While the buck is being passed, dairy producers are talking with lawmakers about the unintended consequences from the Class I mover change Congress enacted in the 2018 Farm Bill.

By Sherry Bunting, Farmshine, May 2021

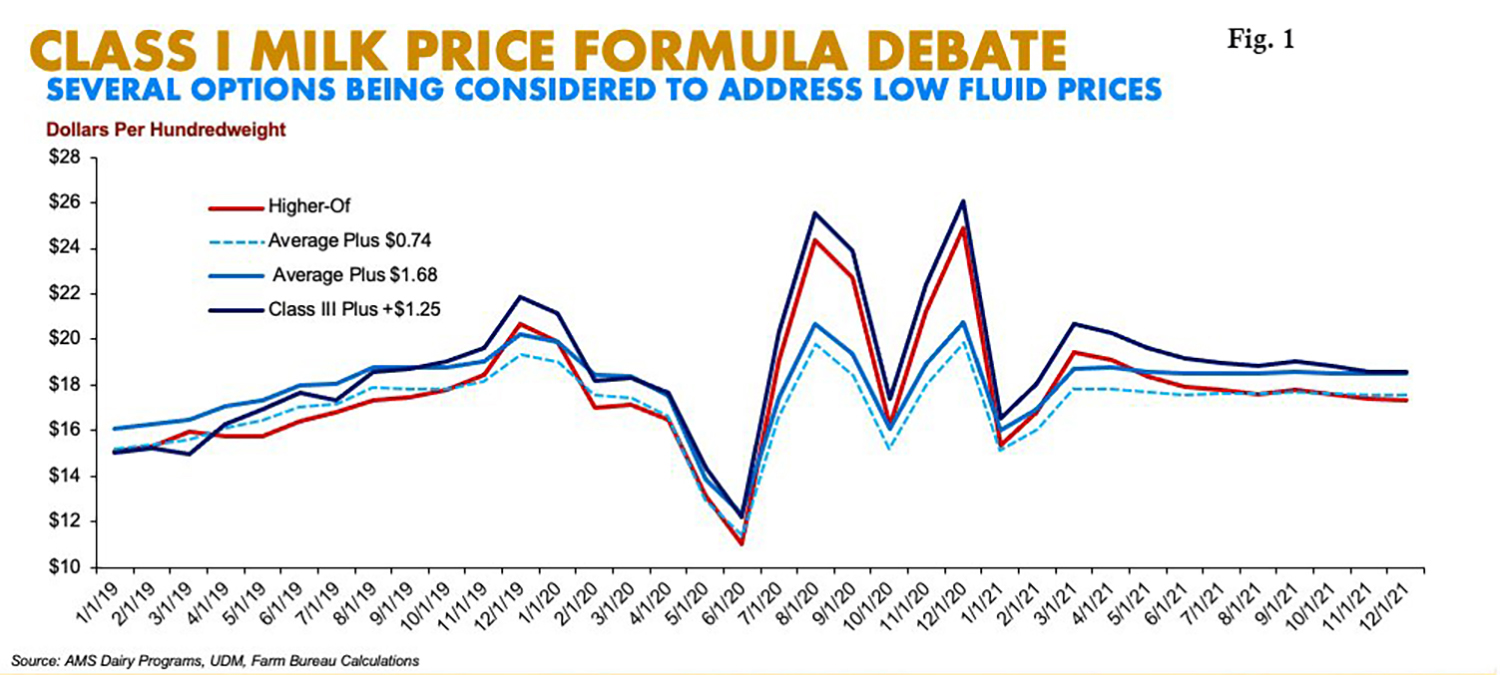

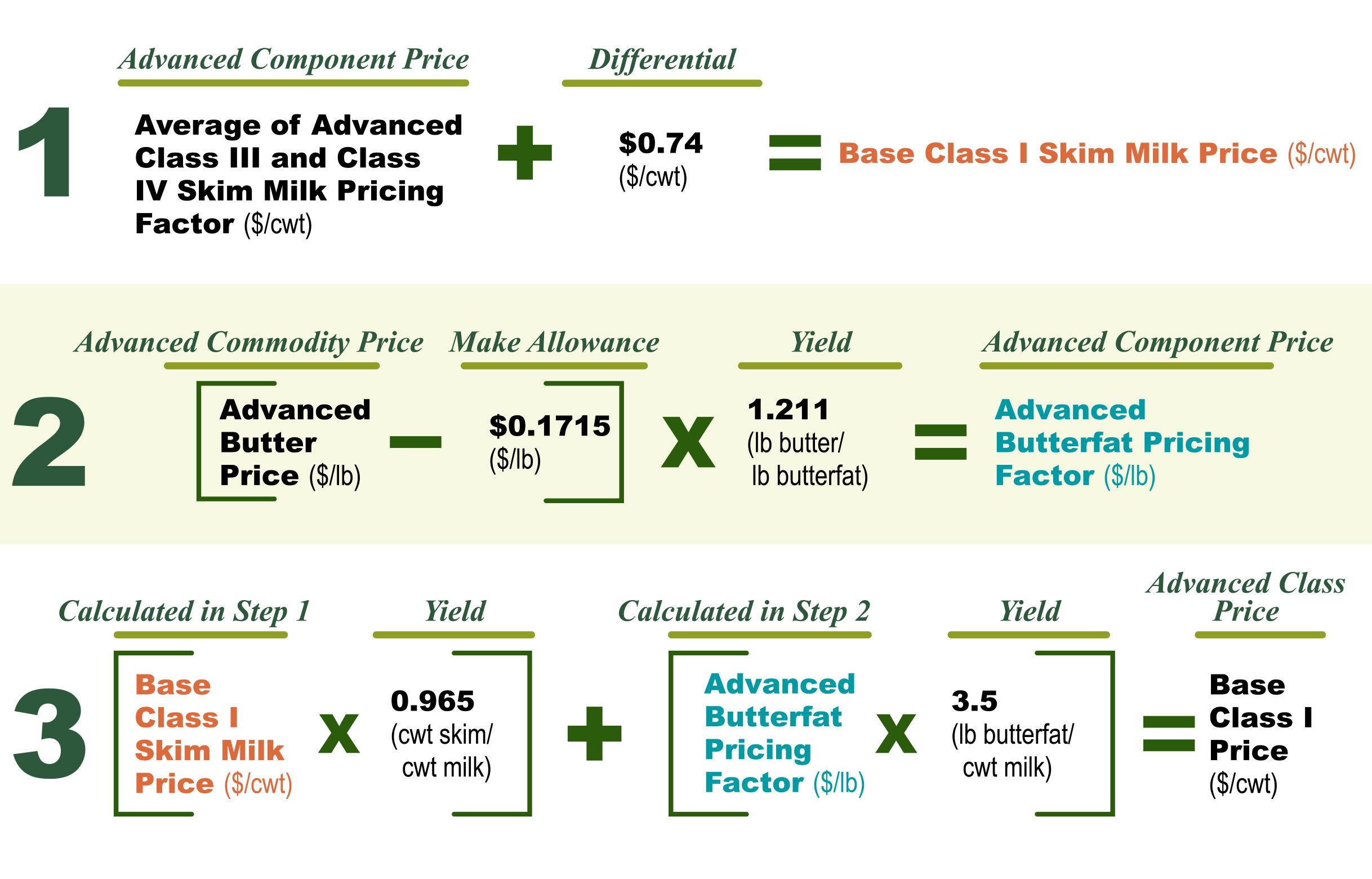

WASHINGTON, D.C. — The Class I ‘mover’ is the subject of much discussion — two years after the averaging method plus 74 cents replaced the ‘higher of’ method to determine the base producer price of Class I beverage milk in May 2019.

