Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

35 dairy farmers, industry representatives, and farm media attended “Winners and Losers: a discussion about USDA’s proposed milk pricing reforms,” hosted by the American Dairy Coalition during the 57th World Dairy Expo in Madison, Wisconsin October 3rd.

By Sherry Bunting, Farmshine, October 11, 2024

MADISON, Wis. – “I’m in Wisconsin, and on the graph (below) it looks like producers in Order 30 are having to decide between less money with an Order or even less money without an Order. Am I wrong and is there a silver lining?”

That was the crux of the question one dairywoman asked during the American Dairy Coalition’s (ADC) ‘Winners and Losers’ seminar and press conference Oct. 3 at World Dairy Expo. Over 35 farmers, industry representatives, and media professionals gathered to hear insights about USDA’s recommended decision on changes to Federal Milk Marketing Order (FMMO) price formulas.

American Farm Bureau economist Danny Munch was the invited presenter, followed by time for questions, moderated by Kim Bremmer of Ag Inspirations, and opportunities for networking and farmer-to-media connections during the remainder of the two hours.

Dairy farmers attending ADC’s press conference gave interviews after the discussion on USDA’s proposed milk pricing changes.

At issue was the impact on FMMOs with more cheese and less fluid milk, that would experience the negative impacts of a proposed hike in processor make allowances without the positive buffer of higher Class I location differentials.

Bremmer said over 126 individuals and organizations provided comments to USDA. The comment period ended Sept. 13.

During his visit to Expo on Oct. 4, Ag Secretary Tom Vilsack said USDA would issue a final decision in mid-November. Also on Oct. 4, USDA held a webinar explaining the producer referendum expected in January. (Look for more specifics in a future Farmshine, and check out the Farm Bureau recap here)

The short answers to the above question appear to be yes, yes, and yes. With an Order, producers in some regions will see lower FMMO blend prices. Without an Order, they would lose minimum prices altogether and other important FMMO functions.

The silver lining? Munch pointed to better competition currently for milk, and he sees opportunity for milk in the future as consumers focus on protein.

