EDITORIAL – OPINION

By Sherry Bunting, Farmshine, July 16, 2021

Farmshine readers will recall coverage of the U.S. Senate Ag Committee’s climate hearing in 2019, when Tom Vilsack, then president and CEO of U.S. Dairy Export Council, lobbied the Senate for climate-pilot-farm-funding. Remember, he announced DMI’s Net Zero Initiative at that hearing – five months ahead of its formal unveiling.

In that same June 2019 hearing, animal scientist and greenhouse gas emissions expert Dr. Frank Mitloehner of University of California-Davis explained the methane / CO2 ‘biogenic’ cycle of cows.

He said that no new warming, is produced when cow numbers are “constant” in an area because methane is short-lived and converts to CO2 in 10 years time, which is then used by plants, cows eat the plants, and the cycle repeats. It is always cycling.

Dr. Mitloehner also said that this cycle changes when cattle concentrations move from one area to another.

Nationally, dairy cow numbers are rising after decades of declining. However, in the Northeast and Southeast milksheds, cow numbers are declining — and by a wide margin.

This should indicate net methane reductions in the biogenic cycle or climate-friendly milk for the fluid milk regions of the Northeast and Southeast.

As USDA and the industry coalesce around DMI’s unified approach through the Net Zero Initiative and the work of DMI’s Dairy Scale for Good with partner WWF — stating large integrators can be net zero in five years to spread their climate ‘achievements’ across the footprint of all milk in the dairy supply chain — I have to wonder what this means for the areas of the country beyond the ‘chosen’ growth areas.*(see footnote at the end)*

Looking at the work of DMI’s Innovation Center and it’s fluid milk revitalization committee, sponsoring the launches of various diluted dairy-‘based’ beverages, something occurred to me from a marketing standpoint.

Here is a thought that could be helpful in the future for whole fluid milk bottled regionally to compete with emerging climate claims of dairy-‘based’ beverages that are made with ultrafiltered solids shipped by centralized cheese and ingredient facilities (without the water) to be reconstituted as mixtures with plant-based alternative beverages for population centers on the coasts.

The milk produced and bottled in the Northeast and Southeast milksheds is not just climate neutral, it’s already offsetting, producing not just no new methane, but less than prior-decades’ methane.

Bear in mind, these new dairy-‘based’ — blended — beverages are NOT Class I products. I have been informed that the 50/50 blends, for example, do not meet the standard of identity for milk, nor do they meet the milk solids profile that requires Class I pricing. This means that even though milk is part of a fluid dairy-‘based’ beverage, it is not priced as Class I.

The milk used in these emerging products that combine ultrafiltered solids with water, additives and maybe an almond or two, fall into Class II or IV, some are Class III if whey protein is used. Examples include products like DFA’s Live Real Farms ‘Purely Perfect Blend‘ that arrived recently in Pennsylvania and the greater Northeast after its first test-market in Minnesota.

Think about it. Unity is great on many levels, and is to be encouraged in an industry such as dairy, but when it comes to marketing, who is calling the shots for future viability within the DMI integration strategy, otherwise known as unity?

Pre-competitive alliances and ‘proprietary partnerships’ working on food safety are wonderful because all companies should work together on food safety. But animal care? Environment? Climate? Why not just offer quality assurance resources and pay farmers certain premiums for investing as companies would like to see and pay them for providing the consumer trust commodity — instead of implementing one-size-fits-all branches in programs like F.A.R.M.?

These so-called voluntary programs have the power to negate contracts between milk producers and their milk buyers even though consumer trust is a marketable commodity that producers already own and are in fact giving to milk buyers, and their brands, without being compensated.

Instead, producers are controlled by arbitrary definitions of the consumer trust commodity that the producers themselves originate. This goes for Animal Care, Worker Care, Environment, and Climate.