A letter drafted by Senator Kirsten Gillibrand of New York is gathering signatures from Senators and will be sent to Ag Secretary Tom Vilsack regarding financial assistance to cover direct and indirect losses borne by dairy farmers due to the formula change exacerbated by the pandemic.

“By allocating more direct payments through CFAP, USDA could take action to reduce the strain that dairy farmers are facing. Specifically, the agency should continue issuing payments to dairy farmers under CFAP, or through any further assistance programs that USDA conceives, including the Pandemic Assistance for Producers initiative, for the first six months of 2021 and make these payments retroactive to January 1st,” the Senator’s letter states.

The American Dairy Coalition is urging producers to contact their Senators about signing onto the letter by end of day Monday, May 17. Senators should contact Dominic Sanchez at Senator Gillibrand’s office by email at Dominic_Sanchez@gillibrand.senate.gov

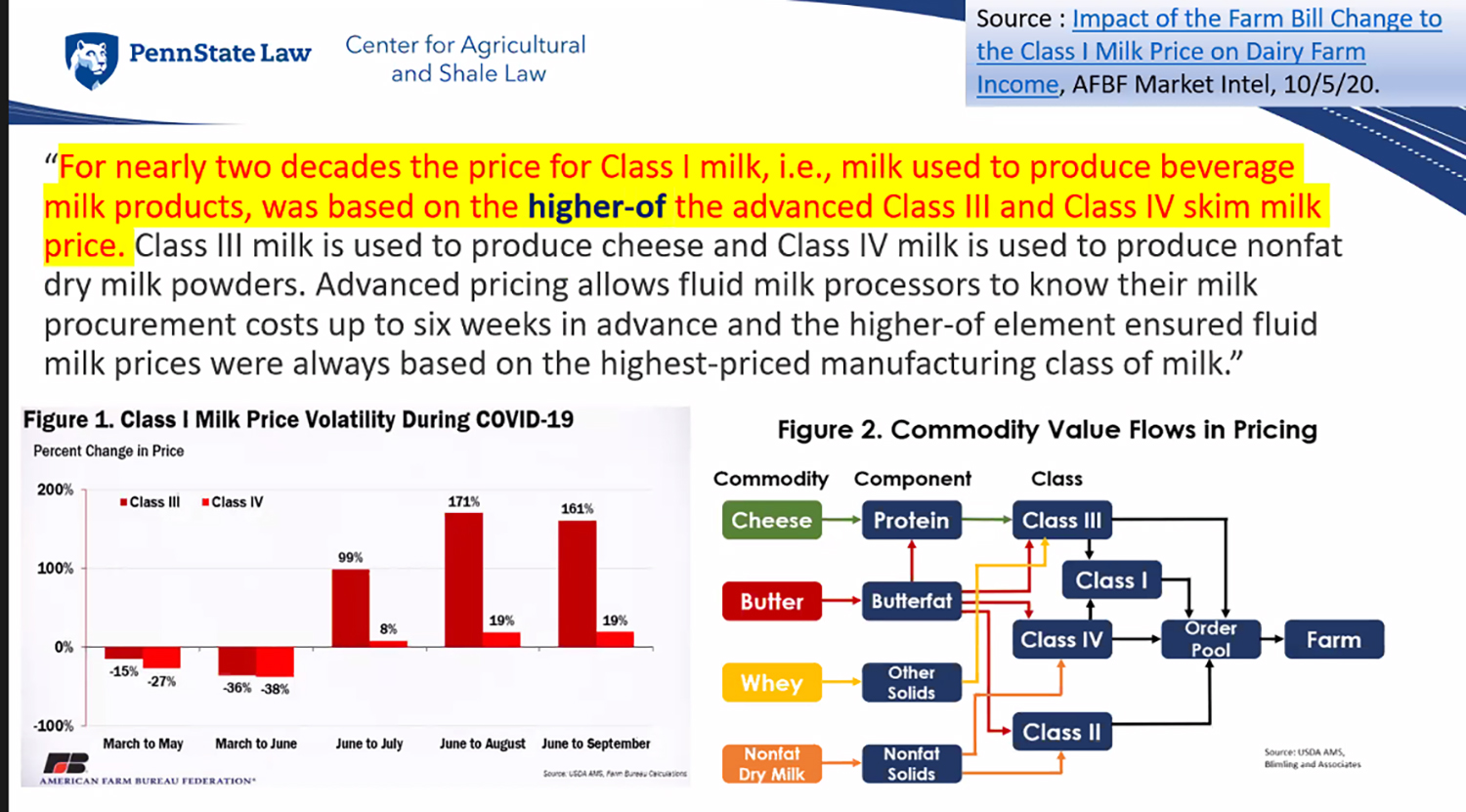

A transparent USDA hearing process was used 20 years ago to originally set the ‘higher of’ as the method when USDA rejected proposals for averaging Class III and IV due to depooling and negative differentials. However, in the 2018 Farm Bill, the Class I mover was changed from ‘higher of’ to an averaging method legislatively without hearings, without comment, without the producer referendum — without vetting.

