Talking candidly about dairy markets and trade were market experts (l-r) Tom Wegner, Land O’Lakes economist; Tom Roosevelt, founder and owner of West Chester-based Roosevelt Dairy Trade, Inc; and Matt Gould, owner of Philadelphia-based Dairy & Foods Market Analyst, LLC. Photos by Sherry Bunting

By Sherry Bunting, published previously in Farmshine, November 30, 2018

BAINBRIDGE, Pa. – “There is a long list of demands coming from consumers with unprecedented opportunities for milk,” said Matt Gould, owner of Dairy & Food Market Analyst LLC, based in Philadelphia. “Consumer demands are the key, and they are willing to pay for them.”

That was the good news. Gould said that Pennsylvania has an image to capitalize on, and part of that image is family farms working close to the land and animals — the iconic Lancaster County Amish-made image — for example.

But by the end of the forum, it was clear that how the state of Pennsylvania — and the eastern states in general — can tap into value-added dairy opportunities will require both individual and collective soul-searching.

The not-so-good news was the main substance of three hours with three dairy market experts at the annual Professional Dairy Managers of Pennsylvania (PDMP) Fall Issues Forum on November 14 at the Bainbridge Fire Hall in Lancaster County.

Each expert, in their own way, painted a changing and sobering portrait of the dairy market landscape. Producers in Pennsylvania, and the eastern U.S. in general, are not located where commodity processing growth is occurring to serve rapid growth for export and foodservice markets, but instead, exist in a market where declining fluid milk consumption is dictating the terms and leaving mainly the option of slow growth consumer niche markets that take time to develop and must be “continually fed.”

The experts noted that even though the Northeast is down to 30% Class I utilization, 87% of fluid milk sales is water that is expensive to ship, so, in a sense, the albatross around the neck of eastern dairy farmers is the fluid milk market needing farms nearby consumers, but at the same time declines in fluid milk sales are pressuring those farms.

In fact, the experts characterized the East as mainly a fluid and specialty market for dairy. Not the news many wanted to hear since a recent Pennsylvania Dairy Study suggested the Keystone State is a good location for a new cheese plant, and the Port of Philadelphia was tagged in the study as a vehicle to potentially capitalize on export growth markets.

Tom Roosevelt, founder of Roosevelt Dairy Trade, Inc., West Chester, said that commodity processing expansion is mainly associated with export growth and that is all being centered on the West and Midwest.

“A new cheese plant is not my first thought for Pennsylvania,” he said bluntly.

In fact, all three panelists agreed that the Keystone State’s hope is in building niche markets, and they offered these strategies: 1) branding the state’s image, 2) improving milk components, 3) marketing to consumers who have an emotional connection to where their food comes from and how it is produced, and 4) altering production practices — such as Organic, non-GMO and animal welfare labeling — to meet those niche demands.

They also preached the need for greater efficiency and market discipline, that producers here will increasingly see base/excess programs and will need to be using risk management tools and futures markets to get a ‘flat’ price because a ‘flat’ price is where the industry is headed in the midst of volatile global trade factors.

All three experts indicated that the deepening national and global dairy crisis won’t get better any time soon, and that Pennsylvania has some additional long-term challenges if it wants to retain and grow dairy.

Billed as a session to take dairy markets and trade ‘beyond the spin,’ the forum discussion was brutally honest. While disheartening, the information about what is happening here in the context of what is happening elsewhere is important for constructive ongoing discussions in Pennsylvania and other eastern states about the future of their dairy farms that are key to agriculture infrastructure and state and local economies.

When asked about the potential to change how milk is priced, Roosevelt said that there is no question the CME is thinly traded, but that electronic trading has brought in more activity. He said the USDA National Dairy Product Sales Report that provides the product prices for milk pricing formulas, is outdated.

He and Gould agreed that substantial changes to Federal Order milk pricing are not likely to happen because the investments of large companies (think Walmart, Leprino, etc.) rely on a “stable regulatory environment to protect their investments.”

Adding value

Gould challenged Pennsylvania’s dairy industry to instead focus on “value-added” processing and marketing instead of focusing on making more milk.

Tom Wegner, economist with Land O’Lakes said that, “Three years of tough markets would seem to be due for a price peak, but I don’t want to give any notion that it will get better soon. That is the impact of long milk. We are long on milk, and that will probably continue for a while.

Tom Wegner, economist with Land O’Lakes, shows global milk production patterns during the PDMP forum on dairy markets.

