Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

CARMEL, Ind. – USDA’s federal milk pricing hearing continued into its 7th week on Wednesday, Oct. 4, and USDA announced another virtual farmer testimony session for Friday for Oct. 6, with the signup notice and link posted at the hearing website with just three days notice on Oct. 3.

Farmer testimony was heard virtually also on Friday, Sept. 29, including from two Pennsylvania producers and a third from the Keystone State testified in person on Tues., Oct. 3. More on their testimonies in a future edition.

Here are some observations as I’ve listened on and off over the past several weeks as the testimony and cross-examinations dug into this issue of the Class I mover formula.

As one can imagine, daily testimony from 8 to 5 with exhibits and cross-examination add up to a lot of material for USDA to parse through.

This is particularly daunting with the introduction of significant testimony about the CME futures, hedging, risk management and other such business management by farms and processors and how FMMO changes affect these practices.

Last week, Pittsburgh milk bottler Chuck Turner of Turner Dairy Farms testified in support of the Milk Innovation Group’s concept of modifying the current ‘average of’ method for calculating Class I to create a floor under which the add-on adjuster cannot fall below.

The fairlife CEO also testified about the MIG proposal for the Class I mover last week, explaining that fairlife relies on hedging so the company can offer 9 to 12 month pricing of extended shelf life fluid milk products to foodservice, institutional food buyers and convenience stores that purchase plant-based alternatives and other beverages with annual contracts.

He explained that if the Class I price goes back to the ‘higher of’, companies like fairlife and Nestle (also testified), and others will not be able to hedge that annual price without introducing increasingly volatile price risk to their businesses.

The Nestle rep noted that Nesquick sales increased since late 2019. That’s when they started offering buyers longer-term pricing because the Class I mover was changed to the averaging formula in 2019.

For his part, even Turner said hedging on the CME butter, powder and cheese markets might work to build a protected price for selling fresh fluid milk to schools and other buyers that want longer term pricing.

He was asked several questions about the role of the Pennsylvania Milk Marketing Board in his payment of farmers and competition in the state and region.

Here’s the problem: Grocery stores still largely receive fresh milk a few times a week direct-ship to stores.

On the other hand, the extended shelf life milk, aseptically packaged (shelf stable) milk, and various milk based innovations are shipped to a warehouse. They are not treated the same as fresh fluid milk from a pricing and supply standpoint.

Additionally, the foodservice, institutional, convenience stores, and schools want to know a price for 6 months, 9 months, one year. Bottlers say they can’t offer that if they can’t protect their risk.

So, to minimize risk for processors, the ‘average of’ formula for the Class I mover was put into legislative language in the 2018 Farm Bill with the acknowledgment that it could be changed in two years by a USDA hearing process like the one in Indiana the past six weeks.

That change ended up introducing significant risk to dairy farmers, who found their ability to hedge THEIR risk was jeopardized.

Just as there are two classes of Class I processors — fresh milk and ESL fluid products, there are two classes of dairy farmers. On the one hand, producers whose milk routinely goes to Class I fluid milk plants or pool distributing manufacturing plants cannot be depooled, but milk routinely going to manufactured dairy products can be depooled.

When manufacturing class prices are higher than the Class I mover, a ripple effect occurs that disrupts the class pricing alignments. When higher priced milk is depooled, the processors can keep that money, or pass it on to their own shippers — disrupting one of the functions of the FMMOs to have orderly marketing and uniform pricing.

As one market analyst noted in her testimony last week, it’s like the story of Goldilocks and the Three Bears. These alternate Class I mover proposals are complicated with rolling adjusters to be added to the averaging formula.

For the function of the FMMOs, the ‘just-right’ porridge is the ‘higher of’ for the Class I mover, many have testified.

Trouble is, some regions may see more processors leave the FMMOs if they can’t make it work for them, and the bifurcation in the Class I fluid milk market will leave some processors unable to adapt to long-term pricing for large institutional buyers.

Which way is fluid milk consumption heading? That may be the question to answer first.

In the Eastern U.S., one thing’s for sure, the current flat milk production is being soaked up by strong bottling demand, and the market is paying above class prices right now to get milk for other uses.

The Class I pricing question, along with the other proposals in the lengthy USDA hearing, are being looked at by USDA through the lens of the FMMO’s purpose, especially “orderly marketing.”

However, USDA has no concrete definition for orderly marketing. Will we see that intuitive definition change? What do farmers have to say about it?

For its part American Farm Bureau Federation has been orderly in its presentation of testimony. Economists Roger Cryan and Danny Munch have testified. Farm Bureau members have testified.

This week, Cryan testified on removing the “advance pricing” from the Class I and II formula as this function of using two weeks of product prices to determine four weeks of pricing the following month is another piece of the puzzle bringing more volatility into the equation that can lead to depooling.

However, processors say they want advance pricing, and they want long-term hedging too! They want it all!

According to AFBF data presented at the hearing, advanced pricing has disrupted the orderly marketing of milk and led to unfair marketing conditions for dairy farmers. This disruption is caused when the price of other classes of milk rises above the announced advanced price of Class I and Class II milk. A full explanation of advanced pricing is available via AFBF’s Market Intel.

AFBF supports several proposals by the National Milk Producers Federation, which would increase Class I prices, drop barrel cheese from the Class III price formula, and return to the “higher-of” Class I formula. AFBF also supported in testimony its proposals to add salted butter and 640-lb block cheese to the pricing survey.

Milk pricing formulas and ‘make allowances’ can feel like rocket science, farmers point out the pitfalls in ignoring the impact of mozzarella and the rising costs on dairy farms. Georgia and California producers among those testifying on make allowances, along with economists, including Dr. Mark Stephenson

Previous FMMO hearing updates can be found here and here

By Sherry Bunting, Farmshine, September 15, 2023

CARMEL, Ind. — “It’s really simple. We made it to the moon back in the late 60s… if you tell me that we can’t figure this little (mozzarella) equation out, we got something wrong,” said Joaquin Contente, the son of Portugese immigrants and a lifelong dairy farmer near Hanford, California as he gave virtual testimony Friday, Sept. 8 during the ongoing USDA Federal Milk Market Order (FMMO) hearing in Carmel, Indiana.

Contente serves on the California Dairy Campaign (CDC) board, which is a member of California Farmers Union (CFU) and National Farmers Union (NFU) as well as Organization for Competitive Markets (OCM). His son and daughter today run the 1100-cow multi-generational dairy farm in California’s San Joaquin Valley.

“Mozzarella should no longer be ignored. This issue was raised in 2000, and the volume and demand have grown dramatically since then,” he said, referencing CDC’s proposal and citing USDA data showing mozzarella production last year was nearly 5 billion pounds while cheddar was short of 4 billion pounds, and all cheeses totaled just over 14 billion pounds.

“I represent myself and many other producers who are reluctant to step up and speak out in opposition to what is being said by milk handlers, out of fear of retribution,” he reported. “It is essential to include the largest cheese category – mozzarella. The volume has significantly exceeded cheddar, and the Class III price should be modified to reflect these market conditions.”

Contente noted comments about the change in the Class I base price from ‘higher of’ to ‘average of’ costing farmers $1 billion over four years’ time.

“This mozzarella issue, if you understand the formulas and yield factors, is costing dairy farmers more, annually, well over $1 billion — and that’s a conservative number I am using,” he said.

“We have situations where the milk price drops dramatically, 30 or 38%, so you have to look at this discrepancy going on over a couple of decades. Nobody is talking about it… you’ve got to be a little bit quiet about mozzarella because you don’t want to upset ‘the mozzarella people,’” said Contente, noting that mozzarella production is 12% larger than cheddar with very high yields.

“There is information that needs to be collected, and that is the roadblock right now. It’s the largest category, and yet there is no reference to it, and the yields are so high that these cheesemakers are making product that they’re not getting charged for. It’s for free — off our backs,” he said. “We are in a system that requires price discovery of the uses of milk, and here we have the highest (volume of cheese) use in mozzarella, and we just turn the other way… why?”

The past two weeks of the daily 8 to 5 hearing sessions have been quagmired in the nuts and bolts of multiple proposals on what’s included or excluded from the pricing surveys as well as the corresponding make allowances as the hearing moved into its fourth week Wednesday (Sept. 13).

Like other producers testifying so far, Contente detailed the loss of dairy farms around him and the discrepancy between milk prices and cost of production leading to mass exodus of dairy farms currently.

Economists from academia and from cooperatives later showed numbers revealing the hard reality that the farm-well for pulling out more processor investment money is running dry.

In fact, Contente pointed out that the processor make allowance cost surveys include “return on investment,” something he said is lacking for dairy farmers in their milk prices. This was corroborated in later testimony by Cornell’s Dr. Chris Wolf and DFA’s Ed Gallagher.

During Dr. Mark Stephenson’s testimony Tuesday (Sept. 12), we learned that the current voluntary make allowance cost surveys include “opportunity cost” for plant assets used to make the products included in the survey.

“As farmers, we don’t get a return on investment,” said Contente. (And the numbers put up by expert witnesses show farmers don’t get ‘opportunity cost’ either.)

In fact, Gallagher said it’s important for USDA to consider the impact of its hearing decisions on farmers because if they can’t reinvest in their operations, it affects the infrastructure, the lending and the farmers’ access to capital — putting the milk supply at risk.

While Contente’s testimony focused on the mozzarella proposal supported by CDC, CFU, NFU and OCM, he also voiced their opposition to any increase in make allowances for processors.

On the latter, American Farm Bureau Federation agrees. AFBF also opposes any increase in make allowances based on voluntary surveys without first seeing results of a mandatory and audited processing cost survey.

AFBF’s chief economist Roger Cryan on cross-examination asked Contente if NFU opposes the make allowance increases due to the voluntary and unaudited nature of the cost surveys. “Yes,” was his response. “Very good,” said Cryan.

