Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

WASHINGTON –- USDA officially announced Monday (July 24) the national public hearing to consider proposals seeking to amend the uniform pricing formulas across all 11 Federal Milk Marketing Orders (FMMO). The hearing begins Wednesday, August 23, 2023 at 9:00 a.m. at the 502 East Event Centre, 502 East Carmel Drive, Carmel, Indiana.

Farmers will be able to testify in person at any time, or virtually on Fridays by pre-registering.

Approximately 40 proposals were submitted by 12 organizations and were explained during a webinar in mid-June. Of those, 21 will be considered within the uniform pricing scope of the hearing, according to the USDA notice. Copies of the notice, a list of proposals being considered, guidelines for how to participate, the hearing schedule, and corresponding hearing record can be found and followed on the Hearing Website.

The Class I mover formula will be addressed in the national hearing’s scope, including the proposals from National Milk Producers Federation and American Farm Bureau to go back to the ‘higher of’ method. The change from ‘higher of’ to ‘average of’ was made legislatively in the 2018 farm bill without a hearing.

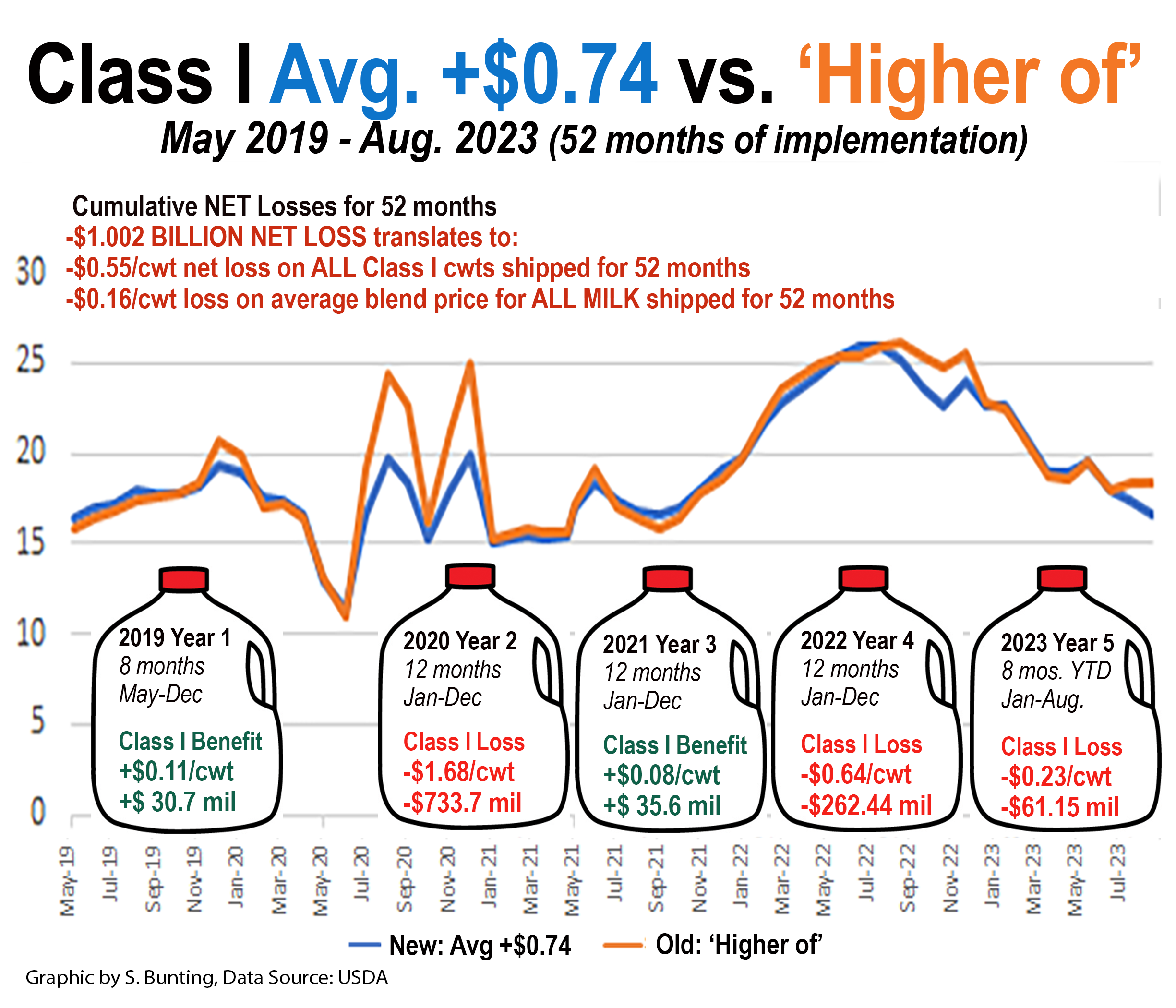

Since USDA implemented the ‘average of’ method in May 2019, net losses from this change are projected to exceed $1 billion after August 2023 milk is paid for in September.