“Your production of components here is more important to enhance milk checks than anything else,” Wegner said.

Roosevelt was particularly candid: “It’s tough to look at this part of the country and think you’ll have dairy exports. The real benefit you have here is in value-added.”

He gave the example of conventional nonfat dry milk selling for 85 cents a pound when organic powder is over $4.00/lb. (The flip-side of this proposition is the very high feed costs and other costs for organic production in which consolidation is also happening, so those producers also are having tough times.)

“It is hard for you to compete on a commodity level,” said Roosevelt from his experience trading dairy commodities at a ratio of 60% domestic use, including animal and pet feed makers, and 40% exports, noting the export trade really began in the past eight years.

“We do a lot of business with Land O’Lakes and Maryland-Virginia,” he said, “but we don’t move hardly anything into export markets out of the Northeast. The fluid market dictates things here in the East compared with the West and Midwest, where cheese is king.”

Roosevelt said the Midwest, Southwest and West are where dairy plants are doing line extensions, and new plants are being planned and breaking ground.

Global volatility

“These companies and cooperatives are going after the commodity big-volume markets to China and Mexico,” said Roosevelt. “If tariffs take those markets out, then it will affect you here because that milk moves down the line. When those markets move product out of the U.S., that means less competition for you here.”

The export markets are deemed the growth markets, said the experts, because domestic demand is declining in some sectors and offers only slow-growth opportunities in other sectors.

With the growth-focused U.S. dairy industry fueled mainly by exports, the volatility of the global market has forced more of the industry to use the CME futures markets to get the ‘flat price’ they want in their quarterly contracts, according to Roosevelt.

“As traders, we trade off the market price and use the futures to convert that to a flat price,” he said. “I would urge you to look at the futures to get a flat price. It’s a tool that will be increasingly important to all of you because, whether we like it or not, we are in a global market and futures are a way to reduce that volatility.”

Roosevelt’s bottom line was for producers to be as efficient as they can and look for the market that “gives you the value, whether it’s artisan or organic.”

Wegner echoed the advice on being efficient. He said the largest farms have the advantage of stretching their economies of scale and taking a longer view in this long period of long milk.

He gave a history of Land O’Lakes with its butter production dating back to 1921 and the eventual merger with Midatlantic here in the East.

“We aggregate demand also,” he said, a nod to Land O’Lakes’ Purina. “We want more of our members to buy more of our products, not just sell us milk.”

Explaining Land O’Lakes’ market-back philosophy, Wegner said the cooperative has put tools together that include traceability and are trying to put production discipline tools into that mix.

“We come to our customers with a farm-to-fork approach and send that back through milk production for an end-to-end view,” said Wegner. “Being farmer-owned is a great part of our background as we continue to grow markets.”

While Pennsylvania’s average herd size is 90 cows, most of the producers attending the forum represented farms with 300 to 1200 cows. Some of the questions lingering in their minds were: How many niches does a dairy market have? And what will it take to develop those in-roads to cover more milk and spread those opportunities beyond the small farm-store label at the end of the drive?

While niche-marketing connects producers and their location and practices with consumers who develop that emotional tie, Roosevelt said the dairy commodity supply-chain has been developing its own sets of practices and programs.

Supply-chain realities

“Traceability is a huge part of our business, and it is as important on the feed side as the food side working with customers like Cargill and ADM,” he explained, noting the huge increase in paperwork following every product delivery. Not only are there certified analyses, date processed, how processed and lot numbers, but in the case of whey, the buyer wants to know what type of cheese process produced the whey because each one has its own profile. He gave the example of whey from Swiss cheese being whiter and higher in protein.

He noted they are getting questions about organic and non-GMO whey, which will produce even more paperwork, and that the traceability aspect is moving back the supply chain to the farm level.

Wegner also talked about traceability. While he didn’t mention it specifically, both Land O’Lakes and DFA are trialing block-chain technology to follow product digitally through the supply chain. Walmart is driving full traceability and moving toward block-chain technology.

“Walmart is one of our biggest customers for butter,” said Wegner. “Just think of the traceability challenges of mixed loads with hundreds of producers.”

The National Milk Producers Federation FARM program was described as a way of consolidating groups of producers into blocks that are being evaluated to use approved practices.

“Members want to know ‘what’s in it for me?’’ said Wegner, “but the reality is that the FARM program contains a lot of the things we have to do to be part of the market.”

