UPDATED! By Sherry Bunting, Updated from the article in July 24 Farmshine print edition

BROWNSTOWN, Pa. — June milk check reports are pouring in after Farmshine’s previous article about negative Producer Price Differentials (PPD) included a request for milk check data from readers. Along with the data, we are receiving many comments.

One producer notes the PPD had typically averaged a positive $1.50 in his area of the Northeast, but for June, it was a negative $5.38, a loss he pegged at $15,000 for the month for his farm.

Another producer in the Mideast area noted a loss of over $60,000 in component value, which would not be covered in the way expected by the Dairy Revenue Protection (DRP) policy he had purchased. The negative PPD loss represents “basis risk”, whereas tools like DRP, forward contracting, even DMC, mitigate “market and margin risk.”

The “markets” did their thing. Demand went up, cheese prices went up, Class III milk contracts gained, but the de-pooling in most Federal Milk Marketing Orders (FMMOs) ate up most of the doubled protein value and other component value gains for farms across most of the country, as reflected in a steeply negative “basis”. There’s really no risk management tool for that, and we’ve received correspondence indicating that producers who opted to manage risk, had losses where they thought they would have coverage.

It’s difficult to make sense of it all, especially when FMMO Market Administrators explain all the workings of PPDs in terms of advance pricing, sudden commodity increases that are complicated by advance pricing of Class I, pooling and de-pooling of milk when Class I milk value is lower than the blend price. But these explanations leave out the fact that Congress changed the way the Class I Mover is calculated at the request of NMPF and IDFA in the 2018 Farm Bill, without holding a milk pricing hearing that so many have requested.

This is a big concern going forward. The spreads between the higher Class III price over the Class I Mover are $9.62 for June and $7.75 (estimated) for July.

From July, forward, the lagtime is less of a factor. However, the new way vs. the old way of calculating Class I is a much bigger factor in predicted negative PPDs because as Class III has been rising, Class IV has been falling, widening the divergence.

The final math equation for the Class I Mover is the same as it was: Class I Mover = (Base Skim Milk Price x 0.965) + Butterfat Price x 3.5). What changed in May 2019 is the way the Base Skim Milk Price is determined before it is placed in that calculation. It used to be simply the higher of the two Advance Pricing Factors — Class III or Class IV — that was plugged into that equation as the “Base Skim Milk Price. Now the two Advance Pricing Factors are added together, divided by 2, and 74 cents is added to that to produce the Base Skim Milk Price for the final equation above.

Under the previous way, using the “higher of,” the August Class I Mover would have been $24.36 — $4.58 higher than the $19.78 Class I Mover announced on July 22 for August. Also, under the previous method, July’s Class I Mover would have been $19.13 — $2.57 higher than the announced July Class I Mover at $16.56.

These new concerns in FMMO pricing bring new variables into how producers manage risk, so the market value that did not make it into milk checks or risk management tools cannot be blamed completely on Covid-19 pandemic disruptions. A convergence of factors have created a situation where the mechanics of risk management like Dairy Margin Coverage (DMC) and Dairy Revenue Protection (DRP) — as well as forward contracting — may not work as intended for all producers in all regions in a time of disrupted markets and extreme risk, with fairly recent changes to certain milk pricing formulas.

This market disruption, and the fallout in negative PPDs, should signal to USDA and the Congress that a National Hearing on Milk Pricing is overdue. Piecemeal changes have consequences. The de-pooling exacerbates the situation. In June, de-pooling contributed to removing hundreds of millions of dollars of value from milk checks across all Federal Orders. As one producer asked, who gets that money? The answer: It depends.

First, if the end-product “market” value found was paid to the plant or cooperative or handler, and if the handler consequently de-pooled the milk and didn’t pass that value back to the farms voluntarily or contractually, then we know who has the money. If the “market” did not pay what we see in the USDA end-product pricing or on the CME spot market and futures markets, then it’s not real money.

Given the wide range in milk check data with most of the nation coming in around $5 to $7 lower than the Upper Midwest — and a $4 range in FMMO uniform prices to begin with — it’s obvious the “market” is paying. But the calculations are not passing through to milk checks, except in the Upper Midwest Order 30 where 50% of pooled milk receipts were utilized as Class III milk, even though Class III volume reductions suggest significant de-pooling occurred.

