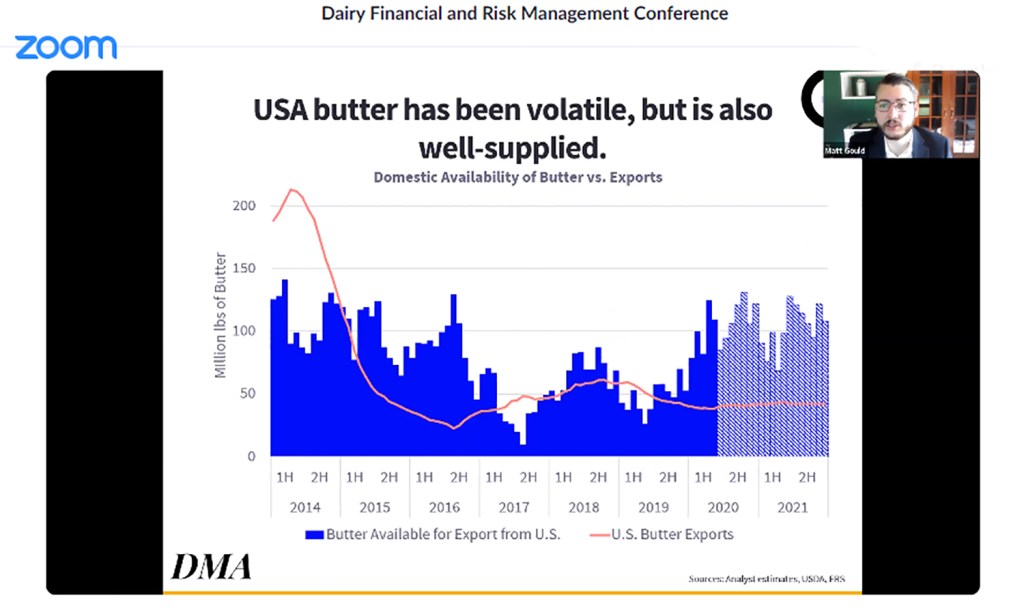

“The global butter market in 2020 saw big destruction of food service demand, which affected cheese, so processors (globally) made more butter, and foodservice is not using as much butter,” said Gould.

“In the short-term, there is an overhang of butter inventory, especially in the U.S., where we had big destruction of demand and the lowest butter price since 2013,” said Gould. “But people call me and say they can’t find butter on the shelf at the store, so how can this be?”

How can we have the lowest wholesale butter price and not be keeping up with retail demand?”

Gould explains that 55% of U.S. butter consumption pre-Covid was foodservice – going out to eat. In this pandemic environment, the foodservice industry has been devastated. Open Table, a company that books restaurant reservations estimates foodservice is still down by half and full-service restaurants are decimated.

“On the flipside, retail butter sales have been extraordinary at times, with some weeks more than doubled over year ago,” said Gould. But plants in the U.S. are specialized moreso than in Europe where dairy plants are more flexible making more different products instead of specialized for high volume and efficiency.

“Where we have the bottleneck in the U.S. is turning bulk butter into quarter pound sticks for retail,” he said, adding that in the past21 days, retail butter sales have slowed to show smaller growth rates over year ago.

In short, while holiday sales will help boost fourth quarter, it won’t make much difference in the overall butter picture because “we’ve already gone through the demand destruction and the inventory is already built. We have more butter in stock than we have domestic sales so we are in surplus,” said Gould.

Gould did not specifically mention the large imports of butter and butterfat into the U.S. from March through July, but he did reference the bottleneck in turning enough bulk butter into sticks for retail. As this pushed retail butter prices higher, Gould noted that importing was incentivized.

Cheese is where some “known surprises” come into play.

The U.S. will see significant new cheese production capacity becoming operational in November (Michigan) and the beginning of 2021 (Minnesota).

“Every one penny in cheese price change is 10 cents of change on the milk check,” Gould pointed out. “As a globe, we are in relatively balanced to tight supply on cheese in the second half of 2020, but the forecast heading into 2021 is driven by the factories and capacity being built.”

He said the long-term export trend for cheese is positive. It has been a “winner” during Covid because the big cheese purveyors are pizza companies that were the first to adopt low and no-contact delivery and saw their sales surge 20% higher.

But new cheese processing capacity in the U.S. and in Europe will present short-term concerns.

“We will see huge growth in cheese processing,” said Gould. The plant in St. John’s Michigan as a joint venture of DFA, Select and Glanbia will be the sixth largest in the country.

“We have never opened a plant in the U.S. that big – that fast – in history. This is a first, and these types of plants have to be run full, or you will lose your tail,” he said, noting these types of plants in the American cheese business operate on margins of 0.5% (one half of one percent). “They’ll make a penny on a $2/lb cheddar price. That’s why they fill full and build to scale and magnitude to make volume.

