Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

MILLERSBURG, Ohio – Consumers today are doing more buying online. Dairy farmers are no different. Every dairy cattle sale today has online bidding available, and the beef industry has been doing exclusively loadlot video sales online for decades.

Today, with more volume buyers on the market for dairy replacements, particularly with U.S. heifer inventories at their lowest levels since 2004, the online medium has become more popular – especially since 2020.

Into these dynamics, Alan and Sharon Kozak of Clover Patch Dairy, Millersburg, Ohio, will have their fifth Jersey cattle production sale of the past 15 years.

All cattle in the sale are from the Clover Patch herd, which has been a closed herd for 20-plus years and is among the top American Jersey Cattle Association (AJCA) gJPI herds in the U.S., currently 11th in the nation.

High component pounds and udder conformation are important in the Clover Patch breeding program, which Alan describes as being focused on using the best bulls in the breed, over and over.

As a grazing dairy, feeding supplemental TMR, the milking herd of 470 registered Jerseys, housed in both freestall and bedded pack facilities, produces a rolling average 20,480M 5.1 1050F 3.7 760P with SCC consistently below 140,000.

All sale animals will be genomic and A2 tested, with 98% of the herd confirmed A2A2.

Alan Kozak has worked with the Jersey breed for most of his life. He and Sharon have strived over three decades to breed them right and raise them right, to milk a herd that is healthy and productive. Alan makes the breeding decisions that produce each calf, and he is quick to credit Sharon and the farm staff for top-notch care of the youngstock.

Why are the Kozaks going totally digital this time? They are looking for volume buyers and have been considering this format since their last sale in 2020 was both on site and online.

Their past Cornucopia sales have attracted volume buyers on site as well. Two such buyers reported on how well the cattle have done for them in a recent NextGen podcast interview.

Alan got to thinking. Why not do it all online?

“On site sales are disruptive to the business. Many of the volume buyers are buying online, and it is much less work and hassle for the staff and the cattle,” Alan explains.

The Clover Patch Cornucopia V online Jersey cattle sale will feature 50 fresh and milking cows, 50 to 100 bred heifers and the balance open heifers and calves.

“Buyers today want to buy a group of similar individuals,” Chad Kreeger observes.

“In 2020, we made the switch from live auctions to 100% online auctions, and we haven’t looked back.”

What are the keys, according to Kreeger?

“Provide accurate descriptions, good video, sell them in groups, and arrange all the delivery and proper paperwork for the buyer,” says Chad. “The seller benefits from global exposure on their sale and less stress on the dairy getting ready for the sale.”

Some things that are important for a totally online dairy cattle sale are the quality of the cattle, the ability to put together similar groups, and the commitment to deliver this quality so buyers can bid with confidence.

“If something is not 100% as was described, we pull her from the load,” Chad explains.

“My first virtual sale was 20 years ago,” Chad Kreeger reflects. “It was simply a slide show at that time. Three years later, I switched it to video. We then conducted video sales periodically as needed over the last 15 years before switching exclusively to timed online auctions in 2020.”

The focus for Kreeger and Associates, based in Cass City, Michigan, is on commercial dairy replacement marketing and dispersal sales. In fact, one week after the Clover Patch Cornucopia V, they will be doing the complete herd dispersal of 300 Holsteins and dairy equipment at Hastings Dairy near Burton, Ohio, totally online, Dec. 6.

In 2022, alone, Chad says they conducted more than 80 online cattle auctions, and through private sales combined, handled over 30,000 head for dairy producers and are on track to do this again in 2023.

With the slogan of ‘bid, buy, sell anywhere on the planet and we will handle the details’ summing up the total online experience, Chad reports that cattle have sold on their online auctions throughout the U.S., Canada, Puerto Rico, and Hawaii.

While most dairy cattle sales are hybrid on site and online, and 100% online might not be for everyone, there are many scenarios in today’s market that fit. One of the keys is to be lined up with the commercial dairy replacement market to offer groups of similar cattle, which abbreviates the length of the auction online.

“The busy life on the dairy today doesn’t always allow people to get away and sit through a long auction. Our program simplifies the process,” he says, noting that the cattle also benefit, going straight from the seller’s farm to the buyer’s farm while the price discovery of the auction remains vibrant.

To make it all work, there is a lot more upfront time spent by the team. According to Chad, the process is: take videos and pictures, prepare marketing materials and a sale catalog, load this onto the system, advertise and promote, and load out.

As for the buyers, says Chad: “It has never been easier to purchase cattle and have them delivered to your door just like a pair of boots.”