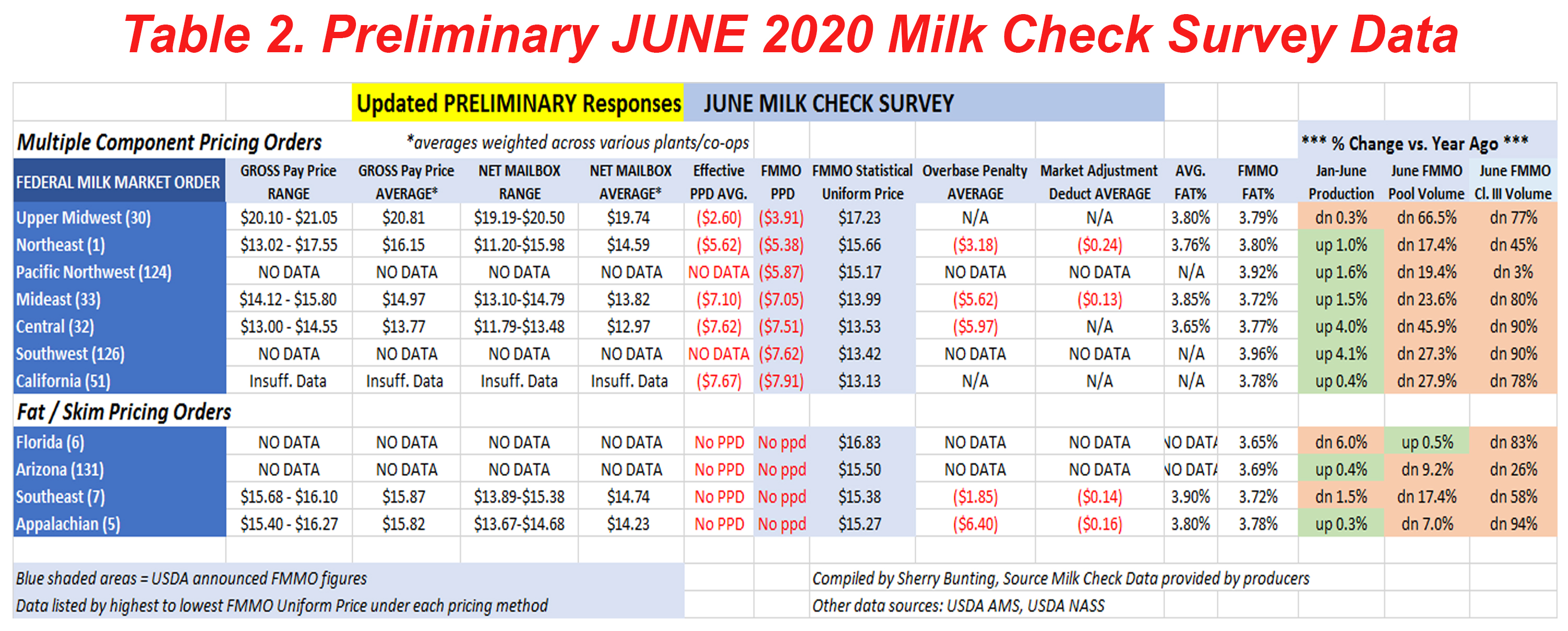

Let’s look at preliminary data from Farmshine readers around the country (Table 2 above).

So far, over 150 Farmshine readers from six of the 11 FMMOs have provided milk check data. Since only a couple responses were received from California, we did not do any math for FMMO 51 yet, until we receive more data. At this writing, we have not received any milk check data from Orders 6 (Florida), 126 (Texas and New Mexico), 124 (Arizona) and 131 (Oregon and Washington).

What is evident in the preliminary review is the significant gap between the highest and lowest gross and net prices paid.

For each of the six FMMOs — where we had enough data to do some math — we see the difference of $7 between the FMMO with the highest average gross price paid (before deductions) of $20.81 in the Upper Midwest (FMMO 30) and the lowest average gross price paid of $13.77 in the Central Order (FMMO 32). When looking at the range of price data, the spread is $8 between some check data as low as $13.02 gross pay price in Pennsylvania to $21.05 in Minnesota.