The IDFA make allowance proposal would reduce farm milk prices by $1.25 per hundredweight initially and even more down the road.

For Class I producers, the net result is an embedded make allowance deduct as large as $3.60/cwt at current make allowance levels, which could rise above $5.00 in a few years if the IDFA proposal is approved.

This producer loss is embedded in the Class I price even though Class I processors are not even asked by USDA to provide their cost data.

Georgia milk producer Matt Johnson testified in support of NMPF’s various proposals, which include returning to the ‘higher-of’ Class I base price and increasing the differentials. On the issue of make allowances, he said the NMPF proposal is preferred because it makes smaller adjustments.

“I understand that make allowances are an important aspect in determining Federal Order class prices, and from time to time, there is a regulatory need to adjust them,” said Johnson; however, “my milk price will go down when make allowances go up. I ask that when increasing make allowances, the Secretary consider the impact on dairy farm milk prices… and profitability. NMPF has proposed more modest changes to the make allowances, which are projected to lower farm milk prices by about $0.50 per hundredweight (not $1.25).”

During cross-examination, Johnson was specifically asked by USDA AMS administrator Erin Taylor to explain how the make allowances affect him as his farm’s milk goes mainly to Class I markets in Florida and the Southeast, not to manufacturing.

“It’s all negative,” he replied. “The make allowances are used in the prices used to figure the base Class I milk price. I don’t know who gets that draw, but for me, it’s all negative.”

In addition to CDC’s proposal to add mozzarella, American Farm Bureau defended its proposal to add 640-lb block cheddar and bulk unsalted butter, and NMPF defended its proposal to remove 500-lb barrel cheddar.

Several days of detailed accounting testimony were heard, and the kicker was when representatives for Leprino and IDFA stated that barrels should be kept in the survey as a ‘market clearing’ product that is ‘storable’, but that bulk mozzarella should not be added because it’s a higher moisture, fresh cheese, not storable like cheddar, making it a product that is not a ‘market clearing’ product. (This idea of ‘what is market clearing’ was further explored this week as needing a new definition now that there is no dairy price support program or government storage of dairy products).

Interestingly, in cross examination, we learned that barrel cheese — which Leprino and IDFA want to keep in the survey — is also a relatively fresh cheese, not all that different from bulk mozzarella, as only 4- to 30-day-old barrel cheddar is reported.

At one point, cheese industry representatives suggested the spread between blocks and barrels is used to price ‘basis’ and to price exported products, while block cheddar is mostly used to price other cheeses. Witnesses indicated some processors use barrel movement to price cheeses, such as mozzarella.

Some expert witnesses contended that other products can’t be added to the FMMO pricing formula because they are not traded on the CME. AFBF’s Cryan retorted that the CME should not be running this show, and he noted that dry whey wasn’t traded on the CME until after it was added to the FMMO formulas.

In fact, CME futures hedging, CME cash spot markets and the risk management tools that use these exchanges were a contentious point. Some witnesses said USDA formula changes will ‘disturb’ risk management contracts, and must be delayed 15 additional months after a USDA final decision to avoid such disturbance.

On a similar note, economist Dr. Stephenson, while providing academic processor cost survey information this week, was cross-examined by economist Dr. Marin Bozic for Edge cooperative. Bozic asked Stephenson if the disturbance of risk management practices would ‘fit’ his understanding of ‘disorderly marketing’.

Stephenson replied: “No… I am not sure hedgers or speculators should be first or foremost in the minds of FMMO personnel. That’s not what we are here to do.”

NMPF, NAJ say higher solids worth more nutritionally,Seek FMMO updates to avoid misalignments and disorderly marketing

Calvin Covington (left) for Southeast Milk and Peter Vitaliano for National Milk Producers Federation testified on what the outdated skim milk component standards mean in terms of underpaying farmers and eroding producer price differentials (PPD), leading to disorderly marketing. This occurs because the skim portion of the milk that is utilized in manufactured products (Class III and IV) is paid per pound of actual protein, solids nonfat and other solids; whereas the skim portion of the milk bottled for fluid use (Class I) is paid on a per hundredweight basis using the outdated standard skim solids levels. The fat portion is not an issue because it is already paid per pound in milk class uses. Screen captures, hearing livestream

By Sherry Bunting, Farmshine, Sept. 8, 2023

CARMEL, Ind. – The national Federal Milk Marketing Order hearing completed two weeks of proceedings, so far, in Carmel, Indiana. The entire hearing is expected to last six to eight weeks, covering 21 proposals in five categories.

Picking up the livestream online, when possible, gives valuable insight into a changing dairy industry and how federal pricing proposals could update key pricing factors.

The first week dug into several proposals to update standard skim milk components to reflect today’s national averages in the skim portion of the Class I price.

Here is a bite-sized piece of that multi-day tackle.

National Milk Producers Federation (NMPF) put forward several witnesses to show what the outdated component levels mean in terms of underpaying farmers, and how paying for the skim portion based on outdated component levels has eroded producer price differentials (PPD), leading to disorderly marketing.

IDFA’s attorney Steven Rosenbaum grilled NMPF economist Peter Vitaliano on this. He tried on seven attempts to establish that the fat/skim orders in the Southeast don’t have component levels as high as the national average, suggesting this change would “overpay” producers in some markets.

In his questioning, Rosenbaum stressed that fluid milk processors can’t recoup the updated skim component values if those components do not “fill more jugs.”

Vitaliano responded to say that protein beverages are a big deal to consumers, and some milk marketing is being done on a protein basis. Rosenbaum asked for a study showing how many fluid processors are actually doing this.

Attorneys for opposing parties kept going back to this theme that the skim solids should not be updated because the FMMOs are based on “minimum” pricing. They contend that processors can pay “premiums” for the extra value if they have a way of recouping the extra value by making more product or marketing what they make as more valuable.

Vitaliano disagreed, saying that even though many processors do not choose to market protein on the fluid milk label, “more protein makes fluid milk more valuable to consumers.”

Attorney Chip English went so far as to ask Calvin Covington on the stand: Why should my clients (Milk Innovation Group) have to pay more for the additional solids in the milk when they are removing some of those solids by removing the lactose?

“Consumers don’t want lactose,” English declared.

Covington, representing Southeast Milk and NMPF, responded to say: “I don’t know that to be true. It is unfair to suggest all.”

Bottomline, said Covington, raising standard skim solids to reflect the composition of milk today vs. 25 years ago adds money to the pool to assist with the PPD erosion so that Federal Orders can function as they were intended and so producers are paid for the value.

As English further questioned whether consumers even care about the higher skim solids and protein levels of milk today, Covington replied: “Skim milk solids have a value in Class I, or fluid milk. People don’t buy milk for colored water. The solids give it the nutritional value. That’s the reason they buy milk. That’s why FDA set minimum standards in some states. Why would you drink milk if not for the nutritional value?”

He also pointed out that the increase in solids nonfat over the past 20-plus years has improved the consistency of lower fat milk options. As noted previously, the milkfat is a separate discussion and is not included in this proposal because farmers are already paid per pound for their actual production of butterfat in all classes, including Class I.

Under cross examination, Covington explained that the Class I price in all Federal Orders pays for skim on a standardized per hundredweight basis and pays for fat on actual per pound basis. Meanwhile, the manufacturing classes pay for both skim and fat on a per pound of actual components basis.

As skim component levels have risen in the milk, the alignment of Class I to the manufacturing classes narrows because of the differences in how the skim is paid for. When this happens, it becomes more difficult to attract milk to Class I markets. That’s one example of disorderly marketing. PPD erosion and depooling of more valuable manufacturing class milk is another example.

Covington explained the impact of this misalignment on moving milk from surplus markets to deficit Class I markets, that the lower skim value becomes a disincentive.

Vitaliano explained the depooling issue as “creating disorderly marketing conditions also, and great unhappiness when one farm is paid a certain price and another handler pays a different price (in the same marketing area). That’s disorderly unhappiness for the Federal Order program,” he said.

He noted that the fundamental reason for pooling is to take the uses in a given area with different values to achieve marketwide pooling where producers in that Federal Milk Marketing Area are paid similarly, regardless of what class of product their milk goes into.

“This removes the incentive for any one group to undercut the marketwide price to get that higher price (for themselves),” he said. “The Orders create orderly marketing with a uniform price. Depooling undermines that fundamental purpose that is designed to create orderly marketing.”

Either way, whether indirectly paying to bring supplemental milk into Class I markets from markets with higher manufacturing use, or in the case of depooling, the dairy farmers end up paying for the fallout from this erosion of the PPD.

Since the beginning, even before 2000 Order Reform, figuring the Class I base milk price had to begin somewhere, according to Covington. Federal pricing has always used the manufacturing class values in determining that base fluid milk price.

The trouble today is that Class III and IV handlers pay farmers per pound of actual skim components in the milk they receive, while the Class I handlers pay per hundredweight based on an arbitrary outdated national average skim component standard. Thus, the “opportunity cost” of moving this now higher component milk to manufacturing classes that pay by the actual pound of protein, for example, instead of by the old standard average protein levels is not accounted for in the Class I price that still uses the old standard average levels.

Pressed again on how it makes sense to raise Class I prices by raising the component level of the skim to more adequately reflect the national average today, Covington said: “It adds to the nutrition, and I stand by that. In proposal one, the price will go up (estimated 63 cents per cwt or a nickel per gallon). I am comfortable charging that extra price to Class I processors.”

Attorney English, representing MIG, retorted that, “The handlers who buy milk and then by adding a neutralizing agent remove the lactose, they’re going to pay more for the milk that they then have to process to subtract the lactose.”

Covington responded that, “There are consumers who think about lactose. There are consumers who buy lactose-free products, yes, because it is on the shelf, but it’s not all consumers.”

On the higher protein, English asked Covington how Class I processors are supposed to monetize that protein in a label-less commodity, a commodity that is declining in its share of total milk utilization?