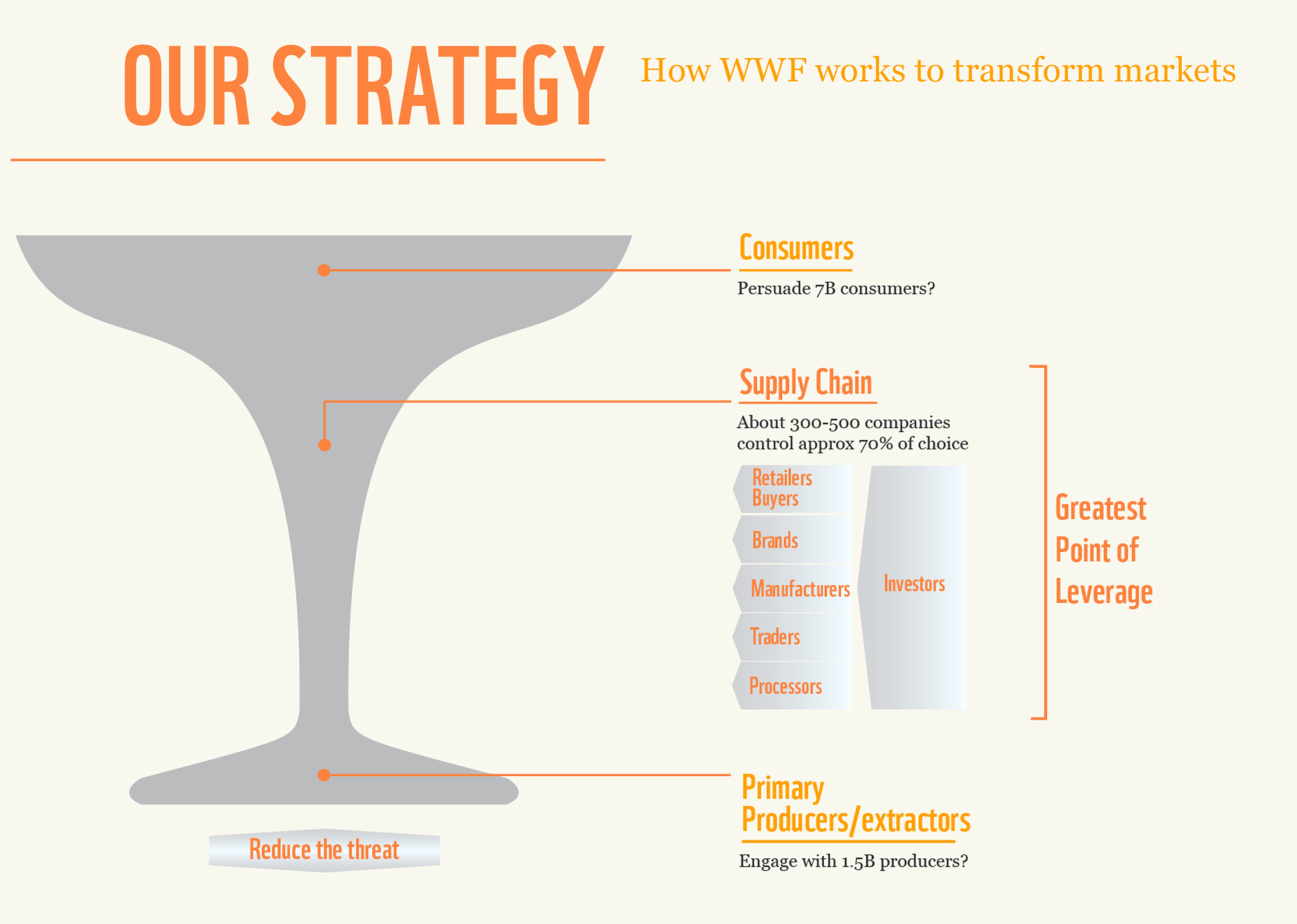

The pre-competitive model used in food safety is applied to all four of the above areas today. This is exactly the supply-chain model World Wildlife Fund (WWF) — DMI’s ‘sustainability partner’ — set in 2010 to “move the choices of consumers and producers” where they want them to go.

*footnote

In the 2019 Senate hearing referenced at the beginning of the above op-ed, Dr. Mitloehner stated that the mere fact there are 9 million dairy cattle today compared with 24 million in 1960 and producing three times more milk shows that dairy producers are collectively not only emitting zero new methane, they are reducing total methane as old methane is eradicated by the carbon cycle and less new replacement methane is emitted.

The problem may be this: Year-over-year cow numbers for the U.S. are creeping higher. While still much lower than four to five decades ago, the issue emerging for DMI’s Innovation Center for U.S. Dairy is how to accommodate growth of the new and consolidating dairy structures to attain the checkoff’s expanded global export goal and to accommodate massive new dual-purpose plants if dairy farms in other areas remain virtually constant in size, grow modestly, or decline at a rate slower than the ‘designated’ growth areas are growing.

DMI is at the core of this, you see, to reach it’s new collective net-zero goal, cow numbers would have to decline in one area in order to be added in another area, or they will all have to have their methane buttons turned off or the methane captured because now the emissions are being tracked in order to meet one collective “U.S. Dairy” unit goal under the DMI Innovation Center and F.A.R.M. We don’t even know if they are using this method of calculation. U.S. cows may be on global calculations where numbers are rising.

At that 2019 Senate hearing, Dr. Frank Mitloehner testified that dairies already create zero new methane but this can be tricky when cattle move from one area to another (as we see in the industry’s consolidation). Then we have DMI’s Dairy Scale 4 Good claiming the dairies over 3000 cows can be net-zero in 5 years and ‘spread their achievement’ over the entire milk footprint. Do we see where this is going?

Will all dairy farms have to meet criteria — set by organizations under the very umbrella of the checkoff program they must fund — to get to a ‘collective’ net-zero using the GHG calculator developed by the checkoff-funded Innovation Center in conjunction with its partner WWF (12 year MOU)? This GHG calculator has been added to the FARM program. These are the big questions. Where is the science and the math?