The other FMMO average data fall into place $4 to $6 below the Upper Midwest with gross pay price averaging between $14.97 and $16.15 before deductions.

On the net mailbox price (after deductions), the difference is almost $7 between the highest mailbox average of $19.74 for FMMO 30 and the lowest average of $12.97 for FMMO 32. Average net mailbox price for FMMOs 1, 33, 5, and 7 trail FMMO 30 by a difference of $5 to $6. (See Table 2.)

Respondents for each of the FMMOs so far are a mix of mostly co-op members, but also some independent shippers, and a range of cooperatives — national and regional — are represented in the data.

In the Upper Midwest FMMO 30 for June, where PPD was least negative and Class III milk utilization was the highest (50%), the Uniform price already reflected the smallest negative PPD in the $3s compared to negative $5s and $7s everywhere else. At the same time, reports indicate the cheese plants and co-ops in that region even shared some of that smaller loss, knocking it back into the negative $2’s.

While large penalties for overbase milk still remain part of the pricing equation, it was not a major factor for most producers in June, perhaps because producers are reducing production as well as dumping, donating or utilizing overbase milk differently to avoid these penalties. This process is continuing into July. In the Northeast and Midatlantic region, reports of milk dumping were confirmed in July. Mostly this was due to producers wanting to avoid overbase penalties, but at least one report involved temporary “plant equipment issues”.

Of the milk check data shared with Farmshine, most showed producers were shipping 93 to 99% of their base for June. But some data includes producers seeing significant assessments on small amounts of overbase milk by both smaller regional cooperatives and larger national footprint cooperatives — except in the Upper Midwest. Also, in pockets of the Southeast, check data show some penalties were waived as a base / overbase blend was shown on checks, but then in another spot, the stub reported “revenues available to pay” a better price. In those instances, it appears the overbase penalty was eliminated and market adjustments reduced, which added 30 to 50 cents to what the location blend would have been.

Elsewhere, producers overbase deductions ranged $1.50 to $6.40.

Another variable was “market adjustments”. No “covid” deductions were seen in June check data, however, many had “market adjustments” deducted to the tune of 13 to 24 cents. In a few cases, the “market adjustment” was described in an earlier letter stating that the “covid” deduction for co-op costs incurred in April and May was being spread out evenly over several months forward.

The averages for the Northeast and Mideast FMMOs belie the wide range in prices. For Pennsylvania, alone, the range in gross pay prices before deductions was more than $4.00/cwt. Even after adjusting for butterfat, the range was $3.50. The lowest net mailbox prices submitted by anyone in any FMMO came from Pennsylvania producers, with instances as low as $11.20/cwt mailbox for June. Overbase penalties and market adjustment deductions contributed to these lower nets.

In Pennsylvania, the Pa. Milk Marketing Board (PMMB) over-order premium (OOP) was set large for June, but was a small factor on most milk checks. It does appear that the western half of the state in Order 33 received at least some OOP benefit to make up for taking a more significant beating from negative PPDs.

Very few producer milk checks showed numbers other than zero in the PMMB OOP line item. However for Pennsylvania producers shipping directly to some Pennsylvania bottlers in the Mideast order, the benefit was $1.25 to $2.00/cwt listed as a line item and serving to simply pull them up closer to where the Northeast blend price sat. Remember, negative PPDs in the Mideast Order, which includes western Pa., were in the $7s. Negative PPDs in the Northeast Order, which includes eastern Pa., were in the $5s.

Meanwhile, out-of-state bottlers buying Pennsylvania milk and selling into the Pennsylvania minimum retail price market passed on about 10% of this floor-setting OOP in June at about 30 to 50 cents.

June’s PMMB OOP was over $4 per cwt because $3.68 was added to the normal $1 to make the difference between the USDA Class I Mover and a temporary $15 Class I floor. The PMMB used the OOP to temporarily accomplish this, but then became an island as USDA did not follow suit. The USDA had canceled a hearing requested by cooperatives petitioning it do the same nationally.

Looking at the milk check data we have received, it is obvious that USDA would have done well to have followed PMMB’s lead — as they were petitioned to do in April — to set a temporary Class I Mover floor at $15 through August.