On July 19, USDA announced the August advance Class I price mover at $16.62. If the previous ‘higher of’ method had been used, the Class I base price would have been $18.29. That’s a $1.67 per hundredweight loss on all Class I milk next month. July’s Class I mover was also calculated substantially lower (by $1.02) using the ‘average of’ vs. the ‘higher of.’ These losses will impact August and September milk checks for July and August milk.

Around 28% of all milk produced in the U.S. is Class I fluid use, so farmers stand to lose an additional 47 cents per hundredweight on all of the milk they market in August and 29 cents on all the milk they market in July — just from this formula change. This is on top of the market declines in the class and component prices. The loss to blended prices will be greater in some Federal Orders and less in others, and this does not include the impacts from de-pooling of higher-value Class IV milk.

The impact of the two-week Class I advance pricing factors is compounded by the ‘average of’ method, which is quite notable for July and August. Cheese and whey were in a tailspin lower; however, on the very next day after the August Class I base price mover had been averaged and locked-in on July 1-15 pricing factors, the dairy product markets began a huge rally, with cheese gaining nearly 40 cents in 8 trading sessions. This boosts the other class and component values much higher for the latter half of the month.

Over the 52 months of its implementation, the ‘average of’ formula has effectively removed an estimated 55 cents per hundredweight from farmer payment for all Class I milk, according to USDA data. On a blended uniform price, this comes out to a national average loss of 16-cents on every hundredweight of all milk used in all classes of products shipped from May 2019 through August 2023. That is like paying another checkoff for 52 months.

Among the other proposals included in the national hearing is the American Farm Bureau (AFBF) Class I and II proposal that seeks return to the ‘higher of’ with additional adjustments such as eliminating the two-week ‘advanced’ pricing.

IDFA’s Class I proposal seeks to keep the ‘average of’ and use either the current 74-cent-adjuster or a ‘rolling adjuster’ based on a calculated difference over 24 months, whichever is higher.

Milk Innovation Group’s (MIG) proposal seeks to keep the ‘average of’ but change the ‘adjuster’ monthly via a 24-month look-back with a 12-month lag.

Two Edge Cooperative proposals are included, one being a Class III-plus formula. The other would use the ‘higher of,’ but would base it on end-of-month four-week announced class and component prices instead of the two-week prior month advance pricing.

The hearing docket also contains four proposals on Class I differentials, including NMPF’s proposal to increase them in all locations by varying amounts as well as MIG’s proposal to lower them across the board by $1.60.

Two proposals from NMPF and National All Jersey will be heard to update milk component factors.

Six proposals will be heard on Class III and IV pricing formulas. Three are separate proposals from NMPF, IDFA and Wisconsin Cheesemakers to update processor credits, known as ‘make allowances,’ as well as three from Select Milk Producers on butterfat recovery, farm to plant shrink and nonfat solids yield.

In addition, the hearing scope includes four proposals on how dairy commodity products are surveyed, including NMPF’s proposal to remove 500-lb barrel cheese from the weekly survey, AFBF’s proposal to add bulk 640-lb block cheese and unsalted bulk butter, while California Dairy Campaign’s proposal would add mozzarella.

Dairy farmers can testify in-person at any time during the hearing, or virtually on Fridays. Beginning Fri., Sept. 1 and for each Friday thereafter until the hearing concludes, dairy farmers may testify virtually in 15-minute time slots beginning at Noon ET. There will be 10 slots for virtual testimony each Friday.

To be included, farmers must pre-register. The pre-registration for each Friday’s time slots will be available starting Monday of the same week at the USDA Hearing Website. For example, the link to testify on Fri., Sept. 1 will be available on Mon., Aug. 28. To submit exhibits for the record, email them to FMMOHearing@usda.gov by 8:00 a.m. ET on the day of testimony.

Those participating in the hearing in person should notify a USDA official upon arrival at the hearing. For additional information, contact Erin Taylor, Director, Order Formulation and Enforcement Division, USDA/AMS/Dairy Program at Erin.Taylor@usda.gov.

Consensus evident on some key proposals, such as returning the Class I mover formula to the ‘higher of’; but 10 packages contain over 30 variations and a few new biggies.

New to the party are:

AFBF wants to end ‘advance’ pricing of Class I;

NAJ wants uniform component-based pricing of Class I in all Orders;

MIG, made up of 7 fluid processors want organic exemptions, an assortment of new credits, and they want to knock $1.60 off the Class I differentials, forgetting they already get over $3.00 in ‘make allowance’ credits while not incurring those costs

California Dairy Campaign seeks an extension to consider alternative pricing formulas

Some proposals want to drop products (500-lb barrel cheese) from the FMMO formulas and price surveys, others want to add products (ie. 640-lb block cheese, mozzarella, unsalted butter)