“We are still selling 45 billion pounds of packaged fluid milk (annually) in this country,” said Covington. “Consumers wouldn’t buy that 45 billion pounds if it wouldn’t have some nutrition.”

English argued that milk is sold as whole, 2%, 1% and non-fat. It is not sold by its protein, so isn’t it “so highly regulated in ways that alternatives are not that any increase in price hinders sales of fluid milk?”

Covington acknowledged that, “yes, it is regulated, but I’m not convinced that this proposal will hinder fluid milk sales. Again, (higher components) add to the nutrition and I stand by that.”

Opponents kept coming back to these value questions, while proponents focused on the price alignment issue and orderly marketing.

CARMEL, Ind. — USDA’s much anticipated national public hearing of 21 proposals on amendments to uniform pricing formulas for all 11 Federal Milk Marketing Orders (FMMO) had a rocky start on Wednesday, Aug. 23 in Carmel, Indiana. The first day kicked off amid objections to the hearing scope as fluid milk processors were seeking to get their excluded Class I proposals onto the docket.

The presiding administrative law judge set the stage for what he said will be an estimated 7-week hearing, held 8 to 5 ET every weekday with virtual farmer testimony on Fridays. (It is being livestreamed for watching by zoom or listening by phone. Look for that information in the graphic above, or find the links and numbers at the end of this article or at the hearing webpage).

The judge stated his authority to interrupt for comments or testimony outside of the hearing scope. “I will not issue a decision,” he said. “USDA will take the information to render a decision.”

Once a recommended decision is put forward by USDA, expected in February or March 2024, a comment period follows before the final decision is issued in June or July and made fully effective in the fall of 2024. Some proposals call for a 12-month delay in implementation, so the full effect of potential decisions could be delayed until fall of 2025.

Given the rocky start to the hearing, even this timetable could be prolonged, but USDA is under a Congressional mandate to render decisions within 18 months of a petition it agrees to hear.

Immediately following the setting of the stage, Chip English, attorney for the Milk Innovation Group (MIG) put forward an objection and a motion seeking reversal of USDA’s decision that excluded two of its Class I pricing proposals from the hearing announcement. One of the excluded proposals would exempt organic milk from FMMO pools and the other deals with ‘shrink’ in the extended shelf life category.

Attorney Chip English for the Milk Innovation Group (MIG) kicks off federal milk pricing hearing with objections to scope, saying two of their Class I pricing proposals were improperly excluded. Screen capture from livestream of first day of 7-week national public hearing on federal milk pricing formulas

“It’s all coming in whether you like it or not,” said English, “because at the end of the hearing, we’re going to be talking about raising Class I, and these are issues that have to be part of that.”

Attorney John Vetne for National All Jersey joined in the objection on procedural grounds because NAJ also had its proposal to make all 11 FMMOs use multiple component pricing was rejected from the hearing. Currently, the 3 southern marketing areas and Arizona are fat/skim priced, whereas the other 7 marketing areas use multiple component pricing (MCP). USDA excluded this proposal since the 4 fat/skim priced marketing areas must regionally call for the change to MCP pricing.

Within the first hour and a half of the first day, the hearing went “off record” into private discussion about handling the objections and handling the exhibits.

In addition to the hearing scope objections, there was extensive cross-examination of USDA AMS Dairy Program staff on its fulfillment of data requests and various exhibits provided by USDA — in some cases calling into question the comparability or reliability of some of the data.

For example, much was made of the differences between the USDA mailbox milk price report as compared to the Federal Order price announcement. Mr. English probed USDA staff on how these reports are audited, how the data is collected, what is included and what it is based on. He did what he has done in Pennsylvania Milk Marketing Board (PMMB) hearings in the past to discredit the comparability of the mailbox price report to state or federal “announced price” reports — because of the differences in the “auditing”.

As each exhibit on pooling figures and other data was put under the cross-examination microscope, the issue of “restricted” data came up due to “confidentiality,” which USDA staff explained is necessary when 2 or fewer companies are in a marketing area — be they plants or farms. In the rapidly consolidating dairy industry, what does this foretell of future market transparency if data are not available for price discovery and market transparency because of too few operators in a region?

There were attempts to keep some exhibits from being included in the hearing record. Most of these discussions were put on hold to be explored through further cross-examination at a later time with future witnesses.

In many ways the sense of this round of cross-examination on exhibits felt a bit like cutting the legs out from under future presentation of proposal testimony even before they get to the floor. Basically, much legal maneuvering on data before the first proposal is even heard and testified to.

If the first day is any indication of what is in store, expect to see many attempts to push the scope boundaries, and expect the judge to err on the side of making sure USDA has all of the information it needs to render decisions, so some latitude will likely be given for these boundary explorations by attorneys.

Attorney English, is well known to any Pennsylvania dairy farmer who has ever sat in on a PMMB hearing in Harrisburg. He has represented Dean Foods and the Pennsylvania Milk Dealers in past years on the price-setting hearings conducted by the PMMB. In fact, the esteemed milk accountants of Herbein and Co. in Pennsylvania are providing material for some of the MIG opposition arguments to come. Cheap Class I milk is the name of the current game.

The MIG will be working overtime through Mr. English to make sure Class I prices are not raised, and in fact are lowered at the farm level since one of their proposals that WAS accepted by USDA is to remove the base Class I price differential of $1.60/cwt from every FMMO — across the board.

Who is the MIG? The Milk Innovation Group members include Anderson Erickson Dairy Co., Inc.; Aurora Organic Dairy; Crystal Creamery; Danone North America; Fairlife; HP Hood LLC; Organic Valley/CROPP Cooperative; Shamrock Foods Company; Shehadey Family Foods, LLC (Producers Dairy Foods, Inc.; Model Dairy, LLC; Umpqua Dairy Products Co.); and Turner Dairy Farms.

After lunch, some high points of the first day included Dr. Roger Cryan for American Farm Bureau Federation requesting volume data on all of the salted and unsalted butter that is graded by USDA AMS for retail. This, he said, is four numbers and should be readily available. It is germane to AFBF’s proposal to include unsalted butter in the product price survey used in the Class IV pricing formula.

Testimony began late in the afternoon on the first proposal from NMPF to raise component levels in the uniform pricing formulas to more accurately reflect today’s protein and other solids levels.

Peter Vitaliano, NMPF’s vice president for economic policy and market research, laid out the proposal and was subjected to intense cross-examination with the promise of hours more of cross examination on the second day by Mr. English before even getting to the first expert fact witness — Calvin Covington, for Southeast Milk and NMPF.

While NMPF witnesses will show the outdated component levels are giving a ‘deal’ to Class I processors paying less for skim that is more valuable today in terms of components, IDFA’s attorney Steven Rosenbaum grilled Vitaliano on this. He tried on seven attempts to establish that the fat/skim orders in the Southeast don’t have component levels as high as the national average by asking for this breakout in seven differently-phrased questions, all the while discreetly suggesting that this change would “overpay” producers in fat/skim orders.

He also questioned how fluid milk processors are supposed to recoup that value if it doesn’t “fill more jugs of milk”. Vitaliano responded to say that protein beverages are a big deal to consumers, and some milk marketing is being done on a protein basis. Rosenbaum asked for a study showing how many fluid processors are doing that, and then basically said, in lawyer speak, the equivalent of ‘never mind,’ as Vitaliano interjected that it’s more valuable to consumers.

In this reporter’s mind, the thought that kept popping up during that exchange was this: If IDFA and MIG are so intent on suppressing the Class I price to avoid paying for the improved value of milk, then maybe they should then start forking over their cost data in audited surveys to the USDA to justify the $3.60 per hundredweight they are getting subtracted from the base Class I price in the form of Class III and IV make allowances that do not even apply to them, but they get that deal anyway.

These are just a few thoughts from an intense first day of the national FMMO hearing that NMPF is calling the “first in a generation opportunity” to make key adjustments to the milk pricing formulas to reflect a changing dairy industry. It appears that many of their proposals will help farmers… We’ll see over the next 6 to 8 weeks where it’s all going.

In the meantime, Congress may want to think about fixing the Class I mistake it made in the 2018 farm bill by changing four simple words from ‘average plus 74 cents’ to ‘higher of’ and at least get that done timely.

This hearing could leave that objective in the dust if the first day is an indication of what is to come.

Information to tune in by livestream through zoom or to dial-in and listen from a cell phone or landline has just been announced.

Or listen via one tap mobile: +1.646.828.7666, using ID 1604805748#

Or listen via landline telephone: +1.669.254.5252 and enter ID 160 480 5748

The hearing schedule will proceed in this order to consider accepted proposals under these categories, according to USDA:

1. Milk Composition (component yield) proposals.

2. Surveyed Commodity Prices (removing or adding commodities to the weekly price surveys used in the class and component pricing formulas).

3. Class III and IV Formula Factors, which includes various ‘make allowance’ proposals as well as butterfat recovery factors, and farm-to-plant shrink.

4. The Base Class I Skim Price (Mover) Formula (6 proposals, 3 favoring return to ‘higher of’, including 2 that also favor eliminating ‘advanced pricing’ of Class I. )

WASHINGTON –- USDA officially announced Monday (July 24) the national public hearing to consider proposals seeking to amend the uniform pricing formulas across all 11 Federal Milk Marketing Orders (FMMO). The hearing begins Wednesday, August 23, 2023 at 9:00 a.m. at the 502 East Event Centre, 502 East Carmel Drive, Carmel, Indiana.

Farmers will be able to testify in person at any time, or virtually on Fridays by pre-registering.

Approximately 40 proposals were submitted by 12 organizations and were explained during a webinar in mid-June. Of those, 21 will be considered within the uniform pricing scope of the hearing, according to the USDA notice. Copies of the notice, a list of proposals being considered, guidelines for how to participate, the hearing schedule, and corresponding hearing record can be found and followed on the Hearing Website.

