Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

Pennsylvania dairy producers were treated to a forward look at Calvin Covington’s milk market radar during R&J Dairy Consulting’s annual seminar. The bottom line is cheese, cheese, and more whey. Photo by Sherry Bunting

Cheese and whey, will continue driving bus,with big growth in processing capacity on the road ahead

EAST EARL, Pa. – Looking at the milk markets for 2025, Calvin Covington sees farm-level milk prices in the Northeast averaging 25 to 75 cents per hundredweight higher this year. He said milk margins, nationally, averaged $11.86 for the first 11 months of 2024, and he expects similar good margins to prevail in 2025.

The caveat? These are forecasted averages, and farmers should expect price volatility in their income and input costs, along with the mixed bag of positive, negative, and unknown impacts from the Federal Milk Marketing Order changes implemented in the second half of the year. He expects butterfat prices to remain good, but lower in 2025; whey prices will be higher, but more volatile; and protein may be lower as huge new cheese processing capacity comes online

Covington mostly shared what’s on his radar for the next 3 to 5 years during R&J Dairy Consulting’s 18th Annual Dairy Seminar, attended by more than 250 farmers at Shady Maple Smorgasbord in eastern Lancaster County, Pennsylvania on Jan. 28th.

He remarked about the number of young farmers in the crowd, and pointed out that Lancaster County is the consummate dairy county in the U.S. — with more than 1100 Grade A dairies, producing over 2 billion pounds of milk last year, which is 4.5% of total U.S. output and more milk than half of the state totals across the nation.

Consumers: more cheese, more fat, more solids

“Cheese is driving the dairy industry, and consumers are consuming more milkfat. That’s what makes stuff taste good,” he said. “Cheese is one-third fat, and that’s one reason why milkfat consumption is growing.”

He also showed how increased fat consumption is demonstrated in fluid milk sales, with “whole milk coming up.”

This trend toward consuming products with more solids is also evident in ice cream sales, which are down, but the fat content is up; and in yogurt sales, which are flat, but move “more milk in the yogurt” in the form of more solids.

Now retired, Covington, a previous National Dairy Shrine Guest of Honor and World Dairy Expo Person of the Year, spent over 50 years working for dairy farmer organizations, including as a DHIA milk tester, CEO of American Jersey Cattle Breeders Association, and CEO of Southeast Milk Inc.

He said the total solids growth in the dairy sales is expected to continue, up from 27 billion pounds total a decade ago to 31 billion pounds in 2024.

The caveat, he said, is that “exports peaked a couple years ago at 17% of total milk solids, and last year (2024) was down at 16%. Exports are a big part of your market, but they have started to level off.”

When asked about imports, Covington said “they keep going up, especially on butterfat” as the U.S. now imports almost as much milkfat as it exports.

He noted increased consumer demand for Irish butter, which is made differently than U.S. butter, with more butterfat. “I hope we start making better-tasting butter in the U.S. instead of importing it,” he shared.

Amid the demand for milk solids, Covington said “it’s amazing what you are doing with your milk components as dairy farmers.” In the Northeast, producers are averaging 4.21 fat and 3.29 protein due to genetics and “the job farmers are doing with their nutritionists and feed companies.”

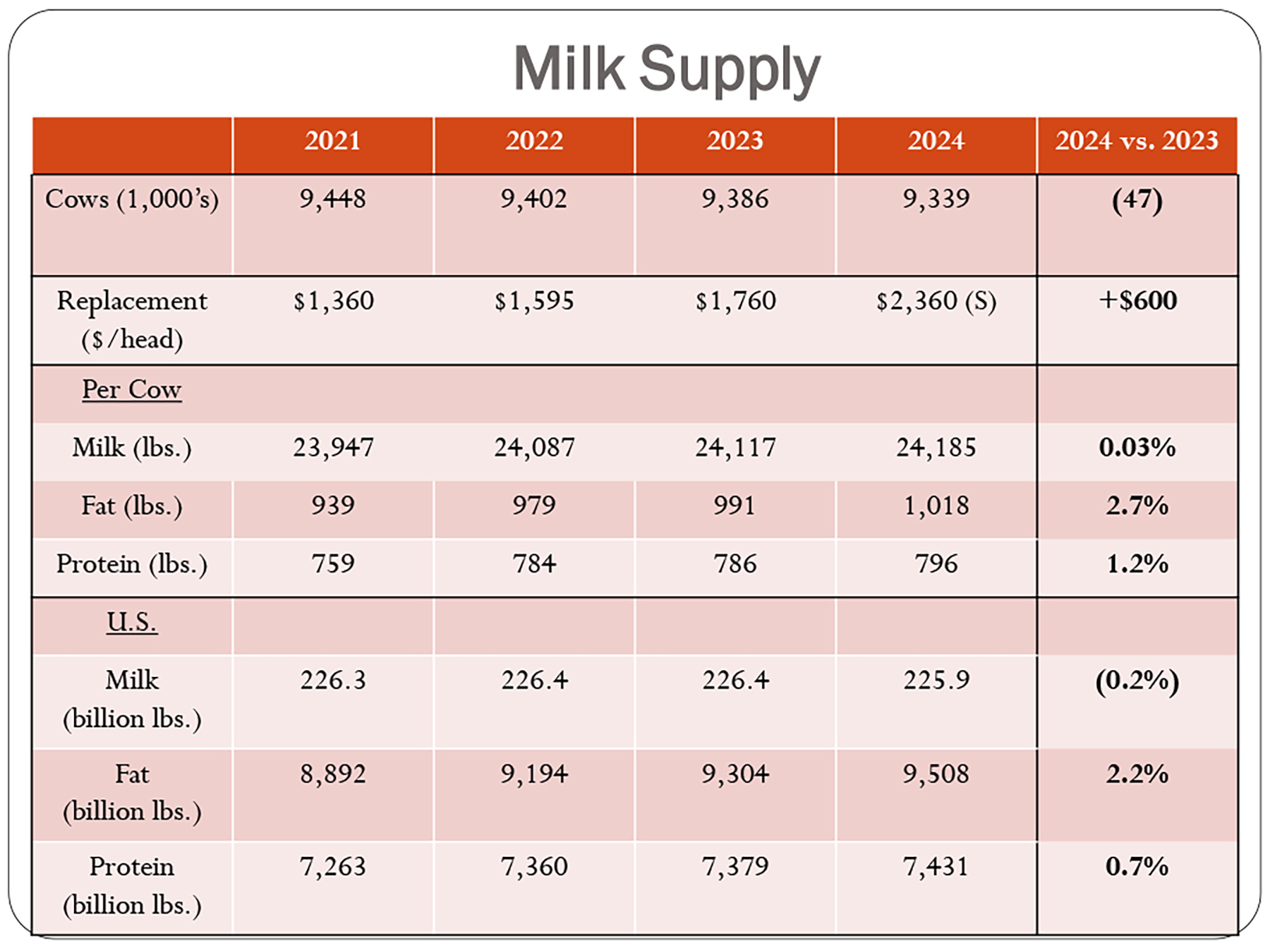

Covington demonstrated with 2023 vs. 2024 comparisons that farmers are increasing the amount of products made by increasing components year over year, instead of milk production and cow numbers.

Components are the big story on the supply side, a trend he also sees continuing. He doesn’t expect dairy cow numbers nor milk output per cow to go back to the year-over-year gains seen in the past any time soon.

With a chart he showed the stark 2024 vs. 2023 data: Cow numbers are down 47,000 head; replacement heifers sell for $600 more per head; average milk output per cow is flat; but average fat pounds per cow is up 2.7% and average protein pounds per cow up 1.2%. This means that even though total U.S. milk production at an estimated 225.9 billion pounds is down 0.2% from year-earlier, total fat pounds at 9.508 billion pounds are up 2.2%, and protein pounds at 7.431 billion pounds up 0.7%.

“You’re doing it with your components,” he said. “And that’s going to continue.”

Cheese (or maybe whey) is driving the bus

Putting aside the import and export caveats, Covington demonstrated that as the overall dairy market is growing, almost all of this growth has been in the cheese market, which has become a much bigger piece of the much bigger pie.

“Cheese has been driving the dairy industry for several years, and everything points to it driving the industry going forward,” he said, showing a chart of the product mix in the year 2000 when 167.4 billion pounds of milk was produced in the U.S., sold as half cheese, and one-third fluid milk, with 15% other products. This compares with 2024, when 225.9 billion pounds of milk was produced and 58% of the sales were in cheese, 20% fluid milk, and 22% other products.

Per capita trends also show “consumers are eating more of their milk instead of drinking it,” said Covington. “We have seen tremendous change since 1986, when consumers first started consuming more of their milk as cheese than as fluid milk. Look at 2023, people consumed 405 pounds of milk (equivalent) in the form of cheese and 128 pounds in the form of fluid milk.”

While home milk delivery is rare today, Covington said it happens now in the form of pizza.

“If I drive around the city on a Friday night, I’ve got to get out of the way of the pizza delivery people. I figure, on average, it takes a little over a gallon of milk to make one average size pizza. Just think how much home delivery we have today of milk, but in the form of something else, not the milkman dropping off half gallons,” he said.

“The market is changing, and it’s going to keep on changing.”

Why is cheese growing so much? Covington pointed to things he hopes are lessons for other products: 1) Convenience, innovation in packaging and varieties, with pizza accounting for 42% of all cheese; 2) Brand identity, there’s still a lot of this in cheese, not making it a commodity to try to get to the lowest price like in other dairy products (i.e. fluid milk); and 3) taste, people love cheese.

Big bets on the future

Big bets are being made for more cheese growth, and the revenue stream of whey ‘byproduct.’

“We are in a slurry right now of a pile of money being spent on new plant construction,” said Covington, listing the states of Kansas, Texas, South Dakota, Minnesota, Wisconsin and New York.

When all of this new construction is complete over the next year or so, Covington expects the need for 30 million pounds of milk a day to fill the new plants or expansions, which he estimates represent investments of at least $5 billion and are owned by private companies or groups of farmers or individual farms that are not cooperatives.

“This kind of money and growth is not being put out there unless there is confidence in getting a return on investment with cheese and whey product growth both domestically and internationally,” he pointed out.

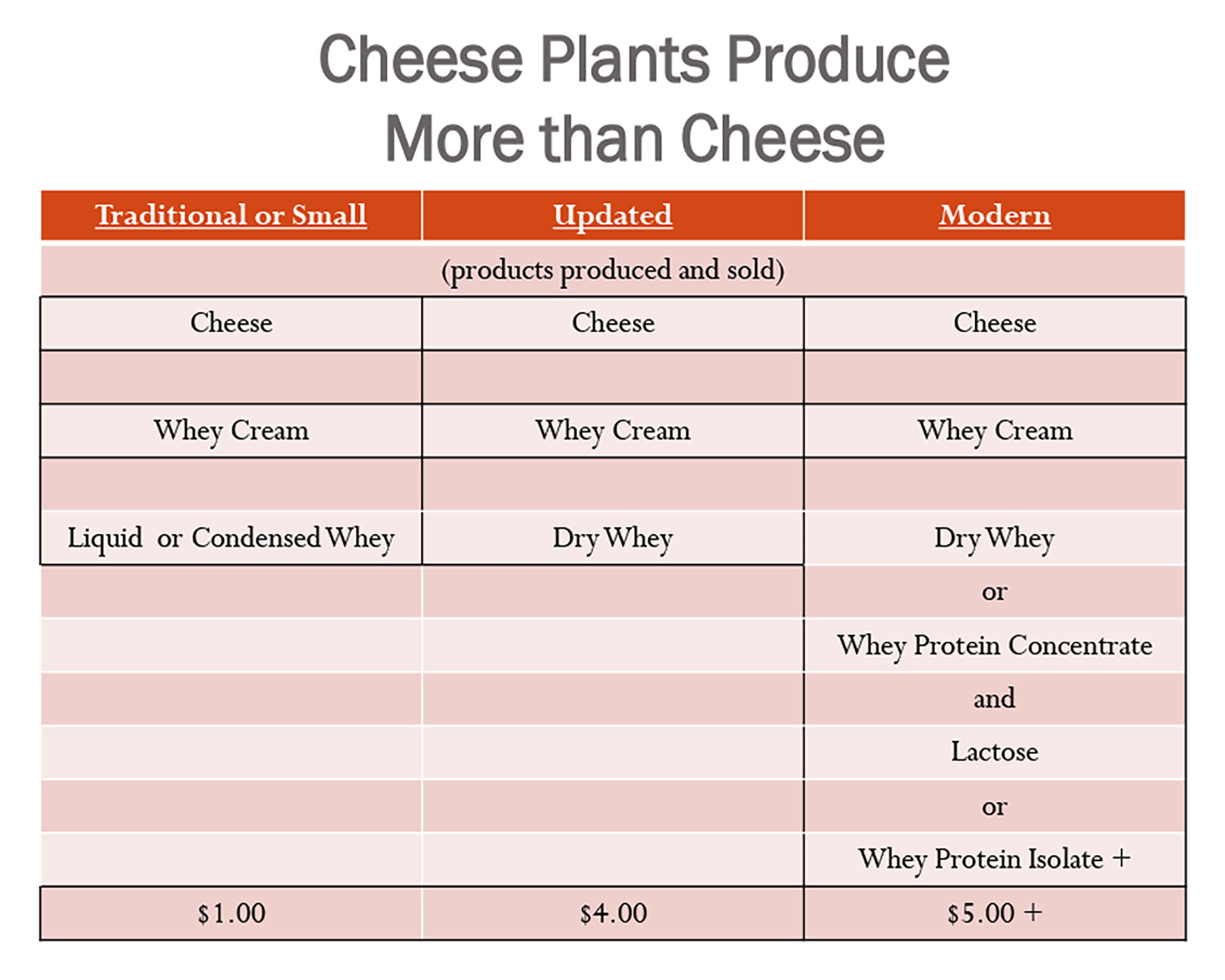

New cheese plant construction, when completed over the next year or so will take in more than 30 billion pounds of milk a day, and they gain a lot of additional revenue from what they do with the whey that smaller traditional cheese plants don’t have the equipment to do.