Dana Coale, Deputy Administrator (top, left) and Erin Taylor, Director (top, right) and their USDA Dairy Division staff engaged with leads for 30 hearing proposals contained in packages submitted by 10 organizations in the pre-hearing information session Friday, June 16. Tim Doelman (bottom), CEO of Fairlife, a Coca-Cola subsidiary, explains one of the Milk Innovation Group’s (MIG) proposals that bucks the consensus on going back to the ‘higher of’ in setting the Class I mover. MIG wants to keep the averaging method with their ‘Floored Adjuster” proposal. He said returning to the ‘higher of’ prevents processors from forward-pricing their milk like soda and other beverage companies do for other ingredients. MIG also wants to knock $1.60/cwt off the current Class I differentials, and they want an assortment of new credits (obviously forgetting that fluid milk processors already get more than $3/cwt in various Class III and IV product manufacturing credits. These so-called ‘make allowances’, are built in as credits on the Class I and II prices also, for costs that fluid processors do not incur.) Zoom screen capture

BySherry Bunting, Farmshine, June 23, 2023

WASHINGTON – In preparation for a potential national Federal Milk Marketing Order (FMMO) hearing, the Dairy Division of USDA’s Agricultural Marketing Service had a pre-hearing information session Friday, June 16. During the day-long session, held virtually through zoom, Deputy Administrator Dana Coale, Director Erin Taylor and others heard presentations of the more than 30 pieces contained in proposals submitted by 10 organizations, and they engaged in questions for clarification as well as accepting requests for data before the 10 proposals were to be modified for final submission June 20.

While the Secretary of Agriculture has not yet declared a hearing, the AMS Dairy Division has publicized the timelines and action plan.

Coale stated that mandated time frames by Congress, govern the amount of time from the point at which a proposal is received to the end of a hearing 120 days later. “All of our proposed time frames are based on keeping us focused to meet the 120-day mandate,” she said.

“Once submitted, USDA will further evaluate them, and the Secretary will make the determination,” said Coale. “If the Secretary intiates rulemaking, you will see a hearing notice containing all proposals to be heard. This will be mid- to late-July, and we would expect to move forward – if a hearing is initiated – on Aug 23 as the start of that hearing.”

The location will be Carmel, Indiana, and because of the new time constraints, new procedures will be put in place, she said.

“Expect to see a very different process than customarily done to create a very efficient process while maintaining transparency and a robust evidentiary record,” she explained, noting this includes a process for submitting testimony in advance, and a naming vs. numbering convention for exhibits.

After the hearing is noticed, there will be another information session, said Coale.

“It takes an entire village,” she stressed. “Ex parte communication does not begin until a hearing is noticed, so if you have questions or need explanation or discussion on data for submitted proposals, contact us at fmmohearing@usda.gov”

The marquis proposal is the comprehensive package submitted by National Milk Producers Federation (NMPF) that set into motion the Secretary’s call for other proposals. The NMPF package has five proposals, previously reported in Farmshine through various articles since the October stakeholders meeting hosted by American Farm Bureau in Kansas City in October 2022.

Retired cooperative executive Calvin Covington is the lead on one of the five NMPF proposals, which seeks to update skim components to more accurately reflect the percentage of protein, nonfat solids and other solids in a hundredweight of milk today.

Covington said he also expects to testify on the NMPF proposal to raise Class I differentials with a new pricing surface map, something that has not been done since 2007-08, and the proposal to return the Class I base price ‘mover’ to the ‘higher of’. The current average plus 74 cents method has been in place since May of 2019, which produced unintended consequences and losses for dairy farmers.

In a phone interview Tuesday, June 20, Covington explained that after more than a year of task force meetings and discussions via NMPF with its members and their farmer members, “We’ve gotten this far, and we have got a consensus,” he said of the NMPF package.

In addition to updating skim components and Class I differentials and changing the Class I ‘mover’ back to the ‘higher of,’ the NMPF package includes a proposal to modestly update make allowances and to discontinue the barrel cheese price in the Class III protein formula while allowing 45-day forward-priced nonfat dry milk and dry whey to be included in the formula price survey instead of the current 30-day forward-price limit.

“It took a year, and that’s pretty good, to have coast-to-coast consensus on five major proposals,” said Covington. “Then you also read the Farm Bureau’s proposal and there’s pretty good consensus there too.”

Central to both the NMPF package and AFBF package of proposals is strong support for returning the Class I mover formula back to the previous ‘higher of’ method.