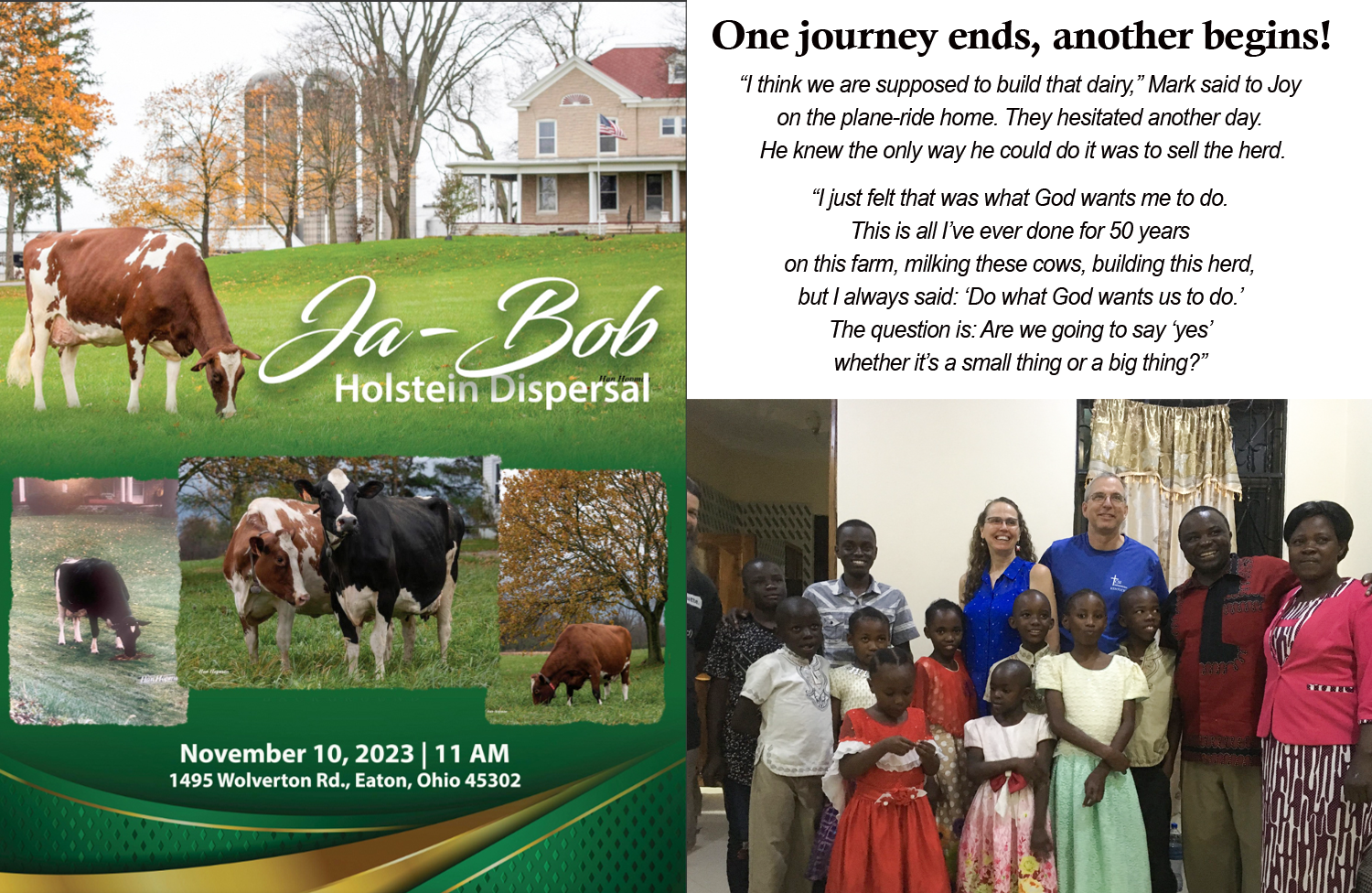

The Ja-Bob Holsteins dispersal Nov. 10 represents a unique journey in Holstein genetics and the first step as Mark and Joy Yeazel embark on a mission to build a dairy at Eternal Families Tanzania

“Every child deserves two parents. Every child deserves love, and they add into that they are raising them as Christians to be future leaders for their community and their country,” say Mark and Joy Yeazel as they talk about the next chapter in early 2024 that begins with the Nov. 10 complete dispersal sale of their Ja-Bob Holstein herd at their dairy farm near Eaton, Ohio. Mark and Joy had visited Eternal Family Tanzania, an orphanage of 130 children, organized as 10 homes with two parents and 13 children each, and they are seeking to be sustainable from a food standpoint. They wanted to milk cows, and if anyone is prepared to help them do that, it’s Mark. “I felt God calling me to do this,” he said. But to do it, he knew he’d have to sell the herd he has been devoted to for 50 years, to end one journey and begin another. Be inspired by the video about the mission here The sale catalog, including benefit lots and donations can be found here

By Sherry Bunting, Farmshine, October 27, 2023

EATON, Ohio – A new chapter begins for Mark and Joy Yeazel of Ja-Bob Holsteins in early 2024. It has been in the making since they first visited Eternal Family Tanzania orphanage in East Africa in March of 2019. In fact, their Junk for Jesus ministry they started 18 years ago had already been financially supporting this ministry — a village of 10 sets of house parents each raising a dozen orphans and growing the farming enterprise to feed them.

Fast-forward to spring 2023 when they went back to see how God was working there. On April 2, Mark, who turns 63 this week, had planned to milk five more years. Seven days later, on April 9, he was planning to sell the herd. Mark says they are doing this for the children, “for the least of these,” called by God to build a dairy at the Eternal Family Tanzania farm.

Nearly 200 lots will be offered at the November 10 complete dispersal of the unique Ja-Bob Holstein herd. All of the dairy equipment, including robots, will sell in the auction managed by Fraley at the farm in Eaton, Ohio, and on Cowbuyer. There will also be donation lots with proceeds going 100% to the mission.

