Whole Milk for Healthy Kids Act reintroduced in style!

‘Most nutritious drink known to humankind’ takes center stage at Ag Secretary confirmation hearing

From grassroots volunteers to halls of Congress, ‘hat’s off to 97 Milk’

By Sherry Bunting, Farmshine, January. 31, 2025

WASHINGTON, D.C. – It was the high point of the four-hour confirmation hearing on Jan. 23rd for President Trump’s Ag Secretary nominee Brooke Rollins, when Senator Roger Marshall, MD (R-Kan.) poured himself a glass of whole milk in front of the television cameras, and said:

Ms. Rollins, welcome. I want to know if you agree with me that whole milk is the most nutritious drink known to humankind and belongs in our school lunches.”

He then promptly took a big swig of nature’s nutrition powerhouse that American children have been banned from consuming at school meals since 2012.

Yes, there was a ripple of good-natured laughter throughout the room at the absurdity of it all – the absurdity that this nutrition powerhouse has actually been banned for 13 years on school grounds to even be bought with one’s own money from midnight before the start of the school day to 30 minutes after the end of the school day, per the 12-years of King Vilsack that Secretary Perdue’s interruption even failed to overturn.

The new Ag Secretary nominee Rollins responded with a hand motion to her mother two rows back among the family, friends, colleagues, ag teacher, fellow former FFA state officers and current little league team she coaches in attendance for the confirmation hearing, as she replied with a hearty and all-too-knowing laugh:

“Senator, I don’t know that you have met my mom – yet. But this is all we had in our refrigerator growing up – not anything else – just whole milk. She is absolutely never going to let us forget this – the fact that this is coming up! But yes, this hits home to me very quickly,” said Rollins.

On the very same day, whole milk champion U.S. Representative Glenn ‘GT’ Thompson (R-Pa.) with prime cosponsor and pediatrician Rep. Kim Schrier (D-Wash.), along with Senator Marshall and prime cosponsoring Senators Peter Welch (D-Vt.), Dave McCormick (R-Pa.) and John Fetterman (D-Pa.) led the re-introduction of the bipartisan, bicameral Whole Milk for Healthy Kids Act of 2025, known as H.R. 649 in the House with 90 total cosponsors to-date, and S. 222 in the Senate with 12 total cosponsors to-date.

The bill in its fifth attempt will allow unflavored and flavored whole (3.25 to 3.5% fat) and reduced-fat (2%) milk to once again be offered in school cafeterias, which are currently only permitted to have fat-free and 1% milk available for growing children, much of which is shunned or thrown away.

“Federal policy, based on flawed, outdated science has kept whole milk out of school cafeterias for more than a decade,” said Rep. Thompson in a Jan. 23rd press statement. “Milk provides 13 essential nutrients for growth and health, two key factors contributing to academic success. The Whole Milk for Healthy Kids Act of 2025 provides schools the flexibility they need to offer a variety of options, while supporting students and America’s hard-working dairy farmers.”

“As a pediatrician, I know how important a balanced and nutritious diet is for children’s health, well-being, and development,” added Rep. Schrier. “A healthy diet early in life leads to proper physical growth and improved academic performance and can set the foundation for lifelong healthy eating habits. Milk contains essential nutrients… This bill simply gives schools the option of providing the types of milk most kids prefer to drink.”

Sen. Marshall was blunt, saying, “(It) should never have been excluded from the National School Lunch Program. Now, 13 years after its removal, nearly 75% of children do not receive their recommended daily dairy intake. I believe in a healthier future for America, and by increasing kids’ access to whole milk in school cafeterias, we will help prevent diet-related diseases down the road, as well as encourage nutrient-rich diets for years to come.”

“Milk provides growing kids with key nutrients they need. Dairy is also an important part of Vermont’s culture and local economy, which is why our bipartisan bill to expand access to whole milk in our schools is a win for Vermont’s students and farmers,” said Sen. Welch.

Sen. McCormick said the bill “puts milk back in schools that growing kids actually want to drink. Pennsylvania’s dairy farmers supply this country (with it)… allowing schools to serve (it) in the lunchroom is just commonsense.

“Kids need it,” said Sen. Fetterman. “Let’s give them the option to enjoy whole milk again in schools – it’s good for them, they’ll actually drink it, and it supports our farmers. This bill is a simple solution that benefits everyone.”

Both National Milk Producers Federation (NMPF) and International Dairy Foods Association (IDFA) rushed to the forefront singing the bill’s praises and promptly issuing press releases, something that in past attempts took a little time.

