By Sherry Bunting, Farmshine, October 9, 2020

BROWNSTOWN, Pa. — The bottom line is the Federal Milk Marketing Orders are not functioning as farm-level pricing can be easily manipulated.

Negative PPDs continue to persist, and all indications are this could be the case through yearend. Several stories in Farmshine since May have covered the Producer Price Differential (PPD) situation and what it means to producer milk checks.

Now, even the American Farm Bureau Federation (AFBF) is on record evaluating the fallout from the new way of calculating the Class I advance base price as implemented May 2019 after passage of the change was made part of the 2018 Farm Bill.

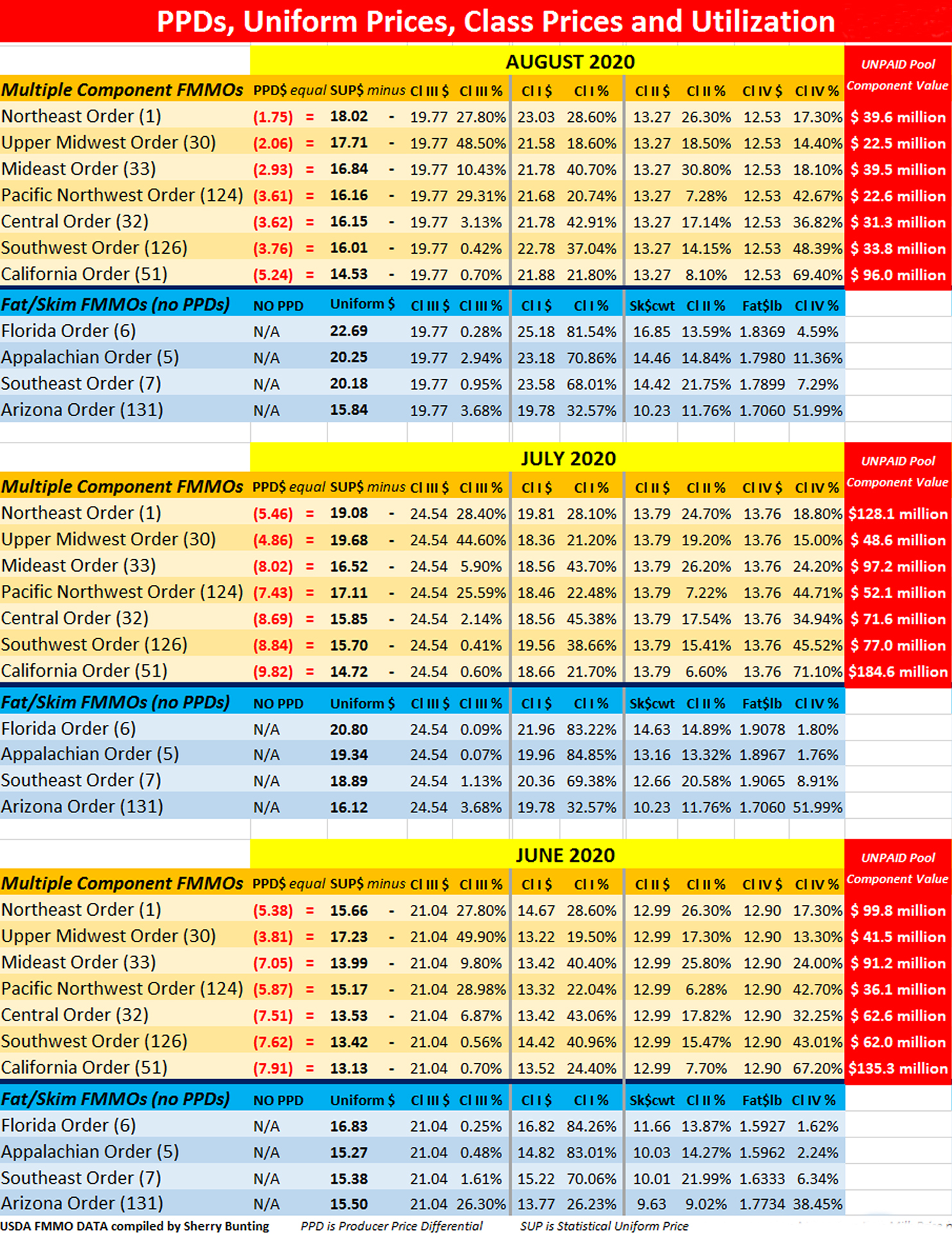

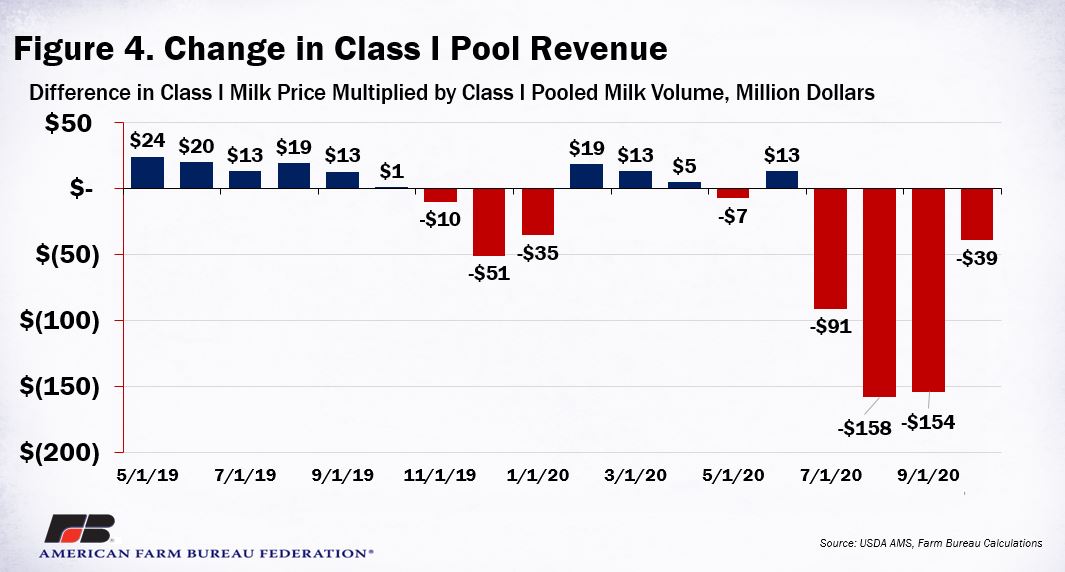

In terms of the money subtracted from Federal Milk Marketing Order (FMMO) pools, Farmshine first reported the $1.48 billion in FMMO revenue gap across 7 of the 11 FMMOs that are multiple component pricing orders. The article and above chart were published in the September 18 edition. September losses will be reflected in FMMO reports in mid-October, and so far PPDs for September milk are mixed, some positive and some negative, but all are well below what would be the case under the old Class I pricing method.

This week, AFBF dairy economist John Newton pegged the cumulative loss to Class I value, alone, at $2.00 per hundredweight or $403 million to-date, across all FMMOs just on Class I milk — money unpaid to farmers that stayed in processor pockets. That figure is about 28% of the $1.48 billion component loss figure shown in FMMO negative balance and it correlates to Class I utilization being roughly 28% of total U.S. milk volume.

The Farm Bureau summary also shows the concentrated loss of $436 million in Class I value for May through October 2020. (Interesting coincidence: DFA is today the largest Class I milk bottler with the May 2020 acquisition of 44 of Dean Foods’ 57 milk bottling plants at a bankruptcy auction price of $433 million.)