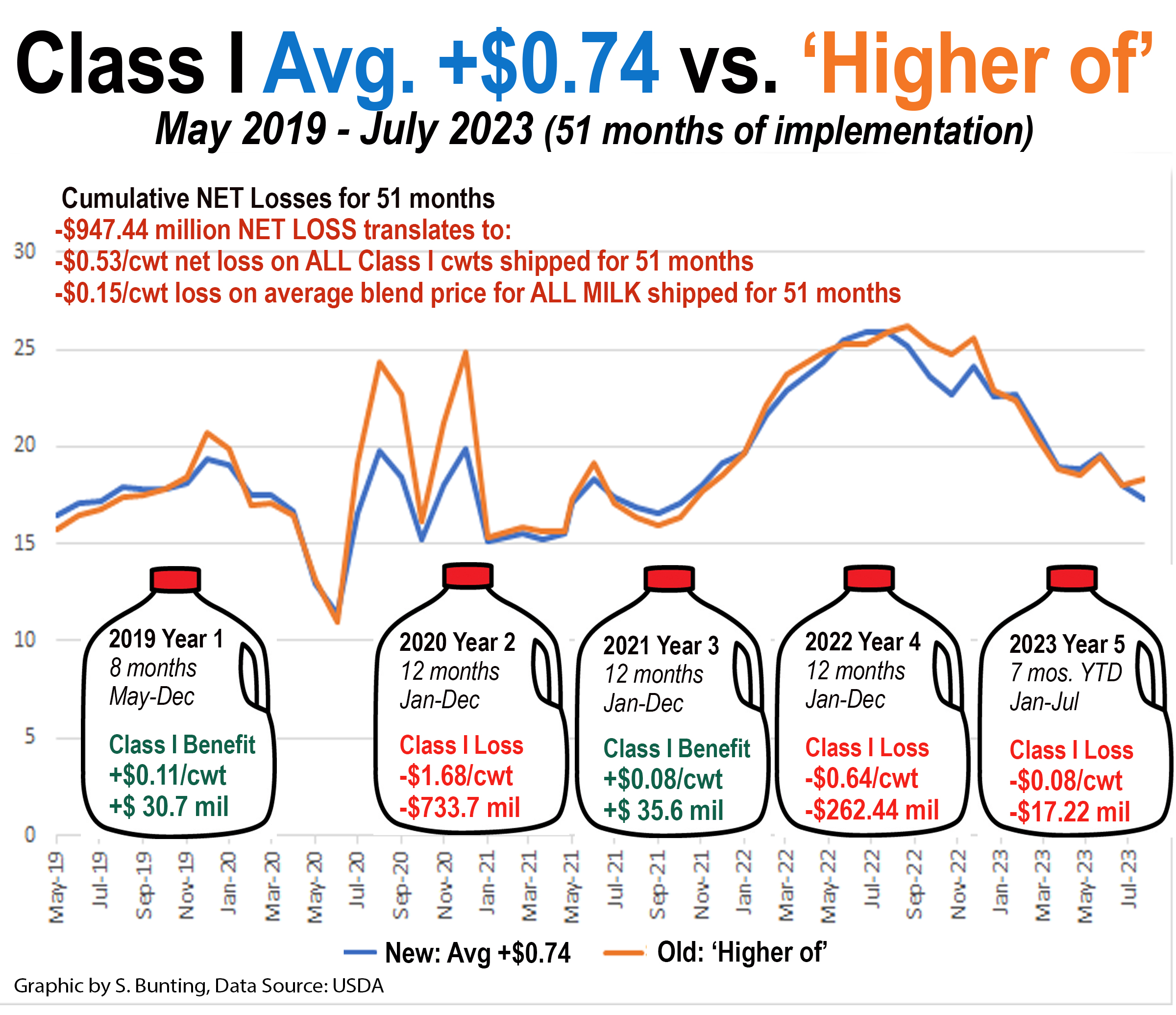

(Farmers have had a cumulative net loss of nearly $950 million, equivalent to losing 53 cents on every hundredweight of milk shipped for Class I use for the past 51 months or 15 cents per hundredweight on the FMMO blend price for all milk across all 51 months — since the change to ‘average of’ was made in May 2019 via the 2018 Farm Bill. In fact, the July 2023 Class I mover was announced June 22, 2023 at $17.32, which is a whopping $1.02 below the $18.34 it would have been under the ‘higher of’ method.)

AFBF supports NMPF’s proposal to restore the Class I mover to the ‘higher of’ Class III or IV, to drop the barrel cheese price from the Class III component and price calculation, to update component values into Class III and IV formulas, and to update Class I differentials, but notes this should be done through careful review where changes are based on a transparent record.

AFBF chief economist Roger Cryan stated that AFBF will defer to NMPF for substantiation on the Class I mover change, but if by any chance NMPF would back away from this proposal, Farm Bureau wants it kept on the table and will defend it.

On adjustment to Class III and IV product make allowances, AFBF supports this under the same logic as the NMPF proposal, but states that “such adjustment cannot be fairly undertaken except in using the data from a mandatory and audited USDA survey of, at least, those plants participating in the National Dairy Product Sales Report (NDPSR) survey.”

The difference is NMPF says it will seek mandatory surveys through legislation, whereas AFBF sees USDA as already having the authority to do this.

AFBF’s package includes some “new” proposals as well. One would add 640-pound block cheese to the Class III component and price formula and the NDPSR survey and another would add unsalted butter to the butterfat and protein calculation and the NDPSR survey.

AFBF includes a proposal to update the Class II differential to $1.56 to account for current drying costs and to adjust formula product yields and include an adjustment to the ‘make allowances’ for cooperatives and plants that “balance the market.”

The AFBF package also cites “universal milk check transparency requirements” regarding clarity to be shared on producer milk checks regarding pooled volume, Order value and actual payment for pooled and nonpooled milk.