The Class I mover formula will be addressed in the national hearing’s scope, including the proposals from National Milk Producers Federation and American Farm Bureau to go back to the ‘higher of’ method. The change from ‘higher of’ to ‘average of’ was made legislatively in the 2018 farm bill without a hearing.

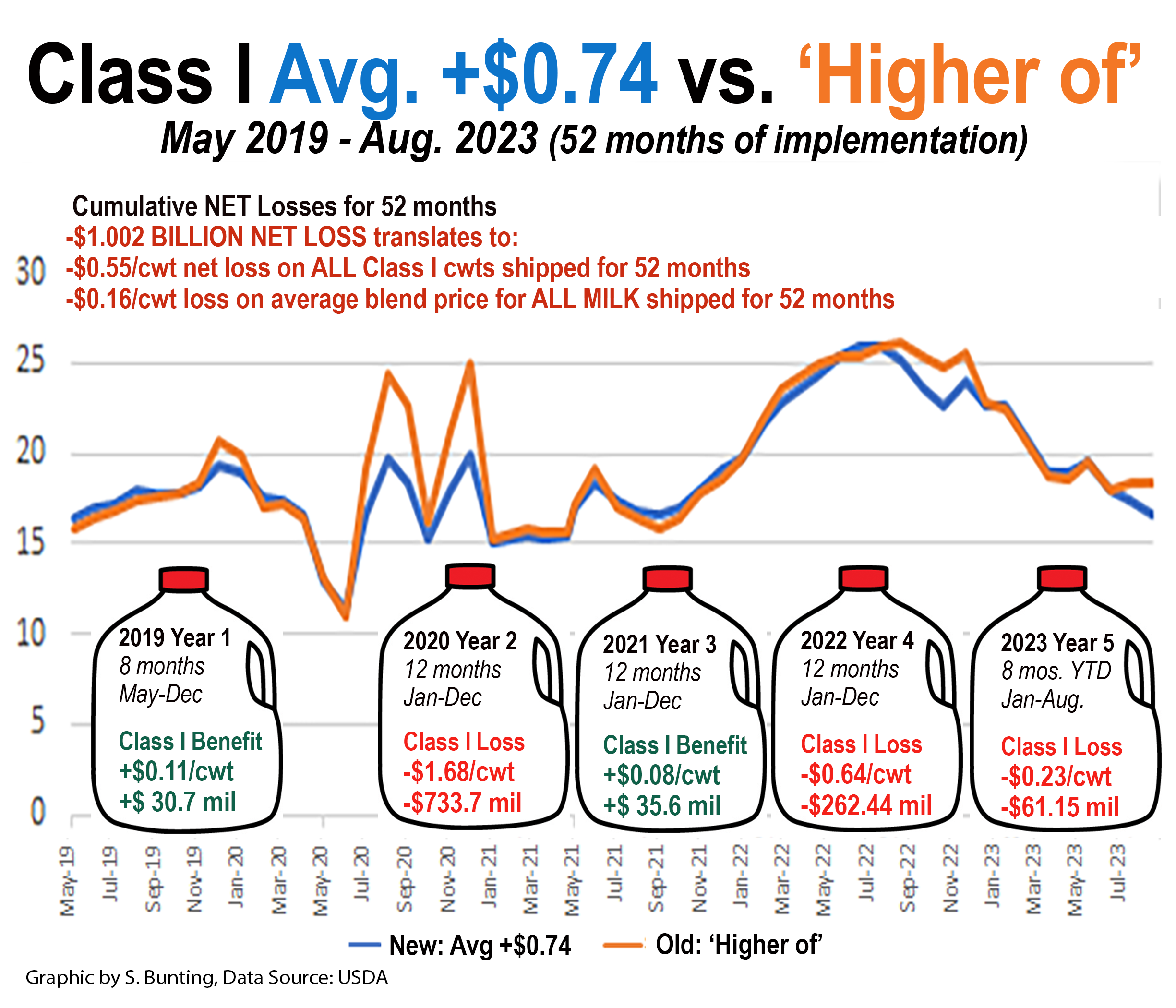

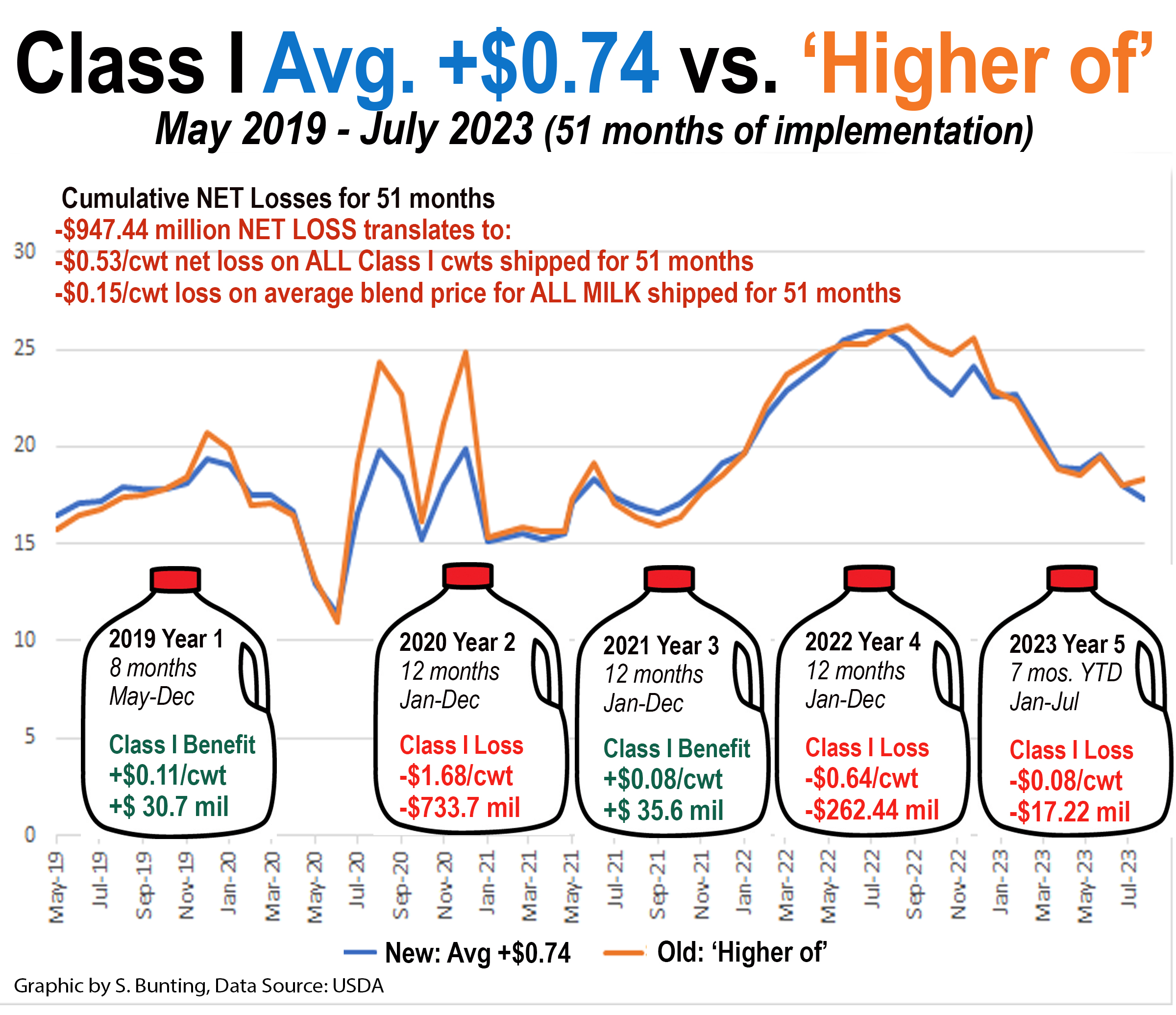

Since USDA implemented the ‘average of’ method in May 2019, net losses from this change are projected to exceed $1 billion after August 2023 milk is paid for in September.

On July 19, USDA announced the August advance Class I price mover at $16.62. If the previous ‘higher of’ method had been used, the Class I base price would have been $18.29. That’s a $1.67 per hundredweight loss on all Class I milk next month. July’s Class I mover was also calculated substantially lower (by $1.02) using the ‘average of’ vs. the ‘higher of.’ These losses will impact August and September milk checks for July and August milk.

Around 28% of all milk produced in the U.S. is Class I fluid use, so farmers stand to lose an additional 47 cents per hundredweight on all of the milk they market in August and 29 cents on all the milk they market in July — just from this formula change. This is on top of the market declines in the class and component prices. The loss to blended prices will be greater in some Federal Orders and less in others, and this does not include the impacts from de-pooling of higher-value Class IV milk.

The impact of the two-week Class I advance pricing factors is compounded by the ‘average of’ method, which is quite notable for July and August. Cheese and whey were in a tailspin lower; however, on the very next day after the August Class I base price mover had been averaged and locked-in on July 1-15 pricing factors, the dairy product markets began a huge rally, with cheese gaining nearly 40 cents in 8 trading sessions. This boosts the other class and component values much higher for the latter half of the month.

Over the 52 months of its implementation, the ‘average of’ formula has effectively removed an estimated 55 cents per hundredweight from farmer payment for all Class I milk, according to USDA data. On a blended uniform price, this comes out to a national average loss of 16-cents on every hundredweight of all milk used in all classes of products shipped from May 2019 through August 2023. That is like paying another checkoff for 52 months.

Among the other proposals included in the national hearing is the American Farm Bureau (AFBF) Class I and II proposal that seeks return to the ‘higher of’ with additional adjustments such as eliminating the two-week ‘advanced’ pricing.

