By Sherry Bunting, Farmshine, March 1, 2024

EAST EARL, Pa. — As seeds of doubt are being sown internally within the dairy industry about whole milk in schools, we have discussed Confusion (will it help milk prices?) and Consternation (unfounded fear about what will processors do with ‘all that skim?’)

This week, we look at the third C: ‘Competition’: If schoolchildren are offered whole milk, will it significantly impact butterfat supplies, raise butter prices, and compete with the industry’s cheap milk cheese-focused future?

Every winter conference for the past few years has had at least one speaker telling dairy farmers that fluid milk sales are declining because Americans are eating more of their milk instead of drinking it.

Fair enough. Cheese is the future, and the industry wants to make more of it. Lots more of it. So much more cheese, in fact, that inventory is growing. Analysts at conferences put up slides with the words “Export or perish!” in large font.

Yes, U.S. Dairy wants to export more cheese, including mozzarella. U.S. Dairy wants to export more butter and cream products. U.S. Dairy wants to export more of the higher-value products. (And we want to sell more cream to the upscale coffee houses and downscale McCafe drinks we adults get to choose while junior sips a paltry half-pint of fat-free chocolate milk, sugar water, in the back seat. What’s wrong with us?)

The industry also wants to take milk down to its molecular level – to turn the jug of milk into ingredients at the start — to make new function-targeted products for the beverage space outside of Class I parameters within an increasingly Class III dominated processing infrastructure.

Toward that end, new processing capacity won’t convert milk to traditional products, leaving elements to be marketed as ingredients. Instead, these new state-of-the-art cheese and ingredient plants start by taking milk apart to the ingredients-level to be used in making health beverages, bars, and other products, as well as to make cheese.

At the Georgia Dairy Conference in January, IDFA CEO Michael Dykes mentioned IDFA’s support for the Whole Milk for Healthy Kids Act, giving attendees a QR code to weigh-in with their Senators.

Later in his presentation, he noted that a shift to more fat in school milk would make a 3% impact on the butter supply.

“I’m a believer that the markets work, when you take it one place, you make a difference and change it someplace else. Those are the things we can work through,” said Dykes.

So, we reached out to Calvin Covington, a former cooperative CEO who is intimately familiar with component pricing as it became part of the Federal Milk Marketing Order (FMMO) system over 20 years ago. We asked his thoughts on how increasing fat in the school milk supply would impact butter.