AFBF seeks a seasonal Class I differential adjustment to “address seasonal differences in supply and demand.”

The most notably divergent AFBF proposal is one that seeks to eliminate the advanced pricing of Class I milk and components and the advanced pricing of Class II skim milk and components. It would base both on the 4-week “announced” Class III and IV components and prices instead of the 2-week “advanced” pricing factors. The advanced factors are calculated for a given month during the first two weeks of the previous month and have been part of FMMO pricing for decades.

Edge Dairy Farmer Cooperative, representing farmers in nine Midwest states shipping to 34 processors also proposes ending advanced pricing of Class I.

MIG is made up of seven companies — Anderson Erickson Dairy, Aurora Organic Dairy, Danone North America, Fairlife, HP Hood, Organic Valley/ CROPP Cooperative, and Shamrock Foods.

They want to REDUCE Class I differentials, whereas NMPF and AFBF support updates that increase them.

MIG companies want to establish Class I differentials that remove the “Grade A compensation” portion that has been built into all Class I differentials from the beginning, as well as removing the “market balancing compensation.”

Together, these removals would account for the $1.60 per hundredweight base differential that all FMMOs receive. As explained in the pre-hearing session, this would have the net effect of reducing Class I differentials (and producer pay prices) by $1.60 per hundredweight across all FMMOs.

In their justification, MIG writes that it is “far past time for the base Class I differential to be reconsidered in light of market changes, including the exploding growth of dairy beverage alternatives… and the exponential growth of non-fluid milk products often sold in the export market.”

(In this reporter’s analysis and opinion, reducing Class I differentials instead of raising them, ignores the fact that every Class I fluid milk processor – including the aseptic, ultrapasteurized, organic, ultrafiltered and other ‘specialty’ fluid milks – are already getting more than $3.00 per hundredweight embedded as a processor credit in the Class I base price mover by virtue of the cumulative sum of all product make allowances on the Class III and/or IV pricing factors used to establish that mover, but since they don’t make Class III and IV product, they don’t incur these costs. Now they want $1.60 more, plus “assembly” and other credits?)

The MIG also proposes exempting processors of Class I organic milk from paying into FMMO pools as long as they show they pay their producers at least the minimum FMMO price. There are a few other guard rails to this.

They also want to receive “assembly credits,” specialty credits, and a higher shrink credit (forgetting that they already get make allowance credits that don’t even apply to them).

Citing the “unequivocal decline in Class I sales,” the MIG sets the stage with its package of proposals to transition further away from pricing mechanisms that support local fresh milk in favor of aseptic, extended shelf-life milks and specialty products. Some of the companies in the MIG are making dairy beverages that are not even Class I, and several are getting big into plant-based and other non-milk alternatives and blends. (Is that a conflict of interest?)

USDA AMS also accepted further information on the prior petition by the International Dairy Foods Association (IDFA) and Wisconsin Cheese Makers Association (WCMA) to update make allowances. With this additional information, their petitions are back on the table and are based on voluntary cost surveys.

The IDFA alternative is described as using the current simple average of the Class III and IV advance pricing factors to set the base Class I price, and floor the adjuster at the current 74 cents — while allowing that adjuster to increase if a two-year look-back shows it was deficient vs. the higher of. This is a complex two-years back “making producers whole” in the two-years forward with the adjuster always being floored to go no lower than 74 cents even if it turns out that this method benefited farmers vs. the ‘higher of.’

The IDFA Class I proposal contains several pages of justification for the averaging method built around “preserving price hedging and risk management” for processors, particularly those in the ‘value-added’ category,” such as ultrafiltered and aseptic Class I milk products.

But it doesn’t end there…

National All Jersey (NAJ) brought forward its proposal, explained by Erick Metzger. “One mirrors NMPF’s proposal to update skim component factors in the Class III and IV formulas, except we want to see it be a simple annual update based on the previous year’s average, with an appropriate lag time to address risk management tools instead of being based on a three-year average,” he said.

In addition, NAJ proposes that FMMOs 5, 6, 7 and 131 (the Southeastern Orders and Arizona) become multiple component pricing (MCP) Orders instead of pricing on a fat/skim basis.

NAJ also proposes Class I payment requirements to be based on MCP pricing instead of skim / butterfat in all FMMOs, nationally.

“We are proposing uniform pricing across all orders — both on how processors pay for components and how producers are paid for components,” said Metzger. “Extensive updates are needed to Orders 5, 6, 7 and 131, and the needed Order language already exists in the other Orders.”

The NAJ proposal notes that Class I should be paid on actual solids, instead of valuing the skim on a skim basis. “In our proposal, it would be valued or priced on actual skim components,” he said.

What this means is if a dairy farm’s actual components processed (in Class I) were below the standard components in the Class III or IV formulas, the processor obligation would be less; and if the farm’s skim components are greater than the standard, then the obligation of Class I processors to the pool would be more. In short, accounting for actual skim components in the NAJ proposal, would replace the current pricing of Class I skim on a pounds of skim basis.