IDFA’s Class I proposal seeks to keep the ‘average of’ and use either the current 74-cent-adjuster or a ‘rolling adjuster’ based on a calculated difference over 24 months, whichever is higher.

Milk Innovation Group’s (MIG) proposal seeks to keep the ‘average of’ but change the ‘adjuster’ monthly via a 24-month look-back with a 12-month lag.

Two Edge Cooperative proposals are included, one being a Class III-plus formula. The other would use the ‘higher of,’ but would base it on end-of-month four-week announced class and component prices instead of the two-week prior month advance pricing.

The hearing docket also contains four proposals on Class I differentials, including NMPF’s proposal to increase them in all locations by varying amounts as well as MIG’s proposal to lower them across the board by $1.60.

Two proposals from NMPF and National All Jersey will be heard to update milk component factors.

Six proposals will be heard on Class III and IV pricing formulas. Three are separate proposals from NMPF, IDFA and Wisconsin Cheesemakers to update processor credits, known as ‘make allowances,’ as well as three from Select Milk Producers on butterfat recovery, farm to plant shrink and nonfat solids yield.

In addition, the hearing scope includes four proposals on how dairy commodity products are surveyed, including NMPF’s proposal to remove 500-lb barrel cheese from the weekly survey, AFBF’s proposal to add bulk 640-lb block cheese and unsalted bulk butter, while California Dairy Campaign’s proposal would add mozzarella.

Dairy farmers can testify in-person at any time during the hearing, or virtually on Fridays. Beginning Fri., Sept. 1 and for each Friday thereafter until the hearing concludes, dairy farmers may testify virtually in 15-minute time slots beginning at Noon ET. There will be 10 slots for virtual testimony each Friday.

To be included, farmers must pre-register. The pre-registration for each Friday’s time slots will be available starting Monday of the same week at the USDA Hearing Website. For example, the link to testify on Fri., Sept. 1 will be available on Mon., Aug. 28. To submit exhibits for the record, email them to FMMOHearing@usda.gov by 8:00 a.m. ET on the day of testimony.

Those participating in the hearing in person should notify a USDA official upon arrival at the hearing. For additional information, contact Erin Taylor, Director, Order Formulation and Enforcement Division, USDA/AMS/Dairy Program at Erin.Taylor@usda.gov.

Consensus evident on some key proposals, such as returning the Class I mover formula to the ‘higher of’; but 10 packages contain over 30 variations and a few new biggies.

New to the party are:

AFBF wants to end ‘advance’ pricing of Class I;

NAJ wants uniform component-based pricing of Class I in all Orders;

MIG, made up of 7 fluid processors want organic exemptions, an assortment of new credits, and they want to knock $1.60 off the Class I differentials, forgetting they already get over $3.00 in ‘make allowance’ credits while not incurring those costs

California Dairy Campaign seeks an extension to consider alternative pricing formulas

Some proposals want to drop products (500-lb barrel cheese) from the FMMO formulas and price surveys, others want to add products (ie. 640-lb block cheese, mozzarella, unsalted butter)

Dana Coale, Deputy Administrator (top, left) and Erin Taylor, Director (top, right) and their USDA Dairy Division staff engaged with leads for 30 hearing proposals contained in packages submitted by 10 organizations in the pre-hearing information session Friday, June 16. Tim Doelman (bottom), CEO of Fairlife, a Coca-Cola subsidiary, explains one of the Milk Innovation Group’s (MIG) proposals that bucks the consensus on going back to the ‘higher of’ in setting the Class I mover. MIG wants to keep the averaging method with their ‘Floored Adjuster” proposal. He said returning to the ‘higher of’ prevents processors from forward-pricing their milk like soda and other beverage companies do for other ingredients. MIG also wants to knock $1.60/cwt off the current Class I differentials, and they want an assortment of new credits (obviously forgetting that fluid milk processors already get more than $3/cwt in various Class III and IV product manufacturing credits. These so-called ‘make allowances’, are built in as credits on the Class I and II prices also, for costs that fluid processors do not incur.) Zoom screen capture

BySherry Bunting, Farmshine, June 23, 2023

WASHINGTON – In preparation for a potential national Federal Milk Marketing Order (FMMO) hearing, the Dairy Division of USDA’s Agricultural Marketing Service had a pre-hearing information session Friday, June 16. During the day-long session, held virtually through zoom, Deputy Administrator Dana Coale, Director Erin Taylor and others heard presentations of the more than 30 pieces contained in proposals submitted by 10 organizations, and they engaged in questions for clarification as well as accepting requests for data before the 10 proposals were to be modified for final submission June 20.

While the Secretary of Agriculture has not yet declared a hearing, the AMS Dairy Division has publicized the timelines and action plan.

Coale stated that mandated time frames by Congress, govern the amount of time from the point at which a proposal is received to the end of a hearing 120 days later. “All of our proposed time frames are based on keeping us focused to meet the 120-day mandate,” she said.

“Once submitted, USDA will further evaluate them, and the Secretary will make the determination,” said Coale. “If the Secretary intiates rulemaking, you will see a hearing notice containing all proposals to be heard. This will be mid- to late-July, and we would expect to move forward – if a hearing is initiated – on Aug 23 as the start of that hearing.”

The location will be Carmel, Indiana, and because of the new time constraints, new procedures will be put in place, she said.

“Expect to see a very different process than customarily done to create a very efficient process while maintaining transparency and a robust evidentiary record,” she explained, noting this includes a process for submitting testimony in advance, and a naming vs. numbering convention for exhibits.

After the hearing is noticed, there will be another information session, said Coale.

“It takes an entire village,” she stressed. “Ex parte communication does not begin until a hearing is noticed, so if you have questions or need explanation or discussion on data for submitted proposals, contact us at fmmohearing@usda.gov”

The marquis proposal is the comprehensive package submitted by National Milk Producers Federation (NMPF) that set into motion the Secretary’s call for other proposals. The NMPF package has five proposals, previously reported in Farmshine through various articles since the October stakeholders meeting hosted by American Farm Bureau in Kansas City in October 2022.

Retired cooperative executive Calvin Covington is the lead on one of the five NMPF proposals, which seeks to update skim components to more accurately reflect the percentage of protein, nonfat solids and other solids in a hundredweight of milk today.

Covington said he also expects to testify on the NMPF proposal to raise Class I differentials with a new pricing surface map, something that has not been done since 2007-08, and the proposal to return the Class I base price ‘mover’ to the ‘higher of’. The current average plus 74 cents method has been in place since May of 2019, which produced unintended consequences and losses for dairy farmers.

In a phone interview Tuesday, June 20, Covington explained that after more than a year of task force meetings and discussions via NMPF with its members and their farmer members, “We’ve gotten this far, and we have got a consensus,” he said of the NMPF package.

In addition to updating skim components and Class I differentials and changing the Class I ‘mover’ back to the ‘higher of,’ the NMPF package includes a proposal to modestly update make allowances and to discontinue the barrel cheese price in the Class III protein formula while allowing 45-day forward-priced nonfat dry milk and dry whey to be included in the formula price survey instead of the current 30-day forward-price limit.

“It took a year, and that’s pretty good, to have coast-to-coast consensus on five major proposals,” said Covington. “Then you also read the Farm Bureau’s proposal and there’s pretty good consensus there too.”

Central to both the NMPF package and AFBF package of proposals is strong support for returning the Class I mover formula back to the previous ‘higher of’ method.

(Farmers have had a cumulative net loss of nearly $950 million, equivalent to losing 53 cents on every hundredweight of milk shipped for Class I use for the past 51 months or 15 cents per hundredweight on the FMMO blend price for all milk across all 51 months — since the change to ‘average of’ was made in May 2019 via the 2018 Farm Bill. In fact, the July 2023 Class I mover was announced June 22, 2023 at $17.32, which is a whopping $1.02 below the $18.34 it would have been under the ‘higher of’ method.)

AFBF supports NMPF’s proposal to restore the Class I mover to the ‘higher of’ Class III or IV, to drop the barrel cheese price from the Class III component and price calculation, to update component values into Class III and IV formulas, and to update Class I differentials, but notes this should be done through careful review where changes are based on a transparent record.

AFBF chief economist Roger Cryan stated that AFBF will defer to NMPF for substantiation on the Class I mover change, but if by any chance NMPF would back away from this proposal, Farm Bureau wants it kept on the table and will defend it.

On adjustment to Class III and IV product make allowances, AFBF supports this under the same logic as the NMPF proposal, but states that “such adjustment cannot be fairly undertaken except in using the data from a mandatory and audited USDA survey of, at least, those plants participating in the National Dairy Product Sales Report (NDPSR) survey.”

The difference is NMPF says it will seek mandatory surveys through legislation, whereas AFBF sees USDA as already having the authority to do this.

AFBF’s package includes some “new” proposals as well. One would add 640-pound block cheese to the Class III component and price formula and the NDPSR survey and another would add unsalted butter to the butterfat and protein calculation and the NDPSR survey.

AFBF includes a proposal to update the Class II differential to $1.56 to account for current drying costs and to adjust formula product yields and include an adjustment to the ‘make allowances’ for cooperatives and plants that “balance the market.”

The AFBF package also cites “universal milk check transparency requirements” regarding clarity to be shared on producer milk checks regarding pooled volume, Order value and actual payment for pooled and nonpooled milk.

AFBF seeks a seasonal Class I differential adjustment to “address seasonal differences in supply and demand.”

The most notably divergent AFBF proposal is one that seeks to eliminate the advanced pricing of Class I milk and components and the advanced pricing of Class II skim milk and components. It would base both on the 4-week “announced” Class III and IV components and prices instead of the 2-week “advanced” pricing factors. The advanced factors are calculated for a given month during the first two weeks of the previous month and have been part of FMMO pricing for decades.

Edge Dairy Farmer Cooperative, representing farmers in nine Midwest states shipping to 34 processors also proposes ending advanced pricing of Class I.