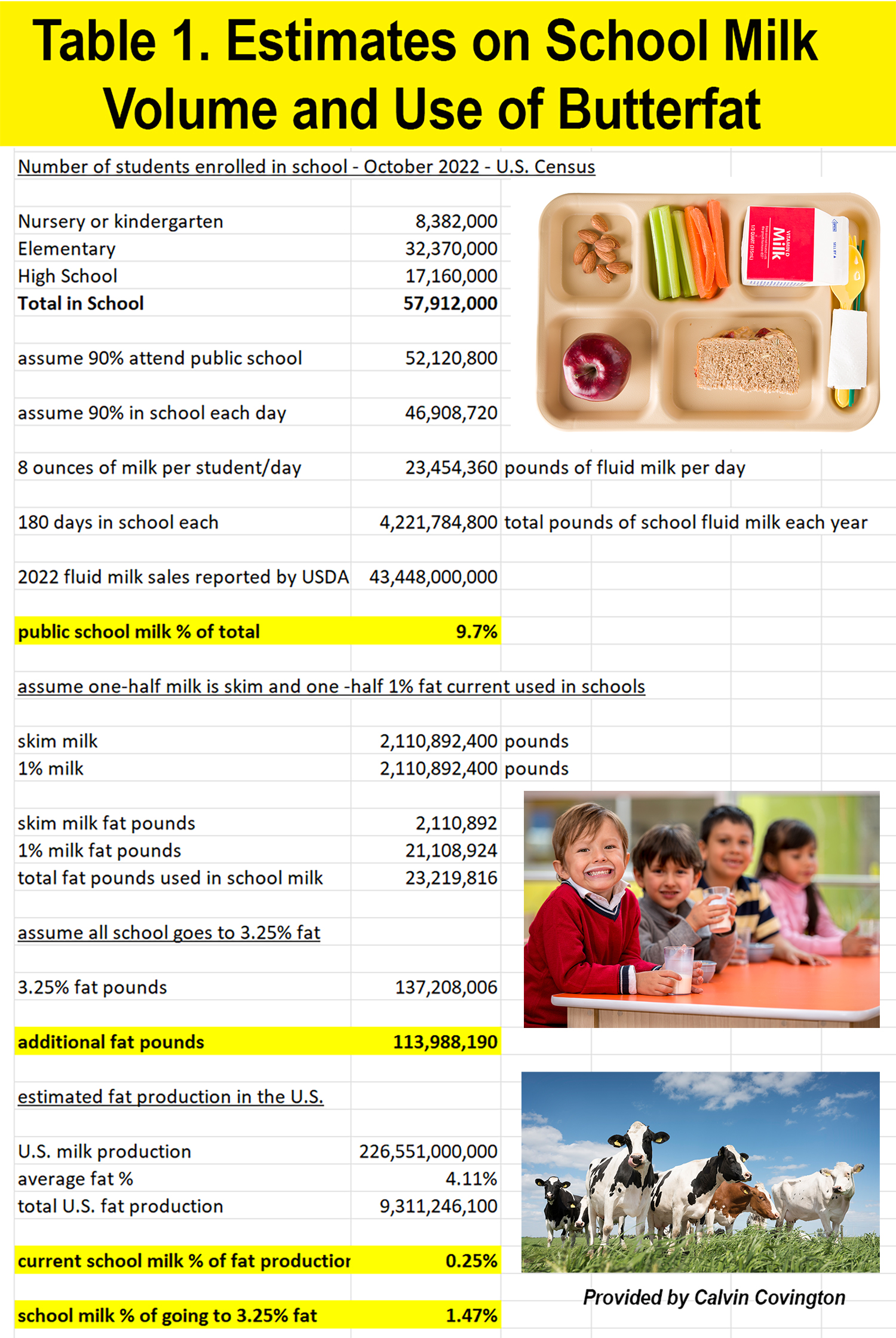

“Increased Cheddar cheese production has used millions and millions of pounds of butterfat. No one complains about this. Doesn’t the dairy industry want to increase demand for all milk components?” he replied and sent forth his own calculations, providing a spreadsheet showing his estimates of milk used in schools and the additional fat that would be needed for all of that milk to go completely to 3.25% (whole) milk.

Covington ran the numbers, moving methodically through assumptions on Table 1 to conclude the impact of shifting from a school milk fat percentage of 0.5% (half fat-free and half 1%) all the way to 3.25% (whole milk) would have a small impact on the butterfat supply — raising the school milk’s usage of butterfat from 0.25% of total butterfat production at the current national average fat test of 4.11% to being 1.47% of total butterfat production at the average 4.11% fat test.

He estimates public schools use 9.72% of all fluid milk, and for the purpose of the spreadsheet exercise, he assumed that half of those school milk sales are currently fat-free and half are 1%. If that is the case, then going to 3.25% (whole) milk for all pounds of school milk sales, the additional fat that would be needed is almost 114 million pounds, he reports.

“This should be a non-issue,” Covington concludes, using estimates that are based on all of those school milk pounds moving to 3.25% fat.

The more likely scenario, however, is that schools would implement a more gradual increase in fat percentage. If it mirrored the national average for fluid milk sales at 2% fat, the increase would be smaller initially. Using Covington’s chart and assumptions, the additional fat that would be needed if school milk fat content averaged 2% is closer to 84 million pounds, going from using 0.25% of total fat production to 0.9% of total fat production.

Not all schools will choose to offer all milk at 3.25%. Some may offer 2% milk, which has also been banned since 2010 and would be given regulatory relief under the Whole Milk for Healthy Kids Act.

Even if 3.25% fat milk is universally offered, some schoolchildren will continue to choose low-fat milk, as they did in the Pennsylvania trial, where the preference was 3 to 1 for whole 3.25% over low-fat 1%.

While a potentially higher fat content in school milk is being scrutinized for its impact on butter and butterfat, the impact of aggressive increases in cheese production is ignored. This speaks a bit to industry priorities.

“As butter and cheese consumption increase, processors do not argue against the increase because utilizing more fat would increase the fat price,” Covington observes, wondering why anyone would be concerned about the impact on butterfat supply if children get to choose whole milk while not being concerned about the impact on butterfat supply in any other sector.