These new plants making all of this cheese will also have a lot of whey.

He explained that small plants get about $1.00/cwt for the whey cream and have the liquid whey to do something with. Some plants might dry it and get $3 per cwt for the dry whey plus the $1 for the whey cream, so that’s $4/cwt.

“Small traditional cheese plants can’t afford the equipment to do what some of these new plants are doing. These new companies not only dry the whey, they fractionate it to make whey protein concentrates. They separate out the lactose for whey protein isolates,” Covington said, rattling off a few items on the expanding list for everything from snacks and beverages, to pharmaceuticals and cosmetics, to milk replacers, to counter-top items, ‘pizza cheese,’ artificial seafood, canned hams, and more.

“It’s just amazing, and it brings in more revenue. When we think about cheese, it’s more than just the cheese, it’s also the income from the whey that’s left over,” he said, adding that the CEO of a large cheese company once told him: “Sometimes I think the cheese is the byproduct.”

With this kind of investment, the new plants are going to be making big volumes and getting income from the whey.

“This puts a crimp on the small cheese plants that can’t do this, and they’re going to have to get it out of the cheese end,” Covington observed, suggesting some potential structural change on the cheese side of the dairy industry with significant domestic and international sales growth needed to stay a step ahead.

On the positive side of the fluid milk industry, in addition to growing whole milk sales, Covington highlighted new investments. He sees a future with more dominance by grocery stores, pointing out the two new Walmart plants going into Georgia and Texas, which will be the largest in the country, processing 50 to 55 loads of raw milk a day.

Other big investments in the fluid milk sector in the Northeast are ultrafiltration and ESL packaging, such as the new fairlife plant under construction in western New York, new ESL expansion at the former Hood plant owned by Maola, and aseptic shelf-stable milk packaging at Cayuga Milk Ingredients.

Editorial Analysis: Tumultuous 2024 spills over into 2025 – Part Three

By Sherry Bunting, Farmshine, February 7, 2025(updated with additional information after print edition published)

EAST EARL, Pa. – A tumultuous dairy and beef market in 2024 is bound to be even more so in 2025. The long-awaited Jan. 1 Cattle Inventory Report is in, and we all saw the kerfuffle about tariffs and trade this week.

The bottom lines are…

— The U.S. beef cow herd continues to shrink, while both the beef and dairy heifer replacement numbers are notably smaller, signaling less domestic beef production and stable, if not reduced milk production in the face of strong domestic demand for beef and dairy products.

— U.S. import volumes of live feeder cattle as well as beef and dairy products have climbed over the past five years.

— Uncertainty prevails about U.S. trade policy, but export volumes of beef and dairy have leveled off already in the past several years. Dairy exports are bound to get a boost in the short-term as U.S. prices are mostly trailing current global prices. Tariffs on Canada and Mexico and potential retaliations are paused.

— Will the dairy herd continue maintaining itself at these shrinking heifer ratios now that we are five years out from the time of plentiful heifers.

Report highlights include…

Milk cow inventory has remained relatively stable over the past five years, ranging from 9.34 million head on Jan. 1, 2020 to the 5-year high of 9.45 million head on Jan. 1, 2021, then back down to just shy of 9.35 million head on Jan. 1, 2024 and Jan. 1, 2025. However, the number of dairy replacement heifers has dropped by 16% over the past five years from 4.61 million head on Jan. 1, 2020 to 3.91 million head on Jan. 1, 2025. This number is down almost 20% — or nearly 1 million head — from the record high 4.81 million dairy replacement heifers recorded on Jan. 1, 2016.

Are milk cows milking longer? Is the average dairy cow getting 16 to 20% more productive life (an additional half lactation)? Is the age at first calving continuing to decline, and are herd culling rates also declining significantly enough to maintain the current cowherd size on 16 to 20% fewer heifers expected to calve vs. 5 and 10 years ago?

According to the Jan. 1, 2025 Cattle Inventory Report, there are not quite 27 heifers expected to calve this year for every 100 cows in the current U.S. dairy herd, and a national cull rate of 29% based on January through December 2024 dairy cow slaughter totals. Five years ago, there were just over 31 heifers expected to calve for every 100 milk cows in the similarly-sized U.S. dairy herd.

Will these trends collide at the 5-year mark this year, given the average productive life of a dairy cow based on the most recent data (2020) is not quite three lactations or roughly 5 years of age? How will the $5 to $10 billion in new processing capacity be filled, or will we see existing plant closures in their stead? Are the investor dairies that put up 10, 20, and 30,000 cow facilities each year filling new barns with milking animals raised on their own calf ranches coming in under the reporting-radar of USDA NASS? Or is the pace of dairies exiting the business on one end mirroring the growth on the other end?

One inescapable conclusion is that the milk cow herd remains relatively stable, while the dairy replacement heifer numbers have shrunk by 16% vs. five years ago and by 20% vs. 10 years ago, and the record-high prices paid for dairy replacements is proof of tight supplies.

This is part three in a four-part series. Part one was published Jan. 3, 2025; Part two on Jan. 17, 2025.

CME graph using USDA NASS Inventory data

U.S. cattle herd down… again

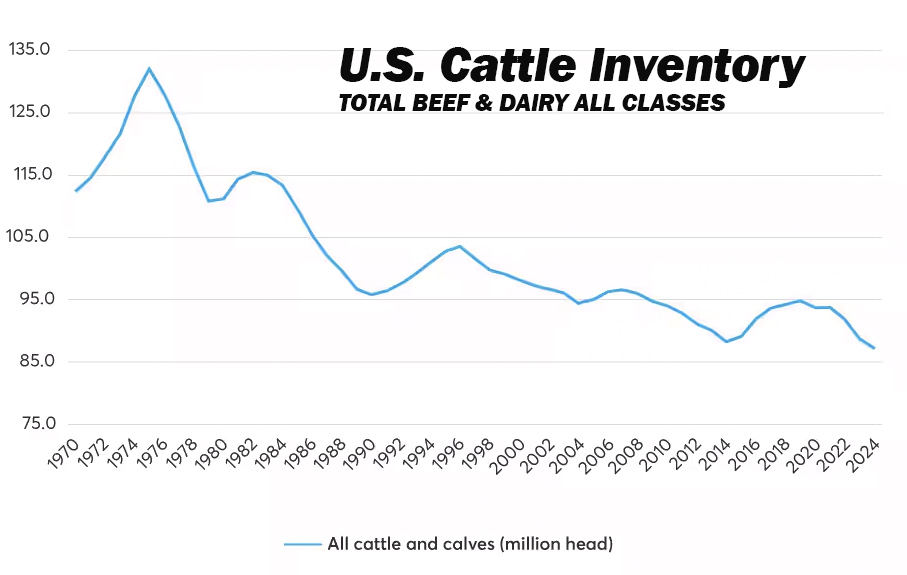

U.S. total cattle numbers on Jan. 1, 2025 are down 1% year-over-year (YOY), according to the All Cattle and Calf Inventory Report released by USDA on Fri., Jan. 31st.

At 86.66 million, the report counted 500,000 fewer head than last year’s total, which was already the smallest in 74 years (Jan. 1, 1951).

The total number of all cows and heifers that calved is down 0.4% YOY at 37.21 million head. That is 147,000 fewer beef and dairy cows on farms as compared with the revised-lower totals a year ago, which were already the smallest in 84 years (Jan. 1, 1941).

The total number of all heifers over 500 pounds on Jan. 1, 2025 (including heifers destined to become beef) was down 1% YOY at 18.18 million head. That’s 140,000 fewer head counted than on Jan. 1, 2024, which was already the smallest total heifer number in 34 years (Jan. 1, 1991).

In the Jan. 1, 2025 report, USDA NASS revised-lower its Jan. 1, 2024 and July 1, 2023 estimates of total animals that had calved, as well as the calf crop in those 12 to 18 month prior Inventory Reports. Statisticians went back and compared the prior estimates to the official slaughter data, the import and export data, and the relationship of this new survey information to the prior surveys.

This means the Jan. 1, 2025 numbers are now estimated at levels below the revised-lower prior reports that had already set records! (A mid-year 2024 inventory would have been helpful, but was canceled by former Ag Secretary Tom Vilsack, claiming insufficient USDA funds).

Chart compiled by S. Bunting with USDA NASS Inventory data

Milk cows flat, heifers shrink

The number of milk cows on Jan. 1, 2025 was essentially unchanged vs. year earlier, up only 2,500 to just shy of 9.35 million head.

However, the dairy replacement heifer total is down 1% YOY at 3.91 million head. At this rate, the number of heifers heading to careers as milk cows is 16% below the 5-year comparison on Jan. 1, 2020.

At 3.91 million head, there are 37,000 fewer dairy replacement heifers than a year ago, which was already the smallest number of dairy replacement heifers in 47 years (Jan. 1, 1978).

As the graph above illustrates, milk cow numbers have held relatively stable over the past five years, while the number of dairy replacement heifers has significantly declined. Are cows experiencing longer productive life? Or are the multi-site investor dairies filling their own expansion sites via their own calf ranches, and escaping the USDA reporting radar?

According to the most recent data (2020), average dairy cow productive life in the U.S. is just shy of three lactations, roughly five years of age. With the number of dairy replacement heifers declining 16% over the past five years, will these two trends collide in the next 12 to 24 months to reduce the U.S. milking herd while escalating the already record high dairy replacement cattle prices? And, what role might HPAI H5N1 play as longer term impacts emerge?

USDA NASS reports that the average auction value of ‘average’ milking cows has increased by nearly $800 per head to $2650 for 2024 vs. $1890 for 2023; $1100 per head higher vs. the $1720 average for 2022; and double (+$1300) the average value reported at $1350 and $1300 per head four and five years ago for 2021 and 2020, respectively.

The average cost to raise dairy replacements has been estimated at $1700 to $2400 per head, which means the value of ‘average’ replacement heifers at $1720 to $2660 from 2022 to 2024 is finally starting to mirror the cost to raise them — on average.

Many dairy producers continue producing only the heifers they need, which is reducing the availability of heifers in the marketplace for those wanting to expand.

Producers continue to respond to the lure of the 3-day-old dairy-on-beef crossbred calves offering substantial margins of $800 to $1000 per head — with no investment, no rearing, no revenue-wait, and no risk.

Basically, a dairy cow can produce $800 to $1000 in revenue for the dairy as soon as she drops a live crossbred calf, no matter what the milk price or margins are doing, and with her whole lactation in front of her.

The Jan. 1 Inventory Report shows the U.S. beef herd continues to shrink, suggesting beef-on-dairy crossbreds will continue to offer bigger per-head margins than growing extra dairy heifers to sell as herd replacements — unless they are premium dairy heifers.

Expanding dairies are having to really plan ahead to raise the animals they need for growth or scramble to get them. Additional upward price momentum may be seen on dairy replacements in the next 12 to 24 months as the more abundant heifers available five years ago ‘age-out’ of the system, statistically speaking, at five years old, which is the industry average age of a milking cow in the U.S.

