By Sherry Bunting, Farmshine, Sept. 24, 2021

HARRISBURG, Pa. – ‘Turning the page’ was the theme for the annual Financial and Risk Management Conference where key takeaways about a changing dairy industry were presented.

The conference was hosted by the Center for Dairy Excellence Sept. 21 in Harrisburg.

Pennsylvania Secretary of Agriculture Russell Redding summarized his own thoughts: “I am still very positive about dairy, but dairy will change. It is changing,” he said.

The Center’s risk management educator Zach Myers set the stage for attending lenders, vendors, producers and industry talking about Dairy Margin Coverage and Dairy Revenue Protection and how these programs have worked (more on that in a separate article.)

Digging into the stress — the ‘change’ — was Marin Bozic, University of Minnesota associate professor of applied economics and dairy foods marketing, who also serves as facilitator for the Midwest Dairy Growth Alliance. He dug right into how and why, discussing some of the Federal Milk Marketing Order complexities, industry trends and pricing relationships. He made the case that more flexibility, competition and innovation are needed in the Federal Orders for a “level playing field” so winners and losers can “self-select.”

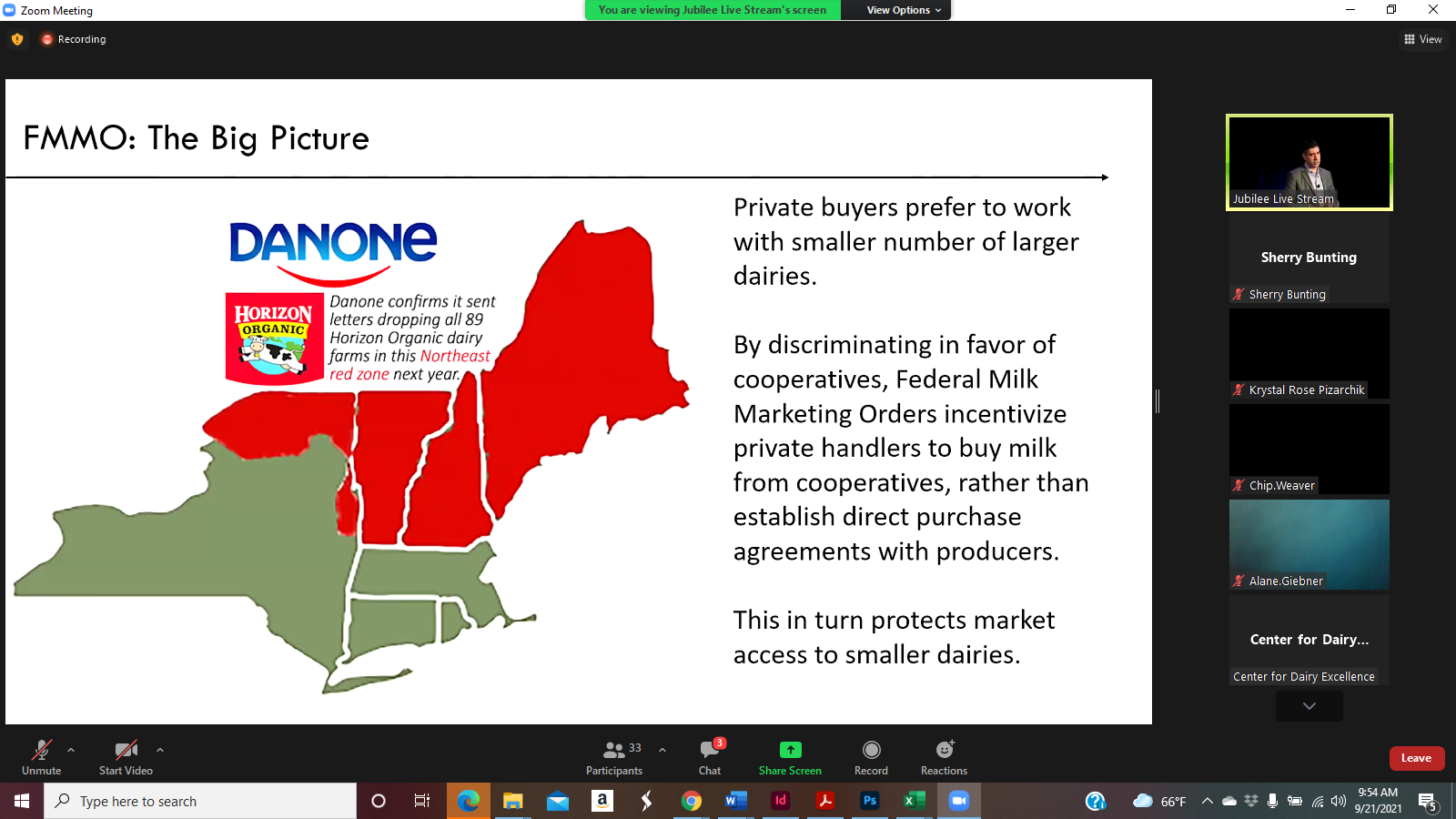

Bringing up the 89 organic producers Danone will drop from Horizon next year, Bozic said it is an example that, “One new farm in Indiana replaced 89 or 90 farms in the Northeast, and they can do that. There is nothing illegal about it. They could say they have a fiduciary responsibility to stakeholders and are minding their bottom line, but none of that helps you if 90 producers get dumped in a year.”

He pointed out the “social mission” of the cooperatives is to leave no member behind, so remaining an independent producer carries more risk today than in the past.

Bozic connected the dots to say the “primary function of the future for Federal Milk Marketing Orders — as an extension of the milk cooperatives — is to ensure market access for dairy producers.

“Market orders are there to ensure orderly consolidation at a humane pace,” he declared.

That’s a change from the central promise of the FMMOs today, which Bozic described earlier as “broken.”

“To navigate our businesses over the next year and longer,” said Bozic, “we have to count the passes and see the gorilla” — a nod to the visual exercise he had the audience participate in.

Bozic mentioned a few gorillas in milk. Gorillas in the FMMOs, in risk management, in dairy markets and in the macroeconomic situation – what else is going on in the world.

