Part One of Six-part “Global Dairy Thoughts” Series in Farmshine

By Sherry Bunting, from Farmshine, April 27, 2018

BROWNSTOWN, Pa. — Even though U.S. per-capita milk consumption is in decline, consumption of other dairy products is strong. As the industry devotes resources to new milk markets abroad and puts the fluid milk market here at home on commodity autopilot: Who’s minding the store?

While it is true that the U.S. dairy market is ‘mature’ — not offering the growth-curve found in emerging export markets — the U.S. consumer market is still considered the largest, most well-established and coveted destination for dairy products and ingredients in the world.

As U.S. milk production continues to increase despite entering a fourth straight year of low prices and market losses, industry leaders look to exports for new demand that can match the trajectory of new milk.

The U.S. has already joined the ranks of major dairy exporting nations, and the U.S. Dairy Export Council (USDEC) has set a goal to increase exports from the current 15% (milk equiv) to 20%. Keep in mind that as our percentage of exports increases while our milk production also increases, the volume of export markets required to meet this goal is compounded.

On one path at this fork in the road is the mature domestic market with its sagging fluid milk sector that is increasingly filled in deficit regions by transportation of milk from rapidly growing surplus regions.

This dilemma of getting milk that is increasingly produced away from consumers packaged and moved toward consumers was cited as a “tricky challenge” by Dr. Mark Stephenson, Director of Dairy Markets and Policy at the University of Wisconsin-Madison, in his presentation on Changing Dairy Landscapes: Regional Perspectives at the Heartland Dairy Expo in Springfield, Missouri earlier this year. In this presentation, Stephenson pegged the Northeast milk deficit at 8 bil lbs and the Southeast deficit at 41 bil lbs. (More on this in a future part of this series).

On the other path at this fork in the road is the industry’s desire to expand exports within a global market that needs a 1.5% year-over-year global production increase. But, as the USDEC reported in its February global dairy outlook, global milk output is growing by twice that rate, mainly from gains in Europe.

Meanwhile, U.S. regulatory pricing structures are based on milk utilization. As the total dairy processing pie grows larger, the neglected fluid milk sector becomes a shrinking piece of the expanding pie, and income is further diminished for dairy farms.

The emerging export markets are rooted in the demographic of rising middle-class populations improving diets with dairy. And yet, just because these new markets offer new growth curves for new milk production, the anchor for this ship is still the U.S. market, still No. 1 as the largest dairy consumer sector globally, and still moving milk via Federal Order pricing that hinges on that shrinking piece of the expanding pie: Class I.

What are the obstacles to improving this sagging fluid milk sector? How are regulated promotion and pricing constraining restoration of declining fluid milk sales?

Over the past three years, two prominent and longstanding milk bottlers in the New York / New Jersey metropolis have either closed their plants (Elmhurst in New York City), or sold their dairy assets (Cumberland Dairy in New Jersey sold to DFA). Amazingly, the former owners of both plants are expanding into the alternative beverage space — adding new plant-based beverages to the proliferation of fraudulent ‘milks’ that already litter the supermarket dairy case.

While dairy milk sales decline, plant-based beverages are a growth market, though the pace of growth has slowed.

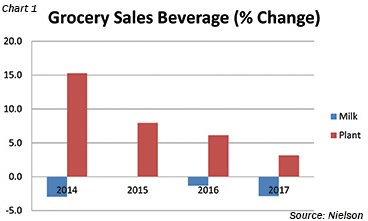

At the Georgia Dairy Conference in January, Rob Fox, Dairy Sector Manager of Wells Fargo’s Food and Agribusiness Industry Advisors, talked about big picturedairy trends, and he showed graphically the way these alternatives are eating into the U.S. dairy milk market. While dairy milk sales decline, the plant-based beverages are a growth market, though the pace of growth has slowed. (See Chart 1)

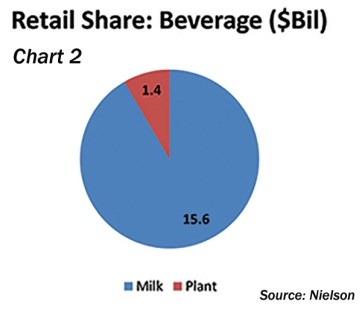

Fox also showed a pie chart of combined supermarket sales of dairy and plant beverages at $17 bil., with dairy accounting for $15.6 bil. and plant-based at $1.4 bil. (Chart 2).