With the Jan. 1, 2025 U.S. milking herd holding steady at a level that is 1.1% smaller than it was in 2021, the expanding dairies are buying up the herds of the exiting dairies at high prices that make dairy farmers think about selling the cows and hanging on to the heifers, for now, if they do not have a next generation to continue the dairy.

Turnover of existing Holstein herds to include other breeds is also occurring, along with genetic improvement within the Holstein breed, as producers work to raise heifers that calve into the milking herd at younger ages, produce more component yield per hundredweight of milk, have improved productive life traits and fewer days open for a tighter average calving interval.

With a 2024 national dairy herd of 9.35 million milk cows and a 2024 national dairy cow slaughter of 2.726 million, the national culling rate last year was 29%. At that rate, even if the average age at first calving is 22-months, the U.S. dairy industry would need 28 dairy heifers to calve successfully in the next 12 months for every 100 milk cows — just to maintain the current size of the U.S. dairy herd.

According to the Jan. 1 Inventory Report, there are 2.5 million dairy heifers expected to calve in 2025 (down 0.4% or -9000 head). This calculates to 27 (actually 26.75) dairy replacement heifers expected to calve in 2025 for every 100 cows in the U.S. dairy herd as of Jan. 1st.

In 2016, when dairy replacement heifer numbers reached their peak at 4.81 million head, 3.11 million head were expected to calve that year, and the total U.S. dairy cow inventory was 9.31 million head, meaning there were 31 heifers expected to calve for every 100 cows in 2016. This has steadily eroded in part because dairy producers have stopped spending the money to grow extra heifers that were worth less than the cost to grow them until this year. They also worked to reduce age at first-calving, days open across the herd, higher component levels in the milk, reduced death loss, longevity, and began gradually re-introducing beef crossbreeding, which has become a pretty big deal over the past five years.

Some parts of the country are down significantly in heifer replacements as of Jan. 1, 2025, while others are up. For example, Pennsylvania has 15% more dairy replacement heifers on farms vs. year ago.

These estimates indicate milk production will be flat to lower for the next 12 to 24 months.

What this does not account for is the increasing milk component levels generating more dairy products per 100 pounds of milk and the increasing volume of dairy imports, particularly cheese, butter, and whole milk powder. But those increases can only do so much in the face of $5 to $10 billion in new processing assets coming online in the next 6 to 18 months.

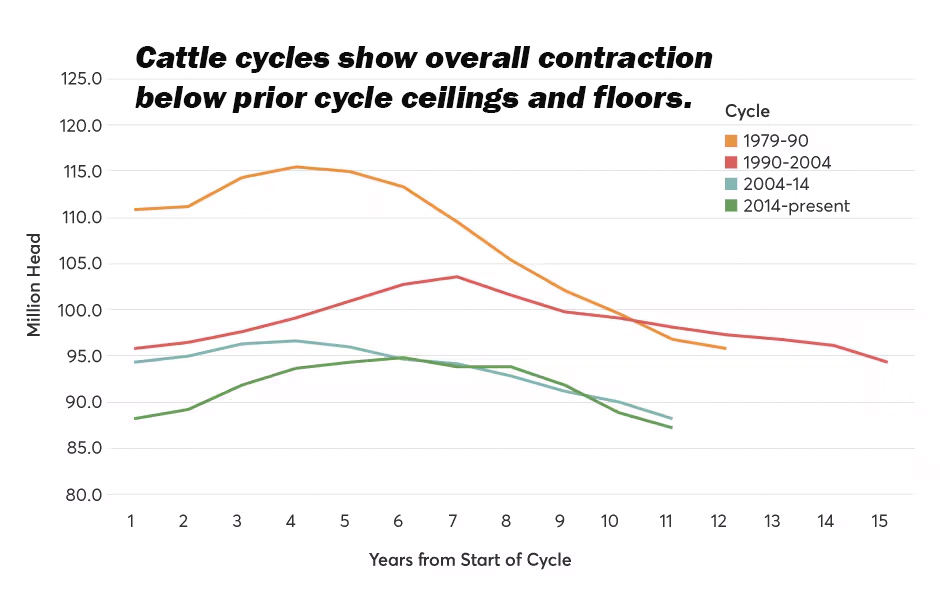

CME graph using USDA NASS Inventory data shows continued overall contraction of total cattle inventory as new cycles mostly fail to breach prior cycle ceilings, floors, and midpoints.

Beef herd shrinks more

The Jan. 1 Inventory shows the U.S. beef herd continues to shrink. At the national level, there are no signs of rebuilding, as the total number of heifers heading to careers as beef mama cows is down 1% YOY. However, in some parts of the country, such as Virginia, more heifers were retained as beef cow replacements and fewer were earmarked for feedlots.

At 4.67 million head, there are 46,000 fewer beef replacement heifers in the U.S. vs. year ago, setting another record low as the smallest number since 1948.

Even more striking is the beef replacement heifers that are expected to calve in 2025 are down a whopping 2% YOY (-50,000) nationally.

Meanwhile, the beef-on-dairy feedlot placements, while a growing segment of the beef industry, are not enough to reverse the downward beef production trend as evidenced by declines in the number of animals over 500 pounds on Jan. 1st heading to feedlots: Steers and bulls are both down 1% (-157,000 and -21,000 head YOY, respectively). Heifers over 500 pounds heading to feedlots are down 0.6%, and the number of cattle on feed as of Jan. 1, 2025 is down 1% YOY at 14.3 million head (-130,000 head).

The Inventory Report came on the heels of the January Cattle on Feed Report, which showed 3% fewer feedlot placements as of Jan. 1, perhaps because of the Mexican border closure to the live cattle imports, due to concerns about transmission of the screw-worm parasite.

Even the total number of all calves (heifers, bulls and steers) weighing under 500 pounds dropped 1% lower YOY at 13.46 million head (-30,000).

These estimates suggest domestic beef production will decline for at least the next 12 to 24 months, maybe longer.

What this does not account for are the number of live cattle crossing the border into U.S. feedlots from Mexico and Canada and the increasing amounts of beef the U.S. imports from other countries, including from Canada, Mexico and South America.

Map compiled by S. Bunting with USDA NASS Inventory data

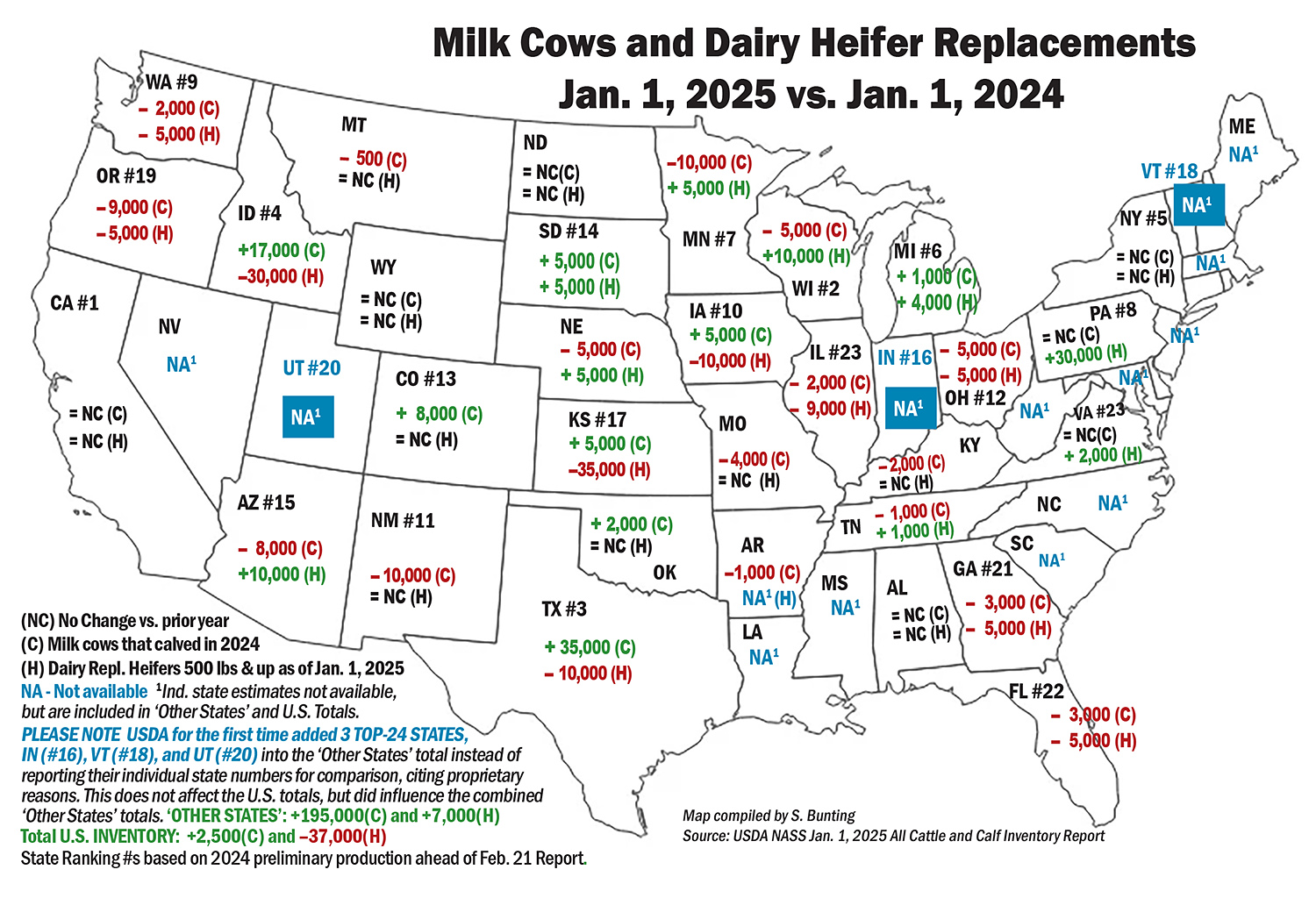

Significant geographic dairy shifts

Breaking the dairy inventory numbers apart, we see big geographic shifts.

The West added 78,000 more milk cows in 2024 vs. 2023, except for California’s numbers being unchanged. On the other hand, the East and Upper Midwest had equal or fewer milk cows, down collectively more than 75,000 head YOY, except Michigan was up just 1000 head.

The biggest 2024 gains were tallied in Texas, up 35,000 head, and Idaho, up 17,000 head. Colorado grew by 8,000 head; Iowa, Kansas and South Dakota by 5,000 each; and Oklahoma by 2,000.

The biggest milk cow declines were in Minnesota and New Mexico, down by 10,000 head each; Oregon down by 9,000; Arizona by 8,000. Wisconsin, Ohio, and Nebraska by 5,000 each; Missouri by 4,000; Florida and Georgia by 3,000 each; Illinois, Kentucky, and Washington by 2,000 each; and Tennessee by 1,000. Smaller unranked states collectively accounted for the remainder of milk cow losses.

Interestingly, USDA pulled three Top-24 Milk Production States into the ‘Other States’ category, choosing not to report their cow and heifer numbers for proprietary reasons. They are Indiana (#16), Vermont (#18) and Utah (#20). Thus the ‘Other States’ category saw an increase of 195,000 cows simply because these three Top-24 states were included anonymously in the total.

The geographic breakdown is interesting when it comes to dairy replacement heifers as the growth is noted in the areas where the cow numbers have declined and vice versa. These shifts could reflect changes in the way heifers have tended to move across state lines for rearing, especially in light of the dairy-adapted B3.13 strain of HPAI H5N1.

Pennsylvania is the biggest outlier as the cow numbers are unchanged YOY, but farmers reported 30,000 more dairy heifers in the Commonwealth on Jan. 1, 2025 vs. year ago.

Elsewhere in the East, Virginia dairy heifer replacements are up 2,000 head; Tennessee up 1,000 head; New York and Kentucky unchanged; Georgia and Florida down 5,000 head each. Again, the ranked states of Indiana, Vermont and Utah had their replacement heifer numbers lumped into the ‘Other States’ category, which consequently showed a gain of 7,000 heifers vs. year earlier when those states were not included in that category.

Beef replacement heifers and feedlot heifers are down a combined 10,000 head in Pennsylvania, while Virginia showed signs of beef herd rebuilding, reporting 4,000 more beef replacement heifers and 4,000 fewer heifers heading to feedyards.

Looking at the Mideast, Michigan had 5,000 more dairy heifer replacements, while Indiana’s numbers were unreported. Ohio is down in dairy heifers by 5,000 head. Beef replacement heifers in that region are up by 7,000 head and feedlot heifers are up by 3,000 head.