“The consequence of that is a shock increase in supply,” said Gould. “Demand doesn’t grow that same way. We don’t wake up and see new demand present itself as a shock-increase like that.”

Some wild cards do exist, including government intervention. What we’ve seen already this year in dairy purchases is greater than dairy has seen in a long time.

“Government purchases (CFAP) are using 2.5 to 3% of the U.S. milk supply,” said Gould. “Normally we forecast within 1% to say a year will be good or bad, but when those purchases end, we are talking about 2.5 to 3%. That’s a huge number. That’s a price negative thing if all of a sudden there’s 2% more milk on the market without government purchases.”

The flip side, he said, is “We are going through a crisis, and people are hungry. When you have hungry people, the prescription is to get them food.”

In this way, government purchase could be a positive wild card if they continue under circumstances where economic slowdown impacts domestic demand.

Other wild cards of course include the progress on a vaccine for Covid, and the status of the economy and foodservice. Positives in those areas could unleash demand for products that can be made quickly in bulk without the bottlenecks of serving retail demand.

— Previously published in Farmshine, Sept. 25, 2020

-30-

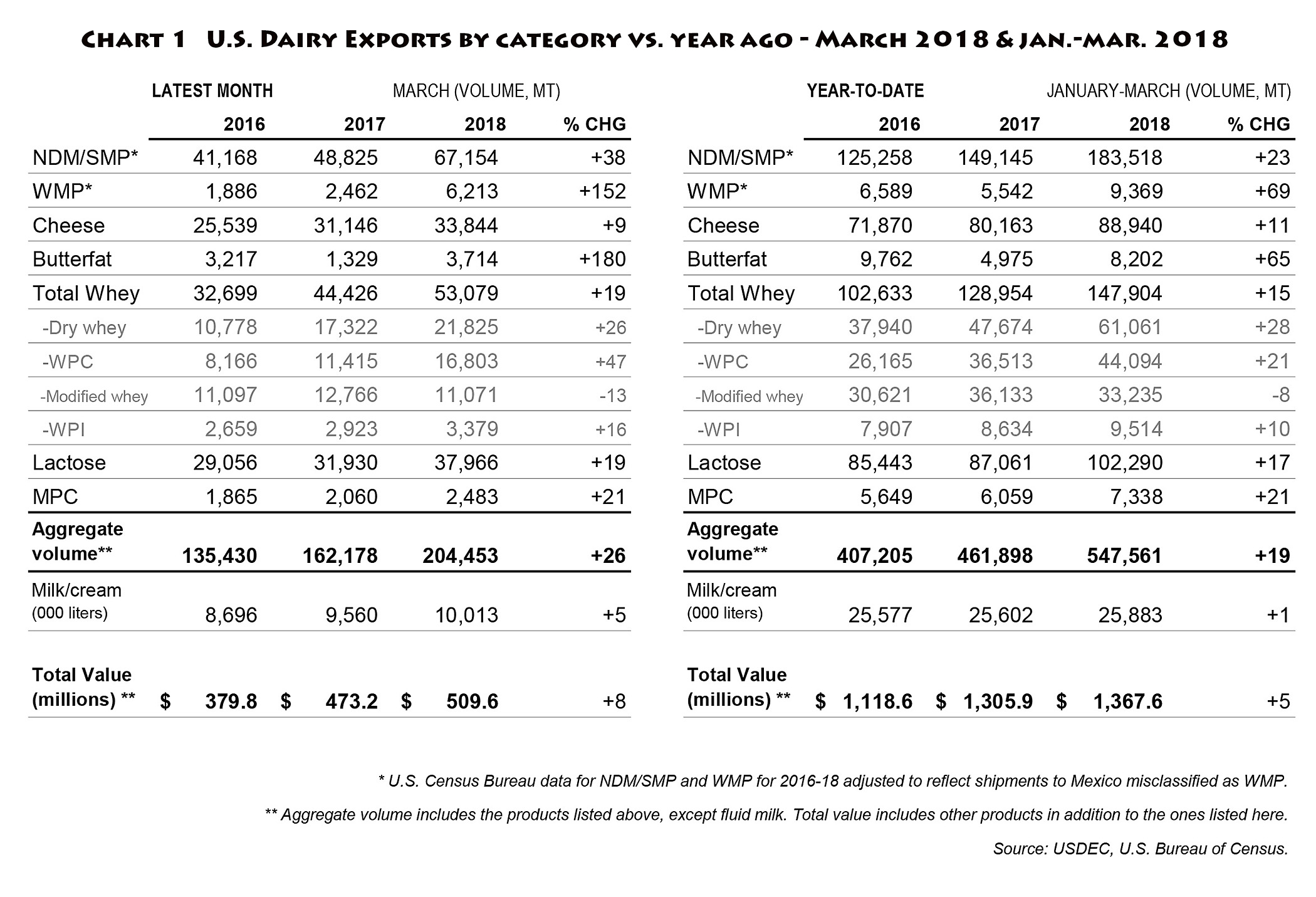

By Sherry Bunting, originally published in Farmshine, June 7, 2018 and examines the utilization of domestic Class I fluid milk vs. exported commodities during the worst three months of pricing at the beginning of 2018, but the trends show how FMMO pricing no longer provides the value to farmers for their milk as exports increase. Read Global Thoughts

By Sherry Bunting, originally published in Farmshine, June 7, 2018 and examines the utilization of domestic Class I fluid milk vs. exported commodities during the worst three months of pricing at the beginning of 2018, but the trends show how FMMO pricing no longer provides the value to farmers for their milk as exports increase. Read Global Thoughts  The total “official” U.S. Class I utilization for 2017 was 26.1%, down nearly 10% from 35.9% in 2009, according to USDA figures.

The total “official” U.S. Class I utilization for 2017 was 26.1%, down nearly 10% from 35.9% in 2009, according to USDA figures. By Sherry Bunting, Farmshine, June 1, 2018