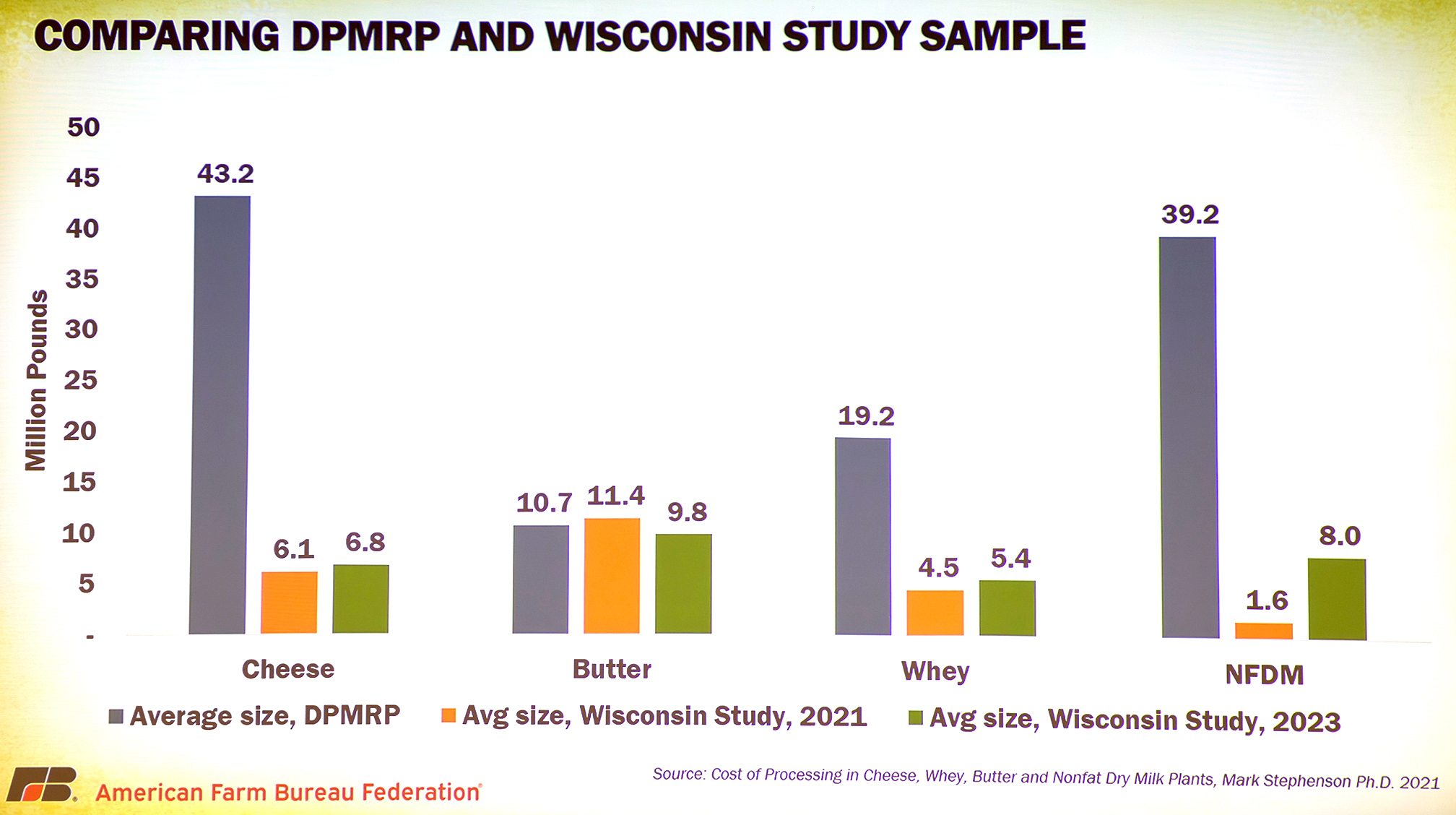

New to the discussion was make allowance data compiled by AFBF for its official comment at the Federal Register showing the average plant size of processors participating voluntarily in the Stephenson Survey relative to the average plant size of processors reporting to the NASS Dairy Product Manufacturing Survey (below)

The average size and volume of the plants in the voluntary cost of processing survey is 5 to 20 times smaller than the size and volume of plants reporting to USDA on price and production. This is further evidence that mandatory surveys are the only fair way to examine and set make allowance levels.

ADC reports that farmers have called with questions and concerns about the FMMO changes they will vote on. Part of ADC’s mission is to inform dairy farmers and help them understand factors like this that affect their businesses, said Bremmer.

For example, it’s helpful for farmers to realize that current make allowances equate to $2.17 to $3.17 per hundredweight in deductions already in the pricing formulas to cover the cost of converting milk to butter, cheddar cheese, nonfat dry milk, and dry whey.

The proposed new make allowances add 70 cents to $1.00, depending on class utilization, bringing the total deduction to about $2.89 to $4.07 per hundredweight, maybe more.

The splitting of Class I into a two-mover pricing system is also causing discontent and concern. On the one hand, USDA would restore the ‘higher-of’ method for conventionally pasteurized fluid milk but use an ‘average-of’ method with a rolling and delayed adjuster for the extended shelf life (ESL) fluid milk products. This new milk class was not vetted nor defined during the hearing.

Also of concern is the delay in implementing positive updates to milk composition standards that have not been updated since Order Reform in 2000.

USDA’s recommended decision applies to all 11 FMMOs nationally but will be voted on by eligible (pooled) producers in each Order, individually.

A two-thirds ‘yes’ vote within each individual Order continues that Order with the changes. If the two-thirds threshold is not met by either producer numbers or volume in an Order, then the result is termination of that Order.

Producers do not have the option of voting separately on the five pieces of the USDA decision, nor do they have the option of voting to keep the FMMO pricing formulas as they are currently.

Economists with National Milk Producers Federation have stated previously that 65 to 70% of the U.S. milk supply is marketed through cooperatives that tend to bloc vote for their producers, but this percentage can vary on an individual Order basis.

USDA determines voting eligibility, based on whether milk was pooled in the reference period selected by each Market Administrator.

“When we get down the road to the vote, and if we vote ‘no,’ that will dissolve the Order, right?” asked one dairy farmer. “What opportunity does any geography have to reorganize a new Order to fit what works for them?”

Munch said producers could start a process to create a new Order, but it would still be required to use the same price formula rules because these will apply to ALL Orders uniformly. In contrast, he noted that USDA leaves pooling and depooling rules to be decided individually by each Order.

One member of the media pressed Munch to speculate on what happens if a western Order votes no, but an eastern Order votes yes?