The Upper Midwest grew their dairy replacement heifer numbers, while the West significantly decreased them. Wisconsin is up by 10,000 head YOY; while Minnesota and South Dakota grew by 5,000 head each.

In the West, the following states with significant growth in milk cow numbers had significant losses in dairy replacement heifer numbers: Kansas down a whopping 35,000 head in dairy replacement heifers; Idaho down by 30,000 head; Texas, Pacific Northwest and Iowa down 10,000 each. Dairies in Kansas, Idaho, Texas, and Iowa contended with avian influenza in 2024.

Meanwhile, in California, New Mexico, and Colorado (all three having dealt with H5N1) the number of dairy replacement heifers was reported as unchanged YOY, but Arizona, which has not had H5N1, grew its dairy heifer numbers by 10,000 head.

USDA Economic Research Service graph

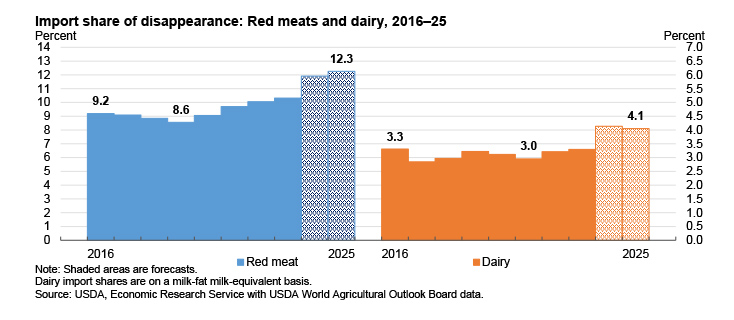

Trade is uncertain(Imports up, Exports leveling off)

Dairy and beef imports are growing, and the industry is responding to ‘tariff talk’ with statements showing fear of trade wars harming farmers or possibly gaining concessions in the context of Agriculture’s current annual trade deficit of $45.5 billion.

On Friday, Jan. 31, the spot cheese and Class III milk futures markets plunged lower in response to U.S. tariff announcements of 25% on goods from Canada and Mexico and 10% on goods from China.

This fear was short-lived, however, because the planned tariffs on goods from Canada and Mexico were promptly paused three days later on Monday, Feb. 3, when leaders agreed to support and combine efforts on U.S. border security, while putting teams together with the pledge to work through U.S. trade issues over the next 30 days.

The announced 10% tariffs on China went into effect Feb. 4, but discussions between the U.S. and China are said to be resuming for phase one of the trade deal struck in the prior Trump Administration just before the Covid pandemic hit globally.

Meanwhile, the total volume (not value) of dairy exports has leveled off on a total solids basis in the past two to three years as the U.S. exports more cheese and less skim milk powder and much less whey – the latter because we domestically produced less commodity SMP and far less commodity dry whey in 2024. Inventories are down for both, meaning domestic demand is using what is produced.

On the flip-side, the U.S. imported more cheese, butterfat, and whole milk powder during the first 11 months of 2024 YOY.

We will take a closer look at the trends in U.S. dairy farm numbers, production, and trade after final 2024 trade and production data are released in late February, and with more information, perhaps, on how U.S. agricultural trade policy may be shaping up for 2025.

Editorial Analysis: Tumultuous 2024 spills over into 2025 – Part Two

By Sherry Bunting, Farmshine, January 17, 2025

EAST EARL, Pa. – Year 2024 was tumultuous, and 2025 is shaping up to be equally, if not more so. Here’s a look at how supply, demand, and other market factors are shaping up for milk prices and dairy margins heading into 2025. This is part two of a four part series, see part one here and part three here.

We are a few weeks away from a few key yearend reports that will give us a better handle on production and cattle inventories, but the current market fundamentals favor a forecast for higher milk prices into 2025.

Better prices

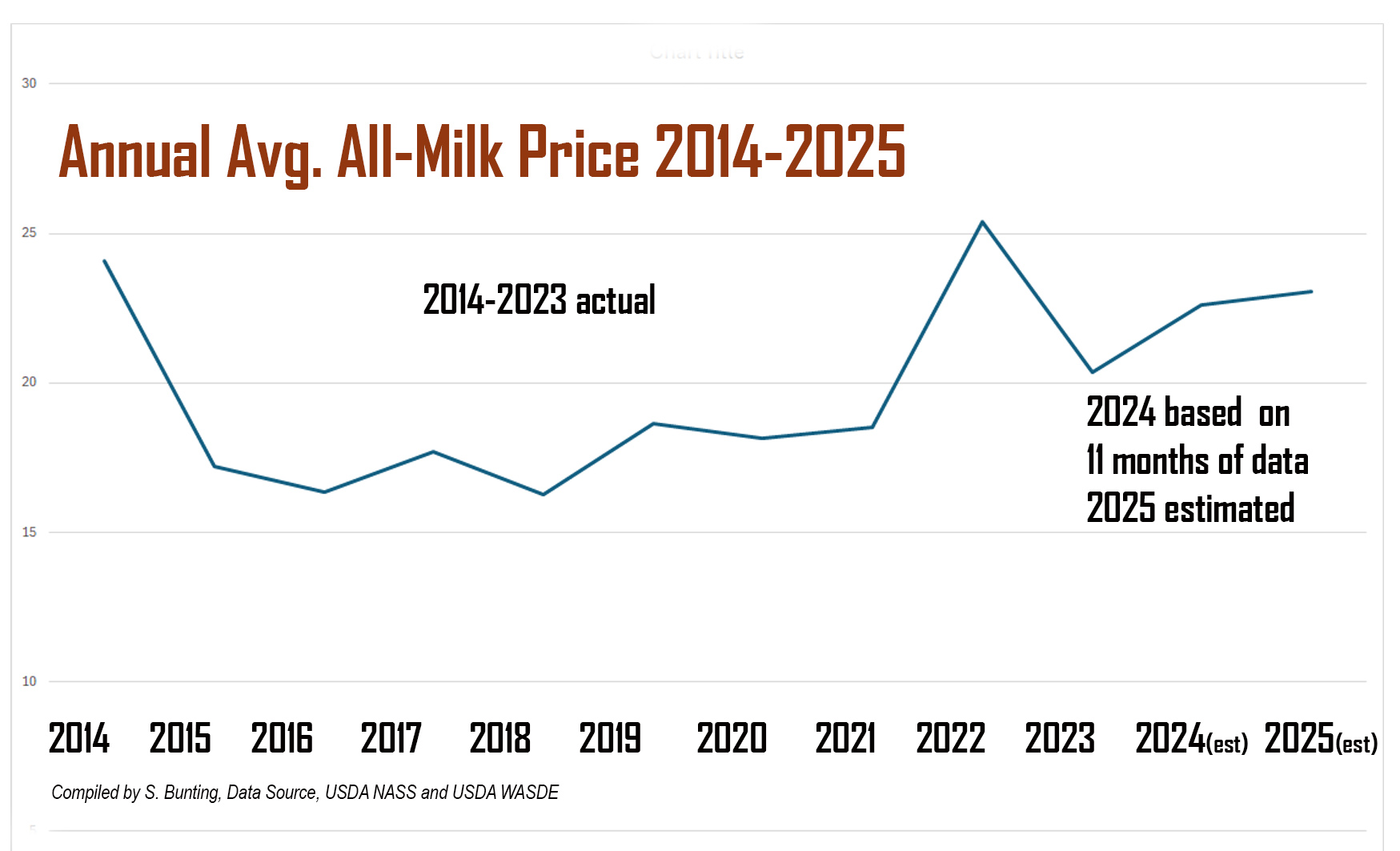

In fact, the Jan. 10th World Agriculture Supply and Demand Estimates (WASDE) just raised by 50 cents per cwt the estimated 2025 All-Milk price average at $23.05 after having lowered it the month before.

Based on 11 months of official data, however, the January WASDE shaved another nickel off the 2024 average All-Milk price, now estimated at $22.60, which would be $2.20 higher than the average All-Milk price of $20.40 for 2023 but $2.80 lower than the decade’s high point of $25.40 in 2022.

At an estimated $22.60, the average All-Milk price for 2024 would be the fourth time in the past decade and the third consecutive year that the annual average All-Milk price was above the $20 mark. (Fig. 1).

Strong demand

Positive supply and demand fundamentals for 2025 include the reported strong domestic and international demand for cheese and butter; tighter than expected milk supplies; tight to adequate dairy product inventories; growth in year over year (YOY) sales of fluid milk; and strong domestic demand for skim solids in the form of nonfat dry milk, dry whey and whey protein concentrate coupled with reduced production of these products limiting the availability for export.

A sustained price rally in the CME spot market-clearing price for the market indicator product dry whey reached a multi-year high of 75 cents per pound by the end of the 2024 and is holding at near 74 cents per pound into mid-January. Trouble is, this market-clearing price has been tardy all year in translating to sales reported on the USDA weekly price survey used in the Federal Milk Marketing Order (FMMO) price formulas.

Despite the positive supply and demand fundamentals, we saw fourth quarter 2024 milk prices decline $1 to $1.50 from the year’s high point at $25.50 in September, and even though dairy products are holding steady on the CME spot cash markets, the CME milk futures markets took a tumble into below-$20 territory across the board this third week of the New Year.

So what’s the deal? Uncertainty.

Fewer cattle?

Uncertainty prevails about future cattle inventories after Sec. Vilsack canceled the mid-year 2024 Cattle Report last summer. The Jan. 1 Cattle Inventory Report comes out Jan. 31st. It’s unlikely to show any big surprises in the two-year trend toward reduced cattle numbers, including dairy replacement heifers. USDA says this report will give the trade an indication of producers retaining dairy heifers for their milk herds.

With prices skyrocketing $800 to $1200 per head above year ago levels for fresh cows and springing, bred, and open heifers, a sudden rise in replacement heifer numbers is unlikely.

Meanwhile, beef-on-dairy calves continue to give dairies an immediate $800 to $1000 check on a 3-day-old bull calf requiring very little input cost. That’s $900 in income per cow for dropping a calf, even before she starts her lactation.

The tug-of-war on breeding decisions for future dairy farm calf crops continues as the total U.S. beef and dairy calf crop, by the way, has already declined 1.6 million head in the two year period from Jan. 1, 2022 to Jan. 1, 2024. On Jan. 31st, we’ll see what the Jan. 1, 2025 numbers say.

Global trade

Uncertainty also exists around global trade amid ‘tariff talk’ against the backdrop of YOY growth in export volume, that is tempered by YOY growth in import volume. The January WASDE expects the trend of export volume growth to continue, but also expects the larger import volumes to continue. While the report specifically mentions cheese and butter, USDA FAS data show growth in the imported volume of skim milk powder, and especially YOY growth in whole milk powder (WMP) imports in each of the past four years.

FMMO changes

Uncertainty about the implementation of USDA Federal Milk Marketing Order (FMMO) price formula changes in the second half of 2025 that will impact risk management. The updated make allowances will trim class and component index prices by 75 cents to $1.00 against a CME milk futures markets that bases contracts on the FMMO formulas. That changeover will have to be dealt with.

Uncertainty about how new, efficient expansions of cheese and ingredient production capacity may be tied into sourcing from multi-site dairy farms that have planned expansions with internal heifer replacement models. What will be the impact on the rest of the industry when they start cranking out tons more cheese on the new and higher make allowance margin.

H5N1 impacts

Uncertainty about milk production trends after the impact of the bird flu outbreak in California dragged down total U.S. milk output well below expectations. The next report for December milk output will be released on Jan. 24th.

The January WASDE reduced its total milk production forecasts for 2024 and 2025, driven by “lower milk cow inventories and lower expected milk output per cow.”

This came on the heels of the November milk production report released in late December, showing California’s 9.3% drop in state-wide milk output, attributed to HPAI H5N1 hitting at that point half of the state’s dairy herds. This drove the total U.S. output down an unexpected 1% YOY.

The WASDE also forecasts “slower growth in output per cow” in its rationale for reducing the milk production estimate for 2025. This means what producers have been reporting is now showing up in the USDA data. Producers in areas hit by H5N1, especially California, report an initial 30 to 40% herd level production loss that only comes back about half-way, six to eight weeks later.

Producers also indicate a 2% increase in herd-level mortality and increased culling. Both veterinarians and producers in previously affected areas are now reporting impacts on dry cows and springing heifers, aborted calves, shaved production peaks, and emerging questions about milking performance in the following lactation.

