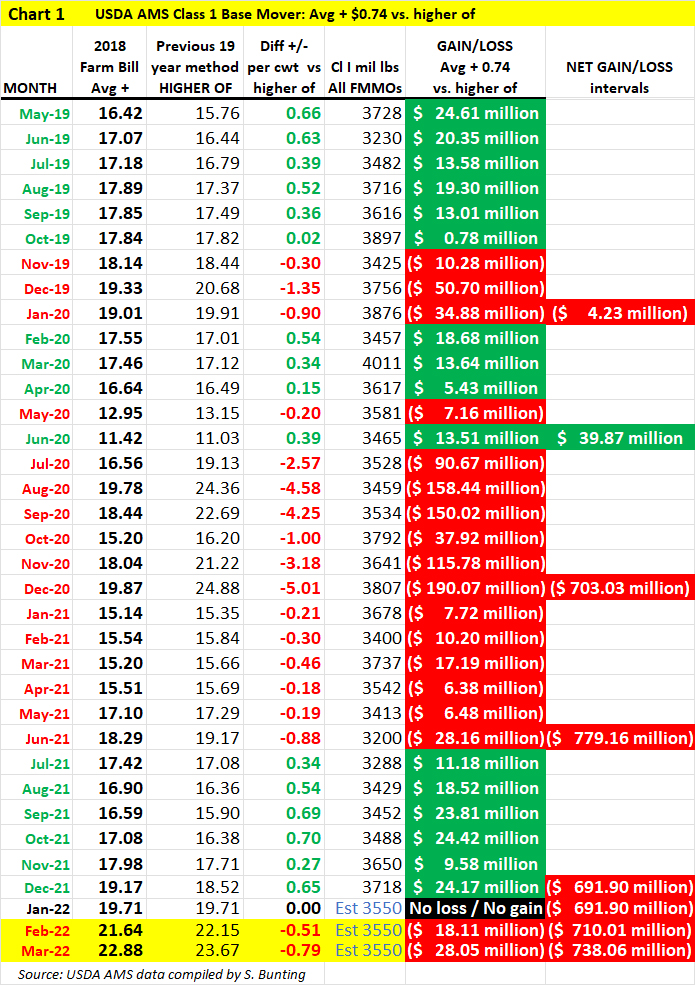

Milk Market Moos, by Sherry Bunting, is a weekly feature in Farmshine. Portions are republished below with the prices updated to Fri., Feb. 25 after the print edition went to press Wed. evening, Feb. 23.

Milk production in all U.S. states collectively during January fell by 1.6% vs. year ago. In the 24 major reporting states, the decline was 1.4%. December’s production was also revised lower than the estimate last month.

January’s production decline came from a combination of reduced output per cow and 63,000 fewer cows compared with a year ago. Cow numbers in January are 5000 fewer than December.

This trend could go on for some time, as we noted recently in this column, that the Jan. 1 semi-annual All Cattle and Calf Inventory Report recently showed a 1% decline in milk cow numbers compared with Jan. 1 2021 and a whopping 3% decline in replacement dairy heifer numbers vs. year ago.

The 2021 production total for the U.S. was also released in the Feb. 23 USDA Milk Production Report showing last year’s U.S. milk production total was 1.3% above 2020.

At the same time, the average number of licensed herds in the U.S. during 2021 (not an end-of-year number) was reported at 29,858 — down 1,794 compared with the average number of licensed herds in 2020 and the first time the number fell below 30,000. This is a 5.7% decline in the average number of licensed dairy herds nationwide. In 2020, there was a 7.5% decline as the nation lost 2550 dairy herds that year.