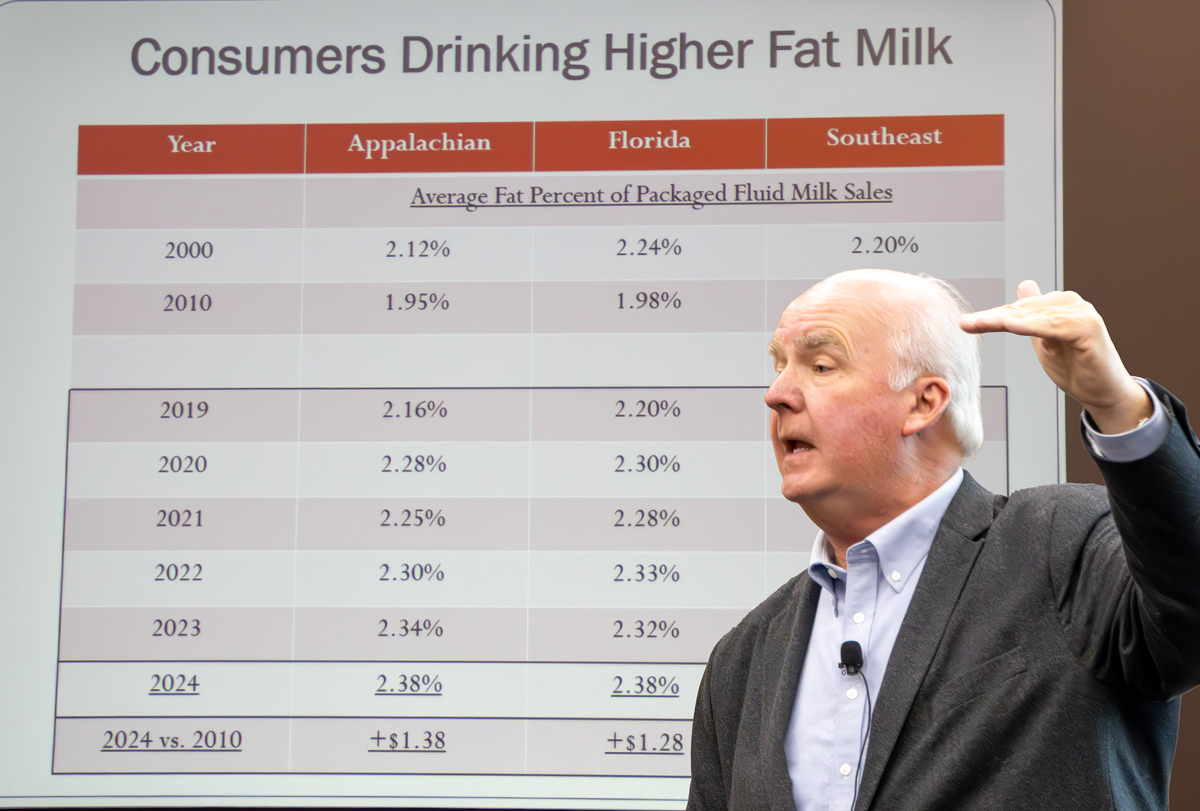

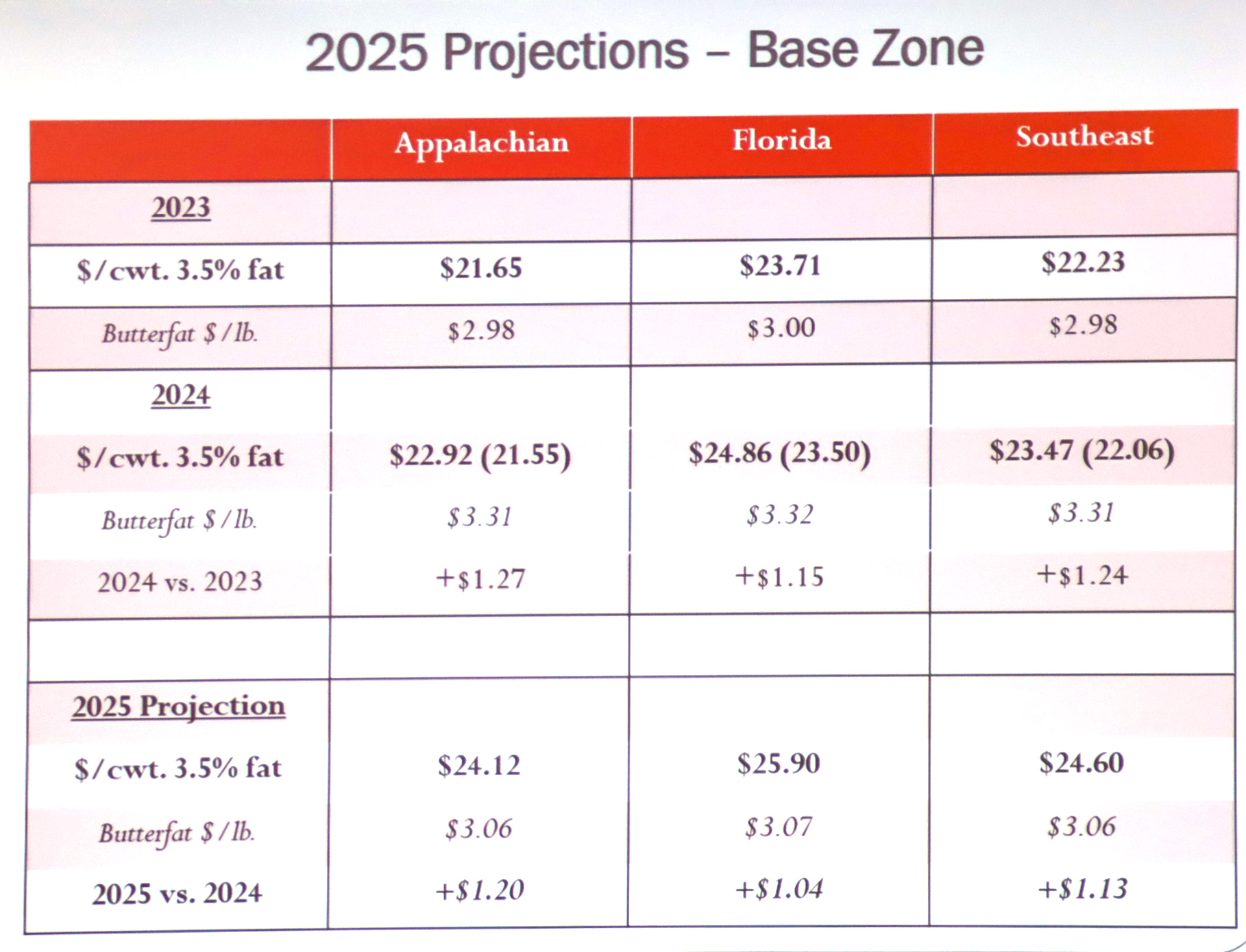