The sale catalog is creating some buzz among breeders for its foundation and the unique traits Mark has brought in. Selling are 105 of the 125 milking cows, 80 calves and heifers, as well as embryos and semen. There will be many unique combinations of red, polled, homozygous polled, A-2 and ‘slick’, from a foundation built on cow families like matriarch Sky-Hi Mars Helen-ET RC 4E92 GMD DOM, and 35 years of aAa breeding. Mark has prioritized width, strength and function.

Some of the lots, as well as donations of semen (including Ja-Bob Jordan-Red) from Triple Hil and embryos from ABC Genetics will directly support the mission. Donated lots continue to come in. This includes a recently added 20 units of early-release Ja-Bob Heritage PP-RED-ET (homozygous polled) from Triple Hil and an anonymous dairyman donated 10 units of sexed Radix P. NoBull Sires recently donated 10 units sexed and 20 units conventional semen (buyer chooses bull in their program).

Mark notes in a Farmshine phone interview that on their spring 2023 visit to Eternal Families Tanzania, they were “so impressed with the village, the design, the school they built, the way they are farming and really embracing the whole vision of caring for the children and doubling the size of the village. One of their stated goals is to be food independent. They built a fishpond and catch water off the roofs. They wanted to start raising chickens, and they wanted to start milking cows and to graze the fields in the off season.”

His wheels started turning. “I think we are supposed to build that dairy,” he said to Joy on the plane-ride home. They hesitated another day. He knew the only way he could do it was to sell the herd.

“I just felt that was what God wants me to do. This is all I’ve ever done for 50 years on this farm, milking these cows, building this herd, but I always said: ‘Do what God wants us to do.’ The question is: Are we going to say ‘yes’ whether it’s a small thing or a big thing?” he says.

Everything he has done may have prepared him and pointed him in this direction.

The Ja-Bob herd dispersal Nov. 10 ends one chapter as Mark Yeazel (right) prepares for the next chapter designing and building a dairy at Eternal Family Tanzania. On a recent visit he talks by the Mahindra tractor his church purchased for the orphanage with founder Mircea Toca (left) of Romania, and George Nywavi who is the farm manager and a house parent. Photo provided

“We are still relatively young and healthy. Our children aren’t interested in continuing what I do here. We’ve accomplished a lot and have been so blessed. To have a cow family like the Helens has been amazing, and the other goals and foundations we’ve been able to build that can be embraced by other breeders who can add their expertise to do good in the world,” he explains.

Talking humbly of the blessing of the chapter that is closing and enthusiastically about the chapter opening ahead, Mark cites Ephesians 3:20: “Now to Him who is able to do immeasurably more than all we ask or imagine, according to His power that is at work within us.”

“The first thing I need to do is to be there and to understand what an East African dairy looks like, not what a Mark Yeazel robotic dairy looks like,” he says, noting he has timelines in his mind, but “I’m not sure what God has in mind. It’s really one step at a time. This is what God has called me to do for the next year. What the following year holds, I don’t know, and that’s alright.”

Mark’s journey in the chapter that is closing really began when he came home from college thinking he needed to add some income to the farm. His interest in genetics led him to look for cows with red factor out of top families. Out of two major cow purchases he made in 1983, it was Helen that turned out to be the brood cow, with some in the Helen family today now 10th generation EX, with up to 12 generations potential in the youngstock.

He added polled over 25 years ago and has had success selling polled bulls into AI. While he did not intend to chase the A-2 genetics, he used enough of those bulls that over 40 head are identified A-2 with over 40 homozygous polled, over 120 polled and 120 red, as well as 9 Linebacks in these categories. Seen here are 31 heifers arriving for the sale from the heifer raiser in Wooster, 80% of the Ja-Bob youngstock are red.

The ‘slick’ gene was added six years ago, working with Girolando embryos. Girolando are Holstein-like in appearance, but with heat-tolerance and adaptability. He wanted ‘slick’ calves out of red A-2. He has sold six slick bulls to the minor AI studs already, and about 20 slick animals are in the sale.

“I felt like we were ignoring some of the needs of the international community, that this is a void, and the heat-tolerant genetics would really help those breeders,”Mark relates. “I was not seeing anyone else doing it, so I thought: ‘Why not make some lines for the common breeder in tropical countries?’”

Not long after he got into it, ST Genetics and Select Sires started doing this also. So, while the large studs did a quick acceleration with genomics, Mark followed the red and the cow families. There were three bulls with the slick gene available, and he used all three, plus some semen from a bull in New Zealand. He also bought some embryos out of the University of Florida for outcross.

“I made my own bulls for the second generation breeding because I came into this early, so I needed several of them,” he explains.

While he didn’t set out a goal to breed for Tanzania, slick embryos could benefit the dairy project there in the future.

“Our first goal in Tanzania is to produce milk for children, so the type of cow is not nearly as important as just getting started in production, to start milking and see where God takes that,” Mark explains, adding that there are no organized dairies in that location, so cattle will be brought in from further away.

Mark’s journey really began when he purchased first-lactation 2-year-old ‘Helen’ at Sky-Hi Holsteins in Lacrosse, Wisconsin. She would become the matriarch of the Ja-Bob Holstein herd. Photo provided

The first major mile-marker in the Ja-Bob journey was exactly 40 years ago in October 1983 when Mark purchased Helen as a first lactation 2-year-old from Sky-Hi Holsteins in Lacrosse, Wisconsin. He knew her full brother was a red ET bull at 21st Century Genetics, but back then there was no DNA testing. So, he looked for an ET sister.