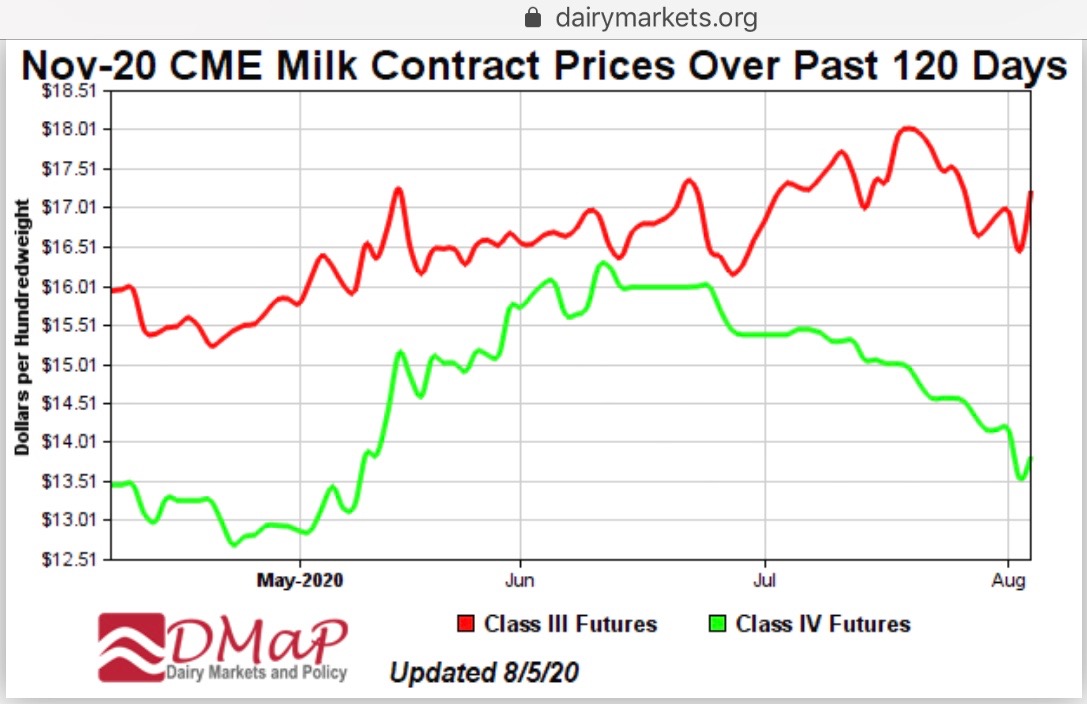

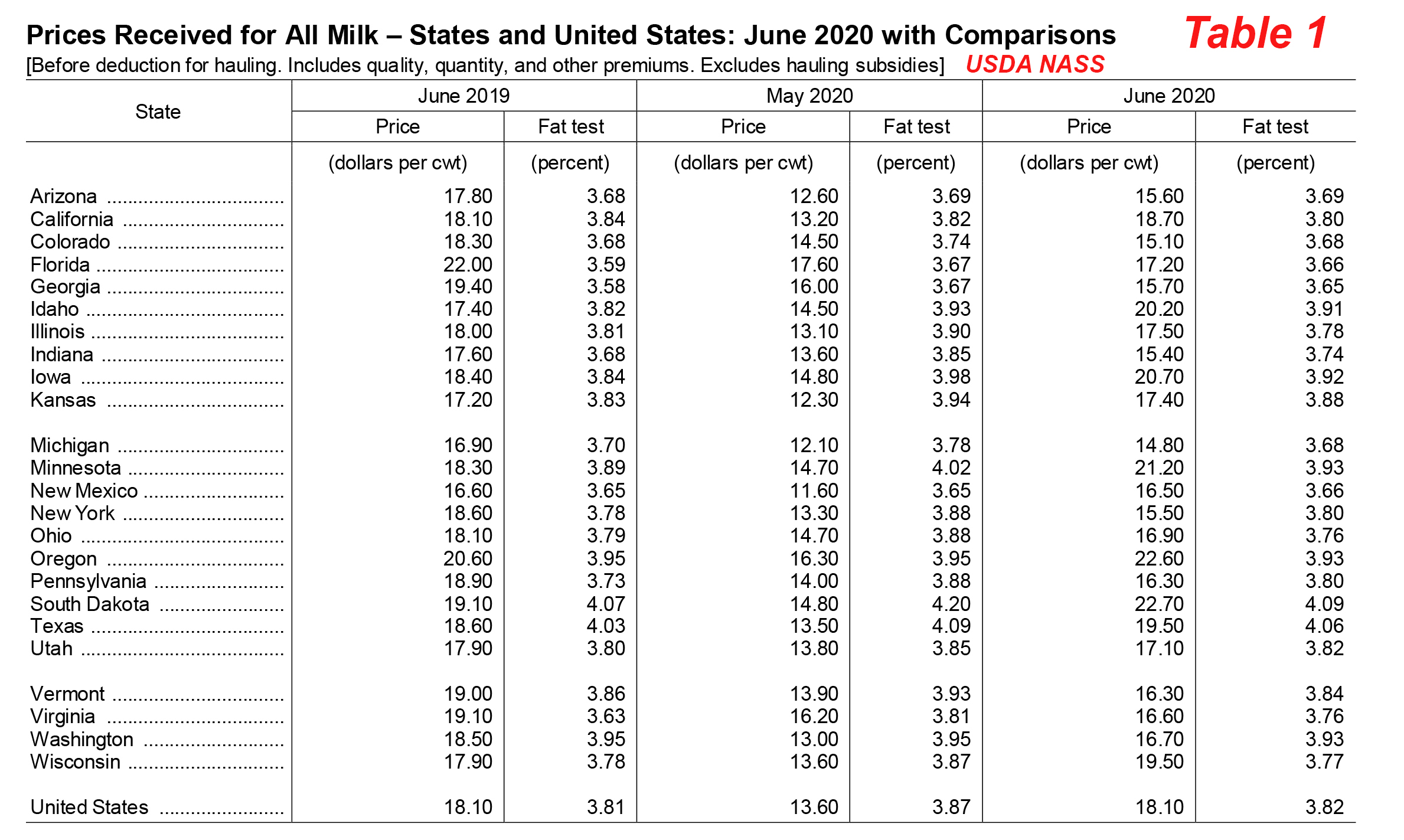

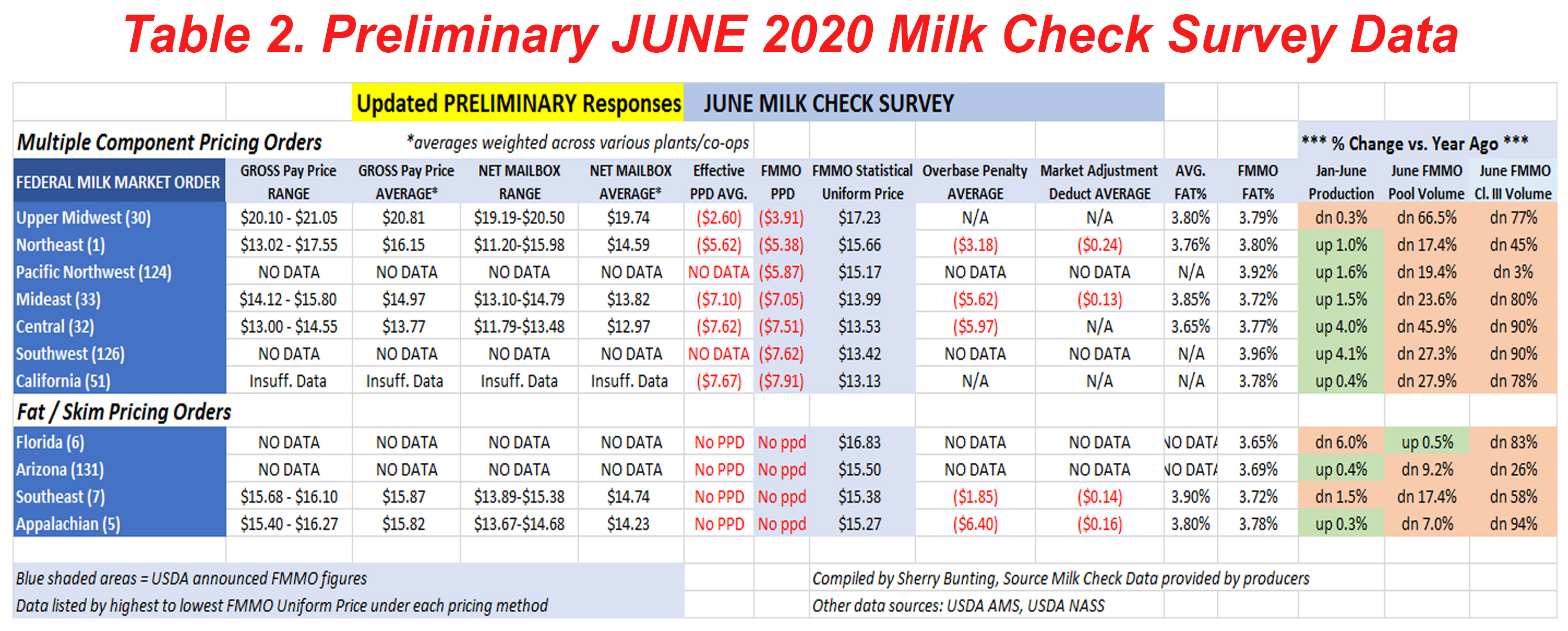

He showed graphs of what Producer Price Differentials (PPDs) looked like for the Northeast in 2020, the $4 and $5 negatives that represented cash flow bleeding, equity bleeding.

While the futures show the view out to the horizon over the next 6, 12, 15 months that would suggest there won’t be a repeat of that carnage, Bozic cited some of these risks, or gorillas, in the market and in world events that could represent shocks that can make the whole thing “go haywire again.”

Observing that the FMMOs are not the same today as when they were designed many decades ago, Bozic stepped conference attendees through the various long- and short-term impacts that reduce PPD, such as declining Class I utilization compared with increasing Class IV utilization and production.