“People always want me to speculate on what happens if California or the Upper Midwest vote out their Order(s). What we’ve seen in the past in unregulated areas, or areas with state orders — they still base a lot of their pricing on the nearby Federal Order system,” he responded.

“If we remove more milk out of the Federal Order system, does that system then play less of a role in pricing milk, and does that unregulated market start to dictate and suck milk out of the regulated areas, if you’ve taken out some of the large milk production states? That’s just some speculation, something to think about in the long term,” he said.

On a more immediate basis, Munch said that if an Order is terminated by this vote, “farmers lose protections like timely payments and component verifications, and the minimum prices. You could end up with a patchwork.”

He pointed out that USDA did not raise make allowances by the full amount requested by processors, but also did not go with the more modest increases requested by the cooperatives.

In their post-hearing comments, processors voiced great unhappiness with the decision, he said, because they didn’t get the multi-year increases to even higher levels.

“We don’t blame USDA for trying to come up with a middle ground… we just don’t have the data. The way hearing processes work is they collect this data brought by stakeholders and try to come up with a compromise that works for everybody,” Munch explained. “Our argument is that the data may not reflect market conditions, and we want to make sure that it does. We can’t get that assurance until there’s an audited, mandatory survey.”

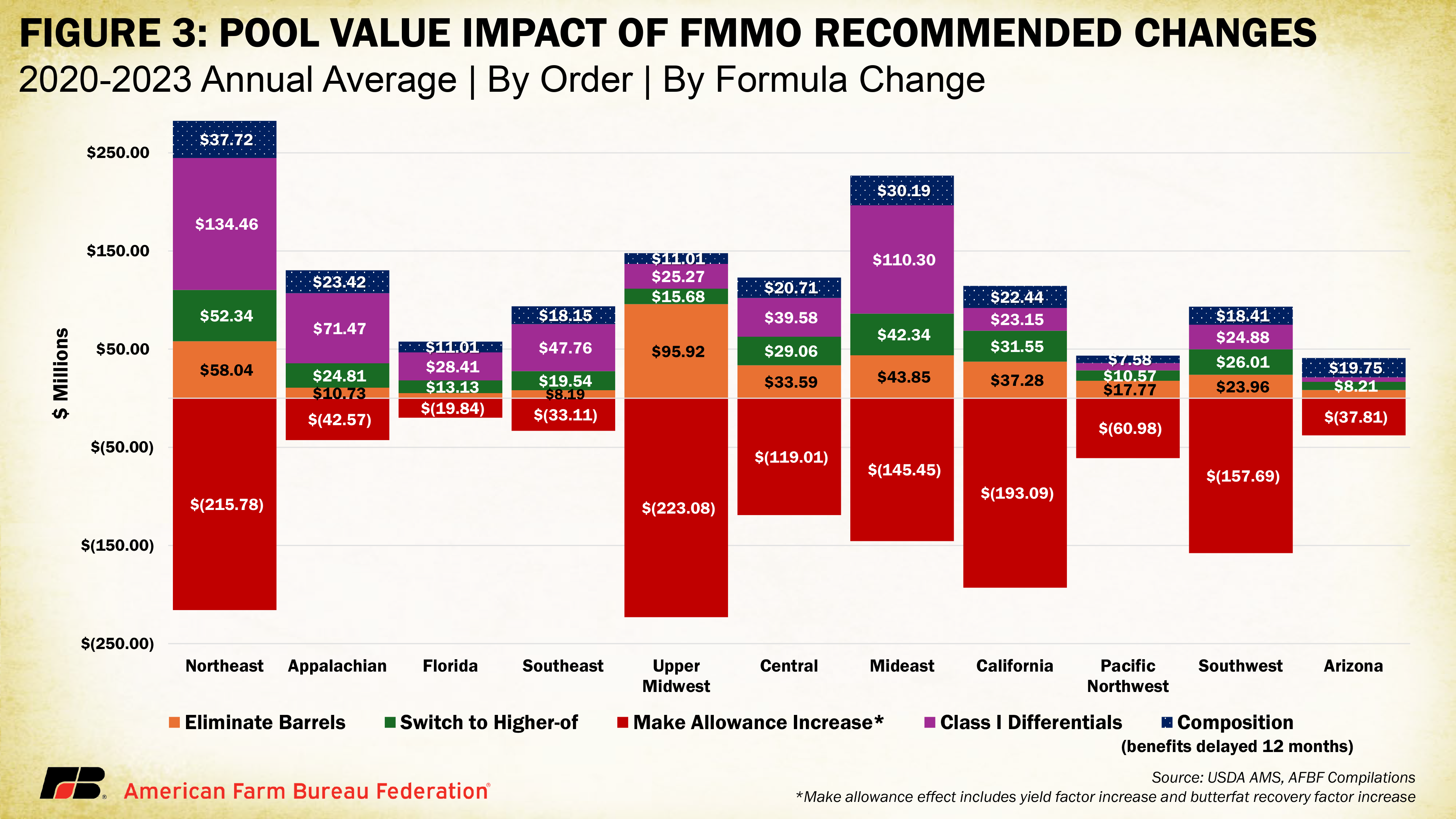

As a standalone piece, AFBF estimates that USDA’s proposed increase in make allowances would remove an additional $1.25 billion annually from producer pool revenue, nationwide, based on past pooling data. However, USDA proposes a one-year delay in implementing the milk composition updates that would contribute $200 million annually in producer pool revenue nationwide.