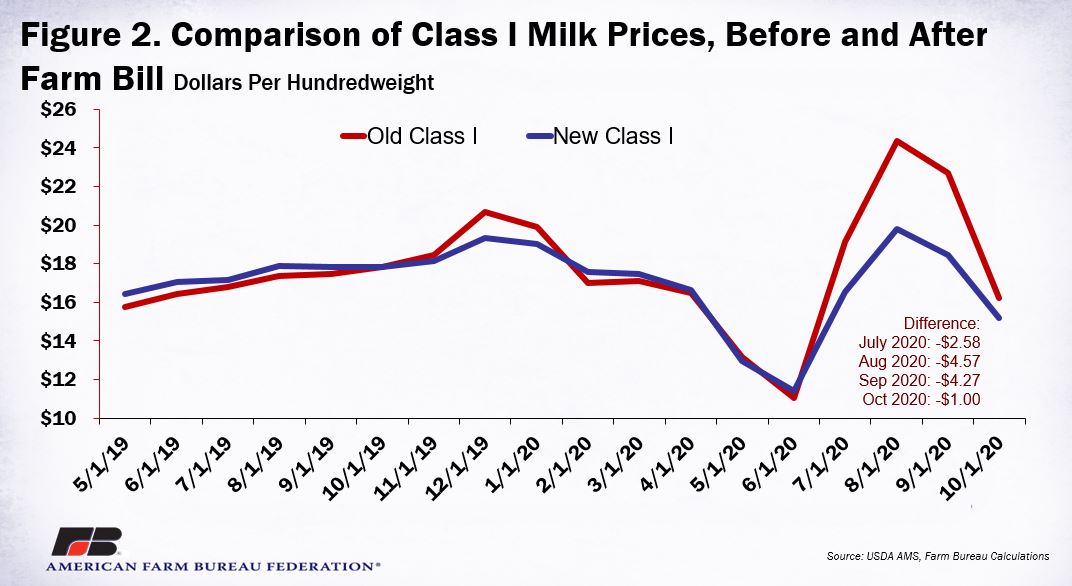

“Due to the rapid rise in Class III prices and a modest increase in Class IV prices, the spread between the two was $6.83 per hundredweight in July, $10.96 per hundredweight in August, $10.30 per hundredweight in September and (will be) $3.56 per hundredweight in October,” writes Newton this week in the Farm Bureau analysis.

“As a direct result of no longer including the higher-of in the milk price formula, the Class I milk price never fully captured the rally in Class III milk prices. Instead, the new Class I milk price was as much as $4.57 per hundredweight below the higher-of formula price in August and $4.26 lower in September,” he continues.

“As identified in Figure 2 (above), had the higher-of formula still been in place, the Class I mover would have exceeded $24 per hundredweight in August,” states Newton.

Newton cites a Class I minimum example for the Southeast, stating that these losses are “before Class I location adjustments are added. In South Florida, for example, with the $6 per hundredweight location adjustment, the Class I milk price would have been more than $30 per hundredweight in August 2020.”