Select Milk Producers cooperative submitted proposals to update product yields to reflect “actual farm-to-plant shrink,” to update the butterfat recovery factor and to update nonfat solids yields. According to their own limited 5-year-average analysis the three proposals combined would net 13 cents/cwt on the Class III price and 42 cents/cwt on the Class IV price, but they’ve requested more data from USDA AMS to analyze — if their proposals are accepted for a hearing.

For its part, Edge Cooperative states in a cover letter to its proposals that a hearing should occur after the farm bill. “There is no imminent crisis that would present a compelling reason to initiate a hearing before the next farm bill is enacted,” the proposal states.

In the farm bill, Edge seeks a mandatory cost of processing survey before make allowance updates could be heard. Edge also seeks legislative language to expand flexibility to base individual FMMOs around something other than uniform pricing, to be determined on an Order by Order basis. This “flexibility” was explained by Lucas Sjostrom and Marin Bozic at the Farm Bureau stakeholders meeting in Kansas City last October.

However, Farm Bureau’s package of proposals asserts that there is no reason to hold off on a hearing while waiting for a farm bill, and indeed seeks the fastest resolution to the Class I ‘mover’ issue. Furthermore, Congress previously mandated timelines that don’t allow “waiting” once proposals are received by USDA. This process is in motion, unless Secretary Vilsack refuses a hearing on any of the proposals.

AFBF, in fact, cited areas of the Agricultural Agreement Act that give USDA authority to do mandatory cost surveys, without further legislation, because the Secretary has discretion to require any reporting deemed necessary from FMMO participating plants.

On the Class I ‘mover, Edge proposes two options, either a Class III-plus option if the ‘advanced pricing’ is retained or if the ‘higher of’ option is used, then to base it on final 4-week announced skim milk prices each month. This option would effectively end the 2-week advanced pricing factors and advance pricing of the Class I ‘mover,’ which has also been proposed by AFBF.

The Edge proposals include a request to align make allowance changes so that they don’t impact ‘risk management tools’ and a proposal to add Order formulation language about the information handlers shall furnish to producers with the intent of “transparency in producer milk checks.”

The California Dairy Campaign’s proposal asks USDA to extend the proposal deadline and to add mozzarella to the Class III component and price formula and the NDPSR survey. They also want consideration of “alternative pricing formulas that guarantee dairy farmers are paid according to current market rates.”

The California proposal includes a National Farmers Union (NFU) Dairy Policy Reform Special Order of Business that was passed at the 2023 NFU Convention in San Francisco. It states opposition to the call for a federal milk marketing order hearing, noting that, “If a hearing is granted, it is essential that any modifications to the federal order minimum pricing formulas take into account the volume and value of all dairy products, particularly high-moisture cheeses such as mozzarella.”

DPA also proposes a supply-balancing feature, whereby milk handlers notify farms at least 7 days prior to milk disposal action, stating the baseline production needs, how much to reduce production, and for how long, with farmers making this reduction by dumping (or not producing) this milk.

In effect, the DPA proposal includes a processor-led supply management program, not a government intervention. But to do it, the FMMOs would be the arbiter, and therefore all Orders would have to be amended to require 100% mandatory participation and pooling of all U.S. milk. Something like that may require legislation since a producer referendum bloc-voted by cooperatives could vote it down, and it’s unclear how unregulated areas would be included since states like Idaho already voted the FMMOs out.

Currently, only Class I milk handlers are required to participate in FMMOs within marketing areas that have FMMOs. Participation is voluntary for most Class II, III and IV processors. Over the past three years, roughly 60% of total U.S. milk production has been pooled on FMMOs.