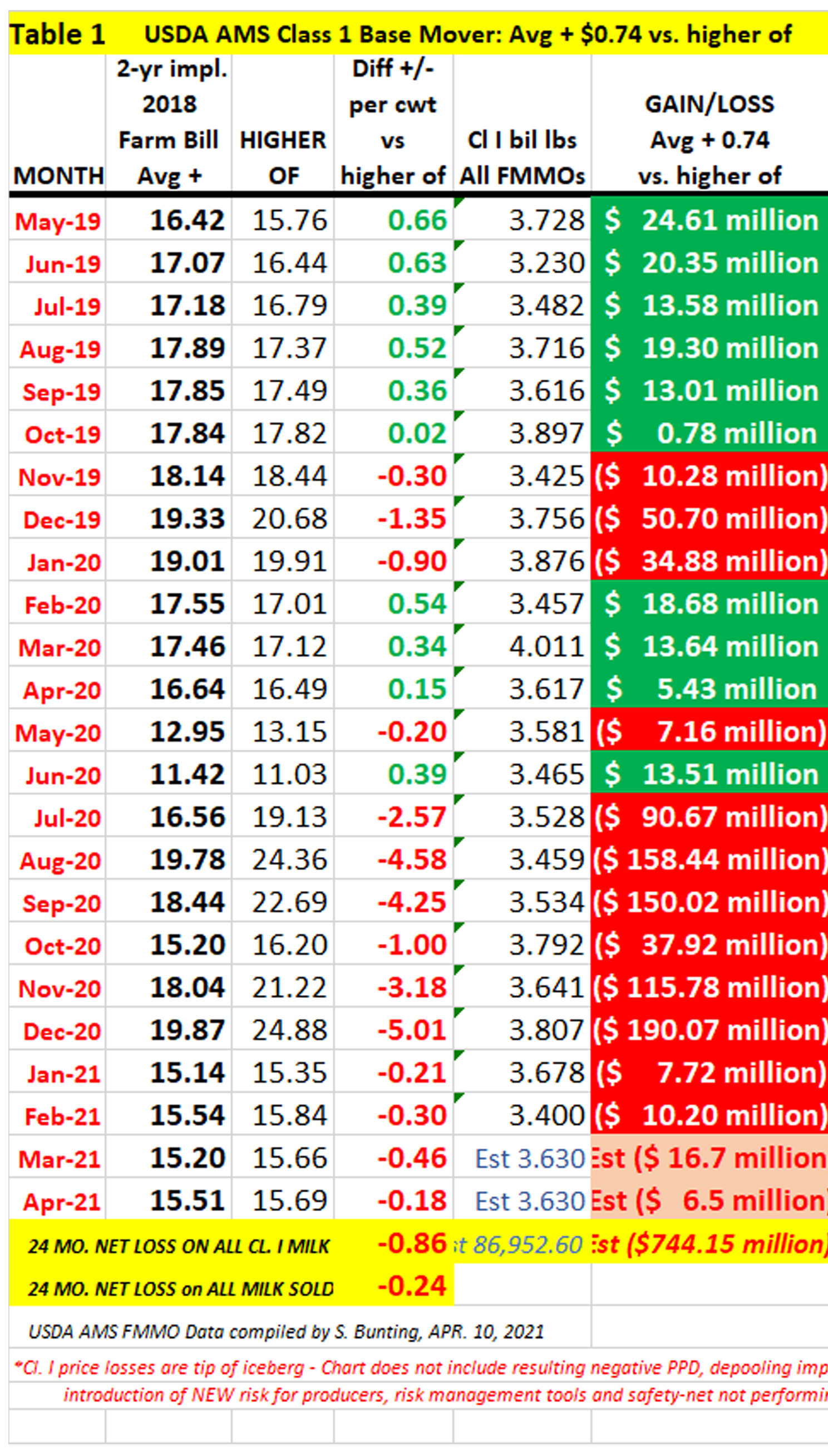

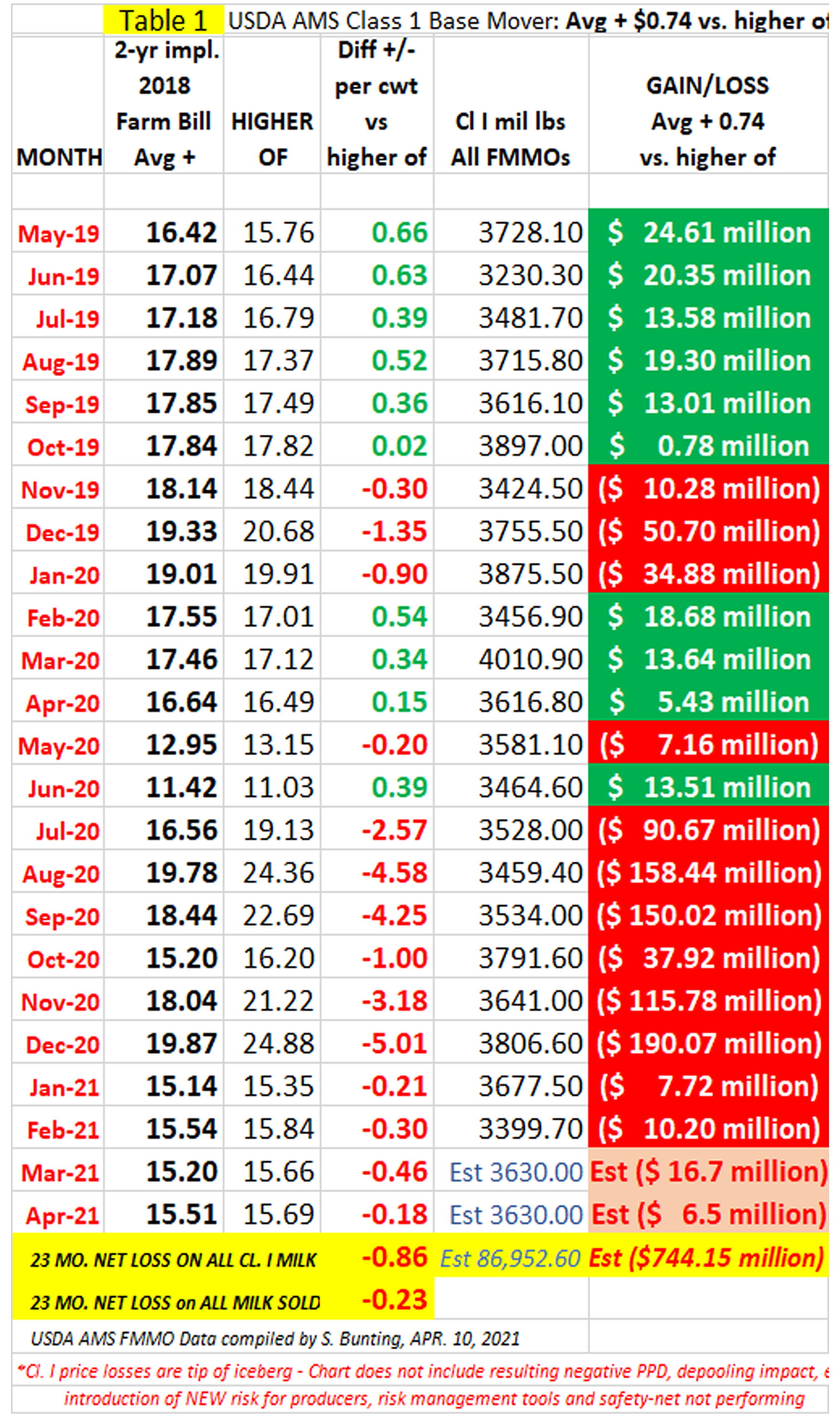

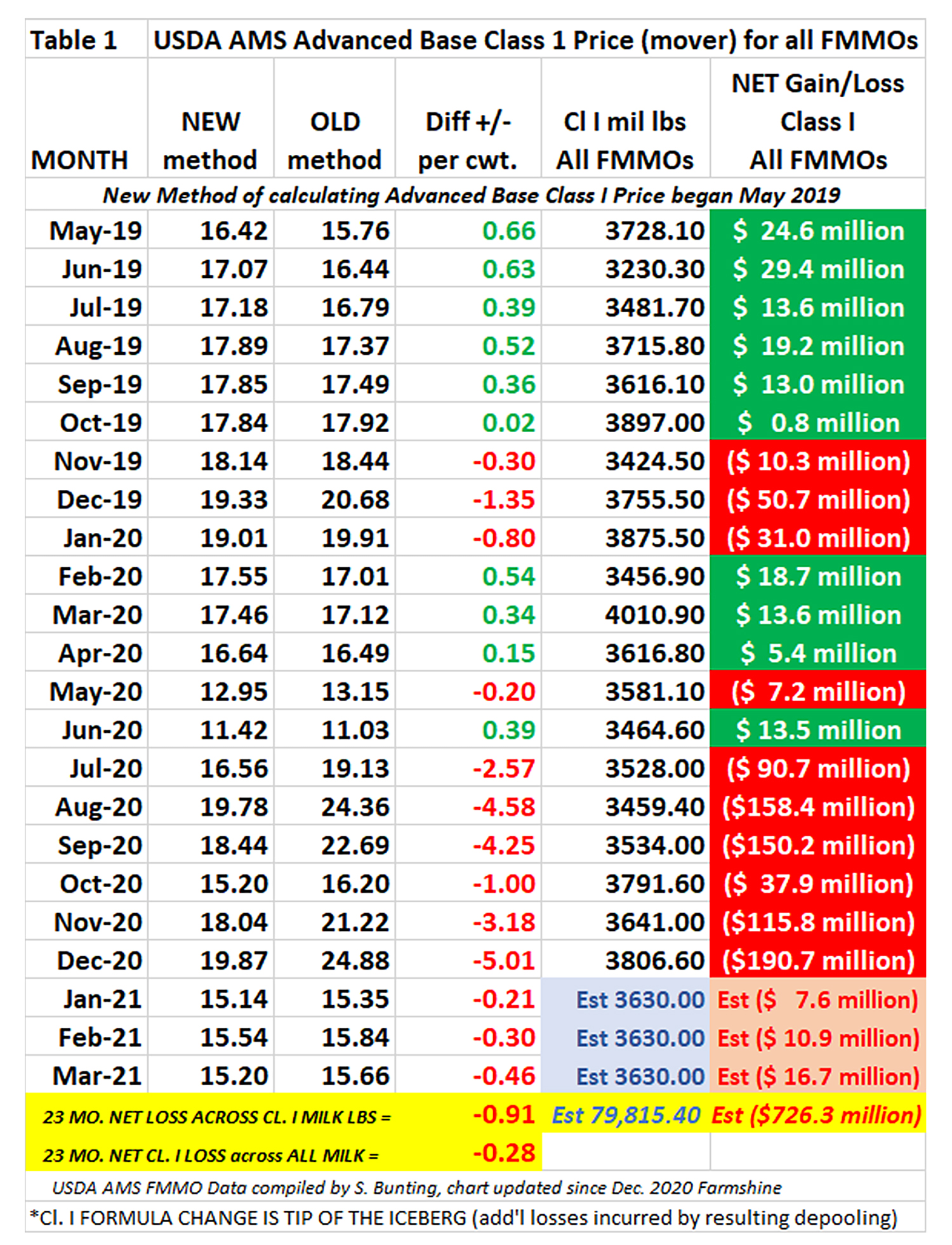

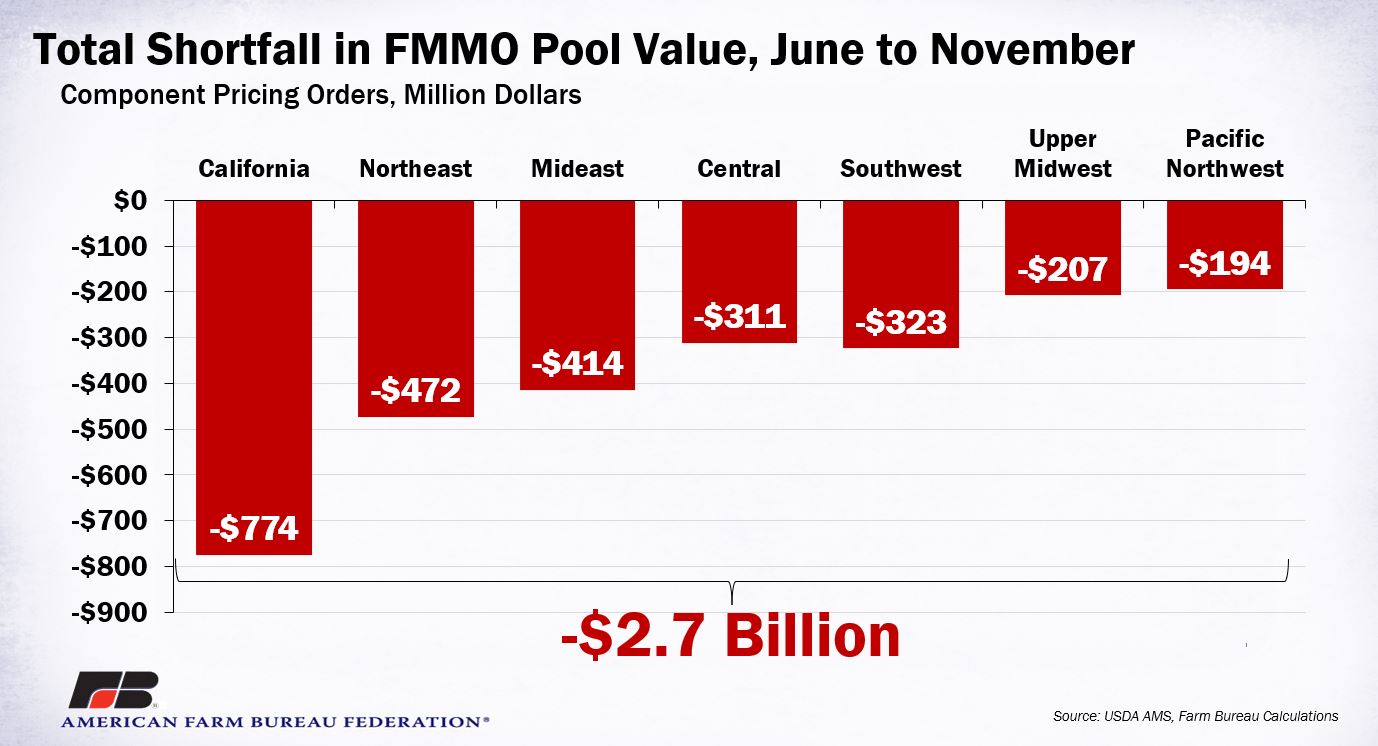

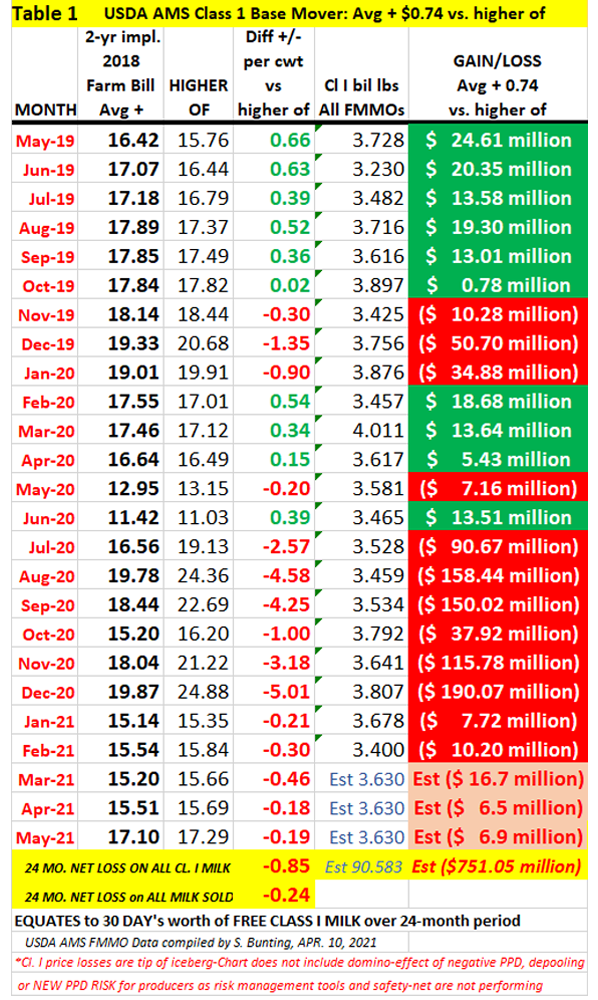

Dairy groups are working to raise awareness among key lawmakers and USDA about the 24-month net loss of over $750 million in the Class I mover price from May 2019 through April 2021. In addition, these losses impacted orderly marketing and other factors, contributing to net losses exceeding $3 billion nationwide from inverted class price relationships that produced negative PPDs and led to depooling. In addition, dairy farmers had risk management losses when their milk was devalued, but they paid for risk management that failed because it was aligned with a “market value” they did not receive.