Munch sees the 12-month delay in implementing the milk composition standards and the splitting of the Class I mover with an ESL adjuster as two things that appear to be “thrown in there,” with a lot of groups voicing discontent and confusion.

When asked by a reporter if the add-ons to Class I will create consumer resistance to what could be a 25-cents-per-gallon increase in retail fluid milk prices, Munch cited the hearing record where economists testified to the relative inelasticity of fluid milk demand.

He also sees great opportunity for milk: “When I go to the gym, I used to see no one drinking milk. Now I see tons of people drinking milk, protein shakes, and other things, and it’s not plant-based products. I think milk can take advantage of marketing the protein benefits that people in my generation are looking for and are willing to pay for.”

Munch was asked if AFBF will recommend how its dairy members should vote.

“We will not make that recommendation. We take positions based on our policy, which includes opposing any make allowance updates until we have mandatory cost of processing surveys, and other aspects related to our policy book,” he replied. “It’s up to our members to make those voting decisions, and there is a regionality to this, so we don’t get involved at that level.”

Florida producers, for example, “will be okay with the new rules” because the over 80% Class I utilization brings with it higher location differentials. The Upper Midwest, on the other hand, has been at roughly 5% Class I and 93% Class III, so there is very little benefit from the Class I changes, but those producers are subjected to the highest make allowance deductions for Class III products, which is 95% of their blend price.

‘We need to figure outa way to get farmers’ voices incorporated into this discussion’