“Orders were designed around the assumption that there would be plenty of fluid milk usage (as a percentage of total production), and we can just take it and designate it to be the highest and use those funds to make everyone whole,” said Bozic.

“The central promise of the FMMOs is that if your milk is as good as your neighbor’s, you get paid the same, so one farmer does not bid against another for market access and a good price,” he asserted. “That promise is now getting broken, not as much here, the East Coast FMMOs still have Class I.”

The next effect in the Northeast is the rise of protein tests. This impact comes through two channels where higher protein reduces PPD, the economist explained.

“Envision FMMOs as all processors paying into the pool and then taking from the pool. First they pay to the pool with classified pricing based on their respective milk solids. Class I pays on pounds of skim milk as volume, not on protein pounds,” he explained. “Even if sales are the same and the only thing that changes is protein, those (Class I) processors would pay the same amount (on skim) into the pool and take more money out (on protein) so there is less money remaining and a lower PPD.”

The second way higher protein production affects PPD is when the value of protein is lower in the powder than it is in the cheese. The butter/powder plant pays to the pool on nonfat solids price but takes money from the pool on protein price, “so that spread between the value of protein in cheese and powder also leaves less money for PPD,” said Bozic.

He explained the Class III price as an index of butterfat, protein and solids, in a straight formula that equals the class price. “When Class III price is higher than Class IV price, the predicted PPD for the Northeast Order declines,” said Bozic. “It’s almost linear.”

Conversely, when IV is above III, PPD goes up. “This has to do with paying the pool based on protein and nonfat solids, but when handlers take money out of the pool for components, everyone takes protein price leaving less money in the pool for PPD.

Bozic explained the demand shock to this system when the Food Box program “focused on smaller packages of cheese to put in every box. They didn’t take bulk powder and butter. So we went from a record low cheese price on the CME to a record high and no one expected this.”

The pull of 5% of the cheese supply for immediate delivery had everyone scrambling, said Bozic.

The amount of spare cheese available was not as high a volume as the government wanted to buy so cheese went from being long to short, and the price skyrocketed. This translated to an historically higher gap between Class III and IV prices as wide as $10 apart.

So why not just send more milk to make cheese? Bozic maintains that Class IV processing is accustomed to “balancing” fluid milk seasonality so there is extra capacity in that system.

Not so with Class III because those plants already run at capacity. “That’s the only way processors of commodity cheese make margin is to run at capacity, so when the demand shock came, and spare product was used up, there was no spare capacity and the price went higher. That was the main driver of negative PPD in 2020,” said Bozic.

Will it happen again? Bozic doesn’t foresee Food box programs with the same intensity in the future, but, “yes, it can happen, but I would say you need to have a pandemic in an election year. Don’t count on a program like this.”

The industry did ask USDA back in the 2008-09 recession to buy consumer packaged cheese instead of bulk commodities, so it could move instead of being stored to overhang the market later. That wasn’t working either.

“Now we understand that this other method disturbs PPDs so the dairy industry is united behind a more balanced approach,” said Bozic, describing the next iteration of purchases through the Dairy Donation Program will not be as aggressive in moving the markets by three orders of magnitude.”

Bozic said quick rallies and crashes impact PPDs also because of advance pricing on Class I based on the first two weeks of the prior month and announced pricing for the other classes at the end of the month.

Bozic explained why the change in Class I pricing was made: “The dairy industry wants to attract new distributors like Starbucks and McDonalds that are used to hedging their input costs. They don’t want to change prices every month. They want it to be what it is for a year, so the industry wants stable, predictable milk price costs to win favor with new distribution channels by making it easier for them to hedge.”

He said the new average plus 74 cents was designed to be revenue neutral. Looking forward, when Classes III and IV have less than $1.48/cwt spread, PPD under the new system is higher than under the old. But the most it can be higher is by 74 cents on Class I, which translates to 20 cents on the blend price.

“The best case scenario is to add 20 cents to the blend price, but when Classes III and IV are far apart “the PPD can go haywire. Bottom line, the upside benefit of the averaging method with 74-cent adjuster is limited but the downside risk is big,” said Bozic.