Sen. Gillibrand’s letter highlights the concern about the unintended consequences of the Class I formula change to averaging and away from ‘higher of’.

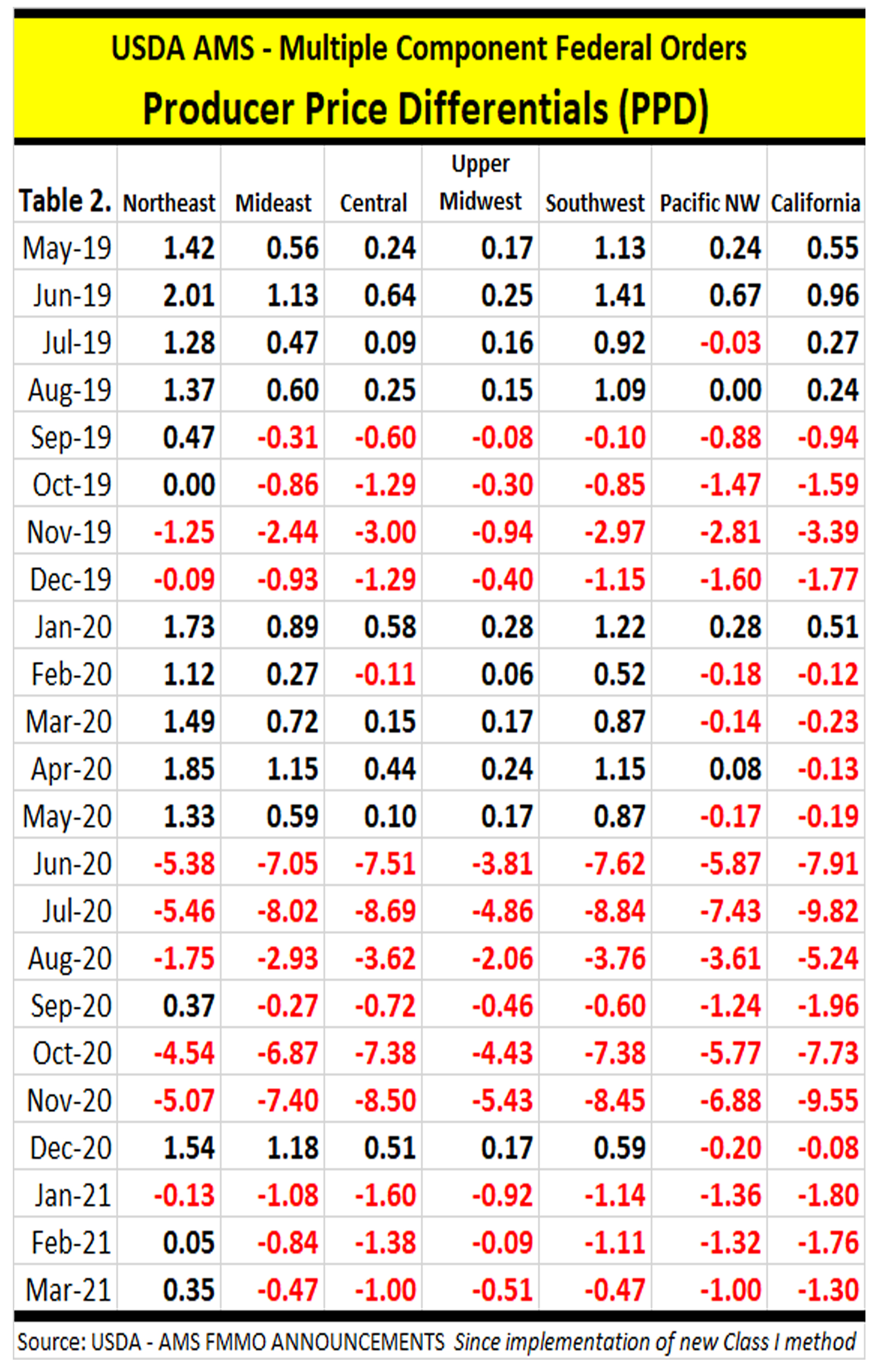

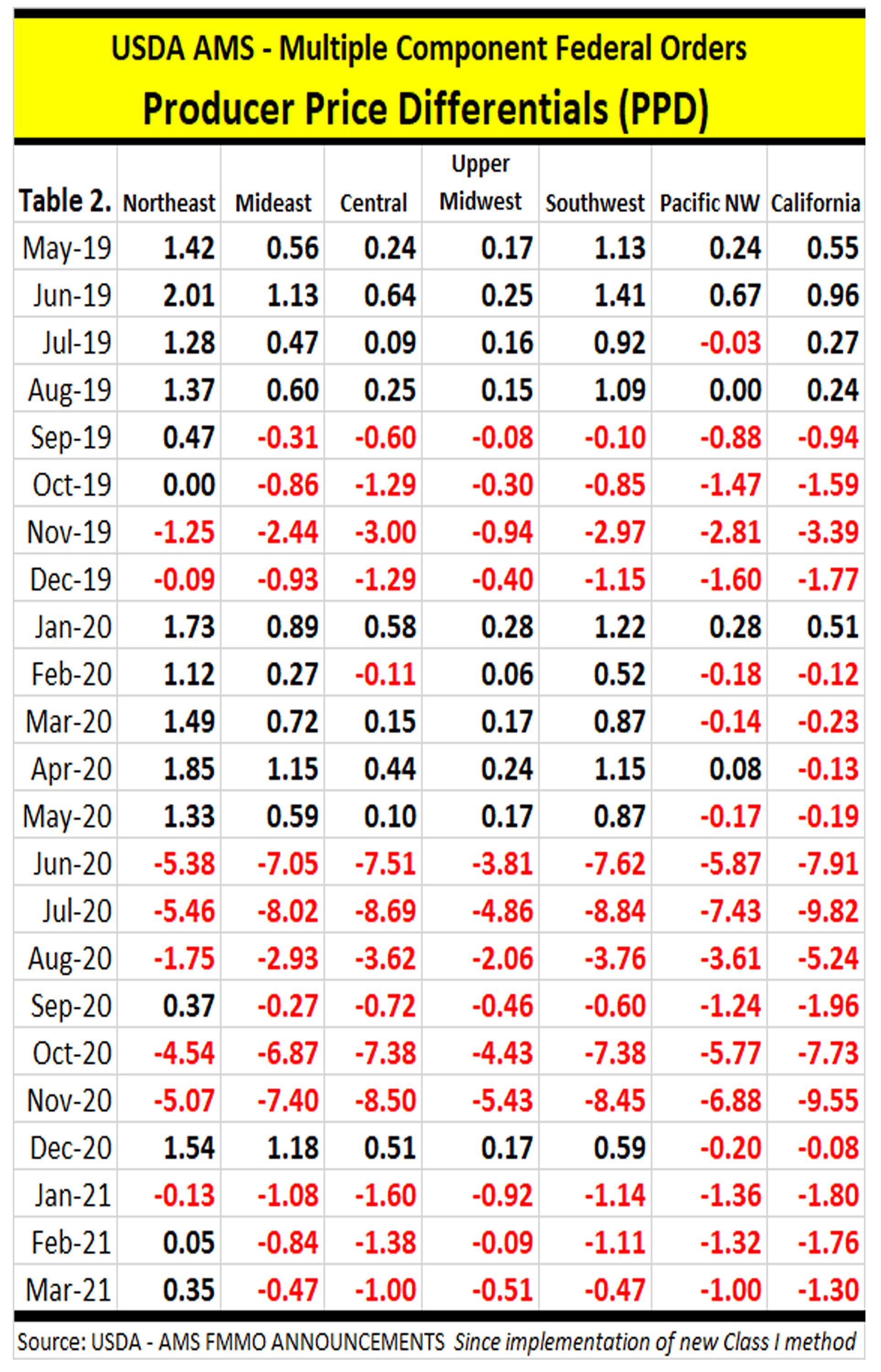

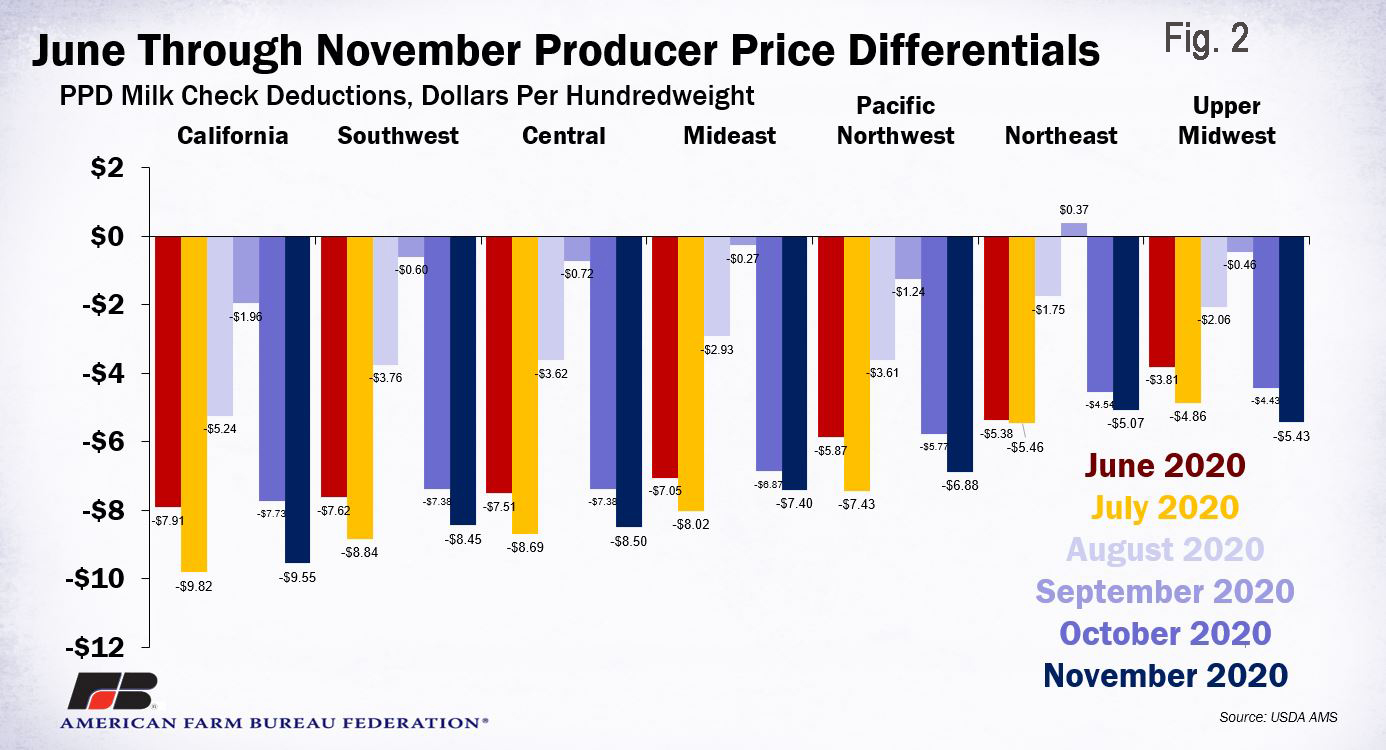