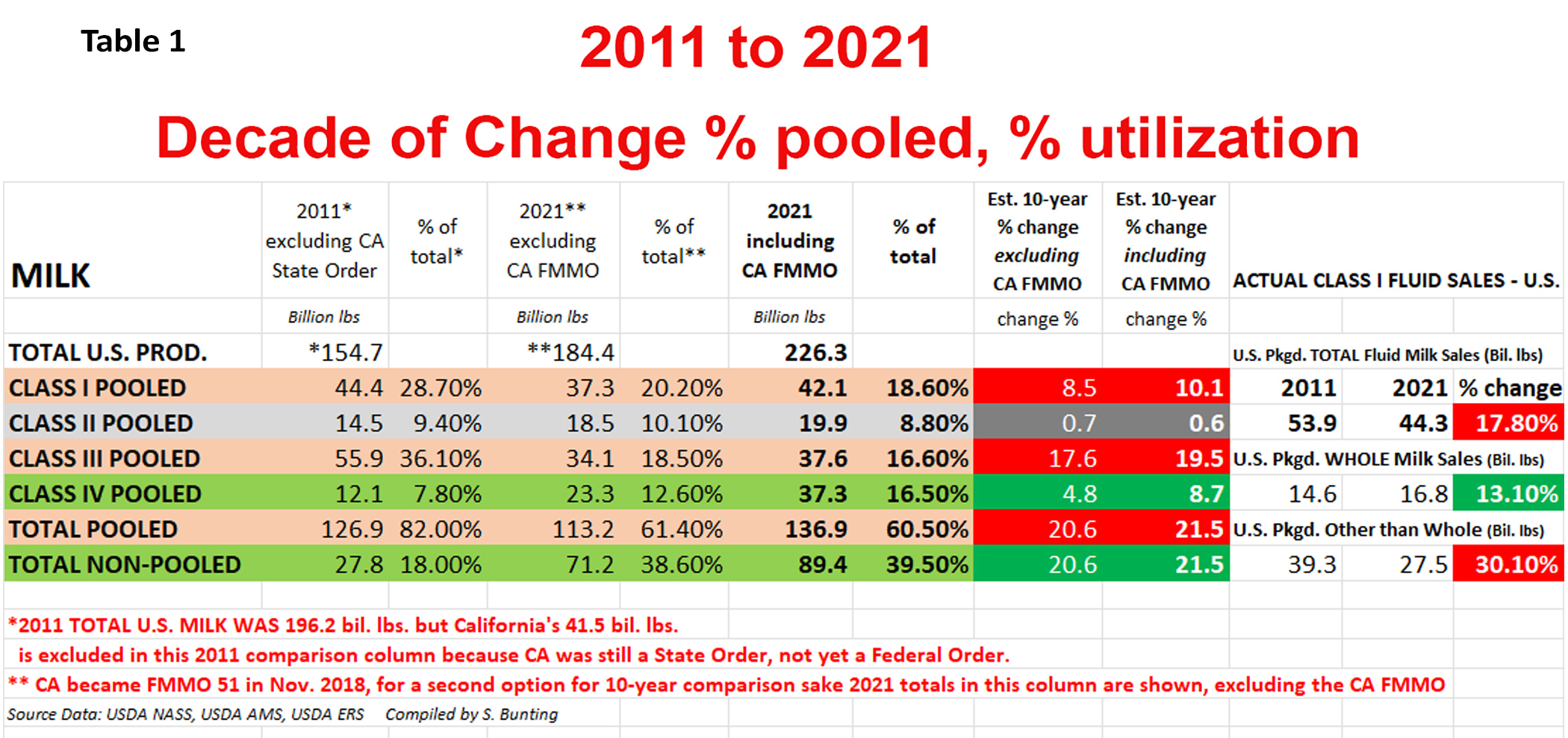

Table I reflects a decade of change in FMMO participation as total U.S. milk production grew 13.3% from 2011 to 2021, and the percentage of milk pooled on FMMOs fell from 82% in 2011 to 60.5% in 2021. California became an FMMO in 2018 after previously being a state order, so California’s production is not included in the 2011 pooling comparison so the pooling percentages are relative to production in FMMO and unregulated regions. Class I pounds as a percent of total production fell from 28.7% in 2011 to 18.6% in 2021. Figures for 2021 are shown both ways, including and excluding California to compare to 10 years ago when the number one dairy state had its own state order with different pooling and classification rules and incomplete data, but the percent of change is nonetheless eye-opening. Chart compiled by S. Bunting

By Sherry Bunting, published in Farmshine, Feb. 18 and 25, 2022

GREEN BAY, Wis. — Do dairy farmers want to save the baby, save the bathwater, change the flow of the bathwater, or tighten the plug on the drain before the bathwater drains to the point of taking baby with it?

That’s a brutal take after 90 minutes and a lot of information, starting with the basics and hearing perspectives and questions during the American Dairy Coalition’s Future of Federal Milk Pricing Forum on Feb. 15.

It was a first step in what ADC sees as a continuing conversation and effort to engage dairy farmers to lead the process. They said the next forum will be in March.

Geared specifically for dairy farmers, the forum attracted 160 participants from across the country, representing every element of the dairy industry — including dairy farmers.

The virtual format was moderated by Dave Natzke, markets and policy editor with Progressive Dairy magazine. Featured presenters were Calvin Covington, retired co-op COO with 45 years of experience in federal and state marketing orders; Frank Doll, a third generation Illinois dairy farmer involved in American Farm Bureau’s dairy policy committee, and Mike McCully, industry consultant on the IDFA dairy ingredients board and economic policy committee.

Included were comments presented by attendees, who pre-registered for three-minute slots. Others typed into the queue.

“This is complicated, and many people say it can’t be fixed, but we have a great amount of expertise and value here. We covered a lot,” said Laurie Fischer, CEO of ADC at the end of the forum. “We can’t just let this drop. We need to continue to move forward.”

“We heard a lot of good information that has everyone’s wheels turning,” added ADC president Walt Moore of Walmoore Holsteins, Chester County, Pa. He encouraged producers to reach out and engage to tackle the hard topics.