At the time that the PMMB took its action, USDA AMS Dairy Programs had indicated in correspondence shared with Farmshine that a date was set to meet with petitioners to hear evidence for a national temporary Class I floor.

But, when word got out, certain dairy economists, such as at the University of Minnesota, along with Minnesota Milk Producers and other entities, including Walmart, protested that this idea of a temporary Class I Mover floor would “decouple” Class I milk and be unfair to the Upper Midwest where Class I utilization is low. Mainly, they complained that a move to stabilize Class I would “disrupt” milk markets and affect the Dairy Margin Coverage.

Well, folks, that disruption happened anyway — in reverse.

What we have seen, in the absence of a Class I floor, is total disruption and instability due to the inherent lagtime in Class I pricing reflecting market trends, and additional severity because of how the Class I Mover calculation was changed by Congress, with no hearing at all, just placed in the 2018 Farm Bill at the direction of National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA).

The so-called “markets” have not worked for any of the FMMO’s dairy producers except for the Upper Midwest where the complaints over flooring the Class I Mover arose.

The change in the calculation of the Class I Mover in the 2018 Farm Bill was implemented one year ago in May 2019. By using an average instead of the “higher of” to determine a base value for components or fat/skim, the Class I Mover no longer moves in concert with the highest value of components or fat/skim.

This is a problem because there is no way to assess market value on Class I in an of itself. Class I beverage milk is a designated loss-leader by the 800-lb retailer-processor gorillas like Walmart and Kroger. Also, in a couple states, the retail milk price is regulated to some degree.

Class I’s new “averaging” method is contributing to the removal of hundreds of millions of dollars from Federal Order pools through de-pooling.

It’s hard to predict what “reality” or “alternate reality” the USDA NASS All Milk price and Dairy Margin Coverage milk margin will reflect when they are announced on July 31.

This is a serious problem, given the widening divergence between Classes III and IV on the futures markets. This divergence is a warning that the current four-class system should be re-evaluated. When two manufacturing classes for stored products can be averaged to produce the basis of value for fresh products and beverages, it’s easy to see how large entities in the marketplace can make decisions that affect imports, storage, supply and demand to move one side of an “averaging” equation and create lopsided returns outside of FMMO pools. If milk moved to its highest value use and components were valued on multiple cross-class markets, a stable Class I base could be established as one piece of an overall value mix with less incentive to de-pool lopsided value.

For example, the July Class III contract stood at $24.41 on the futures markets as of July 27 — now $10.76 higher than the Class IV contract at $13.65. August Class III stands at $22.11, $8.39 higher than the Class IV contract at $13.72. September Class III, at $20.49, is $6.34 higher than the $14.15 Class IV contract. October Class III, at $18.90, is $4.51 higher than Class IV at $14.39. November Class III, at $17.53, is $2.95 higher than Class IV at $14.58. The gap narrows for December, but as of July 27, the difference between the two classes is still more than the $1.48 ‘magic number’ with December Class III at $16.60, $1.81 higher than Class IV at $14.79.