He went to Lacrosse to view the herd, and when he saw Helen standing in the stall beside her 14-year-old dam, it was her deep pedigree for longevity that sealed the deal.

He spent $10,000 on Helen – more than double what his father had ever paid for a cow. He was hoping she would carry the red factor like her brother. “But I knew her pedigree was so good that even if the RC was not there, she was worth it,” he says.

Sky-Hi Mars Helen-ET RC 4E92 GMD DOM

Having just completed an internship at Select Embryos, Mark was excited about the prospects to bring the red gene out faster. Helen was flushed to a couple red bulls, including Needle-Lane Jon-Red-ET.

“Three of the first six calves were born red, and we knew we had the red factor. We also flushed her to black bulls, including Walkway Chief Mark,” he recalls.

It was the natural breeding of Helen to Chief Mark that produced Ja-Bob Mark Heavenly Joy, a cow that would go on to be rather famous in her own right. She was born 20 days after he started dating the woman (Joy) whom he would marry four months later.

While Mark says he has never been hung up on milking averages, the Ja-Bob RHA is 27,641M 4.1 1128F 3.25 898P with a 140,000 SCC. He has a couple cows over 200,000-pounds lifetime and several over 150,000, with some individual lactations over 40,000, and recently the first with 2000 of fat.

His original goals were to sell a bull to AI, make an Excellent cow, and produce a 1000F record. All of that was achieved in the first three years. Did he imagine then that he would sell well over 100 bulls into AI, that he would have 10th generation EX in his herd, and a cow with 2000 pounds of fat?

No, but he knew good things would come from staying true to what was important. To accomplish what he did, he used aAa analyzing to shore up that foundation while pursuing the unique traits with young sires.

“I am not anti-genomics, by any means, but I feel the philosophy of genomics has narrowed the breeding base of the business, and breeds a like-kind cow. Sometimes, you don’t get a lot of balance with that type of cow,” Mark observes.

Strong front ends. Good feet and legs. That’s important, he says.

He talks about showing contacts in Kenya pictures of national champions in the 1970s, 80s and 90s, these wide, strong animals. He believes the industry needs to be “more intentional to sell internationally what fits the environment.” Toward that end, the red and slick bulls, he describes as built to be more rugged.

“I think we can do better,” he says. Even in the U.S., he encourages breeders to go back and look and know the cow’s environment. “If that is delivering feed to cows on concrete, and an average 2.5 to 3 lactations, then you’re making a terminal cow. But if those cows are grazing or in tie stalls, you want a little different type of cow, and the genomics may not reflect that.”

Facebook photo of the Ja-Bob milking herd three nights before the sale, robots visible at rear of the barn.

At Ja-Bob, cows are milked with robots that were installed in June 2013. In that system, teat placement is important, and it’s something Mark says must be considered when using genomic bulls. But when using Triple Hill or smaller studs, he says “I knew that wouldn’t be a problem. It’s the higher genomic bulls that have put emphasis on tight, high udders and short teats. Those are the ones you have to watch out for with robots.”

He notes that the common combinations of aAa matings can be found in higher genomic bulls, so, if that’s what he needs, it will more than likely be a genomic mating. But if he needs a less common combination, a 5-4-6 or a 5-1-3 or 2-1-6, for example, that won’t be genomic.

“If I am looking at red and the occasional RC, and combinations like 5-1-3 or 2-1-6, then I look at Triple Hill and K.I. Samen, and I am watching for those numbers to pop up,” he says, continuing to talk about the way aAa has worked for him from the beginning, something that keeps the foundation on track because it gets complicated when bringing in unique traits that can eliminate whole populations of choices.

What has been most satisfying about this journey as he looks ahead to the next?

Mark tells the story of visiting a farm in Holland many years ago. The breeder wanted to show him daughters of Ja-Bob Horizon-Red, one of Helen’s first sons. “I felt I did my job that a breeder somewhere in the world had a nice daughter from a bull I had bred, and he is happy with her.”

A little fun with the mission fundraising will be had with lots 179 and 180 (aka ‘Jane’ the cow and her daughter ‘cut from the same mold’)! Proceeds from this lot go 100% to the purchase of a cow for the Eternal Families Tanzania.

Of course, breeding a bull like Jordan multiplied this feeling quite a bit as Jordan went into 47 programs worldwide.

Reflecting on two Helen sons Jordan and Helium, he confesses he never set out to breed a top TPI bull, but Jordan was 66th in the top-100 and number one red bull for a while. Helium was the number one udder composite bull for a while in Germany.

“To think that a little breeding program in Preble County, Ohio could impact people all over the world is hard to believe sometimes,” he admits.

“I’ve tracked the Helen family all over the world, so I have traced animals in 16 different countries, and identified 350 EX and over 1000 VG female maternal line descendants in 11 countries — not counting daughters of Jordan.”

In fact, he shares that Roxy may be the only cow to have more EX descendants worldwide. “Bob Miller and I have talked about this,” says Mark. “He traced over 450 EX back to Roxy.”

Helen also produced 13 red sons in AI. Perhaps Apple had that many, but Helen did it decades ago, when ET was in its infancy and long before IVF.