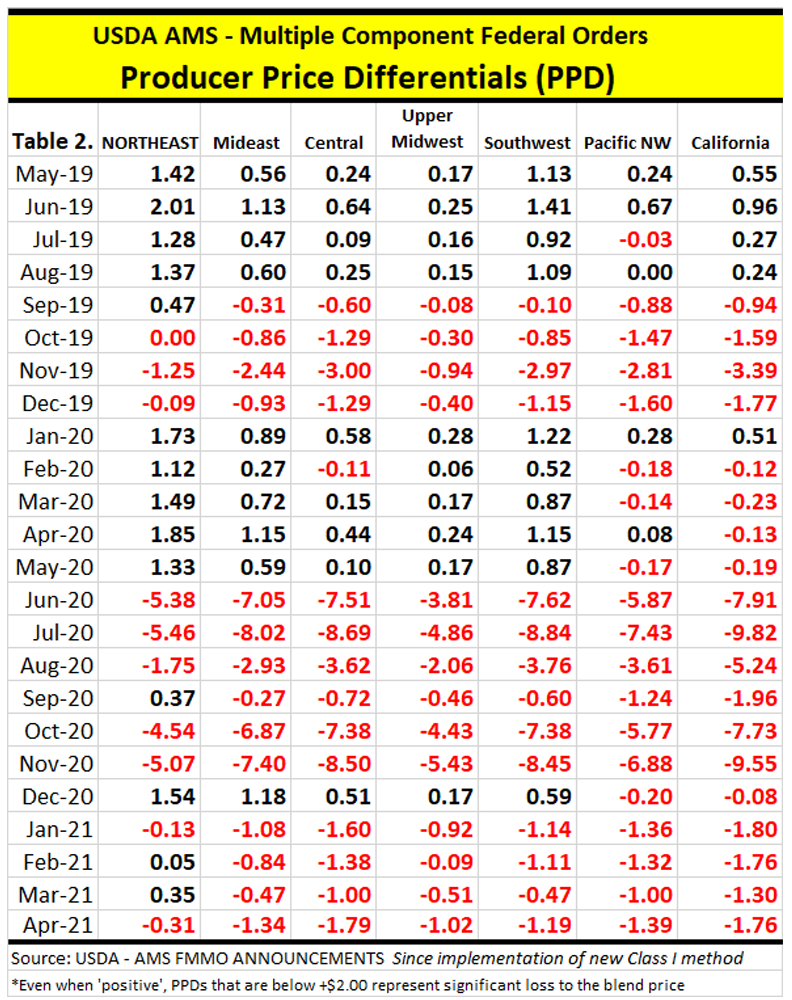

In the Northeast FMMO 1, for example, the Class I change, alone, accounted for a net loss of over $160 million in Class I devaluation over 24 months, and there were broader impacts of basis losses from reduced and negative producer price differentials (PPD) and depooling.