MIG is made up of seven companies — Anderson Erickson Dairy, Aurora Organic Dairy, Danone North America, Fairlife, HP Hood, Organic Valley/ CROPP Cooperative, and Shamrock Foods.

They want to REDUCE Class I differentials, whereas NMPF and AFBF support updates that increase them.

MIG companies want to establish Class I differentials that remove the “Grade A compensation” portion that has been built into all Class I differentials from the beginning, as well as removing the “market balancing compensation.”

Together, these removals would account for the $1.60 per hundredweight base differential that all FMMOs receive. As explained in the pre-hearing session, this would have the net effect of reducing Class I differentials (and producer pay prices) by $1.60 per hundredweight across all FMMOs.

In their justification, MIG writes that it is “far past time for the base Class I differential to be reconsidered in light of market changes, including the exploding growth of dairy beverage alternatives… and the exponential growth of non-fluid milk products often sold in the export market.”

(In this reporter’s analysis and opinion, reducing Class I differentials instead of raising them, ignores the fact that every Class I fluid milk processor – including the aseptic, ultrapasteurized, organic, ultrafiltered and other ‘specialty’ fluid milks – are already getting more than $3.00 per hundredweight embedded as a processor credit in the Class I base price mover by virtue of the cumulative sum of all product make allowances on the Class III and/or IV pricing factors used to establish that mover, but since they don’t make Class III and IV product, they don’t incur these costs. Now they want $1.60 more, plus “assembly” and other credits?)

The MIG also proposes exempting processors of Class I organic milk from paying into FMMO pools as long as they show they pay their producers at least the minimum FMMO price. There are a few other guard rails to this.

They also want to receive “assembly credits,” specialty credits, and a higher shrink credit (forgetting that they already get make allowance credits that don’t even apply to them).

Citing the “unequivocal decline in Class I sales,” the MIG sets the stage with its package of proposals to transition further away from pricing mechanisms that support local fresh milk in favor of aseptic, extended shelf-life milks and specialty products. Some of the companies in the MIG are making dairy beverages that are not even Class I, and several are getting big into plant-based and other non-milk alternatives and blends. (Is that a conflict of interest?)

USDA AMS also accepted further information on the prior petition by the International Dairy Foods Association (IDFA) and Wisconsin Cheese Makers Association (WCMA) to update make allowances. With this additional information, their petitions are back on the table and are based on voluntary cost surveys.

The IDFA alternative is described as using the current simple average of the Class III and IV advance pricing factors to set the base Class I price, and floor the adjuster at the current 74 cents — while allowing that adjuster to increase if a two-year look-back shows it was deficient vs. the higher of. This is a complex two-years back “making producers whole” in the two-years forward with the adjuster always being floored to go no lower than 74 cents even if it turns out that this method benefited farmers vs. the ‘higher of.’

The IDFA Class I proposal contains several pages of justification for the averaging method built around “preserving price hedging and risk management” for processors, particularly those in the ‘value-added’ category,” such as ultrafiltered and aseptic Class I milk products.

But it doesn’t end there…

National All Jersey (NAJ) brought forward its proposal, explained by Erick Metzger. “One mirrors NMPF’s proposal to update skim component factors in the Class III and IV formulas, except we want to see it be a simple annual update based on the previous year’s average, with an appropriate lag time to address risk management tools instead of being based on a three-year average,” he said.

In addition, NAJ proposes that FMMOs 5, 6, 7 and 131 (the Southeastern Orders and Arizona) become multiple component pricing (MCP) Orders instead of pricing on a fat/skim basis.

NAJ also proposes Class I payment requirements to be based on MCP pricing instead of skim / butterfat in all FMMOs, nationally.

“We are proposing uniform pricing across all orders — both on how processors pay for components and how producers are paid for components,” said Metzger. “Extensive updates are needed to Orders 5, 6, 7 and 131, and the needed Order language already exists in the other Orders.”

The NAJ proposal notes that Class I should be paid on actual solids, instead of valuing the skim on a skim basis. “In our proposal, it would be valued or priced on actual skim components,” he said.

What this means is if a dairy farm’s actual components processed (in Class I) were below the standard components in the Class III or IV formulas, the processor obligation would be less; and if the farm’s skim components are greater than the standard, then the obligation of Class I processors to the pool would be more. In short, accounting for actual skim components in the NAJ proposal, would replace the current pricing of Class I skim on a pounds of skim basis.

Select Milk Producers cooperative submitted proposals to update product yields to reflect “actual farm-to-plant shrink,” to update the butterfat recovery factor and to update nonfat solids yields. According to their own limited 5-year-average analysis the three proposals combined would net 13 cents/cwt on the Class III price and 42 cents/cwt on the Class IV price, but they’ve requested more data from USDA AMS to analyze — if their proposals are accepted for a hearing.

For its part, Edge Cooperative states in a cover letter to its proposals that a hearing should occur after the farm bill. “There is no imminent crisis that would present a compelling reason to initiate a hearing before the next farm bill is enacted,” the proposal states.

In the farm bill, Edge seeks a mandatory cost of processing survey before make allowance updates could be heard. Edge also seeks legislative language to expand flexibility to base individual FMMOs around something other than uniform pricing, to be determined on an Order by Order basis. This “flexibility” was explained by Lucas Sjostrom and Marin Bozic at the Farm Bureau stakeholders meeting in Kansas City last October.

However, Farm Bureau’s package of proposals asserts that there is no reason to hold off on a hearing while waiting for a farm bill, and indeed seeks the fastest resolution to the Class I ‘mover’ issue. Furthermore, Congress previously mandated timelines that don’t allow “waiting” once proposals are received by USDA. This process is in motion, unless Secretary Vilsack refuses a hearing on any of the proposals.

AFBF, in fact, cited areas of the Agricultural Agreement Act that give USDA authority to do mandatory cost surveys, without further legislation, because the Secretary has discretion to require any reporting deemed necessary from FMMO participating plants.

On the Class I ‘mover, Edge proposes two options, either a Class III-plus option if the ‘advanced pricing’ is retained or if the ‘higher of’ option is used, then to base it on final 4-week announced skim milk prices each month. This option would effectively end the 2-week advanced pricing factors and advance pricing of the Class I ‘mover,’ which has also been proposed by AFBF.

The Edge proposals include a request to align make allowance changes so that they don’t impact ‘risk management tools’ and a proposal to add Order formulation language about the information handlers shall furnish to producers with the intent of “transparency in producer milk checks.”

The California Dairy Campaign’s proposal asks USDA to extend the proposal deadline and to add mozzarella to the Class III component and price formula and the NDPSR survey. They also want consideration of “alternative pricing formulas that guarantee dairy farmers are paid according to current market rates.”

The California proposal includes a National Farmers Union (NFU) Dairy Policy Reform Special Order of Business that was passed at the 2023 NFU Convention in San Francisco. It states opposition to the call for a federal milk marketing order hearing, noting that, “If a hearing is granted, it is essential that any modifications to the federal order minimum pricing formulas take into account the volume and value of all dairy products, particularly high-moisture cheeses such as mozzarella.”

DPA also proposes a supply-balancing feature, whereby milk handlers notify farms at least 7 days prior to milk disposal action, stating the baseline production needs, how much to reduce production, and for how long, with farmers making this reduction by dumping (or not producing) this milk.

In effect, the DPA proposal includes a processor-led supply management program, not a government intervention. But to do it, the FMMOs would be the arbiter, and therefore all Orders would have to be amended to require 100% mandatory participation and pooling of all U.S. milk. Something like that may require legislation since a producer referendum bloc-voted by cooperatives could vote it down, and it’s unclear how unregulated areas would be included since states like Idaho already voted the FMMOs out.

Currently, only Class I milk handlers are required to participate in FMMOs within marketing areas that have FMMOs. Participation is voluntary for most Class II, III and IV processors. Over the past three years, roughly 60% of total U.S. milk production has been pooled on FMMOs.