-30-

Some of families of Eternal Family Tanzania pictured during one of Mark and Joy Yeazel’s trips. They are selling their Ja-Bob Holstein herd in Eaton, Ohio on Nov. 10 to spend the next year building a dairy there. Screenshot from the video about their mission that can be viewed on vimeo at https://vimeo.com/869267516/6a384f7d82?

USDA production and cow number revisions reveal how very small changes in domestic production now have very large and disproportionate impact on milk prices

By Sherry Bunting, Farmshine, November 3, 2023

EAST EARL, Pa. – The editorial opinion/analysis on the cover of the Oct. 27 Farmshine tells only part of the story after reviewing the USDA NASS downward revisions of five months of previous milk production data on Oct. 19 and looking at the monthly USDA Economic Research Service Supply and Utilization Report, released Oct. 16.

From a supply and demand perspective, there have been more positive fundamentals this year than the spring and summer milk prices would have led us to believe.

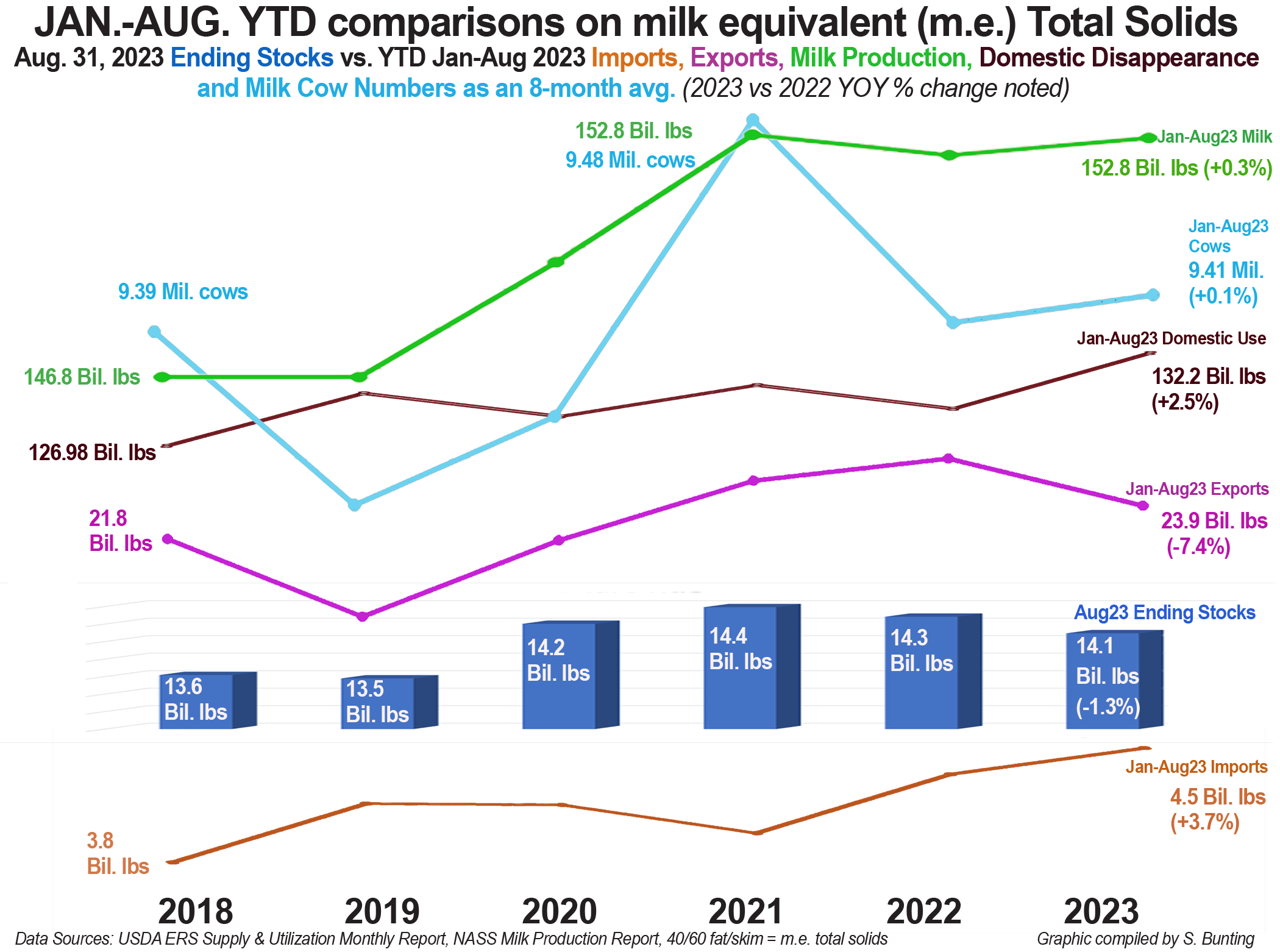

The graph shows it all.

We went back to 2018 to calculate January through August year-to-date (YTD) total solids on a milk equivalent (m.e.) basis for the supply side: milk production, imports, beginning stocks on January 1st and ending stocks on August 31 in each of the six years 2018 through 2023. We also took this approach with the demand side: exports and domestic disappearance.

Here’s what we found:

First and foremost, beginning stocks of dairy products came into January 2023 up 0.5% above year ago. Milk production also came into the first quarter on an upswing of just slightly more than 1%. After the USDA revisions of previously reported April through August data, cumulative milk production Jan-Aug 2023 is 152.8 billion pounds, up 0.3% from Jan-Aug 2022 but unchanged from Jan-Aug 2021.