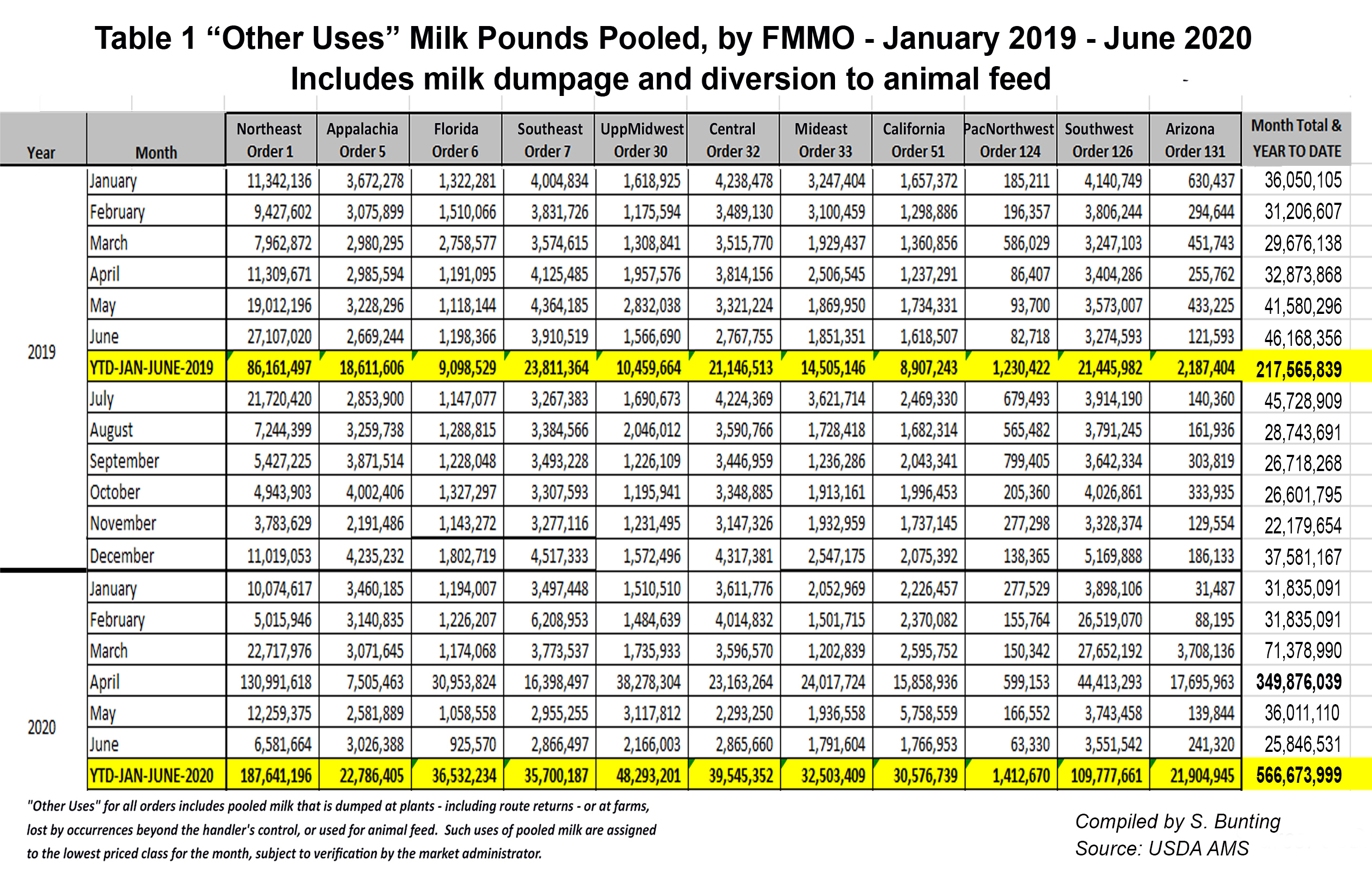

Creating even more value loss in every FMMO in June — whether priced by multiple components or fat/skim — is the amount of Class III milk that was de-pooled. Total volume pooled across all Federal Orders was 9.5 billion pounds in June, down 36% from a year ago and down 28% from May (May 2020 was down 13% from year ago).

While June milk production was reported on July 21 at 0.5% above year ago, milk dumpage in June was down considerably in terms of what showed up on FMMO pools. We know farms are dumping and diverting to avoid overbase penalties, but the pooled “other use” milk, including dumpage and animal feed, was down by 44% compared with a year ago in June. The only Federal Order to have more “other use” milk in June than in May was the Appalachian Order 5, and Central Order 32.

Table 1 (above) shows the “other use / milk dumpage” pooling data. What is mind-boggling is that year-to-date milk dumped totals at 566.7 million pounds for just the first 6 months of 2020, is 125 to 150 million pounds greater than the 12-month annual totals for each of the past five years.

Table 1 (above) shows the “other use / milk dumpage” pooling data. What is mind-boggling is that year-to-date milk dumped totals at 566.7 million pounds for just the first 6 months of 2020, is 125 to 150 million pounds greater than the 12-month annual totals for each of the past five years.