Rob Fox showed a pie chart of combined supermarket sales of dairy and plant beverages at $17 bil with dairy accounting for $15.6 bil. and plant-based at $1.4 bil.

Doing the math, Fox remarked that the plant-based alternatives now represent 8.9% of the combined dairy and plant-based ‘milk’ market. He said that in other countries with mature dairy markets, these alternative beverages tended to level off in growth when reaching 10% of total dairy market share. But at the same time, the combined dairy and plant beverage sector has also declined from 6.4 billion units in 2013 to 6.1 in 2017, according to Fox.

He noted the alternatives are also infiltrating other dairy product categories and that these ‘next generation’ products are offering much better nutrition than earlier versions. “But they will never compete with dairy milk, nutritionally,” Fox said.

What these alternative beverages have going for them, said Fox, is very high margins for processors and investors.

He explained that plant-based dairy products have low ingredient costs, are easier to manufacture, package, market and distribute and are seen as ‘greener’ and animal friendly. They are better positioned for e-commerce and kiosk-type retail outlets and are made by innovative marketing companies and startups with a market and margin profile that attracts investors.

Meanwhile, dairy milk is a highly regulated market with a prevailing commodity mindset worn down even more-so by supermarket price wars at the retail level, making it difficult for the dairy milk sector to adapt to U.S. consumer market trends.

U.S. consumer trends gravitate toward innovation and specialization so everyone can be a ‘snowflake,’” Fox explained, adding that areas of growth for the dairy milk sector will be full-fat in smaller containers, dairy protein in sports nutrition, and non-GMO branding. (No joke: Look for more later on genetically-modified, aka GMO, lab-manufactured products like Perfect Day that are actively defending what they see as their right to use the term ‘animal-free dairy’ because their product is said to be compositionally the same as milk, derived from genetically modified laboratory yeast exuding a white substance they say IS milk.)

That said, where is the true and simply original dairy in its re-branding process? What efforts are being made to compete to reverse this fluid milk market decline? Wouldn’t revitalization of the fluid milk sector also provide a demand pull for U.S. production growth?

Fresh fluid milk is not interchangeable on the global stage as are milk powders, fat powders, protein powders, cheeses, butter and aseptically packaged shelf-stable fluid products.

Meanwhile, the fastest growing surplus regions of the U.S. are busy aligning with retailer/processors and utilizing the Federal Order pricing schemes to pull their production growth into milk-deficit regions, leaving the milk-deficit region’s producers sending their milk to manufacturing homes in other Orders, or even looking for ways to export from eastern ports.

The U.S. has the water, the feed, the space, the transportation, logistics and support infrastructure, as well as a large existing domestic market to anchor the base production level of our nation’s farmers. The U.S. also has a legacy of dairy producers that are respected for their progress, animal care and food safety.

The ingredients for global success are here, but other factors need evaluation because the success is eluding dairy farm families as they face their fourth year of low prices and lost markets forcing increased numbers to exit the business.

In future installments of this multi-part series “Global Thoughts,” we’ll look more closely at the export side of this fork in the road, including the product trends, product and trading platform differences, imports, transportation and logistics, the role of regulatory pricing and cooperative base programs at a time when the dairy landscape is being forever changed.

As this series proceeds, thoughts and questions are welcome: agrite2011@gmail.com

-30-

Pingback: Global dairy thoughts Part II: Who’s being creative? | Ag Moos

Pingback: Global thoughts Part 4: As exports grow, who benefits from ‘new math’? | Ag Moos "Growing the Land"

Pingback: Global dairy thoughts Part 5: First half 2018 butter, milk, cream imports climb! | Ag Moos "Growing the Land"

Pingback: ‘Carbon-negative milk?’ Northeast, Southeast milksheds can already claim it | Ag Moos