According to APHIS data, as of Jan. 10, the virus was detected in 708 dairy herds in California since the outbreak was first reported there in September. That’s nearly 75% of the state’s dairies affected to-date. In the past 30 days, 66 California herds have been affected, with the most recent detection on Jan. 10.

Apart from the California outbreak, the only other detections of H5N1 on U.S. dairies in the past 30 days is one herd in Michigan on Dec. 30. This is good news, considering that 13 states have now been fully brought into the National Bulk Milk Testing Program announced on December 6th as a mandatory program for all 48 continental states.

Those initial states include California, Colorado, Indiana, Maryland, Michigan, Mississippi, Montana, New York, Ohio, Oregon, Pennsylvania, Vermont, and Washington.

Better margins

For 2024, the milk over feed cost margin only fell below the Dairy Margin Coverage (DMC) program’s highest payment trigger level of $9.50/cwt in the first two months of the year. In fact, Sept. 2024 saw the highest DMC margin on record at $15.57 with an All-Milk price of $25.50 and a feed cost at $9.93. Since then, Q4 margins have declined to $14.50 as the All-Milk price fell and feed cost remained fairly constant.

This measure does not account for the higher fuel and energy costs, higher labor costs, rising cost of insurances, higher interest rates on capital, and generally higher costs for other inputs that keep a dairy farm going.

Labeling games

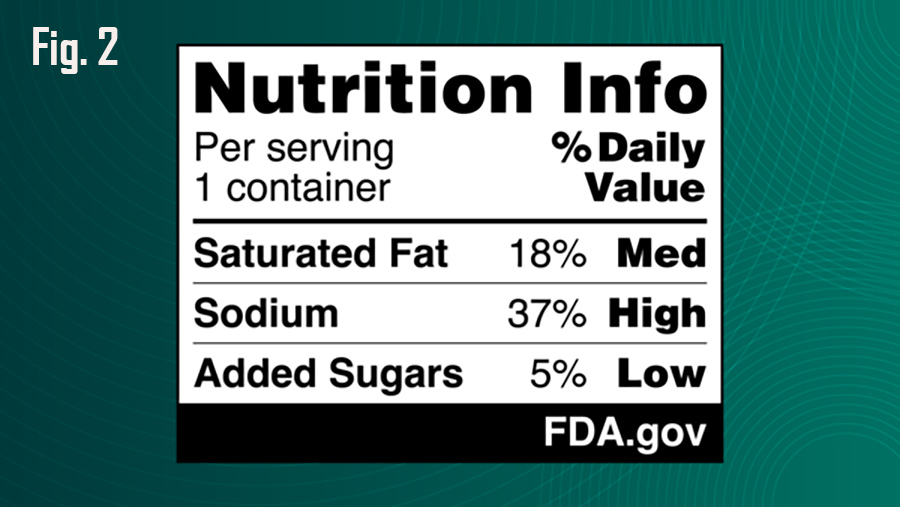

Other market factors may increasingly play a sidebar role. On the demand side, FDA’s new draft rule on Jan. 14 requires front-of-package labeling (Fig. 2 example above), which in addition to listing grams of saturated fat and percent of total recommended daily value, will now use a rating system to mark the saturated fat content of foods and beverages as high, medium, or low as the outgoing Administration attempts to further push consumers into the low-fat Dietary Guidelines regime.

Despite the noise around low-fat and anti-animal, USDA reports strong demand for real beef and dairy, with whole milk the top volume growth category in the fluid milk market.

FDA also issued new draft guidance on Jan. 14 for ‘best practices’ in naming and labeling of fake plant-based foods that are marketed and sold as alternatives for animal-derived foods. This guidance applies to fake meat, eggs, seafood, and dairy products, but does not include the labeling of fake beverage milk. FDA reminded the trade of its 2023 draft rule for plant-based fake milk.

his follows the same pattern as the previous fake milk guidance – recommending that the plant-based food be “qualified by type of plant source” when using the name of a standardized animal product such as cheese or beef. (Fig. 3 above)

This is how FDA has treated fake milk for the past 15 years, by allowing for example, the ‘almond’ qualifier in front of the word ‘milk.’ The FDA’s 2023 guidance on milk, specifically, recommends, but does not require, additional nutrition statements to clarify nutritional differences.

Frankenfoods

Likewise, on the supply side, fake Frankenfood is emerging as FDA continues mulling a draft rule on what to call the products of lab-creation seeking to replace real animal-derived foods.

For dairy, this comes in the form of microbes bioengineered with bovine DNA to excrete fake dairy protein and fat analogs that USDA refers to as “precision fermentation protein products” while lab-created gene-edited cells growing into blobs of fake meat, egg, seafood, even dairy analogs are referred to as “cell-cultured” chicken, seafood, beef, dairy etc.

In late December, the USDA Economic Research Service (ERS) released its first ever report on “The Economics of Cellular Agriculture.” This means the Department has now recognized Frankenfood as part of the Agriculture domain. Yes, we’re talking about fake food from a factory, not a farm.

The 45-page ERS report notes that for 25 years, scientists in the public and private sectors have been “actively researching methods for producing food products that are physically and chemically equivalent to livestock- and poultry-produced foods (i.e., meat, dairy, eggs) but that minimally rely (if at all) on animals.”

By 2023, more than 200 private firms existed worldwide, and cumulative invested capital in the cell-culture and precision fermentation industries exceeded $5 billion. As of 2024, more than 100 patents have been filed. U.S. food agencies (FDA, USDA and FSIS) have been developing regulatory frameworks to accommodate and ensure the safety of these products, according to the report.

To-date cell-cultured fake chicken meat has been commercialized in Singapore and the U.S., largely through unique restaurant chains. This led to states like Florida banning the stuff.

Meanwhile, “precision fermentation-derived fake dairy protein analogs have been commercially available more broadly,” according to the ERS report.

These Frankenfoods tout smaller carbon footprints, less land and water usage, but ERS authors observe that, “Open questions remain concerning the design of bioreactors and important elements of the production process, including cell source, growth medium, and energy requirements, as well as the optimal size and configuration of production-processing plants.”

The report states so-called “precision-fermented dairy products are already on the market in the U.S., and, like their plant-based counterparts, sell for a premium over animal-based. For example, the company Perfect Day partners with other companies that sell products like ice cream and milk featuring their precision fermentation animal-free whey protein.”

In this way the fake dairy protein analogs are marketed as an ingredient in a business-to-business vs. business-to-consumer model.

According to the ERS, precision fermented protein products (fake dairy analogs) are increasingly available in U.S. markets, while cell-cultured products (fake meat and seafood analogs) are not.

Short run profitability, according to ERS, will rely on consumer willingness to pay for these products with current consumer attitudes described as “mixed.” But the labeling guidance remains unclear as the fake dairy protein analogs are actually the harvested excrement of the bioengineered microbes, not the DNA-altered microbes themselves. Consumers need to know what they are buying.

The ERS report also states that despite some of these companies and investors releasing bold lifecycle ecosystem claims, the “environmental impacts are largely unknown.”

Part III in a future Farmshine will look at the yearend reports due later this month.

Whole Milk for Healthy Kids Act reintroduced in style!

‘Most nutritious drink known to humankind’ takes center stage at Ag Secretary confirmation hearing

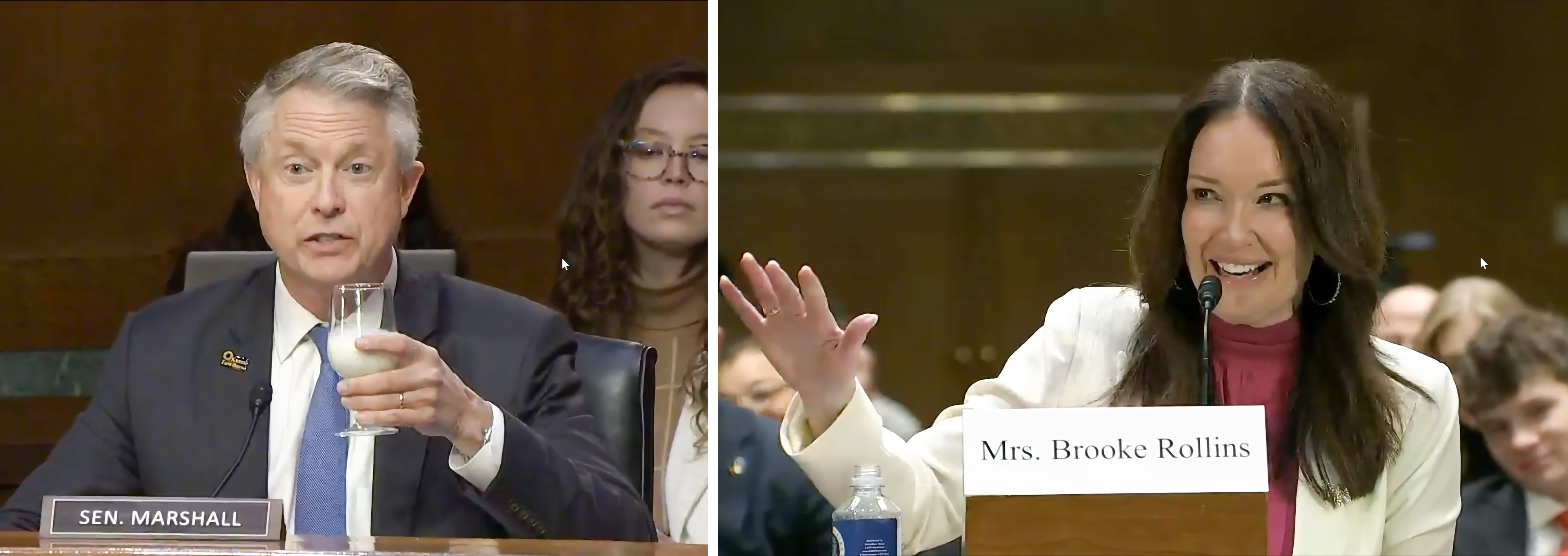

This split-screen moment captures Sen. Roger Marshall, M.D. and Agriculture Secretary Nominee Brooke Rollins during their confirmation hearing exchange on bringing whole milk choice back to schools. Sen. Marshall always comes prepared with THE MILK! Livestream screen capture by Sherry Bunting

From grassroots volunteers to halls of Congress, ‘hat’s off to 97 Milk’

WASHINGTON, D.C. – It was the high point of the four-hour confirmation hearing on Jan. 23rd for President Trump’s Ag Secretary nominee Brooke Rollins, when Senator Roger Marshall, MD (R-Kan.) poured himself a glass of whole milk in front of the television cameras, and said:

Ms. Rollins, welcome. I want to know if you agree with me that whole milk is the most nutritious drink known to humankind and belongs in our school lunches.”

He then promptly took a big swig of nature’s nutrition powerhouse that American children have been banned from consuming at school meals since 2012.

Yes, there was a ripple of good-natured laughter throughout the room at the absurdity of it all – the absurdity that this nutrition powerhouse has actually been banned for 13 years on school grounds to even be bought with one’s own money from midnight before the start of the school day to 30 minutes after the end of the school day, per the 12-years of King Vilsack that Secretary Perdue’s interruption even failed to overturn.

The new Ag Secretary nominee Rollins responded with a hand motion to her mother two rows back among the family, friends, colleagues, ag teacher, fellow former FFA state officers and current little league team she coaches in attendance for the confirmation hearing, as she replied with a hearty and all-too-knowing laugh:

“Senator, I don’t know that you have met my mom – yet. But this is all we had in our refrigerator growing up – not anything else – just whole milk. She is absolutely never going to let us forget this – the fact that this is coming up! But yes, this hits home to me very quickly,” said Rollins.

On the very same day, whole milk champion U.S. Representative Glenn ‘GT’ Thompson (R-Pa.) with prime cosponsor and pediatrician Rep. Kim Schrier (D-Wash.), along with Senator Marshall and prime cosponsoring Senators Peter Welch (D-Vt.), Dave McCormick (R-Pa.) and John Fetterman (D-Pa.) led the re-introduction of the bipartisan, bicameral Whole Milk for Healthy Kids Act of 2025, known as H.R. 649 in the House with 90 total cosponsors to-date, and S. 222 in the Senate with 12 total cosponsors to-date.

The bill in its fifth attempt will allow unflavored and flavored whole (3.25 to 3.5% fat) and reduced-fat (2%) milk to once again be offered in school cafeterias, which are currently only permitted to have fat-free and 1% milk available for growing children, much of which is shunned or thrown away.