Dairy producers wishing to submit June milk check data as well as next month’s milk check data for July to broaden this survey geographically, please send: Gross price, net mailbox price, PPD, butterfat and protein, other deductions (especially ‘market adjustment’ deductions), overbase penalties if applicable, along with your location or the FMMO in which your milk is marketed and information stating whether you market with a cooperative or as an independent. There is no need to provide your name or your specific co-op or plant affiliation unless you choose to include that.

Please consider emailing me at agrite2011@gmail.com or text/call 717.587.3706. All information is aggregated anonymously by state, region and FMMO.

-30-

By Sherry Bunting, Farmshine, June 1, 2018

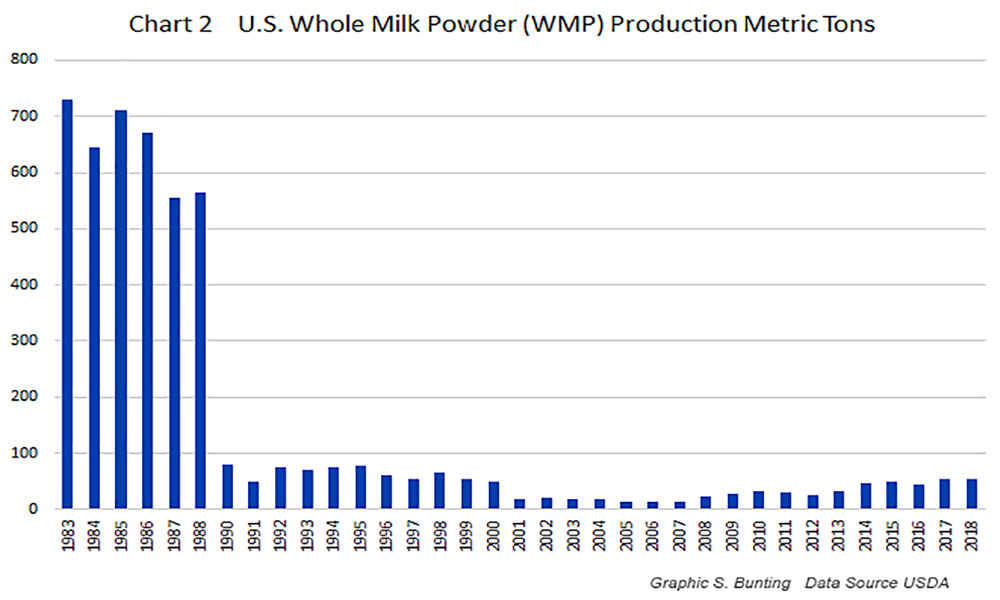

By Sherry Bunting, Farmshine, June 1, 2018 In fact, going back through USDA records to 1983, the U.S. once made up to 700 metric tons of dry whole milk powder (Chart 2). We don’t hear about that.

In fact, going back through USDA records to 1983, the U.S. once made up to 700 metric tons of dry whole milk powder (Chart 2). We don’t hear about that. One reason we don’t make more WMP today is we have a large and growing domestic market for cheese and butter and cream products. U.S. manufacturers want to keep the cream and not sell it overseas, whereas other dairy-producing nations — like New Zealand with its much smaller consumer population — make a lot of WMP for Asia.