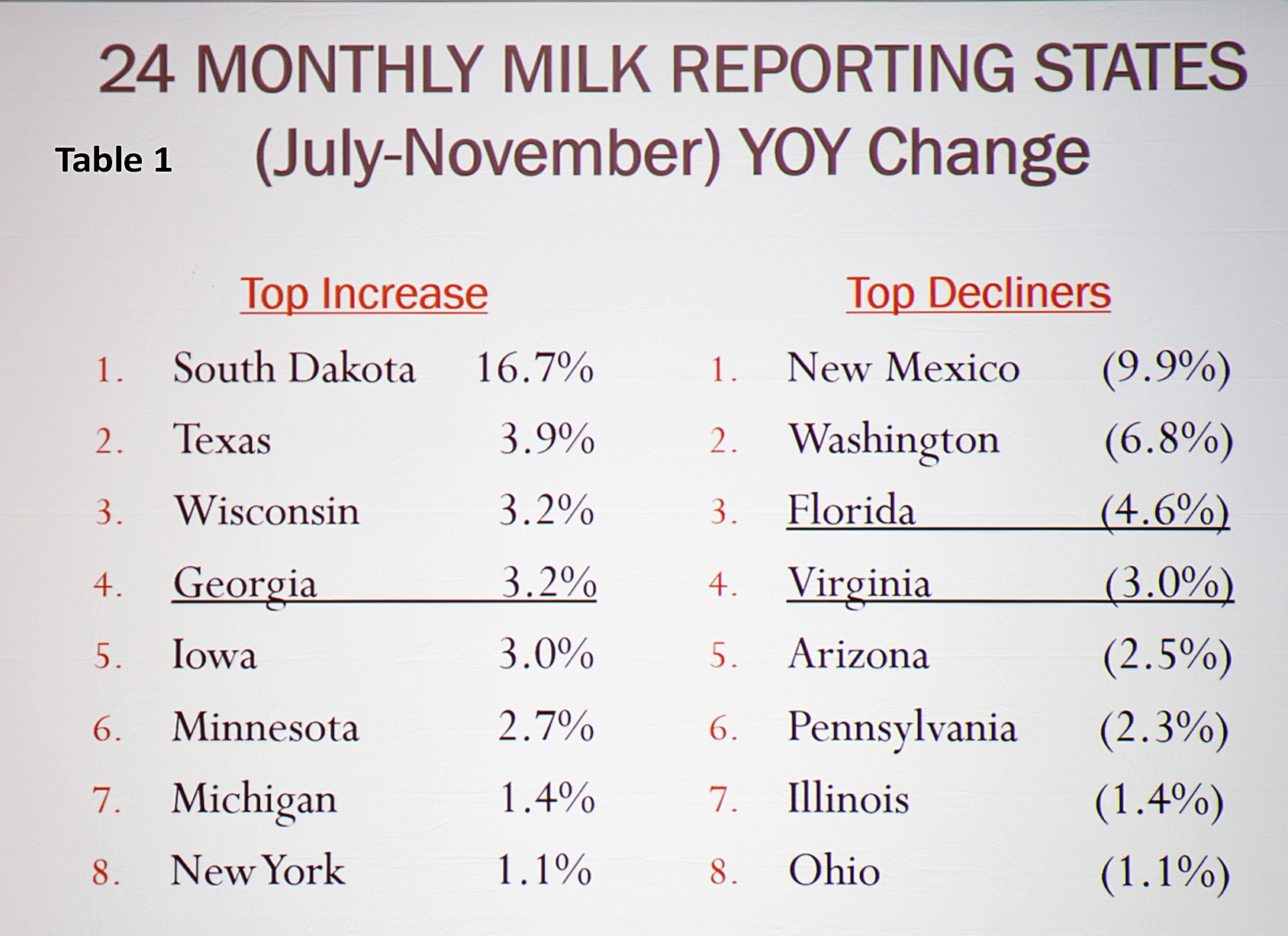

In the Northeast and Midatlantic milkshed, among the major reporting states, Pennsylvania’s production was 2.9% below year ago in January with 6000 fewer milk cows on farms; 2021 production in the Keystone state was 1.6% below 2020 and the average number of cows on PA farms last year was 8000 fewer than in 2020.

January’s production in New York was down 0.6% with 5000 fewer cows; 2021 production in the Empire State was up 1.6% with the average number of cows on NY farms in 2021 numbering 1000 more than in 2020.

Vermont’s cow numbers fell by 1000 head in January 2022 vs. Jan. 2021 and milk production was off by 1.8%; 2021 production in the Green Mountain State was down 1.4% vs. 2020 with 2000 fewer cows as an average for the year.

The average number of licensed herds in Pennsylvania in 2021 was 5200, down 230 from 2020 (4.3% drop); New York 3430, down 220 (6% drop); and Vermont 580, down 60 (a 9.4% drop); Virginia 421, down 54 (11% drop).

In the Southeast milkshed among major milk producing states, Florida’s average number of herds was 75 in 2021, down 10 from 2020 (11.8% drop); Georgia 110, down 20 (15.4% drop). Production and cow numbers were mixed with Georgia growing output by 1.4% in 2021 vs. 2020 with 1000 additional cows; Florida’s production declined 5.1% with 5000 fewer cows, and Virginia’s production was down 3.4% with 2000 fewer cows.

Georgia’s production last month was up a whopping 5.1% as one of only 5 states to show a year over year production increase in January 2022 with 3000 more cows than a year ago even though the number of farms fell by over 15%.

By contrast, January’s production totals in Florida and Virginia were down 3.5% and 3.8% with 4000 and 3000 fewer milk cows, respectively.

Four other states gained production in January vs. year ago, (in addition to Georgia). They were: Iowa, up 1.7% with 3000 more cows vs. year ago; Idaho up 0.6% with 4000 more cows, Texas up 3.5% with 12,000 more cows, and South Dakota up a whopping 18.3% with 28,000 more cows.

The two largest milk production states saw a pullback in January: Wisconsin’s production was off fractionally while California, the largest producing state, saw a 1.9% decline in year over year production in January.

New Mexico’s trend deepened. 2021 production was 4.5% lower than 2020 with 12,000 fewer cows. In January 2022, production was below previous year by 12.1% with 42,000 fewer milk cows. New Mexico’s average number of licensed herds in 2021 came in at 120, down 20 (down 14.3%).

Texas also saw 20 fewer licensed herds last year, at 340 (down 5.6%). However cow numbers grew 27,000 in in the Lone Star State during 2021 with production beating 2020 by 5%.