“Federal policy, based on flawed, outdated science has kept whole milk out of school cafeterias for more than a decade,” said Rep. Thompson in a Jan. 23rd press statement. “Milk provides 13 essential nutrients for growth and health, two key factors contributing to academic success. The Whole Milk for Healthy Kids Act of 2025 provides schools the flexibility they need to offer a variety of options, while supporting students and America’s hard-working dairy farmers.”

“As a pediatrician, I know how important a balanced and nutritious diet is for children’s health, well-being, and development,” added Rep. Schrier. “A healthy diet early in life leads to proper physical growth and improved academic performance and can set the foundation for lifelong healthy eating habits. Milk contains essential nutrients… This bill simply gives schools the option of providing the types of milk most kids prefer to drink.”

Sen. Marshall was blunt, saying, “(It) should never have been excluded from the National School Lunch Program. Now, 13 years after its removal, nearly 75% of children do not receive their recommended daily dairy intake. I believe in a healthier future for America, and by increasing kids’ access to whole milk in school cafeterias, we will help prevent diet-related diseases down the road, as well as encourage nutrient-rich diets for years to come.”

“Milk provides growing kids with key nutrients they need. Dairy is also an important part of Vermont’s culture and local economy, which is why our bipartisan bill to expand access to whole milk in our schools is a win for Vermont’s students and farmers,” said Sen. Welch.

Sen. McCormick said the bill “puts milk back in schools that growing kids actually want to drink. Pennsylvania’s dairy farmers supply this country (with it)… allowing schools to serve (it) in the lunchroom is just commonsense.

“Kids need it,” said Sen. Fetterman. “Let’s give them the option to enjoy whole milk again in schools – it’s good for them, they’ll actually drink it, and it supports our farmers. This bill is a simple solution that benefits everyone.”

Both National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) rushed to the forefront singing the bill’s praises and promptly issuing press releases, something that in past attempts took a little time.

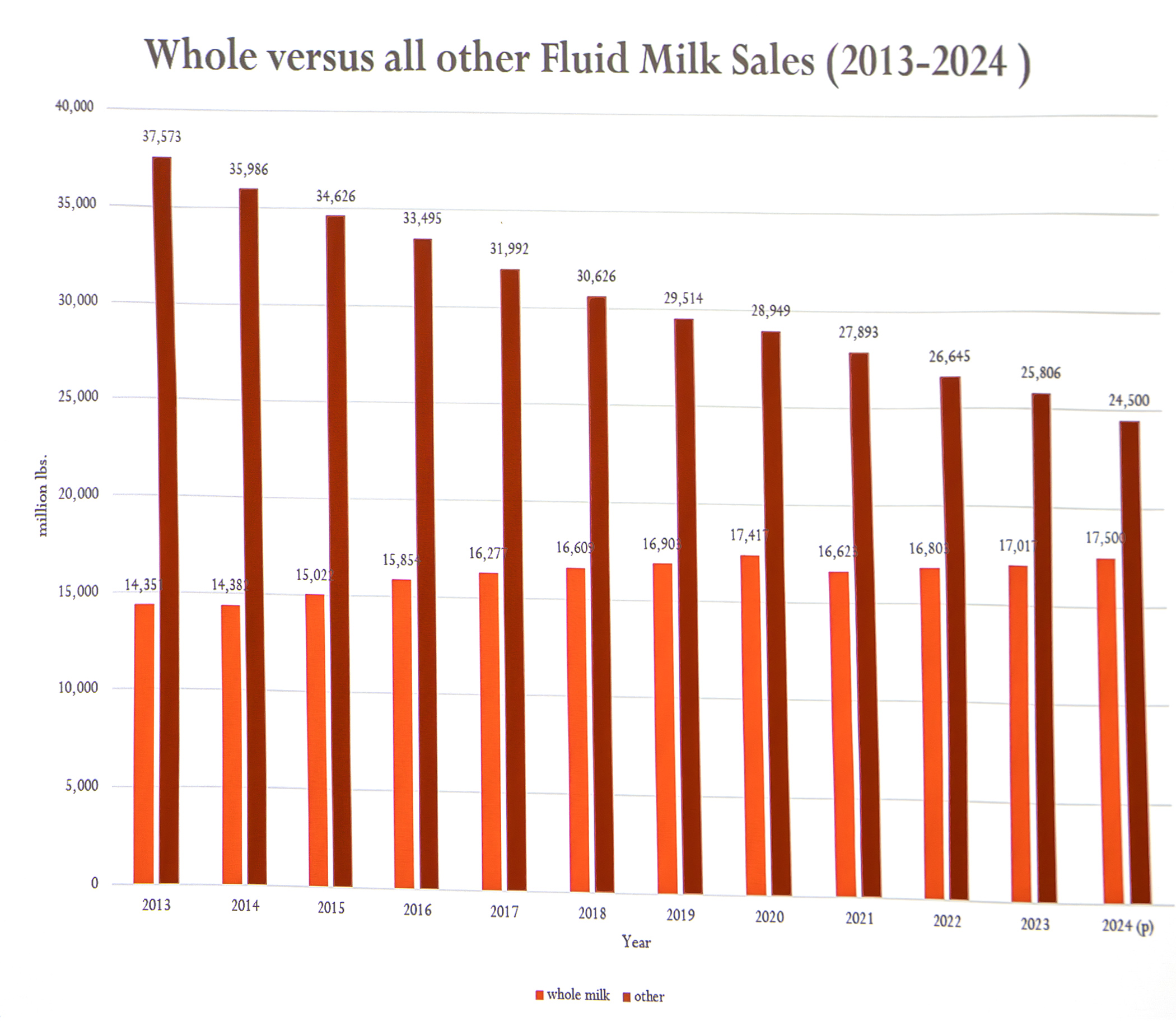

As longtime milk market guru Calvin Covington noted at the R&J Dairy Consulting seminar in eastern Lancaster County Jan. 28th, kudos go to the grassroots efforts. He showed the increase in whole milk sales nationally, while other fluid milk categories have declined. This has somewhat stabilized the steep losses the entire fluid milk category has suffered most steeply in the past 14 years.

“My hat’s off to all of you and what you have done here in Pennsylvania, throughout the state and country, in promoting whole milk. I just wish other dairy farmers would be grassroots like you are and get involved,” said Covington. “Your work has paid off. Look at this graph. In 2013, whole milk sales were a little over 14 billion pounds. Last year (2024 with 11 months of data) I’m estimating 17.5 billion pounds. Whole milk is coming up, and everything else is going down.”

Covington dug into the graph (above) further to show that in 2019, the amount of whole milk sold was 16.9 billion pounds. “But look what happened in 2020, it jumped up to 17.4 and then back down to 16.62 in 2021. That was the pandemic. People were home. Schools were closed,” he said.

“When they were home, they drank good-tasting milk, but unfortunately when the schools opened back up, they had to go back to the other stuff. But my hat’s off to what you’ve done here. We’re selling more whole milk, and one thing people forget is that 100 pounds of Class I milk sales with higher fat content — last year it averaged 2.4 in this market compared to what it was 15 years ago when it averaged less than 2% — the more fat sold in Class I milk, the more income for you as dairy farmers. Class I butterfat is worth more than butterfat in the other markets, so my hat’s off to what you’re doing.”

(Author’s Note: Yes, Covington is speaking of the good work, the hard work, of 97 Milk volunteers who formed the non-profit in 2019 after dairy farmer Nelson Troutman’s painted bales began appearing. This good work is sustained by a handful of volunteers and donations. Just think what could be accomplished with more involvement. One of those volunteers is Jackie Behr of R&J, who puts her marketing skills to work for 97 Milk. She reminded farmers that donations are needed to keep the milk education movement going. An Amish Wedding Feast fundraiser is scheduled for Feb. 8 at Solanco Fairgrounds, with sponsorships still available. The next 97 Milk meeting open to all dairy farmers is March 25 at Durlach-Mt. Airy Fire Hall near Ephrata, Pennsylvania. Check out 97milk.com to learn more about the milk education movement, and hit the donate tab to find out how you can help.)

Whole milk, new farm bill top their bipartisan to-do list

By Sherry Bunting, Farmshine, Jan. 17, 2025

HARRISBURG, Pa. – Bipartisan priorities were evident — especially on getting whole milk back in schools and completing a new farm bill — during Rep. Glenn ‘GT’ Thompson’s annual listening session on opening day of the Pennsylvania Farm Show Jan. 4th in Harrisburg.

With a thin Republican House majority, Thompson, who represents the largely rural 15th district of north central Pennsylvania, will continue as Chairman of the Ag Committee.

He introduced the more than 100 attendees to the Ag Committee’s new top Democrat, Ranking Member Angie Craig, who represents the mostly rural 2nd district of southeast Minnesota.

They were joined by Ag Committee and Ag Appropriations Committee member, Rep. Chellie Pingree, representing the 1st district of Maine, and by Pennsylvania Secretary of Agriculture Russell Redding.

Whole milk

“We got really close to getting this done,” said Thompson about his Whole Milk for Healthy Kids Act after Berks County dairy farmer Nelson Troutman with the Grassroots Pennsylvania Dairy Advisory Committee asked: What’s next for the bill in the new 2025-26 Congress?

“We have to start over, but there is a lot more support this time,” Thompson replied. He doesn’t see any obstacles on the House side after overwhelming bipartisan support in the 2023 floor vote.

He expects the bill to move quickly through the Education and Workforce Committee under its new Chairman Tim Walberg (R-Mich.), a whole milk bill cosponsor. Then Thompson will work with House leadership to get it on the calendar for a 2025 vote.

He said the Senate side also looks “very promising” as Sen. John Boozman (R-Ark), a supporter of the bill, replaces former Ag Committee Chair Debbie Stabenow (D-Mich.) who had blocked it.

Craig gave further assurance. She and the new Ag Committee Ranking Member on the Senate side, Amy Klobuchar (D-Minn.), are working together on this. “We do not see what we saw last time on the Democratic side to get this done for GT,” said Craig.

Both are Democrats from Minnesota who previously cosponsored the bill – Craig on the House side, Klobuchar on the Senate side.

Thompson credited the education and leadership of the Grassroots Pennsylvania Dairy Advisory Committee and 97 Milk in raising awareness and support. “The grassroots effort also helped improve the bill by suggesting language that makes sure the calories don’t count toward the fat in the school meal,” he said.

Pingree is also a big supporter of whole milk in schools. She was “amazed” to see all the Drink Whole Milk signs, banners, and painted bales while visiting her brother-in-law in Lancaster County, Pennsylvania.

“I don’t know too many states where you see something this interesting while you’re driving down the road. It’s pretty impressive. It has spread far and wide,” she noted.

Congresswoman Chellie Pingree (D-Maine) was “impressed” by the Drink Whole Milk signs along roadsides when she spent time in Lancaster County, Pennsylvania. That was music to the ears of Berks County dairy farmer Nelson Troutman with the Grassroots Pennsylvania Dairy Advisory Committee. His original painted round bales in December 2018 motivated the launch of the 97 Milk education movement in February 2019. It is run by volunteers and donations at 97milk.com

ESL milk

Troutman asked if the bill could address extended shelf life (ESL) milk in schools. He is concerned about taste and acceptance by students, saying “schools should only be allowed to serve ESL milk if that’s the only option available to them.”

His concern arises from the volume of new plant capacity coming online across the country for ESL and aseptic shelf-stable milk packaging, along with new Federal Milk Marketing Order formulas that will price Class I milk differently based on shelf life. This creates potential competitive issues, especially in Pennsylvania, for bottlers of conventionally pasteurized milk that tends to be more local vying for school contracts with ESL milk coming from potentially more distant locations.

Farm-to-School

State lawmakers and young people in attendance voiced further concerns about the quality of school meals and the practice of schools shipping-in prepackaged meals prepared out-of-state, leaving Pennsylvania agriculture out of the loop.

They requested incentives for local farm-to-school food programs. Frank Stoltzfus, a 9th generation farmer from Lancaster County pointed to the PA Beef to PA Schools program as a successful example.

These discussions come under the jurisdiction of the House Education and Workforce Committee and its “long overdue overhaul,” said Thompson: “The Childhood Nutrition Reauthorization is where we reform and refine to update school meals. I’ll be encouraging Chairman Walberg that we do that reauthorization, and this (ESL question) is something we can certainly take a look at.”

Pingree noted “some farm bill funding also goes to school meals, and we can put more into resupplying kitchens for on-site meal prep and local procurement.”

Nutrition overhaul

The last time Congress did a Childhood Nutrition Reauthorization was in 2010, when it tied school meals more strictly to the Dietary Guidelines for Americans (DGAs).