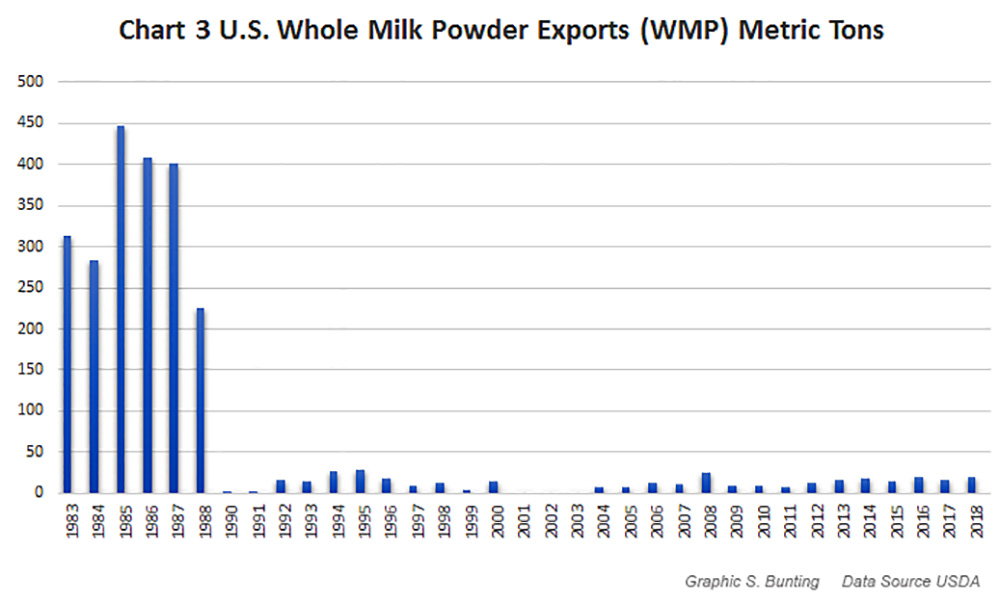

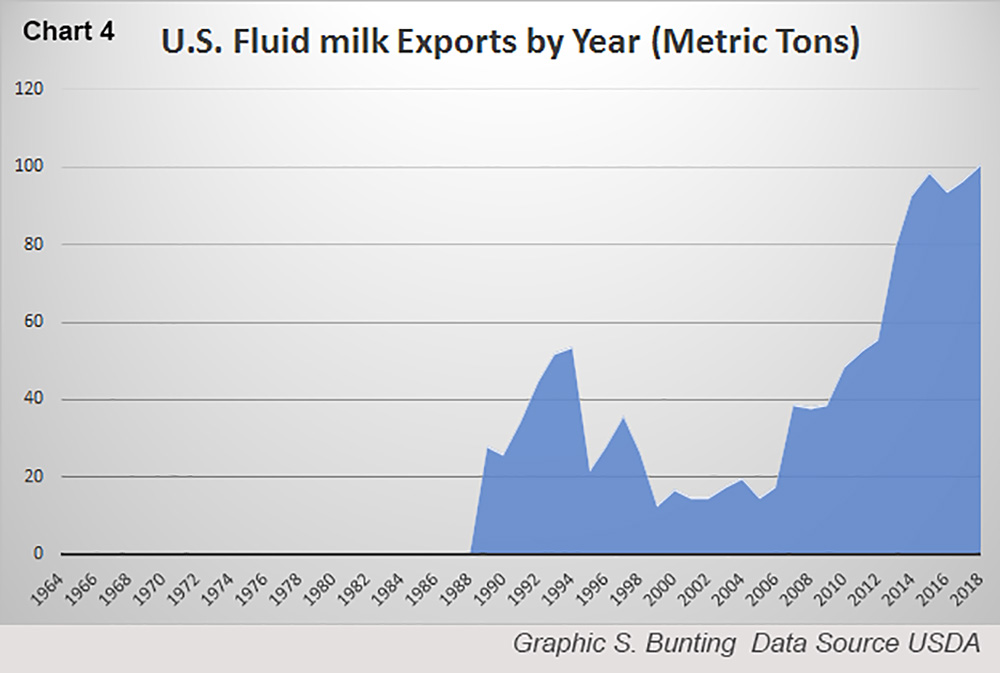

One reason we don’t make more WMP today is we have a large and growing domestic market for cheese and butter and cream products. U.S. manufacturers want to keep the cream and not sell it overseas, whereas other dairy-producing nations — like New Zealand with its much smaller consumer population — make a lot of WMP for Asia. One lesser-known category of exports that grew by 85% in the first three months of 2018 is UHT shelf-stable milk. China is the biggest buyer, and DFA is a primary supplier with its California Gold, a primarily 3.5% fat, shelf-stable drinking milk with a non-refrigerated shelf life of one year. This product is shipped to Walmart and other chains in China. These sales have grown significantly since 2006. (Chart 4)

One lesser-known category of exports that grew by 85% in the first three months of 2018 is UHT shelf-stable milk. China is the biggest buyer, and DFA is a primary supplier with its California Gold, a primarily 3.5% fat, shelf-stable drinking milk with a non-refrigerated shelf life of one year. This product is shipped to Walmart and other chains in China. These sales have grown significantly since 2006. (Chart 4)