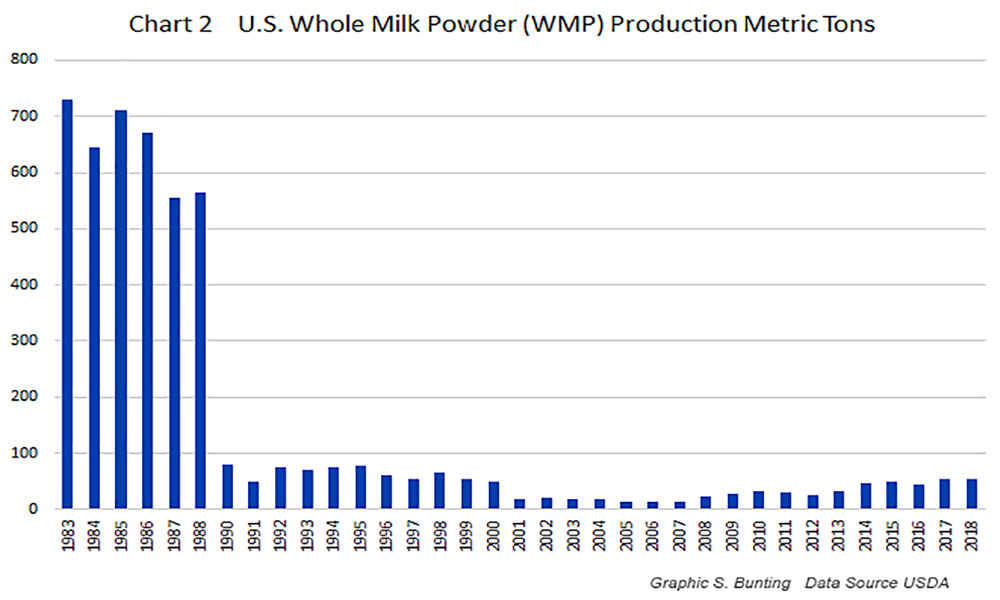

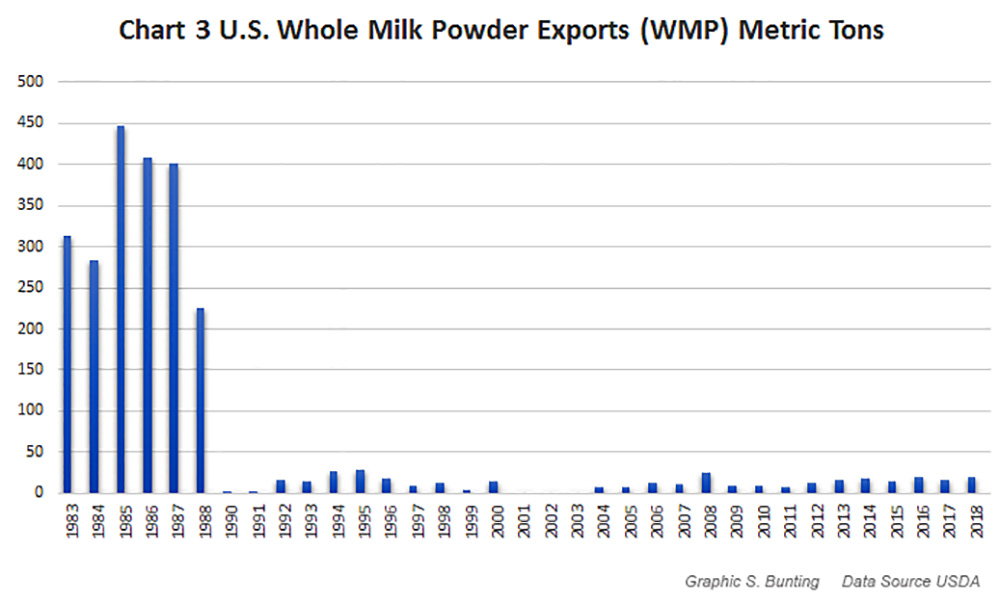

By Sherry Bunting, Farmshine, June 1, 2018 In fact, going back through USDA records to 1983, the U.S. once made up to 700 metric tons of dry whole milk powder (Chart 2). We don’t hear about that.

In fact, going back through USDA records to 1983, the U.S. once made up to 700 metric tons of dry whole milk powder (Chart 2). We don’t hear about that. One reason we don’t make more WMP today is we have a large and growing domestic market for cheese and butter and cream products. U.S. manufacturers want to keep the cream and not sell it overseas, whereas other dairy-producing nations — like New Zealand with its much smaller consumer population — make a lot of WMP for Asia.

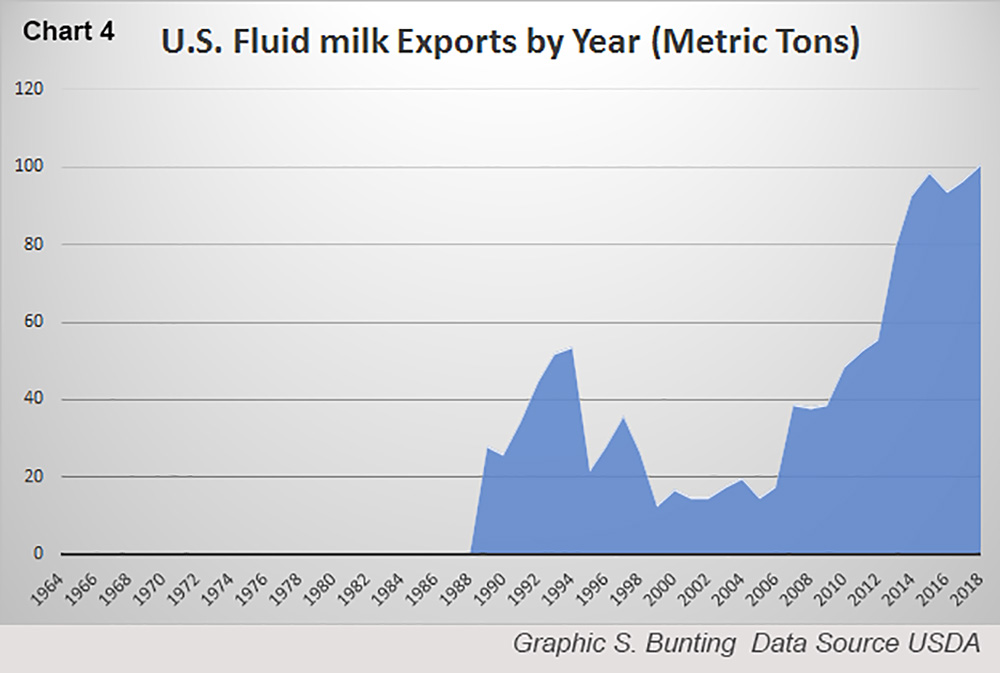

One reason we don’t make more WMP today is we have a large and growing domestic market for cheese and butter and cream products. U.S. manufacturers want to keep the cream and not sell it overseas, whereas other dairy-producing nations — like New Zealand with its much smaller consumer population — make a lot of WMP for Asia. One lesser-known category of exports that grew by 85% in the first three months of 2018 is UHT shelf-stable milk. China is the biggest buyer, and DFA is a primary supplier with its California Gold, a primarily 3.5% fat, shelf-stable drinking milk with a non-refrigerated shelf life of one year. This product is shipped to Walmart and other chains in China. These sales have grown significantly since 2006. (Chart 4)

One lesser-known category of exports that grew by 85% in the first three months of 2018 is UHT shelf-stable milk. China is the biggest buyer, and DFA is a primary supplier with its California Gold, a primarily 3.5% fat, shelf-stable drinking milk with a non-refrigerated shelf life of one year. This product is shipped to Walmart and other chains in China. These sales have grown significantly since 2006. (Chart 4) By Sherry Bunting, from Farmshine May 4, 2018

By Sherry Bunting, from Farmshine May 4, 2018