The goal of this initial forum was to inform dairy producers on the Federal Milk Marketing Orders (FMMO) and pricing process to become engaged and have a greater voice in guiding future policies.

For its part, American Farm Bureau Federation spent the past couple years going through a similar working group with policy recommendations coming from states to national and back to states.

Several commenters concurred with the position of ADC, Farm Bureau and other organizations that Class I pricing should return to the ‘higher of’ method until future policies can go through what could be a long hearing process of potential revision for the future.

In fact, one eye opener during the Forum was Doll’s confirmation that Farm Bureau policy now includes support for going back to the ‘higher of’ — plus adding 74 cents — in the calculation of the Class I mover price, while remaining open to other ideas.

Doll said consensus was hard to find in the Farm Bureau working group of 13 members from across the country due to regional differences in the makeup of processing. But general recommendations found agreement, including the reference to Class I as well as modified bloc voting where co-ops can vote for their members on Federal Orders, but farmers can cast their own votes and be encouraged to do so.

Several attendees cited the need for a vehicle for producers to have real input without fear of retribution, that farmers should collectively ask questions of their cooperatives, seek better representation and together, hold their cooperatives accountable to represent their interests.

“We need to figure out a way to get farmers’ voices incorporated into this discussion. I hear from producers all the time, but there is fear of retribution, the threat that your milk is not going to get picked up. If you are on a board and speak up, you’re not there very long,” said Kim Bremmer, representing Venture Co-op in Wisconsin, a third-party ‘testing co-op’ qualified by USDA.

She addressed bloc voting, saying: “What’s the point of having a hearing if producers can’t vote? We don’t have great representation from some of the groups that say they represent us.”

Bottomline, said Bremmer: “We have to address how to get more of the producer voice and not just the processor voice — because they’re not the same.”

She asked: “Is it a conflict of interest if you’re a processor and you’re marketing milk and you’re also advocating for producers? I think that’s an important question that needs to be answered. We need to stay engaged in this and be able to ask the tough questions and demand some answers.”

ADC’s Fischer said the organization wants to work with farmers and their state and national organizations to provide a vehicle to bring farmers together and compose a list of pricing policy items to explore further with experts.

One clear change in the dairy industry formed the crux of the discussion: The growth of milk production in the U.S. — in concert with growing export sales and declining fluid milk sales — put export sales volume above Class I volume as a percentage of total milk solids in 2021.

McCully described this as “a seismic change.”

Covington confirmed that Class I sales — as a percentage of total milk production — fell below 20% in 2021. The percentage of Class I milk within the 137 billion pounds pooled on 11 FMMOs in 2021 was about 30%.

Contrary to the widely held belief that FMMOs regulate a majority of the milk, they simply do not. Covington confirmed that the 137 billion pounds of milk pooled on 11 FMMOs in 2021 represents only about 60% of U.S. milk production.

The FMMOs aren’t designed for this direction that the dairy industry is going toward global markets, according to McCully.

He said the world will look to the U.S. as the “go-to market,” claiming New Zealand and the EU are maxed out. He described the “white gallon jug” as being the most prime example of a low-margin commodity and predicted ‘value-added’ products will return more dollars to farmers in the future. These are recurrent themes heard from speakers at winter meetings this year.

(Author’s note: In contrast, current industry-wide discussion on the ‘sustainability’ side is for a ‘stable’ U.S. cattle herd to be an indicator of dairy’s climate neutrality. If exports grow, and the U.S. herd remains ‘stable’, then export milk will have to come from growth in output per cow and displacement of Class I production. One can see how geographic camps can set up, since fresh fluid milk sales are vital to the viability of dairy farms in areas outside of the earmarked growth areas for dairy manufacturing in the Central U.S. — the question is how to bridge it.)

At the same time, dragging feet doesn’t seem to be much of an option.

If dairy policy remains ‘status quo,’ leaving the FMMOs ‘as-is,’ they could eventually cover less and less milk and potentially collapse, according to McCully.

Covington also addressed this, noting that FMMOs “were designed for fluid milk, but today, fluid milk is a minority use. People used to drink their milk, now they are eating their milk.”

McCully noted the need for dairy innovation. He said make allowances have facilitated large-scale commodity plant construction supplied by large-scale farms, suggesting it is these built-in make allowance ‘margins’ that favor commodity production and deter innovation.