Meanwhile, exports started the year on a higher note before slipping through the middle months to be down 7.4% as a cumulative total for the Jan.-Aug. period compared with the year-to-date totals for Jan.-Aug. 2022. The cumulative export volume total for those months was also 3.96% lower than Jan-Aug 2021, but nearly 6.5% above 2020 and 2018 and nearly 24% above 2019.

Simultaneously, dairy imports ended the period 3.7% higher than a year ago, and back in the January through April period —precipitating the steep drop in farm level milk prices — we saw cumulative total solids imports up a whopping 15.3% above year ago.

By April 30th, ending stocks had crept 3.3% higher than the previous year, but domestic disappearance was still beating the previous year by 1 to 4%, except January’s domestic disappearance was off 1.5%. For the Jan-Aug 2023 period, domestic disappearance is up 2.5% vs. the same period in 2022.

By August, ending stocks dropped to levels 1.3% below year ago and the lowest August ending stocks on m.e. solids basis since 2019.

Given these numbers, we see precious little space to maneuver in these markets when changes in exports and imports become the tail wagging the entire dog. Combined, they can make such a big difference to the farm-level milk price – even in the face of domestic demand beating year ago every month and what has turned out to be flattish cumulative milk production.

Since April 2023, not only have milk production and cow numbers now declined after several months of disastrous prices, the USDA has now also re-evaluated and revised lower its previously reported numbers. (We said from the beginning the cattle inventory just wasn’t there to support the earlier-reported milk cow numbers, so either USDA under-estimated the biannual inventory or over-estimated the monthly milk cow numbers).

The accelerated imports were a wild card this year from January through April before slowing down in May through August. The cumulative year-to-date total for January through August is 3.7% higher than a year ago after being double-digits higher at the end of April.

Still, when we factor in the 8% gain in imports in 2022 vs. 2021, the total of 4.5 billion pounds (milk equivalent) for the first eight months of 2023 beats the same period in 2021 by 12%. That’s significant.

Ending stocks were higher each month this year until July and August; however, exports were also holding steady to strong through May.

It is the continued year over year increases in domestic disappearance that support the uptrend in milk prices since mid-July.

Bottom line, U.S. dairy producers have just weathered a storm where even though cow numbers were not a whole lot different from a year ago, and even though milk production and beginning stocks were not so out of whack, and even though exports were generally stable until July, we saw prices this spring and summer fall 37% below the previous year, and the DMC margin fell to a record low $3.52 in July, fully 63% below the milk margin of $9.92 the previous year.

This illustrates how tiny the margins are in these supply and demand equations that can make big dents in the farm level milk price.

Increasing the national herd by a mere 5,000 cows deals a much bigger blow when it is coupled with modest gains in milk production per cow. And, even though exports are about four to six times greater in volume than imports, a sudden increase in those imports – even while exports are steady or higher – can bump the market disproportionately lower.

The good news in these graphs is that ending stocks have trended lower through the year, dipping under year ago since July, while domestic use has trended higher than a year ago every month but January. Yes, export volumes have now slowed, but so have import volumes and milk production.

The trouble I see for the future is this: As dairy farmers become more efficient, producing more milk per cow, and against this backdrop of more imports and volatile exports… the risk of extreme volatility becomes even greater whenever a new 5,000 head dairy expansion starts up or a new 10,000 to 20,000 cow dairy is built. Current replacement cattle prices at their highest level since 2015 and record high culling values for beef further push consolidation. Renewable Natural Gas credits push the type of expansions at a minimum 2500 to 7000 cow clip, replacing the diversity of farm sizes in the dairy industry at a more rapid pace.

Against this backdrop of the disproportionate impact of imports and exports on dairy markets today, the entire industry is now disproportionately more vulnerable to small changes in cow numbers. All it takes today is one large-scale business decision to flip the switch and wreck the train and bump more small- and mid-sized family dairies off the track.

It’s to the point where milk production forecasts need a microscope for the minutia, not a telescope to see the planetary alignments.

Most of the information for this report was derived from the USDA Economic Research Service data that are reported around the 16th of every month. The report includes both the dry milk powder and whey stocks as well as cold storage butter and cheese. The monthly ERS Supply and Utilization of Dairy Products by Category reports the imports, exports, and ending stocks on a milk equivalent basis separately for fat and skim solids. Using the 40/60 ratio, we figured the milk equivalence (m.e.) on a total solids basis to generate the graphs. We also updated the milk production totals to reflect the NASS revisions two weeks ago, which were not yet updated in the available ERS reports.

EAST EARL, Pa. — In the June 30 and July 7 editions of Farmshine, we covered the milk market conditions behind the drama that sent farm-level milk prices spiraling lower. The two-part “rockier road for milk prices” series explored factors and asked questions about a situation that was not making sense.

Farmshine readers will recall that we questioned dubious math on the huge milk price losses in farm milk checks – far beyond the predictions for modest declines – in the April through August period.

We questioned the accuracy of government milk production reports and the USDA’s World Ag Supply and Demand Estimates that kept telling us there would be more milk cows on farms and that milk production would continue higher for the year because of… more cows.