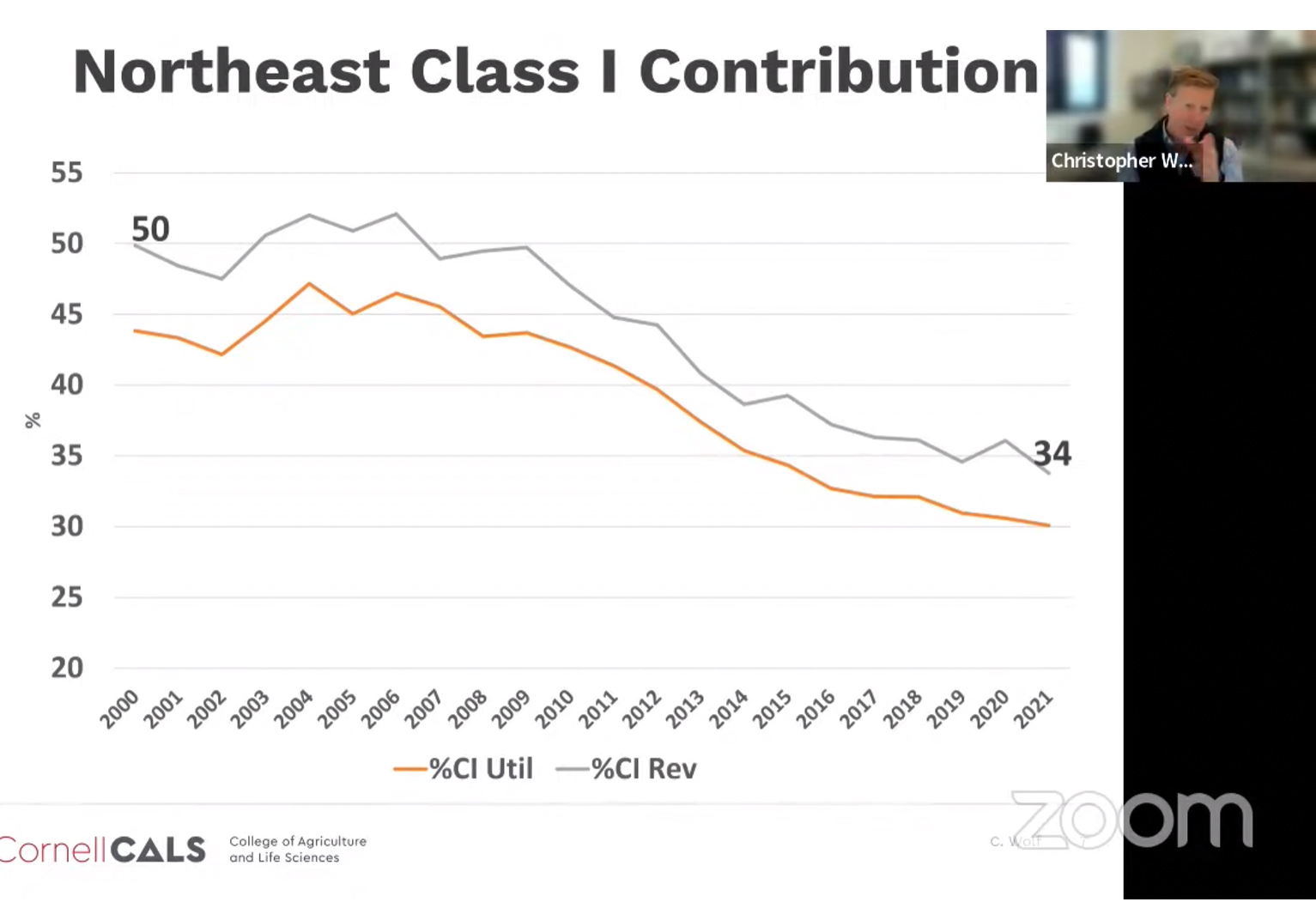

Using the Northeast as an example of a multiple component pricing Federal Milk Marketing Order that still has significant Class I utilization, Dr. Chris Wolf showed how long-term trends and other factors have reduced the Class I utilization and Class I revenue from 50% in 2000 to 34% in 2021 in FMMO 1. The most dramatic part of this decline occurred after 2010 — leaving not enough money to go around with less Class I value in the pool. FMMOs were structured for Class I fluid markets not for the dairy product and export markets where growth is occurring today. Screen capture from Center for Dairy Excellence Protecting Your Profits webinar with CDE’s Zach Myers and his guest Dr. Chris Wolf, Cornell University dairy economist.

By Sherry Bunting

WASHINGTON – There are irons in two fires when it comes to federal milk pricing and dairy policy. One is to do modernization through the Federal Milk Marketing Order (FMMO) hearing petition process. The other is to make some adjustments or seek authorizing language through the dairy title of the 2023 Farm Bill.

On the farm bill front, the May 12 CBO baseline score shows this could be the first trillion-dollar farm bill. Food assistance programs, like SNAP, are eating into the capacity to do other things, say top-level staff for the Senate Ag Committee.

For dairy and livestock, the Dairy Margin Coverage (DMC) baseline now includes $1 billion in additional outlays projected over the 10-years, while livestock disaster outlays have doubled – even without making any changes in these programs that some are suggesting.

Still, farmers and organizations that represent them are seeking some expansion for the DMC, livestock disaster, and other programs and safety nets, and some are seeking language to instruct the Secretary to do hearings on the Class I ‘mover’, or to expand the flexibility of the scope of a hearing, or to require mandatory reporting germaine to things like raising make allowances.

The jury is out on whether a farm bill gets done by September 2023 after the May 12 baseline was announced by CBO in the current political environment, but members of the House and Senate Ag Committees and their chairpersons are gathering information in earnest toward that goal.

On the FMMO hearing front, as previously reported in Farmshine, the USDA responded April 28 to the March 30 petitions from two processor organizations by asking for more information instead of granting or denying a hearing on their make allowance update request.

The two petitions from International Dairy Foods Association (IDFA) and Wisconsin Cheese Makers Association (WCMA) both requested a hearing focused exclusively on updating the ‘make allowances’, which are processor credits that are subtracted from the wholesale end-product prices used to derive farm level milk class and component prices.

Make allowances were last updated in 2008 using 2006 plant cost data.

Four days later on May 2, the National Milk Producers Federation (NMPF) submitted its petition seeking an FMMO hearing on a range of national amendments.

NMPF is petitioning USDA for a hearing on these five items:

1. Increase make allowances in the component price formulas to the following levels: Butter $0.21 per pound, Nonfat dry milk $0.21 per pound, Cheese $0.24 per pound, Dry Whey $0.23 per pound

2. Discontinue use of barrel cheese in the protein component price formula

3. Return to the “higher-of” Class I mover

4. Update the milk component factors for protein, other solids, and nonfat solids in the Class III and Class IV skim milk price formulas

5. Update the Class I differential pricing surface throughout the U.S.

Not noted within this list is a point that NMPF’s board approved on the legislative front, and that is to seek language in the 2023 farm bill directing USDA to do periodic mandatory and audited plant cost surveys instead of voluntary surveys for future hearings on make allowances.

The American Farm Bureau Federation took a positive approach in their response letter to USDA, showing support for the fact that NMPF’s petition is comprehensive and includes areas of strong consensus among farmers such as returning the Class I mover to the ‘higher of.’

However, AFBF president Zippy Duvall also points out in the response letter that the Secretary of Agriculture already has the authority under the Agricultural Marketing Agreement Act to require processors to provide information relevant to FMMO pricing. This could include mandatory surveys of plant cost data when used to determine the processor credit, or make allowance, in the pricing formulas.

It is Farm Bureau’s position that make allowances should only be updated based on mandatory and audited plant cost surveys.

This leaves a bit of a loophole in the discussion about how to acquire the data to make current or future updates. The Secretary may have the authority to require data from plants that participate in FMMOs. However, it is unclear if the Secretary has this authority to require cost data from plants that do not participate in the FMMOs.

The end-product pricing formulas are based on wholesale prices that are collected mandatorily by USDA AMS on a weekly basis through the Livestock Mandatory Reporting Act on only those products that are used in FMMO formulas. This includes butter, nonfat dry milk, dry whey and 40-lb block and 500-lb barrel cheddar cheese.

The USDA AMS weekly National Dairy Product Sales Report surveys 168 plants for this price data. Therefore, if make allowances are updated as processor credits against those prices, then all 168 plants should have to report their costs, and only the costs that pertain to those specific products, whether or not they participate in FMMOs. In a recent voluntary cost survey, more than 70% of those plants did not report their cost data.

During a Center for Dairy Excellence Protect Your Profits zoom call recently, risk management educator Zach Myers had as his guest Cornell dairy economist Dr. Chris Wolf to talk about the FMMO reform process and background from an economist’s perspective.

Dr. Wolf gave some important and relevant background and statistics.

The FMMOs have been around for 85 years and were created because of disorderly milk marketing conditions. Their primary function is to make markets function “smoothly” with a second stated objective to provide price stability.

“If we were to re-do them today, I would say price adequacy should be addressed,” Wolf opined, noting that “we have times that the milk prices are very stable, but not very adequate.”

Other stated objectives of FMMOs are to assure adequate and wholesome supplies of fluid milk and equitable pricing to farmers.

“These things are still important today,” Wolf suggests, adding that the auditing, certification and a certain level of market information that is provided by the FMMOs benefits all participants and contributes to the public good.

He explained that FMMOs are changing.

“The primary sources of dissatisfaction with FMMOs in recent years arise because there is not enough money to go around, and some of this is related to the longer-term trends (in Class I sales),” Wolf explains.

He showed that while per capita dairy consumption has been increasing roughly three pounds per person per year, the decline in Class I fluid milk is the underlying factor.

“It really is startling how much of that decline (in Class I) in most areas really happened since 2010,” Wolf illustrated with graphs.

Not only did per-capita fluid milk sales decline more rapidly since 2010 than the already long-term decline charted since 1980, but population growth in the U.S. also stalled — so the total Class I sales have been hit with a double-whammy.

“This relates back to where the value is in the Orders, with most of the decline in the past 20 years occurring in that second half, — since 2010,” he explains.

(The Healthy Hunger Free Kids Act of 2010 was the precursor to USDA removing whole and 2% unflavored and flavored milk from schools and requiring flavored milk to be fat-free. Today, USDA has a proposed rule that could eliminate flavored milk until grade 9 as reported previously in Farmshine).

Because Class I has to participate in FMMOs, the FMMOs were “intentionally structured” in a way that the Class I revenue has always tended to be the highest class price because the FMMOs are in place to structure the fluid milk market, and so Class I accounted for at least 50% of the pool revenue – until 2010.

“We finished 2021 at 34% (down from 50%),” Wolf notes. “So there’s not enough money to go around with less (Class I) value in there.”

What changed? Wolf notes some of the long-term trends.

“First, exports are now 18% of U.S. milk solids production when it used to be that the U.S. exported about 5%… Milk beverage consumption is down while cheese, butter and yogurt are all up. We are still importing 4 to 5%, but as a large net-exporter now,” he says, “The U.S. is basing bulk commodity product prices off the world market. This introduces more outlet for milk but brings back the issues that come with international price-setting, overall,” he explains.

Another change, according to Wolf, is the level of consolidation at every level of the supply chain.

Wolf went over some of the make allowance data based on existing voluntary surveys as well as a prior California state order audited survey. He showed there is a wide range in costs between older and smaller plants vs. larger and newer plants. When determining where to set make allowances – as an ‘average’ or at a percentile of this wide range — there are regional impacts to consider, he suggests.

Wolf also took webinar attendees through the steps of a hearing that can take at least a year or more to complete and he dug into the make allowances from an economic perspective and some of the other pieces of potential reform. Over the next few weeks, we’ll continue to examine them in this series.