Texas officially surpassed New York as the 4th largest milk producing state with 15.6 billion pounds of milk vs. New York’s 15.5 billion pounds in 2021. The January 2022 figures show 12,000 more cows and 3.5% more production vs. year ago in Texas.

South Dakota lost 15 herds at an average 165 for 2021 (down 8.4%). However, South Dakota gained 21,000 cows and 15.5% in milk production for 2021 vs. 2020. Neighboring Minnesota, the 7th largest milk producing state gained 13,000 cows and 3.7% in production in 2021 at 10.5 billion pounds — putting more daylight ahead of Pennsylvania, the 8th highest producing state at 10.1 billion pounds in 2021.

Look for more analysis of the yearend report in the next print edition of Farmshine and here at agmoos this week.

Cl. III and IV milk futures mixed,12-mo. Cl. III avg. $21.51, IV $23.25

Class III and IV milk futures were mixed when Farmshine went to press at midweek, Feb. 23 — before global reports showed a shrinking milk supply and before the Russian invasion of Ukraine commenced. Figures in the Farmshine print edition of Milk Market Moos have been updated using milk futures quotes at the close of Friday, Feb. 25 trade below.

Class IV split the trend with first half 2022 steady to lower, second half firm to higher, while Class III was mostly higher, except March and April contracts under downward pressure. In the Class III trading, new contract highs were set for August through December 2022.

The bullish USDA milk production report came out at the close of CME trade on Feb. 23 — prompting after hours trade to tick higher Feb. through Aug. by 25 to 65 cents on Class III, strengthening further at the end of the week on news of global supply deficits tempered by the uncertain impacts of war in Eastern Europe.

Class III milk futures recouped twice as much as was lost last week, averaging $21.63 for the next 12 months on the close of trade Wed., Feb. 25. This is 29 cents higher than the average a week ago,

Class IV futures averaged $23.46 for the next 12 months, generally steady at midweek compared with the previous week’s average, but gaining 22 cents Thursday and Friday on the average.

The average spread between the Class III and IV milk futures contracts for the next 12 months Feb. 2022 through Jan. 2023 stood at $1.83/cwt on Feb. 25 — 10 cents narrower than a week ago with Feb. through August contracts $1.80 to $2 apart and narrowing to right around the $1.48 threshold by September.

CME spot dairy commodities lose ground

CME spot dairy prices moved higher on Class III products (cheese and whey) before turning lower at the end of the week. For Class IV products (butter/NFDM) the trend started lower and continued lower through week’s end.

By Fri., Feb. 25, butter lost two-thirds of last week’s huge gain, pegged at $2.5785/lb with 2 loads trading. This was 20 cents lower than the previous Wednesday, with 8 cents of the loss occurring in a single session Friday.

Grade A nonfat dry milk (NFDM) lost 5 pennies this week then gained one back on Wed., Feb. 23 when the spot price was pegged at $1.86/lb — down 4 cents from a week ago with 12 loads trading. Thursday’s trade saw a penny and a half increase, which was lost Friday, to end the week at $1.86/lb.

On the Class III side of the ledger Wed., Feb. 23, 40-lb Cheddar blocks were firm at $1.99/lb, gained 3 cents Thursday, but lost 7 cents Friday, Feb. 25, when 40-lb blocks were pegged at $1.9450/lb, down 4 1/2 cents from a week ago with a single load changing hands; 500-lb barrels at $1.90/lb were 1 1/2 cents lower than a week ago with 2 loads trading Friday.

The spot market for dry whey gained a penny, at 81-cents on Wed., Feb. 23, with no loads trading, but then lost 3 cents in end of week trading, pegged Fri., Feb. 25 at 78 cents, no loads traded.

Grain market rallied

Corn rallied 10 to mostly 30 cents per bushel higher last Wed., Feb. 23 on the eve of the Russian invasion of Ukraine, most strength near term; soybean meal $10 to $30/ton higher with far off contracts $5 to $10/T higher than a week ago. Those levels followed wheat higher on the news in the wee hours of Thursday morning of the Russian invasion of Ukraine, a global exporter of wheat, corn and other grains and oilseeds, number one crop being sunflowers.

By Friday, Feb. 25, the run-up had tamped down, but with near-term contracts still much higher than a week ago — May corn closed at $6.55 down from highs over $7 the previous day; May soybean meal closed at $442.70 Friday.

Auction prices for market cows, calves, dairy fats backoff a bit after big gains two weeks ago

Market cows, fat dairy steers, and return to farm Holstein bull calves, especially beef crosses, jumped significantly higher two weeks ago and edged off a bit in the Feb. 17 to 22 auction market trade in Lancaster County. Choice and Prime Dairy steers averaged $115.00, Breaking Utility cows $81.10, Boning Utility $74.50, Lean cows $65.75. Holstein bulls 90 to 125 lbs averaged $143.00 with beef crosses bringing more than double, averaging $340.00; 80-100 lb $130.00, beef crosses $280.00.