Not only are domestic commodity dairy sales being driven by large fast food chains that want to be sure a farm-level animal welfare issue, for example, doesn’t damage their name, the export markets have this concern as well where brands are involved.

Wegner noted that Pizza Hut is launching a new restaurant every 18 hours, globally, and the Yum brand, which includes Pizza Hut and Taco Bell, are opening new restaurants every 8 hours across the globe. He said that 80% of the menu items at these restaurants include dairy. They secure cheese from the U.S. and are concerned about capacity and traceability over the next three years.

For example, Leprino has 80% of the market share for U.S.-produced mozzarella, said Wegner, and their growth is more concentrated in states like Michigan, Colorado, New Mexico and California.

Trickle-down effect

With the commodity production for export and large chain foodservice sectors growing — and served mainly by the Midwest and West — Roosevelt maintained that this export growth is still very important to the East because “the benefit trickles down from the West.”

He said that, “The value of growing exports, for you, is that you will have less competition coming from the Midwest and West.”

What can alter that picture — overnight — is the impact of trade tariffs and trade wars with the top three countries for off-shore dairy trade, in order: Mexico, Canada and China.

He said the tariffs have had an incredible effect on lactose trade. Those customers can go to Europe. “There’s plenty of lactose in Europe and they are quick to fill the gap with a lower price,” said Roosevelt.

Another big trade item is permeate, which is 70 to 80% lactose with some protein left in. There are fewer global competitors in this market, but when the tariffs hit, product was “in the water” and fourth quarter contracts were being negotiated, resulting in buyers and sellers splitting the extra costs and new contract offers coming in on lower bids.

The bottom line on these two commodities, according to Roosevelt, is less market for U.S. lactose and a lower price on U.S. permeate.

As for nonfat dry milk powder, it goes all over, but primarily to Mexico, Canada and China, in that order. The “new NAFTA” and the trade war with China, combined, can have an impact on all three export destinations for nonfat dry milk.

Mainly, Roosevelt’s point was that trade uncertainty can create changes “overnight” that affect dairy, and that tariffs are bad for agriculture, in general, because they “create inefficiencies that stop the normal market dynamics from taking effect.”

Like every other economist at every other meeting, Wegner talked about how Europe “really put on milk” when the quotas were removed. He admitted that he was among those who didn’t believe it would happen. But it did. And this extra milk, said Wegner, resulted in stockpiled powder that drove prices down globally.

With some intervention and drought conditions affecting Europe, the EU’s growth this year was only 1.4% instead of 2.5%. But a 1.4% growth in Europe represents far more milk than the same percentage of increase in the U.S.

Growth challenges

Wegner explained that the U.S. is growing milk production at roughly 1% per year now, but that equates to 2 billion additional pounds of milk annually. At the same time 600 million fewer pounds are going into bottles for Class I sales.

“That is what is challenging our system,” he said. “We are seeing the cows come out of the system, but better cows are going back in. For things to get better, a lot more cows need to come out.”

With Land O’Lakes having a national footprint, Wegner observed the challenges of more milk coming on in some of the largest herds in the nation. While California is not growing year-on-year, Texas and the Southwest states are growing rapidly.

He noted that even though Michigan’s growth slowed this year, “Michigan is the poster-child for the hazard of growing ahead of the market,” said Wegner. “They doubled their production from 5 billion pounds in 2000 to over 10 billion pounds by 2018, and this drove their price $2 below everyone else because their milk has to move around.”

Wegner touched on the recent Pennsylvania Dairy Study and its finding that a new cheese plant or other new processing capacity could reduce hauling costs for producers and add value to farm level milk pricing.

“New processing is easy to do, but what do you do with the additional product?” he suggested. “We take a market-back approach at Land O’Lakes because if we don’t sell it or eat it, the product gets stored.”

Wegner called cold storage cheese stocks “very high” and he said that butter stocks were “a little higher than they need to be.” (Note that the USDA cold storage report the following week showed a record-high draw-down in butter stocks that may have improved the butter storage situation.)

Wegner also said that Mexico’s retaliatory tariffs, if they remain in place until a new trade agreement is signed, are already stagnating U.S. cheese production into storage – cheese that had been going to Mexico. (Cheese exports were down 9% compared with a year ago in September.)

The bright spots, he said, are the dairy ingredient markets. “But the Class III market, right now, is a dog.”

The Class IV market is improving as Europe works through its mountain of powder, bit by bit. That powder is getting close to two years old, and Wegner observed that the U.S. is selling fresh powder at a price advantage to buyers who want fresh.