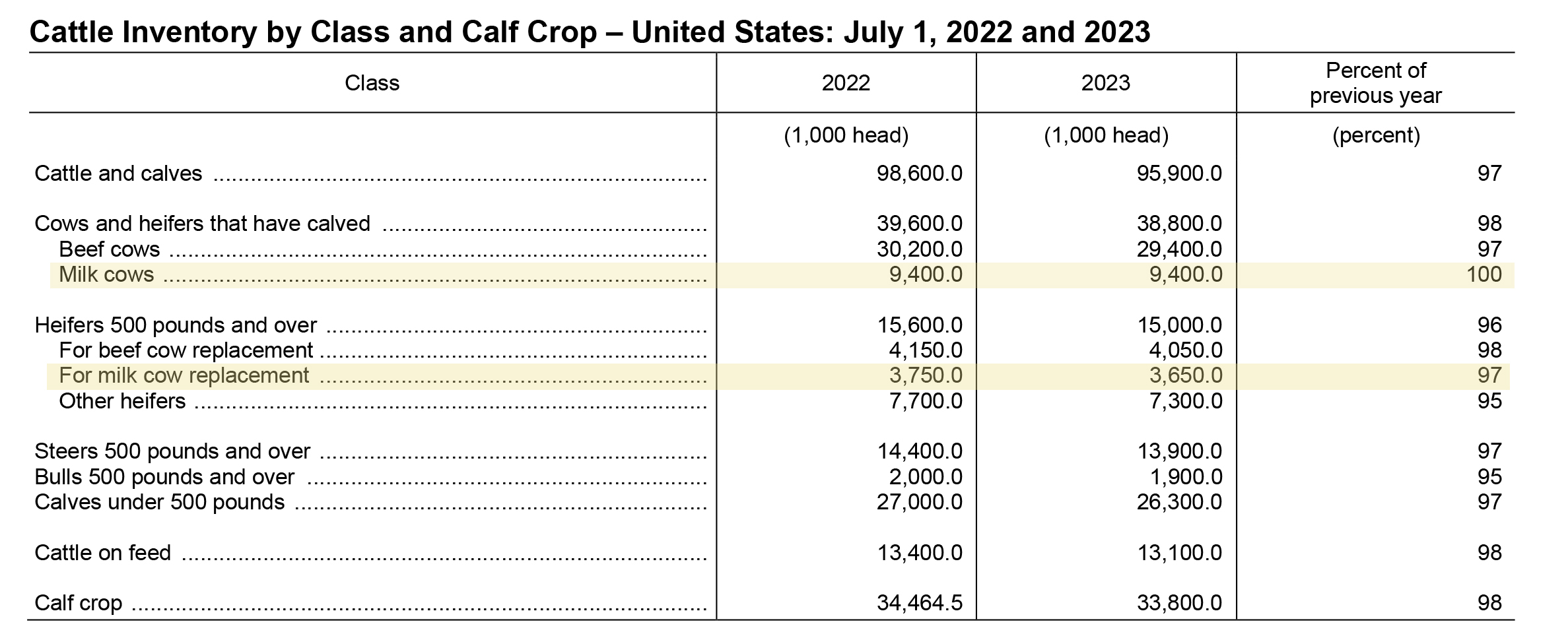

We doubted this was possible given the semiannual cattle inventory reports over the past year showing static to shrinking milk cow numbers and major shrinkage in the number of dairy heifer replacements (down 2% in Jan. 1 inventory, down 3% in mid-year inventory, a drop of over 100,000 head!). We have reported the escalating dairy replacement cattle prices setting multi-year record highs that are bearing these inventory numbers out.

We asked: Where are all these cattle coming from?

The June and July two-part series also indicated the 51% increase in the volume of Whole Milk Powder (WMP) imports coming into the U.S. compared with a year earlier in the January through May period — the highest volume for that 5-month period since 2016. (WMP is basically dehydrated milk for use in making any product or reconstitution.)

We also consulted Calvin Covington for his read of the situation. He reported to us that his calculations showed a 15% cumulative increase in total milk solids imported January through April, and that this extra volume was equal to 63% of the year over year increase in ending stocks on a total solids basis.

Well, what do you know! On Thursday, October 19, USDA issued its monthly milk production report for September. The report also went back and revised downward the previously reported totals for milk production and cow numbers for April through August.

Lo, and behold, in June and July while markets crashed, U.S. farms milked 13,000 and 34,000, respectively, fewer cows than a year ago. The September Milk Production report has now gone back to shave around 0.1% off of several months of previously reported milk production, and it has revised milk cow numbers lower than previously reported as follows: The May revision added 1000 head vs. prior report, the June revision shaved 4000 head off the prior report, July’s revision shaved 11,000 head, and August 14,000 head.

How convenient that while the Milwaukee Sentinel and area news stations were reporting five weeks of milk dumping in the sewers during June and July, and USDA Dairy Market News was reporting six to eight weeks of spot milk loads selling at $10 to $11 under the abysmal Class III price as it hit multi-year lows, the USDA reports had been telling us we were milking more cows than a year earlier, and those cows were making more milk.

Prices had plunged by more than 37%, and no one was talking about the scale-back of mozzarella cheese production and the ramp up of whole milk powder imports.

Sure, they were talking about the softening of dairy exports, and maybe that’s the point. The industry had to get the U.S. price levels below global levels in a hurry to honor the global goals set by the national dairy checkoff under previous USDEC president Tom Vilsack to keep growing exports on a Net-Zero pathway to get to 20% of milk production on a solids basis.