“When it comes to nutrition, if kids won’t eat it, then it’s not nutritional, and we are seeing a lot of waste today,” Thompson observed.

On that score, he pointed to “good reforms” to the Dietary Guidelines process that will again be part of the markup of the farm bill to “take some of the food politics out of the process coming from the so-called ‘experts.’ We want science-based not agenda-based guidelines.”

Farm bill

Asked about a timeline for the new farm bill, Thompson was optimistic. New committees are still being populated, and new members will need some farm bill education.

“But I would love to see this farm bill go to committee markup in the first quarter of this year — that is my goal – and then see it move quickly to the floor,” he said in a Farmshine interview after the event. “We will continue to do listening sessions, but I want to move ahead. We’ve had great input from all across the country, but I do think it’s important that we keep listening and touching base.”

Both he and Craig shared concerns about nosediving grain prices and net farm income. They differed on what constitutes cuts vs. cost-control on the Supplemental Nutrition Assistance Program (SNAP) that makes up the bulk of the now over $1 trillion farm bill. They both want the Inflation Reduction Act (IRA) funds pulled into the conservation title and baseline, but they differ on removing the IRA’s climate mandates for these funds.

Thompson warned about competition from conservatives who are interested in using these funds as ‘pay-fors’ on tax policy, which he said Ag Committee Republicans would oppose. “I want these IRA funds in this farm bill,” he said.

Craig said the IRA funds best practices like carbon sequestration, and Pingree said she likes the focus on resilience for healthy soils. They pointed to carbon markets that see the value and lauded Sec. Vilsack’s use of $3 billion in CCC funds for pilot projects that will “help give us better metrics.”

While there is general agreement that most practices on farms improve the planet, the question is – how do the things farmers already do get monetized?

“They are not getting enough credit for their ecosystem services — carbon sequestration, air quality, water quality, filtration of rain. Farmers improve our environment just by farming,” said former State Senator Mike Brubaker. “Is there some way for them to get paid?”

SUSTAINS Act

Thompson said the farm bill does not address this specifically, but legislation passed in 2022 includes the SUSTAINS Act, which he described as “providing a framework for private industry to be involved.”

Corporations and foundations can donate funds to USDA for conservation purposes, like improving technical assistance for more farmers to have access to popular programs like EQIP. He cited a “great return on investment” from Chesapeake Bay Foundation initiatives as an example.

But he pushed back on the Ag Secretary’s use of CCC funds for such purposes because administrations come and go, with their own changing priorities.

“Having certainty going forward is incredibly important,” he said. “Sec. Vilsack wanted to do things by regulation and his interpretation of how CCC funds could be used. He should have come to us (Congress), instead.”

Likewise, concerns were voiced about emerging land use policies at local, county, state and federal levels.

Renewable energy

Asked for their views on traditional and alternative energy, a bipartisan preference emerged for balancing affordable and renewable sources with science, technology and innovation as “pathways for solutions.”

“We need ‘all of the above’ because energy will be a mix for a very long time,” said Pingree. “But we have to stay in this (renewable) dialog.”

Thompson said the ultimate destination of the Farm Show butter sculpture — a digester on a Pennsylvania dairy farm — is a good example of renewable energy produced from cow manure and food waste.

Craig said biofuels through E15 standards are vital for corn and soybean farmers in her district of Minnesota, with new biobased aviation fuel standards an exciting opportunity that U.S. farmers should benefit from, not imported corn from Brazil.

“Our farmers have to be at the forefront of it, we have to get this right,” said Craig. “As Ranking Member, I’ve got to manage my caucus just like GT does as Chairman, to work together for the right solutions, which are probably somewhere in the middle.”

Food security

Questions were also raised about invasive species, animal health, and safeguarding the food supply — especially in regard to inspection of border crossings for invasive pests that threaten all types of agriculture and novel cross-species migration of highly pathogenic avian influenza (HPAI H5N1) in poultry and now dairy operations.

“We have to make sure we keep investing in our laboratories, inspections, and research,” said Thompson.

According to Redding, the Pennsylvania Diagnostic Laboratories System (PADLS) was born out of the poultry industry’s first difficult encounter with avian influenza back in the early 1980s. Today PADLS is instrumental as the state is one of the first to enter the mandatory national bulk milk testing strategy, and has established some protocols credited to the poultry industry.

He stressed the importance of cross-species engagement between Pennsylvania’s top two ag sectors of poultry and dairy, where biosecurity is essential.

“We’re at about 100% of milk representing our nearly 5000 dairy farms, and we’ve not found (H5N1) on the third cycle of testing now,” Redding reported. “The difficulty with a national strategy is finding a model that fits the diversity of all the states.”

Craig said HPAI is a big concern for her home state of Minnesota, which is No. 1 in turkey production and No. 7 in dairy.

They look forward to working with the new U.S. Secretary of Agriculture on what the national strategy looks like going forward “without overburdening the farmers.”

SAVANNAH, Ga. – Flat milk production volume, but with higher components, and a more unpredictable demand are factors new to the dairy industry that make price projections more difficult for the year ahead.

Calvin Covington has spent his life in milk marketing, now retired from managing Southeast Milk Inc., and before that working with cheese processors to see (and pay) the value of higher protein and fat when he was with the American Jersey Cattle Association earlier in his career.

Covington gave his dairy outlook for 2025, with emphasis on the Southeast markets during the Georgia Dairy Conference attended by over 400 in Savannah, Jan. 20th.

“I was way low on my projections last year. 2024 ended up with prices higher than anticipated,” he said.

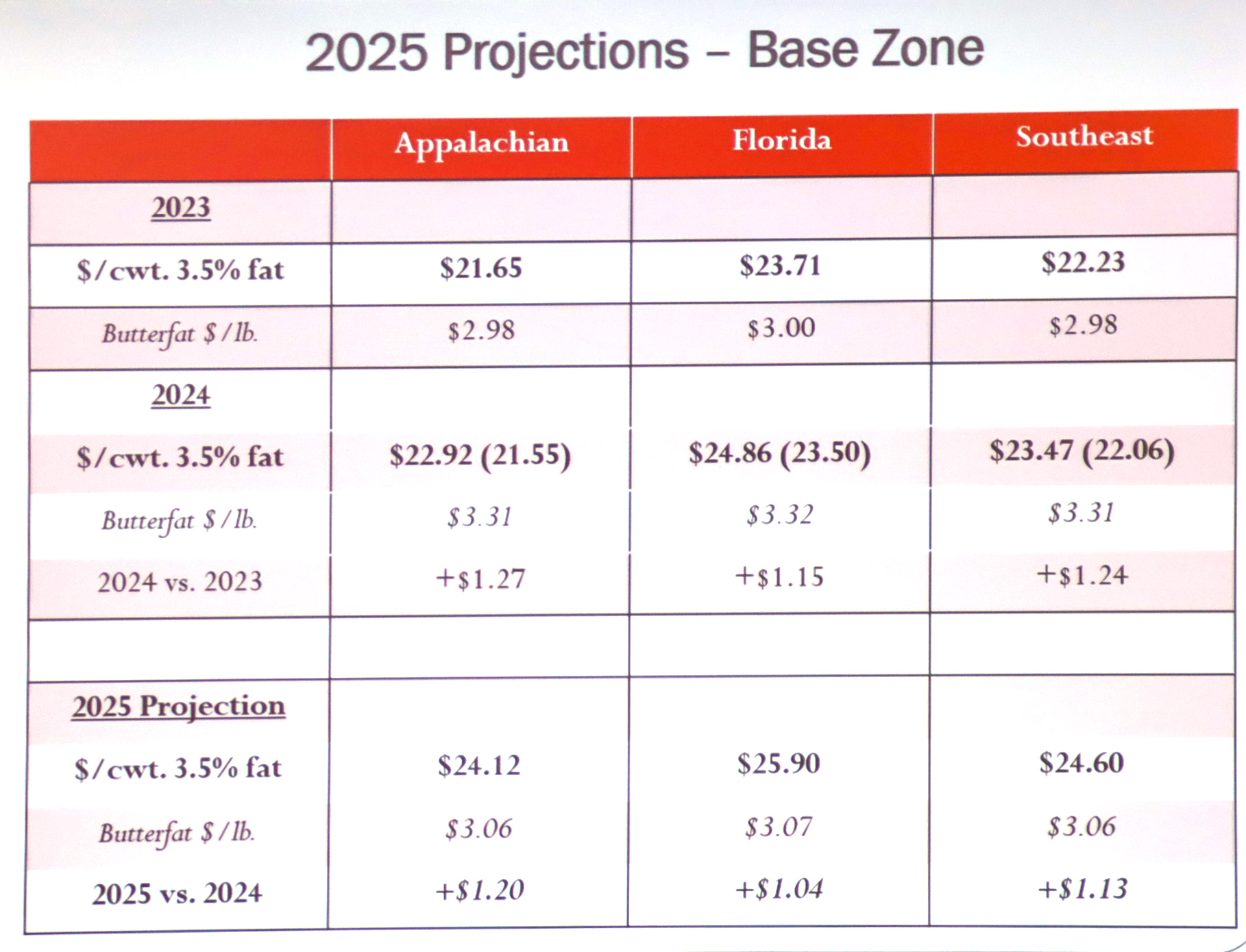

This year, he is projecting prices in the Southeast markets to rise by $1.20 per hundredweight as an average for 2025 vs. 2024 in the Appalachian region ($24.12), $1.40 in Florida ($25.90) and $1.13 in the Southeast Order ($24.60). Most of the increase will come from the skim side this year because the FMMO changes, which will be implemented in the second half of 2025, will pressure butterfat value.

Covington shared his price projections for Southeast milk markets for 2025.

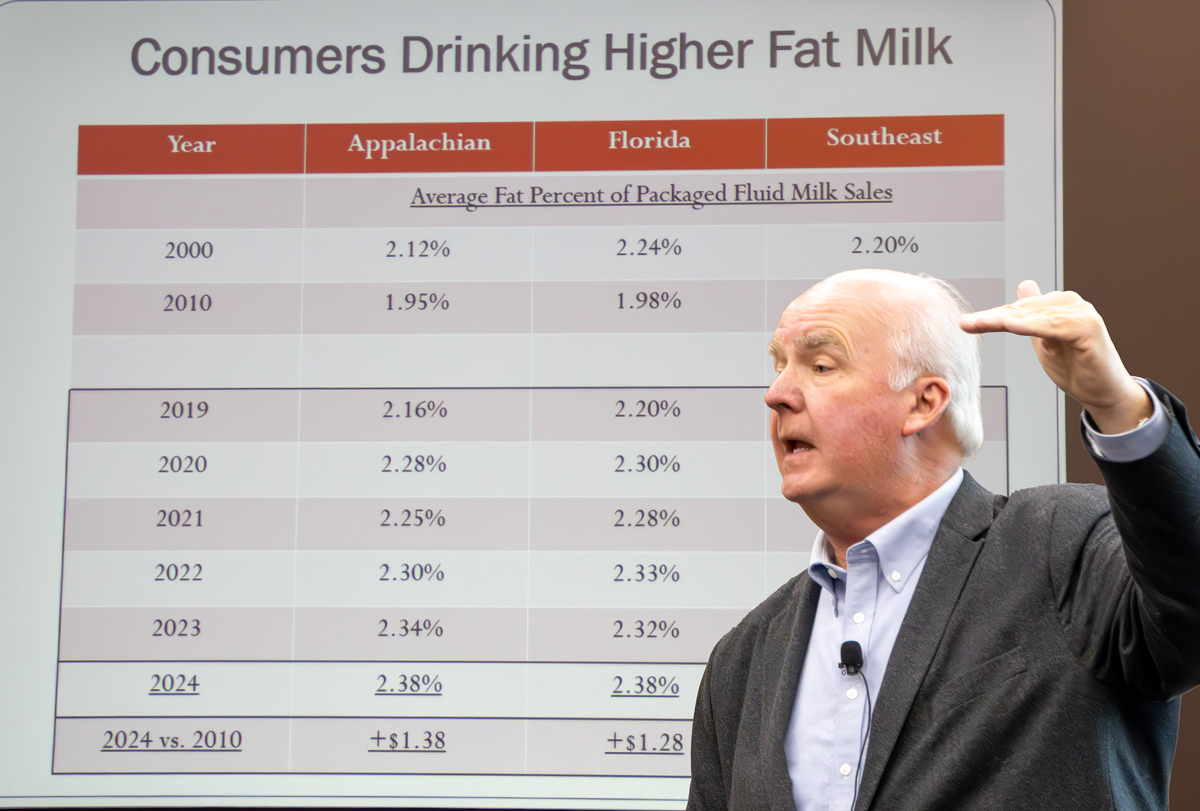

Producers are making higher butterfat milk, averaging well over 4.0% across the three Southeast Orders at 4.06 in Appalachian, 3.92 in Florida, and 4.11 in the Southeast. This compares with 3.65% across the three Orders in 2010.