Looking at some of the specific market impacts of the trade tariffs, Wegner stressed the “woefully underestimated” tariff-mitigation payments by USDA to dairy farmers, and all three experts agreed that these tariffs, and more that will potentially kick-in January 1st, are having very negative impacts on the U.S. dairy supply chain.

When asked how these impacts could be blamed for the lack of a price recovery when U.S. dairy exports have been record-high for January through September (most recent figures), the response was that producers should not expect higher export levels to improve farm-level prices because these export markets are largely “market-clearing” commodity markets.

PDMP executive director Alan Novak opens the discussion to questions from the 60 dairy producers and industry representatives gathering at the Bainbridge Fire Hall on November 14 for the Professional Dairy Managers of Pennsylvania’s (PDMP) Fall Issues Forum focused on dairy markets and trade.

Also driving milk production and processing west are the incentives western states provide for new plants, new dairy operations, and growth of existing businesses. For example, the I-29 corridor of the Dakotas is an area that has lots of capacity, is building more, and has dairies, like Riverview, adding cows in a big way.

Indiana and Michigan are other examples of states becoming big dairy suppliers via Select Milk Producers and Fair Oaks. Colorado’s growth is fueled by Leprino, and Texas has multiple growth influencers, including line extensions by Hilmar.

Taken together, the U.S. has grown milk production by 17 to 18 billion pounds of annual production over the past five years, according to Wegner. That’s like adding another Pennsylvania and Minnesota to the nation’s milk load. Wegner said that boils down to 50 million more pounds of milk per day moving in the U.S. compared with five years ago.

Wegner also talked briefly about Land O’Lakes’ base/excess plans. “This is our way of putting some discipline into the discussion, which goes to our market-back approach,” he said. “We moved a lot of milk from our milkshed this year, and that long milk has a cost. At the same time, he noted that Land O’Lakes has been stripping and dumping milk here, that its producers are assessed to pay for that.

“We worked with DFA (Dairy Farmers of America) and DMS (Dairy Marketing Services) on this step to do cream salvage,” he added.

Land O’Lakes’ view of investing in processing is that the products have to be able to move along the value chain in order to produce more of them.

-30-

By DIETER KRIEG

By DIETER KRIEG

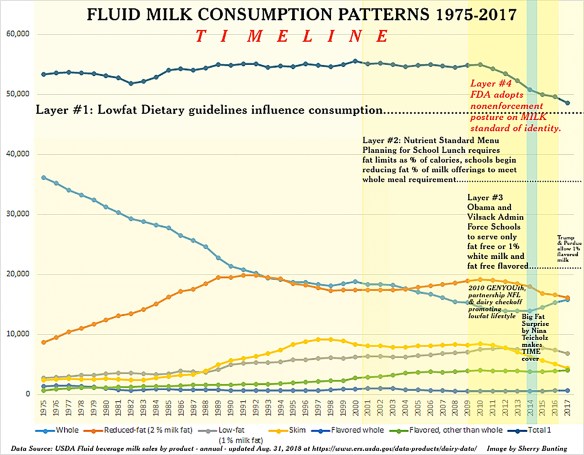

That is, until we hit 2009-10, when the third and fourth layers (see Chart 1 above) were added to the lowfat-push — that consequently pulled total fluid milk sales into the bucket at the same time that exports began their rapid ascent.

That is, until we hit 2009-10, when the third and fourth layers (see Chart 1 above) were added to the lowfat-push — that consequently pulled total fluid milk sales into the bucket at the same time that exports began their rapid ascent.

By Sherry Bunting, originally published in Farmshine, June 7, 2018 and examines the utilization of domestic Class I fluid milk vs. exported commodities during the worst three months of pricing at the beginning of 2018, but the trends show how FMMO pricing no longer provides the value to farmers for their milk as exports increase. Read Global Thoughts

By Sherry Bunting, originally published in Farmshine, June 7, 2018 and examines the utilization of domestic Class I fluid milk vs. exported commodities during the worst three months of pricing at the beginning of 2018, but the trends show how FMMO pricing no longer provides the value to farmers for their milk as exports increase. Read Global Thoughts  The total “official” U.S. Class I utilization for 2017 was 26.1%, down nearly 10% from 35.9% in 2009, according to USDA figures.

The total “official” U.S. Class I utilization for 2017 was 26.1%, down nearly 10% from 35.9% in 2009, according to USDA figures.