We wrote with concern in June and July about how even those prior numbers did not make sense at those previously incorrect levels, how a tiny change such as milking 7000 more cows in May vs. year ago and a little more milk per cow through the period could result in prices falling this hard in June and July. We have even more questions as even those small supply-margin factors have now been edited by USDA to be lower than previously reported for the April through August period.

Cow numbers have always been a driver for milk prices. Now we know there was an average of 21,000 fewer cows milked in the June-July period. And, by July, there were actually 34,000 fewer cows on U.S. farms vs. year ago.

For the Q-3 July through September period, the revisions show an average of 33,000 fewer cows nationwide compared with the third-quarter of 2022. Maybe this will also be revised lower in the future — as it includes the number of milk cows on U.S. farms in September that is now said to be 9.37 million as a preliminary figure.

In the space of six months, U.S. total milk production has gone from running 1% above year ago in Q-1 to nearly 1% (0.7%) below year ago in Q-3. But within that difference lies a revision that begs big questions about what was really going on while prices were plunging.

According to the tables in the September milk production report, the reality of the situation in June and July — while milk prices hit rock bottom and milk was being dumped and sold for $10 to $11 under class — we were already milking 13,000 fewer cows in June compared with a year ago and a whopping 34,000 fewer cows in July vs. year ago, according to these revised numbers. Now, in September, we’re milking 36,000 fewer cows in the U.S. vs. year ago.

In fact, these revised reports show that milk cow numbers have fallen by 74,000 head from the March 2023 high-tide – an unrevised and supposed 9.444 million head — to the August revised number of 9.376 million head and the September preliminary 9.37 million.

Think about this for a moment. We had unprecedented sets of proposals for milk pricing formula changes flowing into USDA in April and May with USDA announcing in June that a hearing of 21 proposals in five categories of formula changes would begin August 23rd.

While this was staging, we saw milk pricing drama unfold.

How useful this drama was for processors during the first eight weeks of the USDA Federal Milk Marketing Order hearing that has now been postponed due to “scheduling conflicts” to pick up where it left off on Nov. 27.

How convenient it was for processor representatives to be able to point to dumped milk, below-class spot milk prices and negative premiums as justification for their proposals to increase make allowances while attempting to block farm-friendly formula changes — all in the name of investments needed in capacity to handle “so much more milk!”

(A year earlier, Leprino CEO Mike Durkin warned Congress in a June 2022 Farm Bill hearing that, “The costs in the formula dramatically understate today’s cost of manufacturing and have resulted in distortions to the dairy manufacturing sector, which have constrained capacity to process producer milk,” he said, calling the situation “extremely urgent” and warning that immediate steps needed to be taken to “ensure adequate processing capacity remains.”)

Fast forward to the first eight weeks of the USDA FMMO hearing in Carmel, Indiana in August, September and October. We listened as large global processing representatives (especially Leprino) pontificated about how the make allowances are set too low, saying USDA is setting the milk prices too high. They pointed to all of the drama this summer as proof that farmers are suffering because processors can’t afford to invest or retain capacity to handle “all this extra milk.”

Now here we are, September milk production nationwide is down 0.2% from a year ago, product inventories are tight to adequate, prices have improved… but along the way the industry managed to shake out hundreds of dairy farms — large and small — that have liquidated during the steep downhill slide this summer that so few were prepared for, as no one had a clue it would be this bad given the tight number of milk cows and replacements steadily reported in inventory.

What was really behind the dairy cliff we just experienced, where even USDA Dairy Market News recently reported a significant number of herds milking 200 cows or less have recently liquidated in the Upper Midwest?

With record WMP imports, a pull-back in fresh Italian cheese production, and other elements behind the scenes… was the fall-out of a so-called milk surplus manufactured to prove a point? (Remember, Leprino’s Durkin warned that if make allowances aren’t raised, sufficient processing capacity may not remain. And take note that other Leprino representatives warned during the USDA FMMO hearing last month that they may not invest in U.S. processing capacity in the future, if make allowances are not raised and FMMO minimum prices lowered.)

Or was the fall-out this summer manufactured to fulfill the dairy checkoff’s goals for exports? You see, we are told there was excess product in Europe and New Zealand, and our overseas sales were softening, but still well above 2020 and about even with 2021. The industry is driven to get the deals to secure more global market each and every year, even if the means to those ends are detrimental to how we serve our domestic market in the future.

Given the pullback in mozzarella production during this “rockier road for milk prices”, we have to wonder about the testimony of Leprino representatives in the FMMO hearings. They have been doing the loudest complaining.

Leprino is also a major strategic partner with DMI and the organizations under that umbrella: USDEC, Innovation Center for U.S. Dairy, Net Zero Initiative, and on and on.

They want FMMO milk prices lowered, they said, so they can pay premiums again (?), and they believe you, the farmers, should help pay for their sustainability pledges within the make allowance formulas as a cost of doing business.

They likely want to free up capital out of the FMMO pricing levels to pay for Scope 3 emissions insets from RNG-project dairies to compete with other industries that can buy those renewable clean fuel credits as offsets.

They likely want to use your milk money to pay for concentrated manure-driven expansion in the Net Zero wheel-of-fortune pathway that has been constructed with your checkoff money.