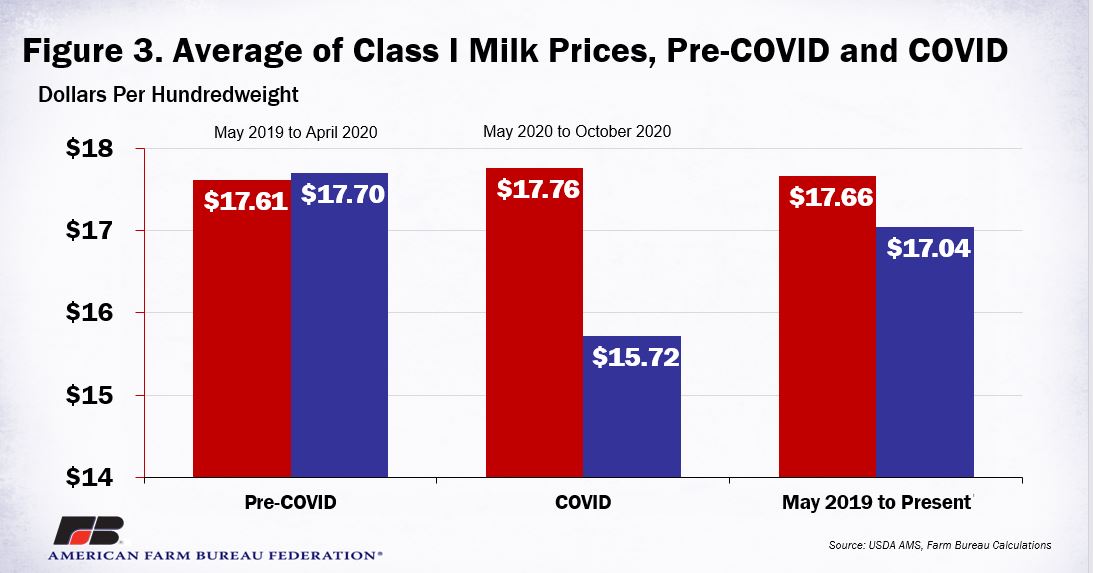

Newton notes that from May 2020 to October 2020, the average difference between the old and new Class I milk price formulas was $2.04 per hundredweight in favor of the beverage milk processor. This means that the regulated minimum prices fluid milk processors had to pay dairy farmers from May through October 2020 were an average of $2.04 lower than what they would have been if the higher-of was still in place.

Going back to May 2019 when the new Class I formula was implemented, Newton notes that the Class I milk price was 62 cents per hundredweight lower on average for the past 19 months compared with the pre-farm bill higher-of formula. (Fig. 3 above)

When looking just at the 12 months pre-Covid from May 2019 to May 2020, the new Class I calculation added 9 cents per hundredweight to Class I pooled volume.

Newton writes that the Class I volume, alone, saw a $32 million benefit in the new Class I pricing in the first 12 months May 2019 through April 2020. Post-Covid, the new Class I pricing method is reflected as a $436 million loss May to October 2020, so the cumulative loss is estimated at $403 million over 19 months of implementation.

This analysis, says Newton, was based on actual Class I pool volume as determined pre-Covid, and does not account for the impact on all milk in and out of the pool for which producers were paid at or near FMMO blend price, before deductions.

The bottom line in looking at the Farm Bureau analysis, along with our own past four months of analysis, the new way of calculating Class I – per the 2018 Farm Bill – would be a relatively benign factor in a ho-hum market if dairy product and component values were at least somewhat accurately reflected across multiple manufacturing classes.

On the other hand, it works poorly in a lopsided market where markets are disrupted, huge government purchases occur on some products and not others, and where huge imports of some products (butter) and not others (cheese) impact accumulating inventory differently for the different milk classes.

While magnified in a severe market disruption like Covid-19 has created, the dairy “market” complex has had lopsided markets in the past and will again in the future at some level. The fact that this pricing change was made without a national hearing and without a dairy producer vote and without an FMMO administrative hearing is concerning.

Some members of Congress have stated that National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) — together — agreed on and requested this Class I pricing change and that Farm Bureau took a non-position, making the change a “no-brainer” for Congress to include in the Farm Bill.

Farm Bureau had done analysis before the change was implemented showing the average over time was neutral. But neutral over time does not reflect month to month cash flow impacts and messed up risk management tools when markets diverge.

What we see in this so-called “neutral” change is the capacity for processors to manipulate the transfer of market value by playing one class against others and essentially removing ‘market value’ from producer milk checks.

Congress needs to hear the story of how dairy farms are impacted in their cash flow and use of risk management tools when a minimum of $1.48 billion in component value is simply sucked out of milk checks over a 4-month period.

Yes, CFAP payments help dairy farmers. But government payments lead dairy even farther away from establishing market value to become more reliant on government payments that, quite frankly, come with more and more strings attached.