“An increase in fluid milk sales, in schools, or anywhere, benefits all dairy farmers. With all things being equal, it would shift milk from Class III and IV to Class I, which is a (normally) higher milk price,” Covington explains. “If Class III or IV need more milk to replace the loss to Class I, more money would need to be paid by Class III and IV milk buyers, again, helping dairy farmers.”

So, what is the current status of butterfat production and usage?

The national butterfat average is 4.11%. A decade ago, it was 3.69. From 2011 to 2022, total butterfat pounds produced on farms in the U.S. grew by 2 billion pounds from 7.3 billion to 9.3 billion. That’s a butterfat volume response to a price signaling demand.

Where’s it all going? Around 20% goes to butter production, 8% to ice cream and frozen desserts, 10% in fluid milk sales, and close to 50% is used in cheese production. And then there is this growing market for cream used in coffee drinks.

Meanwhile, dairy producers out West report receiving a letter from a large cheese plant, putting in a new base program at 1.5% over base.

Another producer in an unregulated state in the West reported receiving a letter from his cheese plant stating they will reduce the butterfat multiple in their cheese milk payment, beginning April 1. The reason, according to the letter, is the farms are making too much butterfat, and the plant is having to buy condensed solids (skim) to pair with the additional fat or sell the extra fat as excess sweet cream at a loss.

During the FMMO hearing, fluid milk bottlers complained that the higher fat and component levels in milk today are more costly for them to deal with, that they must move the excess cream at a loss, and they have to clean the separator more often because of ‘sludge’ buildup. (I kid you not, one witness called it ‘sludge.’)

Processors have petitioned USDA with multiple proposals to get regulated minimum prices down to their definition of a ‘market clearing’ level that then allows them to add market premiums to attract new milk. Read that sentence again.

Who would be paying those premiums to grow milk supply? Not the processors. It would be revenue coming out of the regulated minimum price benchmarks for all farmers, including farmers that are not growing, to then get added back in by the processors wherever they want to direct growth.

Cheap milk is the name of the game, while at the same time, dairy farmers are being challenged to grow to meet the future ‘demand gap’ to fill $7 billion in new processing investments that will become operational over the next few years.

Dairy analysts tell how milk production expansion to meet this investment will not be as easy to do and will take longer than in the past because of the shortage in replacement heifers.

We’re at a standoff, so to speak.

Dairy producers have bred beef-on-dairy to bring margin back to their farms after 10 years of dairy margin compression. This strategy has been a good hedge against overproduction of milk in the era of sexed-semen, and it has helped protect farm balance sheets by reinforcing the value of the cattle as collateral.

So, what tool will be used now to drive consolidation and growth in dairy? Dykes told Georgia producers that, “Sustainability will be one of the biggest drivers of consolidation we’ve seen in a generation. Why? Because it’s going to take investment, and it’s going to take scale. We need to figure it out, to measure it, verify it, account for it, not double count it. We’re going to need investments to make sure we have the infrastructure.”

He said sustainability will become the gateway for exports where countries have mandates and carbon taxes for purchased ag products.

So, here we are back at the question about milk supply, butterfat supply, skim supply and school milk. Wouldn’t whole milk sales to schools offer a much-needed tug on the demand side to help shift some milk away from this runaway, market-depressing, buildup of excess cheese production that elicits the powerpoint headline: ‘Export or perish?’

Just think, if the fluid milk sales to schools increased as they did in the Pennsylvania trial by 52%, or even half that, by 25% as more kids choose milk instead of refusing it, market principles could work — gaining something in one place to affect it someplace else.

Meanwhile, the industry can do some soul-searching and adapting amid the double-speak. If more milk, fat and components are needed, then farmers need to be able to make a living milking cows and producing fat and components.

Is the problem not enough milk? Or too much milk? Not enough fat? Or too much fat? Not enough skim? Or too much skim? Or is the problem rooted in making sure milk can be bought cheap and that farmers are forced to find revenue in other ways, such as carbon monitoring?

Let’s get it straight please.

On the horizon, we see: Checkoff-funded fluid milk innovations for new beverages that identify and separate specific milk molecules for specific benefits (sleep drinks, energy drinks, immune function drinks, specific protein type drinks)? More on that in Milk Molecules Initiative Part I and Part II

-30-