By Sherry Bunting, Farmshine, October 28, 2022 (updated with additional information after publication)

The National Milk Producers Federation (NMPF) Board gets high marks for passing a Federal Milk Marketing Order Modernization Plan this week at its annual meeting in Denver, Colorado that includes returning the Class I mover to the previous ‘higher of’ formula — a virtually unanimous consensus item that came out of the Farm Bureau Forum in Kansas City earlier in the month.

However, the NMPF modernization plan also includes a few items that were not fully discussed, items that seem to run counter to what dairy farmers were prioritizing, and it leaves out a few items the consensus-builders were vocal about in Kansas City.

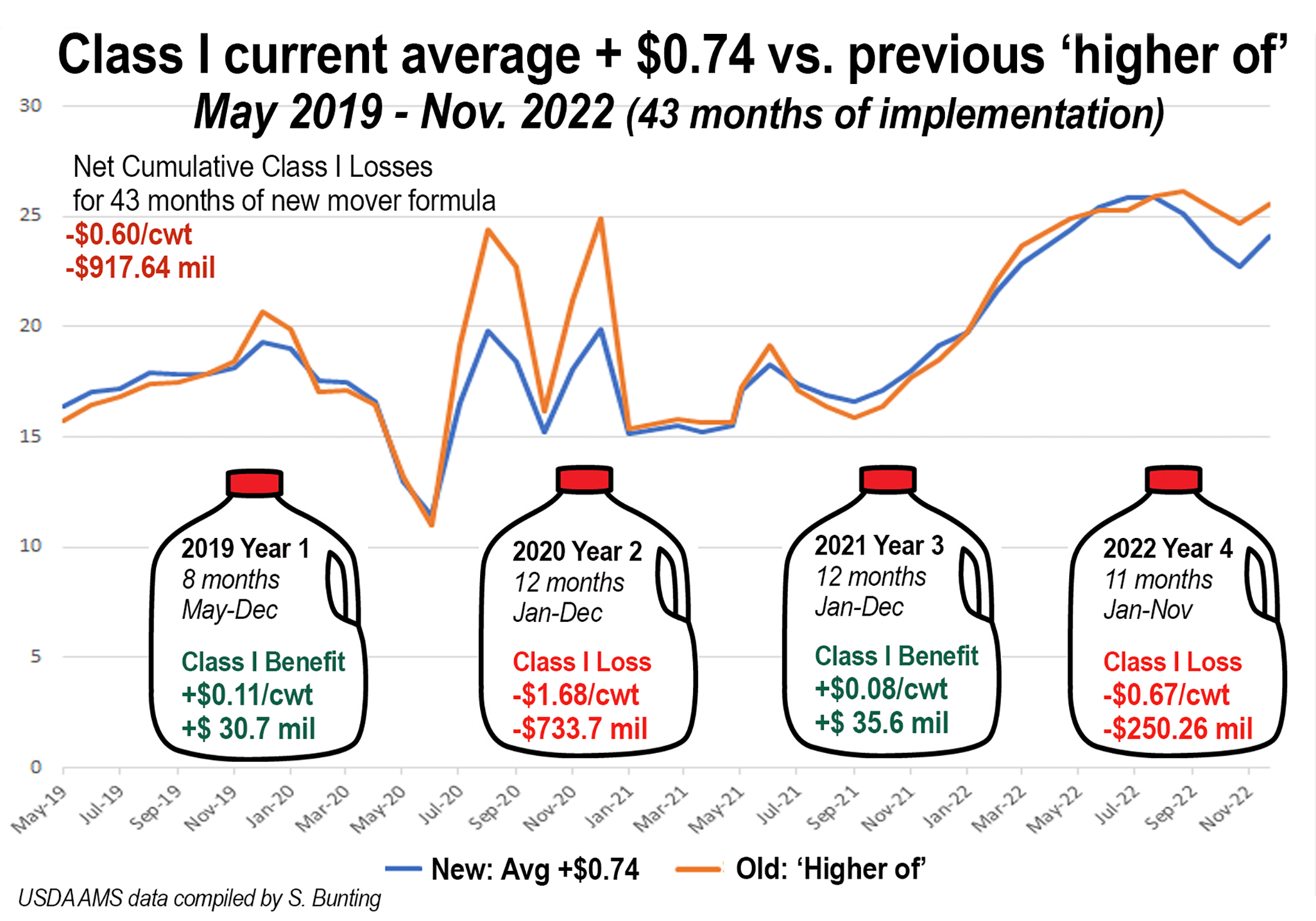

The recommendation to return to the higher of Class I mover is an important response by NMPF to dairy farmer concerns. That ball has been in USDA’s court after the first two years of implementation, according to the farm bill language that changed it to an averaging method in the first place. Four years and nearly $1 billion in cumulative Class I net value losses have passed (see chart), but Ag Secretary Tom Vilsack said he needed to see “consensus” before allowing a hearing to be opened.

In post-conference interviews, several Farm Bureau Forum attendees said this was their main priority for participating – to show Secretary Vilsack there is consensus to “fix the mistake.”

For NMPF to include it in their plan is a win.

Another item in the NMPF plan is to develop a process to ensure make allowances are reviewed more frequently through legislation directing USDA to conduct mandatory processor cost studies every two years and to update the make allowances contained in the USDA milk pricing formulas.

There was general agreement from stakeholders in Kansas City that processor costs need to be evaluated and make allowances updated. Over half of the table-groupings identified this. There was also healthy discussion of some ways to do this to minimize the sudden impact on farmer milk checks – all good points for developing a process and for a USDA hearing process to fully evaluate it.

Of the bones to pick, one NMPF recommendation that runs counter to what more than half of the table-groupings prioritized in Kansas City concerns expansion of the pricing survey to include more products. NMPF’s task force decided not to add any products to the price survey, and in fact they are recommending dropping one.

On the chopping block is the 500-pound barrel cheese price in the protein calculation for Class III.

Initially, NMPF’s task force committees looked at adding unsalted butter, skim milk powder (a higher value more standardized product than nonfat dry milk), and they looked at mozzarella cheese. In all three cases, the task force chose not to recommend additional products.

The fact that they are recommending elimination of a product from the pricing survey is curious.

Less than one-third of the Kansas City table-groupings listed elimination of barrel cheese pricing as a priority. Few people questioned NMPF economist Peter Vitaliano on the sensibility of this recommendation – except for yours truly.

I asked this question: “On the blocks and barrels, what do you foresee happening if the barrels are dropped? Right now we’ve got barrels doing more trading than blocks. We’re really not seeing much trading at all in blocks on the CME spot market. Also, would this mean that the cost of making those barrels will be backed out of the processing cost survey in terms of establishing new make allowances?

Vitaliano gave this answer: “That’s an interesting question. I’ve heard different interpretations of what’s going to happen to barrels if they are not used in the formula. Some folks feel they’ll just be priced at a discount to blocks, and the cash market for barrels will go away. I’m not sure I buy into that totally because barrel cheese is becoming a different product.”

The NMPF economist continued with his answer: “Under current quality standards, barrel cheese is the only major way that you can get uncolored whey, which is demanding a premium in the marketplace because all of these nutrition products, these high value nutrition products in demand by millennials and others, they don’t want to show ‘bleached whey’ on the label, they want the white uncolored whey powder that comes from barrel cheese production.”

Apparently, yellow whey from block Cheddar production is less desirable. But we’ve known this for at least 15 years.

In other words, according to Vitaliano, there is right now a ‘subsidy’ effect from the premium paid for the higher value of the uncolored whey that creates the environment to produce more barrel cheese – regardless of what the cheese market is doing.

Vitaliano noted that FDA is going to consider some changes that might alter how this cross-product scenario is playing out by allowing microfiltered milk to be used in plants producing standard-of-identity cheese, but the bottom line is that barrel processors making whey protein concentrate as co-products benefit from the white-whey premium whereas block cheese processors do not.

When the two are averaged together in the Class III protein formula, they represent different markets when they historically moved together, said Vitaliano.

Interestingly, however, barrels have traded higher — not lower — than blocks on the CME for most of this year.

In the purely cheese market history, barrels and blocks moved together more closely, then in times of market shocks beginning in 2009, we would see periods of wide spreads and inversions, sometimes barrels over blocks and most of the time blocks over barrels. During intervals in 2016-17, barrels sold at 10 to 20-cent discounts to blocks. Since 2018, we’ve seen long intervals of barrels over blocks by up to 25 cents and then the flipside with blocks over barrels.

This year (2022), barrels have sold at a premium to blocks consistently since April. The barrel premium over blocks stood at 15 cents per pound last week. That’s a significant impact on farm-level milk prices — to the good.

Coincidentally, barrel prices crashed this week, losing 22 cents, where blocks lost a nickel, thereby pushing barrels under blocks by a few cents on Oct. 25, the same day that the NMPF Board voted unanimously to endorse the multi-pronged modernization plan that includes dropping 500-lb barrel cheese out of the FMMO end-product pricing formula.

For the year (2022), barrels will likely average a nickel above blocks.

There is also the question of price discovery. For the year, we have seen more barrels traded on the CME compared with the volume of blocks.

When following up in a question about what happens to price discovery if the barrels are eliminated from the pricing formula, Vitaliano responded that 15% of the cheese reported in USDA’s weekly price survey is barrel cheese. Rather than reduce the weighted average to reflect that, and rather than including mozzarella in the pricing survey (a higher volume and value item than cheddar), NMPF is simply recommending the elimination of barrels to avoid the block/barrel spread.

Vitaliano said pricing formulas are based on the USDA price survey, not on the CME spot market. However, the CME spot market is used to set pricing for the USDA-reported sales.

Vitaliano also noted that price discovery on the CME spot market is achieved even if no product changes hands because it is a marginal market-clearing trade in the first place.