“Additionally, consumers are also drinking higher fat milk,” said Covington, calculating the average fat percentage of Class I sales in the three Southeast Orders rose from 1.95% in 2010 to 2.4% in 2024.

Covington calculated that fat percentage in milk sales showing the change in consumer preference for higher fat milk puts more money in producer milk checks.

“In 100 pounds of Class I milk in the Appalachian Order, for example, that 2.38% fat made the milk worth more money, $1.38 per cwt more,” he said, with a chart showing Southeast producers saw a $1.28 benefit; Florida $1.35.

“There has been a big change in consumer preference, and that has raised your Class I price,” he said.

He commended dairy producers for improving their components, which has also improved their milk price.

“You’ve done this through genetics and feeding and nutrition programs, and it’s not going to stop. We are moving quickly to Holsteins making milk like Holsteins and testing like Jerseys.”

Other good news heading into 2025 is dairy product inventories are in good shape, he said. Cheese stocks are down, powder is up just a small amount, dry whey inventory is way down and butter inventory is flat.

Dairy product demand is up, but Covington sees a bit of a challenge looking at demand on a total solids basis because “we are exporting more cheese and less powder.”

Looking ahead, he gave attendees a lot to think about on the changing structure and markets in the dairy industry.

Covington observed that 10% (140) of the 1408 dairy farms that were counted in the 2022 Census of Agriculture in the Southeast had 64% of the region’s milk sales.

Of that 140, there were 22 farms with 2500 cows or more, producing 32% of the region’s milk.

“This is happening all over the country,” said Covington. “We are getting more concentrated.”

This year the milk production advantage flipped back to Florida by slightly more than Georgia, but the two states together have reached 50% of Southeast milk sales. Covington thinks by 2030, “we will see 60% of the milk produced in the Southeast coming from Georgia and Florida.”

When asked what has led to Georgia’s rapid increase in production over the past few years, Covington said “Georgia dairy farmers want to expand and they have the ability to expand. They are progressively making more milk per cow and have the land mass and support.”

His “demand and supply” summary for the Southeast region shows 1160 dairy farms at the end of 2024, producing 8 billion pounds of milk with 32 regulated milk plants. The region had 8.3 billion pounds of Class I fluid milk disposition, and 0.9 billion pounds of Class II products processed.

Against those numbers, the amount of packaged fluid milk products sold in the Southeast was 10 billion pounds. “The Southeast is still a deficit area, and there is room for growth,” he said.

As for total U.S. milk production, Covington doesn’t see it rebounding any time soon. Cow numbers are moving lower and milk per cow is simply not making the year over year gains seen in the past.

“Milk production has been pretty constant for the last three years,” he said. “We have to go way back to see where that has happened before.”

But he also wanted producers to think differently about production, to realize that in making more components, their milk is generating more products. He calculates that today’s hundredweights of milk, nationwide, yield a half pound more cheese. That adds up.

“You as dairy farmers are doing this. By getting your components up, you are also improving sustainability over time. You are making more products from the same volume of milk,” Covington explained.

“Based on average component level changes, if a plant is making one million pounds of cheese a day, they now need 177 loads instead of 185 loads a day for that same output,” he said.

Calvin Covington shared that the collective impact of all the FMMO changes on the Northeast Order farms is likely to be neutral to slightly beneficial, while farms in the three Southeast Orders will benefit the most because of bigger Class I differentials and greater Class I utilization. Butterfat and other solids prices will be lowered, and the wild card will be protein because barrel cheese prices moved higher than blocks in 2024, but the barrel price will no longer be used in the protein price formula after June 1st. Photo by Sherry Bunting

SAVANNAH, Ga. and EAST EARL, Pa. — As part of his annual outlook for Southeast milk markets, and also in his look ahead for the milk market nationally and in the Northeast, well-respected retired milk co-op executive Calvin Covington broke down the final USDA Federal Milk Marketing Order (FMMO) formula changes into three categories: The positive, the negative, and the unknown. (Plus, there is also the ‘unvetted.’)

Covington spoke to over 300 attendees from 10 states at the 2025 Georgia Dairy Conference in Savannah onJan. 20th, just a few days after USDA’s announcement that producers in each of the 11 FMMOs approved the final rule. Then, on January 28th, he was in eastern Lancaster County, Pennsylvania speaking to 250 dairy farmers on this topic at R&J Dairy Consulting’s 18th Annual Dairy Seminar at Shady Maple Smorgasbord.

The FMMO changes will be implemented June 1, 2025, except for the increased milk composition factors, which will be delayed six months due to impacts on “risk management.”

Covington shared collective analysis based on USDA’s backward-looking data (2019-23), showing that all six pricing changes, combined, would have benefited producers by 26 cents per hundredweight across all FMMOs, nationwide, during those years.

“But, like the disclaimer on a financial prospectus, ‘past performance is not an indicator of future results.’ It is all relative,” he said. “The three Orders of the Southeast are by far the biggest beneficiaries, but going forward, there are a lot of things we just don’t know.”

Calvin Covington shared analysis of how the recently approved FMMO milk pricing changes could collectively impact each of the 11 Orders, but warned that analysis based on past performance, may not be an indicator of future results.

Orders with estimated negative net impact at test are: Pacific Northwest (124) -5 cents; Upper Midwest (30) -9 cents; Arizona (131) -11 cents; and California (51) -27 cents.

Orders with estimated positive impacts at test are: Appalachian (5) +$1.90; Southeast (7) +$1.80; Florida (6) +$1.43; Central (32) +52 cents; Mideast (33) +50 cents; Northeast (1) +35 cents; and Southwest (126) +7 cents.

The good

“The Southeast will see the majority of benefit, with the updated Class I differentials,” Covington reported, illustrating how they vary by location for an average increase of $1.42 per cwt across the country – but only for Class I milk. The three Orders of the Southeast will see more of this benefit because they have the largest Class I differential increases and their blend prices are predominantly Class I.

A University of Wisconsin-Madison study had previously looked at where the plants are and where the milk is, in order to think about moving milk from where it more is produced to where it is needed.

The highest differential increase is along the route 85 corridor, beginning near Atlanta, up into West Virginia, where there are plants but no milk. Interestingly, his chart showed that the smallest increases for the region are in Florida locations as well as Valdosta, Georgia, where the new Walmart milk plant is being built.

In the Northeast, Covington said dairy farmers will have to get used to what this looks like on their milk check, and they will also see more incentive to move milk South under these new differentials.

“Each county has a differential assigned to it,” he said, pointing to the area of the R&J Meeting, near New Holland seeing a $1.40 per cwt. increase in Class I differential, but this is a smaller increase compared to the much larger increase put on at Boston, Mass.

“That big increase in Boston is because there’s not any milk around there, and it’s raised to get the milk to move to the people there,” he said. This means that even though the new Class I differential will raise the Class I price in New Holland, “farmers will have to get used to seeing their location differential as a bigger negative on the milk check,” because the increased differential in Boston is so much bigger.

The milk composition factor updates are straightforward, he said, yielding about a 35 cents per cwt benefit to the Class I milk price in all FMMOs, and will raise the standardized skim value of the other classes in the three southeastern Orders that are still priced as fat/skim instead of by multiple component pricing.

The bad

The make allowance increases will lower the price for butterfat and other solids value, he said, “but we don’t know what will happen with the protein price because of the elimination of the barrel cheese prices from the formula.”

This will manifest as lower butterfat and other solids component prices for the Northeast, he said. “We would expect the protein price to be higher, based on history, but that depends upon the block to barrel price spread and its relationship to the butterfat price.

The unknown

Historically, the 500-pound barrel cheese price was lower than 40-pound block price.

“Last year, however, barrels have been higher, so we don’t know,” said Covington.

Also in the unknown category is the return to the ‘higher-of’ as USDA’s method for setting the base Class I skim price.

“In the past five years, the average-of method cost dairy farmers millions of dollars, but we don’t know going forward if the skim factors (Class III vs. Class IV) will get back to being closer together, which would lower prices. If the spread stays wide, this change to the higher-of will increase prices,” he explained.

When asked if the Covid pandemic created the loss in Class I value under the average-of vs. higher-of, Covington said the Covid period — while most obvious — only accounts for one year out of five years in which the spreads between Class III and Class IV and between block and barrel cheese were detrimental.

“The thing going forward is, we just don’t know,” he said.

The unvetted

The sixth change is not listed separately in the Jan, 16th USDA notice to trade, and it was not part of any hearing proposal. Covington said he views the extended shelf life (ESL) adjuster as “a new class of milk.”

“The ESL adjuster is only on Class I. You’ll have a Class I mover skim price that will be calculated for conventional milk based on the higher-of III or IV,” he said. “Then you need a big spreadsheet to show what’s going to happen next. They’ll look 36 months previous to 12 months previous at the difference between the higher-of and the average-of, and that will be the adjuster to use for ESL milk that month.”

He estimates the ESL adjuster would have averaged -30 cents in 2024, but for some months it would have been a plus.

“My initial analysis is that it will not make a whole lot of difference in the short term, but we just don’t know going forward if some will try to manipulate this,” he said. “My concern is that it was not proposed at the hearing at all, and there’s no definition for extended shelf life. I know being in this business all these years, if there is a way to work around it for a benefit, they will find a way to do it.”

When asked about the competitive issues between conventional and ESL fluid milk and between out-of-area packaged ESL milk competing with in-area fresh milk, Covington observed potential competitive issues between conventional and ESL milk in the same area.

“You’ll have two different costs at the same location. What has always been the beauty of the Federal Order system is having the same raw product costs at the same location,” he said, adding that new ESL plants are being built and others are expanding.

“As ESL grows… there could be some months with a price advantage,” Covington suggested, pegging that difference historically to be as much as $1.00 per cwt in some months. “That kind of difference can create disparity between conventional and ESL milk.

“The thing is, we just don’t know, going forward, what it’s going to look like.”

Covington urged farmers to pay attention and be involved. Federal Order reforms are a slow process involving a lot of time and compromise. Changes this big only happen about every 25 years, he said.

He noted that Farmshine has kept dairy farmers “well-informed” with effective reporting on the markets and the FMMO process.

He said that as more manufactured products are sold and less fluid milk, compared with 25 years ago, the future could look different if future administrations and lawmakers feel differently about the pricing of milk. If manufacturers perhaps choose not to participate, FMMOs could some day be looked to primarily for handling the payments and test weights.

However the future plays out, Covington urged: “Stay informed and be involved because it is your milk check.”

Editorial Analysis: Tumultuous 2024 spills over into 2025 – Part One

By Sherry Bunting, Farmshine, January 3, 2025

EAST EARL, Pa. – Year 2024 was tumultuous, and 2025 is shaping up to be equally, if not more so. Spilling over from 2024 into 2025 are these three areas of potential for good news to trump bad nutrition policies that are having negative impacts on dairy farmers and consumers.

Farm bill and whole milk bill

Both the farm bill and the whole milk bill showed promise at the start of 2024. No one championed the two pieces of legislation more than House Ag Committee Chairman Glenn ‘GT’ Thompson (R-15th-Pa.). He even found a way to tie them together — on the House side.

The Whole Milk for Healthy Kids Act made it farther than it ever has in the four legislative sessions in which Thompson introduced it over the past 8 to 10 years. It reached the U.S. House floor for the first time! But even the overwhelming bipartisan House vote to approve it 330 to 99 at the end of 2023 was not enough to seal the deal in 2024.

GT Thompson, found a workaround to include it in the House farm bill, which passed his Ag Committee on a bipartisan vote in May. The language was also part of the Senate Republicans’ draft farm bill under Ranking Member John Boozman (R-Ark.)

It too fell victim to Stabenow dragging her feet in the Senate. By the time the Ag Chairwoman released a full-text version of the Senate Democrats’ farm bill, little more than 30 days remained in the 2023-24 legislative session.

Key sticking points were the House focus on dollars for the farm side of the five-year package. It put the extra USDA-approved Thrifty Food Plan funding into the overall baseline for SNAP dollars and brought Inflation Reduction Act climate-smart funds under the farm bill umbrella while removing the methane mandates to allow states and regions to prioritize other conservation goals, like the popular and oversubscribed EQIP program.