Remember, USDA Dairy Programs responded in a Farmshine interview in August to explain that the value missing from pools is “still in the marketplace” even if it doesn’t show up in the FMMO blend prices.

Specifically, USDA stated in that August 3 email that, “The blend price (SUP) is a weighted average of the uses of milk that was pooled for the marketing period (month). If some ‘higher value’ use milk is not in the ‘pool’ then the weighted average price will be lower. It is important to note that the Class III money still exists in the marketplace. It is just that manufacturing handlers are not required to share that money through the regulated pool.

From the looks of milk checks shared in Farmshine’s Market Moos survey in June and July — and looking at the All-Milk prices reported by USDA through August — this ‘money that still exists in the marketplace’ has been largely unshared with producers.

The Class I pricing change was made, according to NMPF / IDFA to so that Class I processors could manage their price risk with forward contracting.

However, CME market brokers and analysts who were questioned about the use of forward contracting by Class I milk bottlers say that few, if any, are doing it. Part of the NMPF / IDFA push for this change was their statements that Class I bottlers would use risk management to stabilize their milk costs if the higher-of method was abandoned in favor of “averaging”.

In fact, some analysts we spoke with report there’s no incentive – even with the new formula – for processors to forward contract a perishable, quick-turnaround product like gallon jug milk. It doesn’t sit in a warehouse like cheese or butter or powder.

… Unless it is shelf-stable ultrafiltered milk — like Coca Cola’s Fairlife products. Coca Cola purchased the remaining shares of Fairlife from the Select Milk Producers cooperative on Jan. 3, 2020 — just 9 months after the new Class I pricing method was implemented.

The industry said this Class I pricing change was needed so that fluid milk processors could stabilize prices and in turn be positioned to invest in fluid milk processing and innovation, which would help dairy producers in the end by providing more Class I markets.

But what happened? Just 6 months after the new Class I pricing method was implemented, the largest fluid milk bottler, Dean Foods, filed for bankruptcy protection and sale in November 2019 with DFA waiting in the wings to buy. Then, 3 months after that, Borden filed bankruptcy and ended up selling to a consortium headed by former Dean CEO Gregg Engles.

Farm Bureau’s analysis this week estimates the impact on dairy farmer revenue from a purely Class I perspective. It does not quantify the full extent of component value removed from FMMOs in the process. Thus, the $403 million cumulative loss impact declared by Farm Bureau represents about 28% of the total loss – which is equivalent to the current nationwide Class I utilization.

This is a Class I pricing calculation change, but its impact on FMMO blend prices and farm-level mailbox prices is pervasive.

In addition, it is important to be aware in this discussion of loss impacts that there is absolutely zero method of calculating the market value of fresh fluid milk. It is not possible to determine what fresh fluid milk is worth because it is:

1) Regulated by federal and state milk marketing orders and boards,

2) Used as a loss-leader by supermarkets selling it far below its cost – especially the largest milk bottling retailers like Walmart and Kroger, and

3) Federal government restrictions on the fat level of milk children are “allowed” to consume at school or daycare.

In short, the federal government controls fluid milk through USDA in lockstep with NMPF / IDFA — and don’t forget, DMI. Dairy checkoff figures prominently in this equation with the same heavyweights at the same table — pushing fat-free, low-fat, ultrafiltered, shelf-stable products, even 50/50 plant-based blends.

Even DMI CEO Tom Gallagher is on record stating that the white gallon isn’t the future because even if children can have whole milk “innovation” is needed and admitting that his job is to “get processors to do stuff with your milk”.

For processors to “do stuff with your milk”, they have to be promised a bigger margin. This could explain why the forward-looking focus of farmer-funded checkoff efforts is on innovation (processing partner margin), not on promoting and educating consumers about fresh fluid milk. And, it might explain why this new Class I formula was needed to average the only so-called market value left in the so-called dairy market.

CFAP payments are salve on some wounds, but the larger issue is still clear: Dairy producers need a voice — apart from the organizations that claim to represent them.

-30-