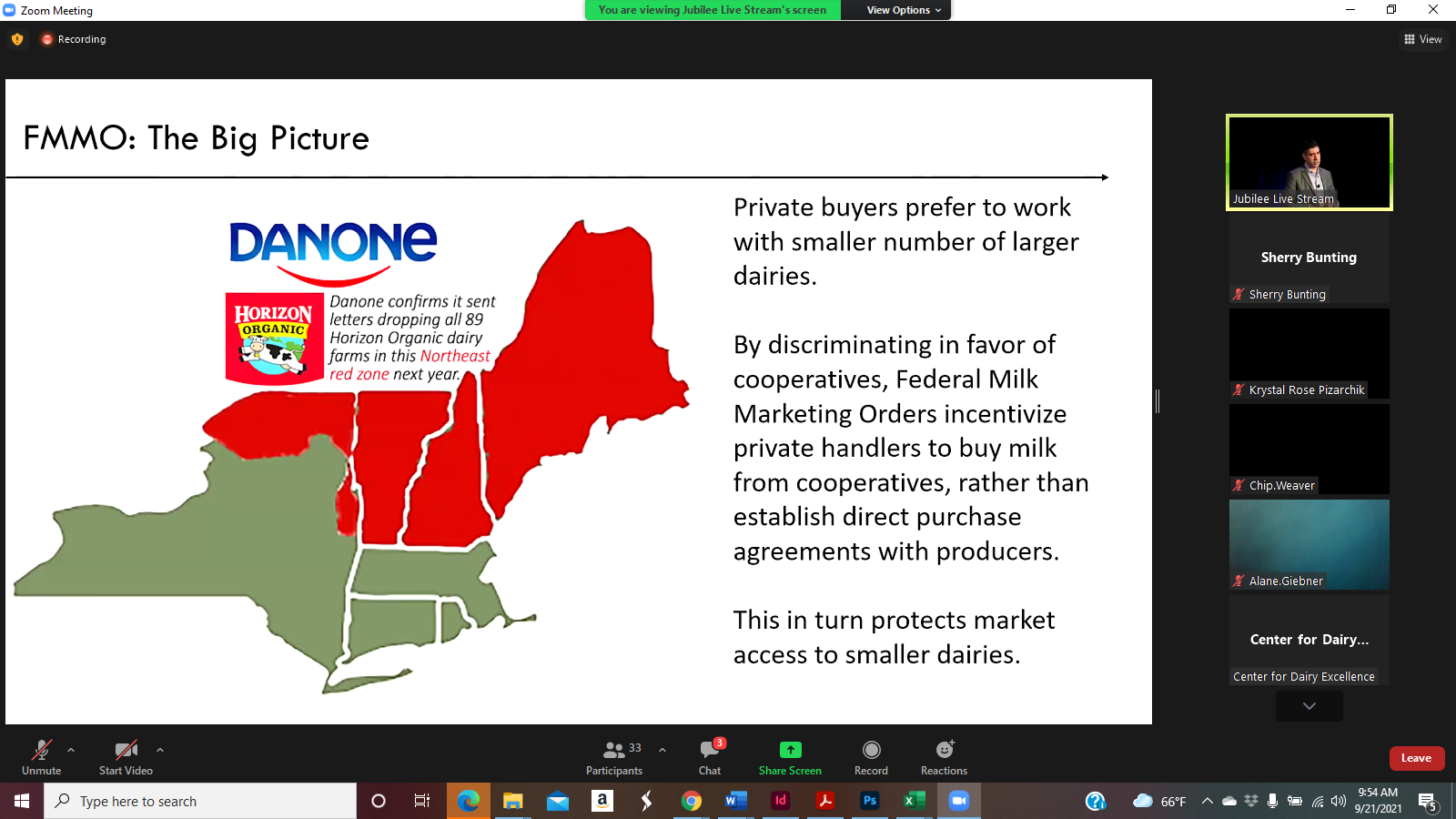

Using a graphic pulled from the September 10, 2021 edition of Farmshine in which a follow up story ran about Danone dropping 89 organic dairy farms from its Horizon brand — all of its Horizon farms in the Northeast — Bozic explained that the ‘social mission’ of cooperatives is to market all of their members’ milk. He said the “primary function of the future” for the Federal Milk Marketing Orders — as an extension of the cooperatives — is to ensure market access for dairy farms. “Market Orders are there to ensure orderly consolidation at a humane pace,” he declared.

By Sherry Bunting, Farmshine, Sept. 24, 2021

HARRISBURG, Pa. – ‘Turning the page’ was the theme for the annual Financial and Risk Management Conference where key takeaways about a changing dairy industry were presented.

The conference was hosted by the Center for Dairy Excellence Sept. 21 in Harrisburg.

Pennsylvania Secretary of Agriculture Russell Redding summarized his own thoughts: “I am still very positive about dairy, but dairy will change. It is changing,” he said.

The Center’s risk management educator Zach Myers set the stage for attending lenders, vendors, producers and industry talking about Dairy Margin Coverage and Dairy Revenue Protection and how these programs have worked (more on that in a separate article.)

Digging into the stress — the ‘change’ — was Marin Bozic, University of Minnesota associate professor of applied economics and dairy foods marketing, who also serves as facilitator for the Midwest Dairy Growth Alliance. He dug right into how and why, discussing some of the Federal Milk Marketing Order complexities, industry trends and pricing relationships. He made the case that more flexibility, competition and innovation are needed in the Federal Orders for a “level playing field” so winners and losers can “self-select.”

Bringing up the 89 organic producers Danone will drop from Horizon next year, Bozic said it is an example that, “One new farm in Indiana replaced 89 or 90 farms in the Northeast, and they can do that. There is nothing illegal about it. They could say they have a fiduciary responsibility to stakeholders and are minding their bottom line, but none of that helps you if 90 producers get dumped in a year.”

He pointed out the “social mission” of the cooperatives is to leave no member behind, so remaining an independent producer carries more risk today than in the past.

Bozic connected the dots to say the “primary function of the future for Federal Milk Marketing Orders — as an extension of the milk cooperatives — is to ensure market access for dairy producers.

“Market orders are there to ensure orderly consolidation at a humane pace,” he declared.

That’s a change from the central promise of the FMMOs today, which Bozic described earlier as “broken.”