“If end-product pricing continues, the make allowances will have to be raised,” he said, citing a new make allowance study “fresh off the press.”

In 2019, USDA commissioned Dr. Mark Stephenson, dairy economist at University of Wisconsin-Madison, to do the study. Stephenson recently announced it is complete and will soon be released by USDA. McCully’s glimpse at the report shows make allowance calculations to be “significantly higher” than the amounts embedded currently in end-product pricing formulas.

Western Pennsylvania dairy nutritionist Harry Stugart offered his concise, data-driven argument that the make allowances be removed from the formula for the ‘advance’ Class I mover price because these make allowances do not pertain to fluid milk. In January 2022, he said they amounted to $2.67 per hundredweight.

Another crucial part of the discussion was how FMMOs actually work and what they do, besides pricing.

Covington gave attendees a primer of key points to think about as discussions move forward. What he shared may be old news to some, but it’s surprising how many people do not know these facts:

— FMMOs are not required by law, they are simply “enabled” to exist by law. This means producers vote to have them (California in 2018) or to terminate them (Idaho 2004).

— Only Class I fluid milk plants are required to be regulated under FMMOs.

— Class II, III and IV plants participate voluntarily, and they tend to do so “when it’s economically feasible.” Rules of participation vary from Order to Order.

— FMMOs establish other things besides minimum pricing for regulated plants. This includes setting payment terms, providing market information and market services such as testing and auditing.

— The last FMMO reform (2000) was complicated and took four years. It was a combination of legislation (1995 Farm Bill) and an administrative rulemaking process.

— Today, there are four classes of milk, but that was not always the case.

— Today, the Class I mover (base price), as well as the Class II, III and IV prices are established to be the same in all FMMOs, but in the past different FMMOs had different mechanisms.

— Cooperatives are not required to pay FMMO minimum prices even if they own regulated Class I plants because cooperatives are viewed by the FMMOs as one big producer and can make their own decisions about distributing the revenue received to their farmer-members.

— Today, over half of the Class I fluid milk plants in the U.S. are either owned by cooperatives or by large retail supermarkets. Over the past 60 years of consolidation, FMMOs have gone from regulating 2250 fluid milk plants in 1960 to just 225 in 2021.

— Cooperatives balance the Class I market at a cost. Excess milk can go to unregulated buyers at a price that is several dollars below the minimum price. Some co-ops run their own balancing plants. These costs can result in paying farmers below minimum price.

“Milk pricing should return a fair cost to producers, processors and retailers. A chain is only as strong as its weakest link,” said Sherry Bunting, speaking on behalf of the Grassroots PA Dairy Advisory Committee. She also highlighted the Whole Milk for Healthy Kids Act, H.R. 1861, explaining how support for this legislation is essential — no matter how milk is priced.

“In the process of working on this legislation, our (Grassroots PA) committee has identified other concerns. It is hard for producers to advocate when even such a simple and good thing as whole milk in schools is rebuked,” said Bunting. “Farmers hear from leaders and inspectors: ‘If we sell whole milk in schools, do you think we can just stop making cheese and other products?’ Or ‘All you are doing is disrupting markets and creating a butterfat shortage.’ Or ‘Be careful what you wish for.’ These are veiled threats.”

Bunting highlighted the need for greater competition, accountability, transparency and timeliness of price reporting.

“Dairy farmers have farms to run, cows to care for, and they become paralyzed by the complexity and lack of transparency in the system and their milk checks. They become overwhelmed and unconfident, even fearing retribution,” she said.

“We have members with attorneys that cannot interpret their milk checks. That has to stop,” said Bremmer. “Why wouldn’t processors want to show farmers what they are paying them? What is the reason? To have attorneys and others looking at it and they can’t figure it out, that’s a real problem. We think they’re probably re-blending some things to make another ‘make allowance’. We know these things are happening all across the United States.”

Payment terms are critical in this conversation. Even the best-made plans for risk management mean nothing if farmers don’t receive timely and consistent payments for their milk due to the high capital costs and cash flow needs of running a dairy farm.

One commenter said farmers want their income to come from consumers, not from the federal government. He wondered why Federal Milk Marketing Orders (FMMOs) are even needed to guarantee payment.

“Why? So you get paid,” replied panelist Covington. “The FMMOs all establish dates when advance and final payments are made. Having been a co-op manager working with fluid milk plants, I can’t emphasize enough how important this is.”