Northeast producer blend price losses are estimated to be $1.10/cwt, net, from May 2019 through April 2021. (Calculations are being done for other FMMO regions so stay tuned.)

Similar loss estimations can be made for broader impacts across the U.S., depending upon how cheese plants determined pay prices for farmers when the FMMO uniform blend prices were suppressed by $1 to $10 across 7 of the 11 FMMOs that report producer price differentials. These PPDs were severely negative from October through December 2019 and from June 2020 through April 2021.

These formula-related losses are expected to continue through most of 2021 due to current market factors affecting how the class pricing formulas, with the change to Class I, relate to each other and how this impacts depooling.

Producers from the Southeast U.S. also began circulating a letter to Secretary Vilsack this week highlighting the steep losses in the three Southeast FMMOs and seeking direct payments through Coronavirus stimulus funds.

The Southeast letter asserts that milk producers in FMMO 5, 6, and 7 (Appalachian, Florida and Southeast) disproportionately bore 21% ($155 million) of the lost revenue directly attributable to the Class I mover change, because the 21% of Class I value loss fell on dairy farmers shipping just 5.5% of total milk pooled across all orders in the U.S.

Southeast producer blend price losses are pegged at $1.25/cwt.

The Southeast letter states that the loss was not shared equitably among all dairy farmers, due to depooling, which the letter indicates made it possible for dairy farmers marketing milk to cheese plants (Class III) to receive the shortfall.

However, many producers whose milk was depooled from FMMOs did not receive that shortfall from milk buyers, unless they had milk contracts based directly on cheese prices. Many manufacturing class handlers use the FMMO blend price as the benchmark for paying producers outside of pooling.

Several industry sources observe that this change turned out to be a big benefit to processors at great expense to producers. The problem surfaced under market conditions before the pandemic and was made worse by market conditions since the pandemic.

Even National Milk Producers Federation (NMPF) has admitted as much, stating that the International Dairy Foods Association (IDFA) wanted this change in the first place. NMPF indicates they went along with it after studying some historical trends thinking the 74-cent adjuster to the average would produce a result that was “revenue-neutral” for dairy farmers.

It was anything but ‘revenue-neutral’ for dairy farmers, even before the pandemic. The pandemic impact simply magnified the severity of loss.

Proposals continue surfacing since NMPF announced its intention to seek a USDA emergency hearing with a proposal to tweak the adjuster to the average every two years.

Minnesota Milk Producers, Wisconsin Dairy Business Association, Edge Cooperative and the Nebraska State Dairy Association joined together with a concept to change the Class I mover to a Class III-Plus that would be based on Class III announced prices instead of advance prices.

FarmFirst Cooperative based in Madison, Wisconsin, announced it would put forward a proposal to return to the ‘higher of’ calculation — if USDA holds a hearing. However, to-date, no official FMMO hearing requests have been received by USDA.

The first few months of the new Class I mover formula in 2019 were net-positive to the Class I price, but this dissolved by July, almost a year before the pandemic, when the gap between the rising Class III price and the averaging method for the Class I mover narrowed because the spread between Class III and IV widened.

Government food box dairy purchases through the pandemic included more Class III products (cheese) than Class IV (butter/powder) or Class II (soft products that are priced by Class IV).

But food boxes included plenty of Class I (fluid milk). Trouble is, fluid milk is not ‘market valued’ except for the value of its components in manufacturing. Fluid milk is discounted as a ‘loss-leader’ by large supermarkets, especially those that process milk.

Another factor that contributed to the wide spread between Class III and IV pricing has been the difference in product inventory as a factor of production, exports and imports.

In 2020, butter inventory reached a 20-year high, while cheese inventory declined. Butter production increased, especially in the first half of 2020, to exceed the record-breaking production of 2018, making less cream available for cheese production. Meanwhile, cheese exports rose 16% while butter exports declined 5%.

On the flip side, cheese imports declined 10% while butter imports were the second largest on record, up 15% over the previous year for the first 7 months of 2020. The U.S. ended 2020 with butter imports 6% above 2019.

The Class I formula change made FMMOs even more vulnerable to massive depooling against this volatile and divergent backdrop of Class III vs. IV. As averaging reduced Class I pricing, and the Class III milk was depooled, the net result was blend prices that reflected a larger portion of the much lower Class IV (and II). Dairy farmers have been educated to produce milk with higher component levels of fat and protein as a method to improve profitability, but negative PPDs snub this value at the farm level.