“To navigate our businesses over the next year and longer,” said Bozic, “we have to count the passes and see the gorilla” — a nod to the visual exercise he had the audience participate in.

Bozic mentioned a few gorillas in milk. Gorillas in the FMMOs, in risk management, in dairy markets and in the macroeconomic situation – what else is going on in the world.

He showed graphs of what Producer Price Differentials (PPDs) looked like for the Northeast in 2020, the $4 and $5 negatives that represented cash flow bleeding, equity bleeding.

While the futures show the view out to the horizon over the next 6, 12, 15 months that would suggest there won’t be a repeat of that carnage, Bozic cited some of these risks, or gorillas, in the market and in world events that could represent shocks that can make the whole thing “go haywire again.”

Observing that the FMMOs are not the same today as when they were designed many decades ago, Bozic stepped conference attendees through the various long- and short-term impacts that reduce PPD, such as declining Class I utilization compared with increasing Class IV utilization and production.

“Orders were designed around the assumption that there would be plenty of fluid milk usage (as a percentage of total production), and we can just take it and designate it to be the highest and use those funds to make everyone whole,” said Bozic.

“The central promise of the FMMOs is that if your milk is as good as your neighbor’s, you get paid the same, so one farmer does not bid against another for market access and a good price,” he asserted. “That promise is now getting broken, not as much here, the East Coast FMMOs still have Class I.”

The next effect in the Northeast is the rise of protein tests. This impact comes through two channels where higher protein reduces PPD, the economist explained.

“Envision FMMOs as all processors paying into the pool and then taking from the pool. First they pay to the pool with classified pricing based on their respective milk solids. Class I pays on pounds of skim milk as volume, not on protein pounds,” he explained. “Even if sales are the same and the only thing that changes is protein, those (Class I) processors would pay the same amount (on skim) into the pool and take more money out (on protein) so there is less money remaining and a lower PPD.”

The second way higher protein production affects PPD is when the value of protein is lower in the powder than it is in the cheese. The butter/powder plant pays to the pool on nonfat solids price but takes money from the pool on protein price, “so that spread between the value of protein in cheese and powder also leaves less money for PPD,” said Bozic.

He explained the Class III price as an index of butterfat, protein and solids, in a straight formula that equals the class price. “When Class III price is higher than Class IV price, the predicted PPD for the Northeast Order declines,” said Bozic. “It’s almost linear.”

Conversely, when IV is above III, PPD goes up. “This has to do with paying the pool based on protein and nonfat solids, but when handlers take money out of the pool for components, everyone takes protein price leaving less money in the pool for PPD.

Bozic explained the demand shock to this system when the Food Box program “focused on smaller packages of cheese to put in every box. They didn’t take bulk powder and butter. So we went from a record low cheese price on the CME to a record high and no one expected this.”

The pull of 5% of the cheese supply for immediate delivery had everyone scrambling, said Bozic.

The amount of spare cheese available was not as high a volume as the government wanted to buy so cheese went from being long to short, and the price skyrocketed. This translated to an historically higher gap between Class III and IV prices as wide as $10 apart.

So why not just send more milk to make cheese? Bozic maintains that Class IV processing is accustomed to “balancing” fluid milk seasonality so there is extra capacity in that system.

Not so with Class III because those plants already run at capacity. “That’s the only way processors of commodity cheese make margin is to run at capacity, so when the demand shock came, and spare product was used up, there was no spare capacity and the price went higher. That was the main driver of negative PPD in 2020,” said Bozic.

Will it happen again? Bozic doesn’t foresee Food box programs with the same intensity in the future, but, “yes, it can happen, but I would say you need to have a pandemic in an election year. Don’t count on a program like this.”

The industry did ask USDA back in the 2008-09 recession to buy consumer packaged cheese instead of bulk commodities, so it could move instead of being stored to overhang the market later. That wasn’t working either.

“Now we understand that this other method disturbs PPDs so the dairy industry is united behind a more balanced approach,” said Bozic, describing the next iteration of purchases through the Dairy Donation Program will not be as aggressive in moving the markets by three orders of magnitude.”

Bozic said quick rallies and crashes impact PPDs also because of advance pricing on Class I based on the first two weeks of the prior month and announced pricing for the other classes at the end of the month.

Bozic explained why the change in Class I pricing was made: “The dairy industry wants to attract new distributors like Starbucks and McDonalds that are used to hedging their input costs. They don’t want to change prices every month. They want it to be what it is for a year, so the industry wants stable, predictable milk price costs to win favor with new distribution channels by making it easier for them to hedge.”

He said the new average plus 74 cents was designed to be revenue neutral. Looking forward, when Classes III and IV have less than $1.48/cwt spread, PPD under the new system is higher than under the old. But the most it can be higher is by 74 cents on Class I, which translates to 20 cents on the blend price.

“The best case scenario is to add 20 cents to the blend price, but when Classes III and IV are far apart “the PPD can go haywire. Bottom line, the upside benefit of the averaging method with 74-cent adjuster is limited but the downside risk is big,” said Bozic.