He also pointed out the important auditing, weights and measures, and market information the FMMOs provide.

McCully said these other services provided by FMMOs are “something we need more of going forward. We need less (price) regulation and more (market) information,” he added. “What’s not working is the milk pricing.”

Here’s where the crux comes into play: The FMMOs are not set up to regulate a global product market, and the industry has set its sights on exporting even more. This is leading the dairy industry to look at how other countries price milk as it relates to the U.S. pricing system and its ability to “be globally competitive.”

As the percentage of Class I sales have declined in relation to growth of U.S. milk production over the past decade, the percentage of milk pooled on FMMOs has also declined from 82% in 2011 to 60% in 2021 (See Table I).

Covington explained how pooling plays out within the FMMO system: “A regulated plant is required to pay its direct shippers and any co-op supplying milk a minimum blend or uniform price. Each Order takes the revenue from each class at the minimum price and pulls it together into one pool to come up with the uniform price.”

He said Class I differentials “have two purposes, to move milk to fluid use and to gain additional revenue for dairy farmers.” They range from $1.60/cwt in the extreme northern U.S. to $6.00/cwt in Miami, Florida and are added to the base Class I mover price.

The regulated Class I plants pay the difference between the uniform price and the Class I minimum price into the FMMO. Other class plants voluntarily participate to take a draw from the FMMO to add to what they pay their producers. That’s how it has worked most of the time – until now.

Diminished Class I sales as a percentage of total milk flip this switch, and the 2018 Farm Bill change to averaging Class III and IV skim plus 74 cents — instead of the ‘higher of’ — along with the advance pricing element, have increased the de-pooling pressure on this system, especially during times of volatility.

When asked about wide price inversions that occurred in some months over the past two years, both Covington and McCully observed the impact on bottlers paying above minimum prices to attract milk away from then higher-value Class III.

In thinking about the future, Covington reminded attendees of the past. He said at one time some Orders had individual handler pools — not marketwide pools — a nod to the idea of how FMMOs could continue to regulate Class I, if handlers in the other classes lose interest in participation.

Back when California was a state order, virtually all milk was pooled. Plants had to make decisions about pooling annually by January 1.

McCully contended that this scenario led to dumping of milk and inefficient transport to other areas. According to his analysis, the idea of making the pooling rules more restrictive and uniform across all FMMOs would lead processors to completely leave the system, and they can do that because their participation is voluntary, except for Class I.

Risk management was on the mind of several commenters, including Doll. He pointed out how the ‘holes’ in the Class I pricing change were exposed by the pandemic volatility. (Significant losses to Class I value are occurring again in the February and March 2022 Class I price.)

Joining Doll as a fellow Illinois dairy farmer was Bryan Henrichs. He said the class price inversions during the pandemic left many farmers on the losing end of what they thought were ‘safe’ $18 Class III forward contracts. The up to $9 negative PPDs kept them from achieving that price when the Class III price exceeded the contract level, but the farmer didn’t receive that price in the milk check — a double whammy.

Henrichs and others noted that milk should be priced competitively and simplified. Henrichs mentioned the idea of pricing milk at one price — no matter what it is used for — allowing market participants, including farmers, to manage risk and trade location basis, like for corn.

Arden Tewksbury’s comments from Progressive Agriculture Organization based in Meshoppen, Pennsylvania were presented by Carol Sullivan — highlighting the need for cost of production in the pricing equation, along with a realistic supply management program.

Annual FMMO pooling decisions (instead of in and out), and his longtime support for whole milk in schools were other key points offered by Tewksbury.

One attendee stated that if processors are looking to raise their ‘make allowances,’ why not add a ‘make allowance’ for producers?

On cost of production, McCully pointed out that the range is wide between a 50,000-cow dairy in western Kansas and a 40-cow dairy in northern Vermont, for example. He said interstate movement of milk and the fact that FMMO participation is voluntary for over 80% of the milk outside of Class I creates issues for using a blanket national average cost of production.

McCully said ‘cost-plus’ contracts are being used today by some processors and producers, but this is only for milk sold outside of the FMMO system.

As confirmed by Covington, 40% of the U.S. milk supply was priced outside of the FMMOs in 2021. He said this could increase as Class I becomes a smaller slice of the growing pie, especially in areas of the country where Class I is already quite small.