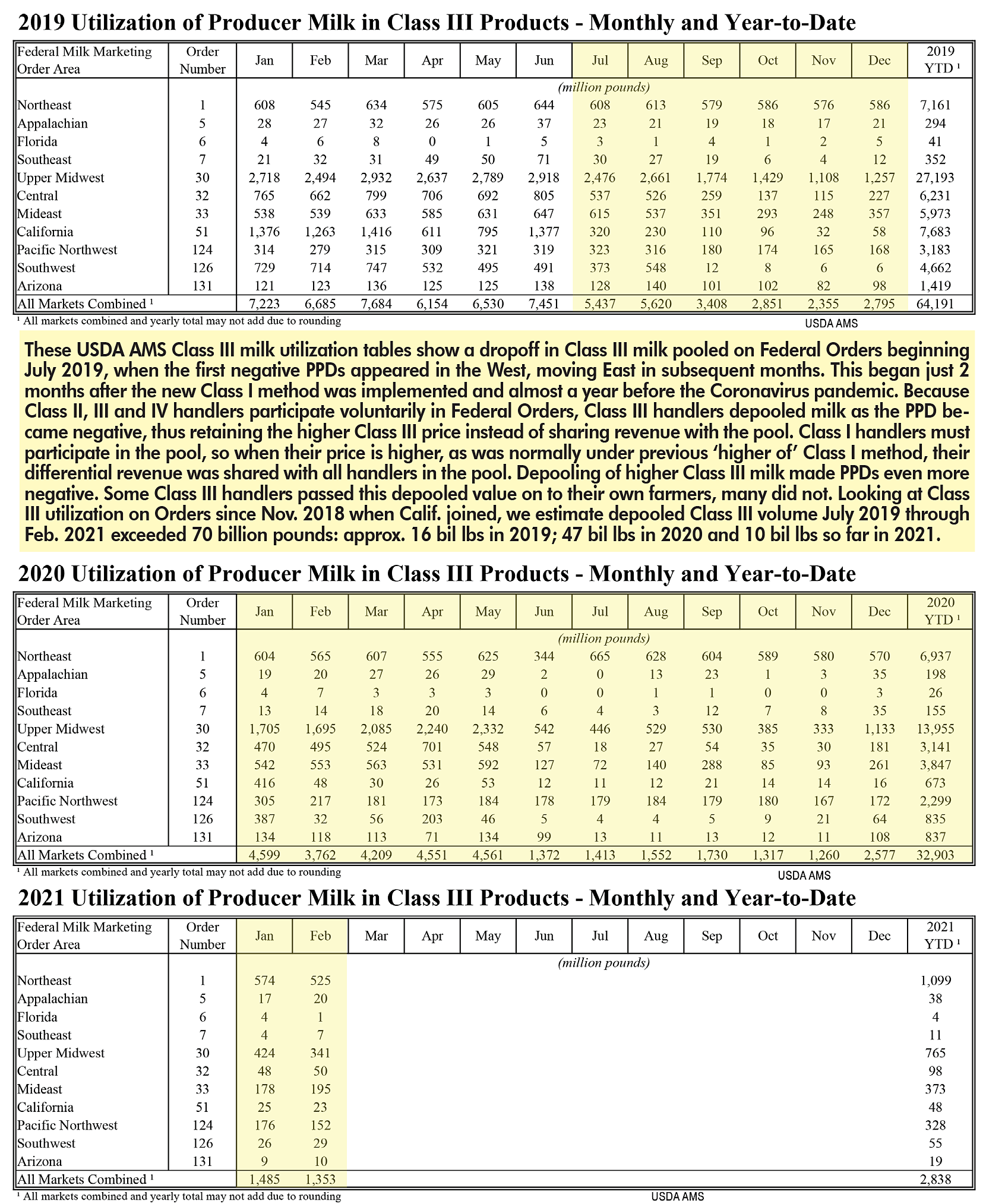

Looking through USDA Federal Milk Marketing Order statistical bulletins, this reporter calculates over 70 billion pounds of milk were depooled across all FMMOs from July 2019 through March 2021 due to inverted class pricing.

The depooling of Class III milk and the negative PPDs (above) began on the West Coast in July 2019. By September through December 2019, all multiple component FMMOs had negative PPDs, that became more negative as volumes of depooled milk were noted in the central part of the country, moving east.

The four skim/fat pricing FMMOs in the Southeast and Arizona were quite negatively affected by lower Class I minimums in the fall of 2019 and for many of the months thereafter. Topsy-turvy All-Milk and Mailbox Milk prices reported by USDA are further proof of shrinking basis in producer milk checks affecting the performance of purchased risk management tools. Even those USDA-reported All-Milk and Mailbox prices do not tell the whole story because USDA states that “the value is in the marketplace” even if it is not equitably shared with producers.

In essence, the Class I mover change was made to give large global companies buying large volumes of milk a means of ‘hedging’ their risk through forward-contracting on the futures markets. But this ‘benefit’ has resulted in taking real money out of dairy farm milk checks and has made it difficult, in some cases impossible, for producers to manage their risk with tools they purchase in the marketplace and through USDA.

Interestingly, the nation’s largest Class I fluid milk company — Dean Foods — filed for bankruptcy sale and reorganization in November 2019 in the midst of the first appearance of negative PPDs and depooling pre-pandemic.

By January 2020, PPDs turned positive but narrow in comparison to prior history, so that’s still a loss. Then, in February, a month before the Coronavirus shutdown, negative PPDs and depooling again showed up in the Central, Pacific and California FMMOs.

By June 2020 — in the midst of the Covid-19 pandemic and one month after the bankruptcy sale of most of the Dean Foods Class I fluid milk plants to DFA — severely negative PPDs of -$1 to -$10, exacerbated by depooling, were prevalent across all FMMOs, most every month from June 2020 through the present.

Even in the Northeast FMMO, where statistics show positive PPDs in some months when other FMMOs were negative, the basis loss to Northeast producers is real because even the positive PPDs in FMMO 1 over the past 24 months are $1 or more below where they were just two years earlier.

As reported in Farmshine last week, Secretary Vilsack says it’s “complicated” and the industry is “divided” so no “significant” changes can be made “quickly.”

NMPF says it intends to request an FMMO hearing of its proposal to adjust the adjuster to improve equitable treatment of producers.

IDFA is publicly silent.

Other groups are floating a proposal that, if officially proposed in an emergency hearing, would turn the deal into a full and lengthy FMMO hearing.

During a Hoards Dairy Livestream session May 5 with Erin Taylor from USDA AMS Dairy Division, a little more was learned about how USDA handles ‘emergency’ FMMO hearings. Taylor said proposals can be put forward with arguments as part of the package, explaining the emergency to make a case for why the USDA should move quickly. USDA then typically responds and gives the industry a 30 day notice if a hearing is granted, but the statute only requires 15 days, and 3 days at a minimum — depending on the emergency conditions.

Like other FMMO hearings, testimony is taken, and if USDA agrees with the proposal based on the evidence, the department could do a recommended decision, receive public comment and then publish a final decision and conduct the producer vote. Or, the Secretary can do a tentative final decision for immediate producer vote while taking testimony concurrently. In such a scenario, USDA would come back and consider that testimony, and if a change to the tentative final decision is made — based on testimony and comment — then a second producer vote would be conducted.

Generally speaking, according to Taylor, a move to use a tentative final decision cuts about 4 to 5 months out of the hearing process, but this is not done without proponents showing good cause and when there is no opposition to the proposal.

And the Congress? They made the change from ‘higher of’ to ‘average-plus’ at the request of IDFA with agreement by NMPF in the last Farm Bill.

Many members of Congress don’t know what they did. Others are “blowing it off” as “pandemic-related,” when in reality the issues began in 2019.

Lawmakers are also being told the 2018 ‘average-plus’ deal was an historic agreement between “producers” (NMPF) and “processors” (IDFA), when in reality the grassroots in either of those categories had no opportunity to be heard, to testify, to comment, and producers were denied a referendum on the change. In addition, there was little industrywide discussion.

National and state dairy organizations have been collaborating on weekly calls facilitated by American Dairy Coalition to thoughtfully approach a solution from both the short- and long-term perspectives.

While most would agree hearings on long-term FMMO reforms are needed, the short-term fix for the unvetted Class I formula change by Congress could be undone with legislation reverting to the previous formula, or through an expedited FMMO hearing as the flaws of the new formula have been revealed in both the pre- and post-pandemic markets by this average-plus change that was not vetted.

Grassroots efforts seek to raise awareness in Congress to move something forward legislatively.

While the Congress has always said it does not want to set precedent for making milk price formula changes outside of the vetting process of an FMMO hearing, and while the Congress rebuffed numerous requests for a national FMMO hearing in every Farm Bill since 2008, the Congress did go ahead and set that formula-changing precedent in 2018 by passing language in the Farm Bill to change the method for determining the Class I mover from the ‘higher of’ Class III or IV to ‘average-plus’… and here we are.

Producers can point this out when talking with lawmakers, to let them know that the current situation is unsustainable. Producers can explain to their legislators how this impacted them, to help them understand there is more to this story than “it’s the pandemic and you’ll be fine.”

If nothing is done, several industry observers see dairy farm exits rising at a faster rate in the coming year.

In short, the Class I mover change in the 2018 Farm Bill:

— was not vetted through a transparent hearing process,

— disrupted orderly marketing,

— undermined Federal Order purpose,

— created NET losses for producers of $751 million in Class I value (May 2019 through April 2021), and contributed to a net loss of over $3 billion in negative PPDs and depooling,

— created additional losses for producers in the failure of risk management tools not designed for inverted pricing, and

— undermined performance of the DMC safety net due to basis loss.

While the American Dairy Coalition continues to facilitate grassroots producer discussion and seeks a seat at the table for producers with NMPF and IDFA, ADC has also sent an email to dairy producers and organizations with a letter they can provide to lawmakers.

The most important thing is for lawmakers to understand how the pricing change, and the domino effect of negative PPDs and depooling have affected their already struggling dairy farm constituents over the past two years.

To locate the Senators and Representatives for your state, visit https://www.govtrack.us/congress/members