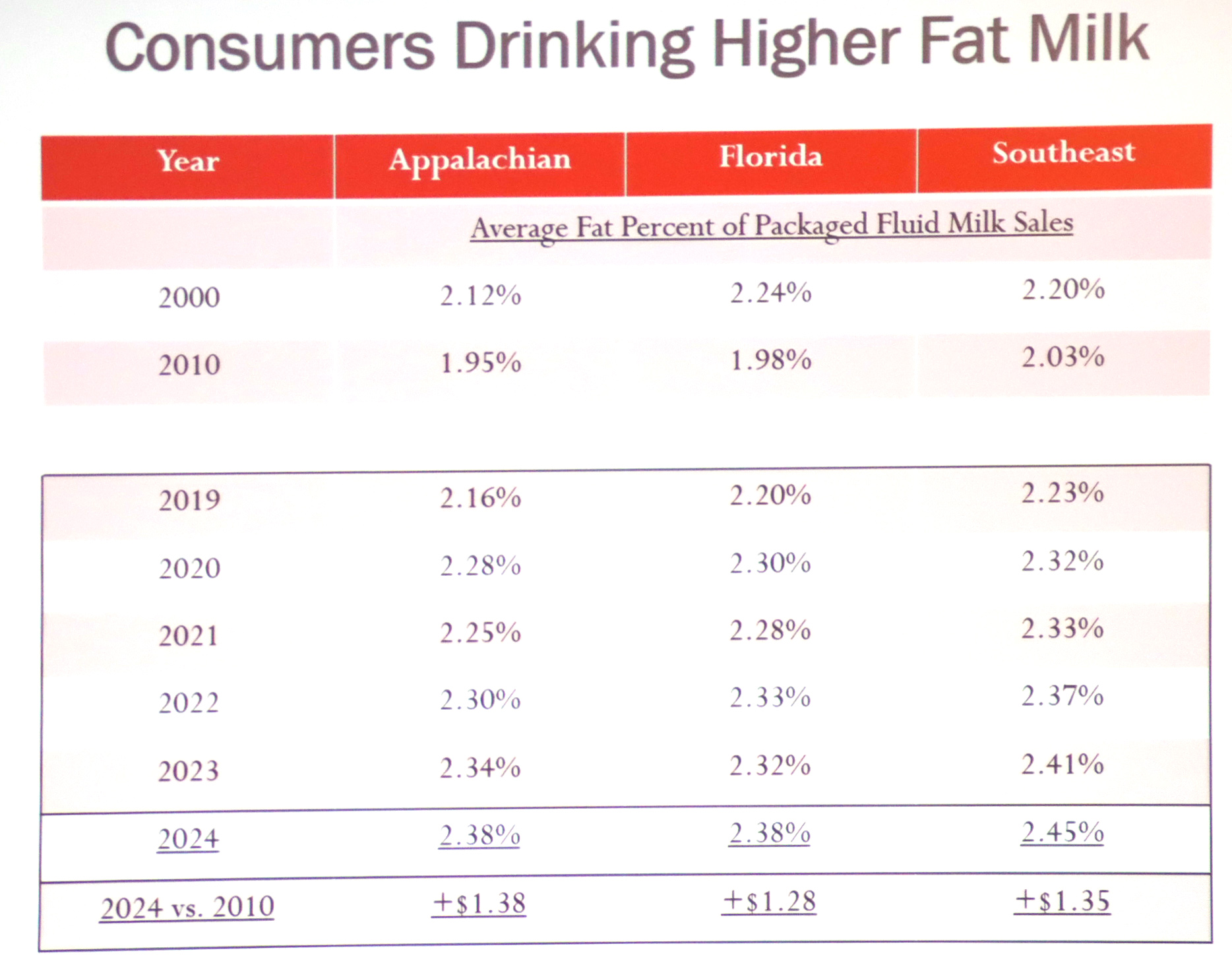

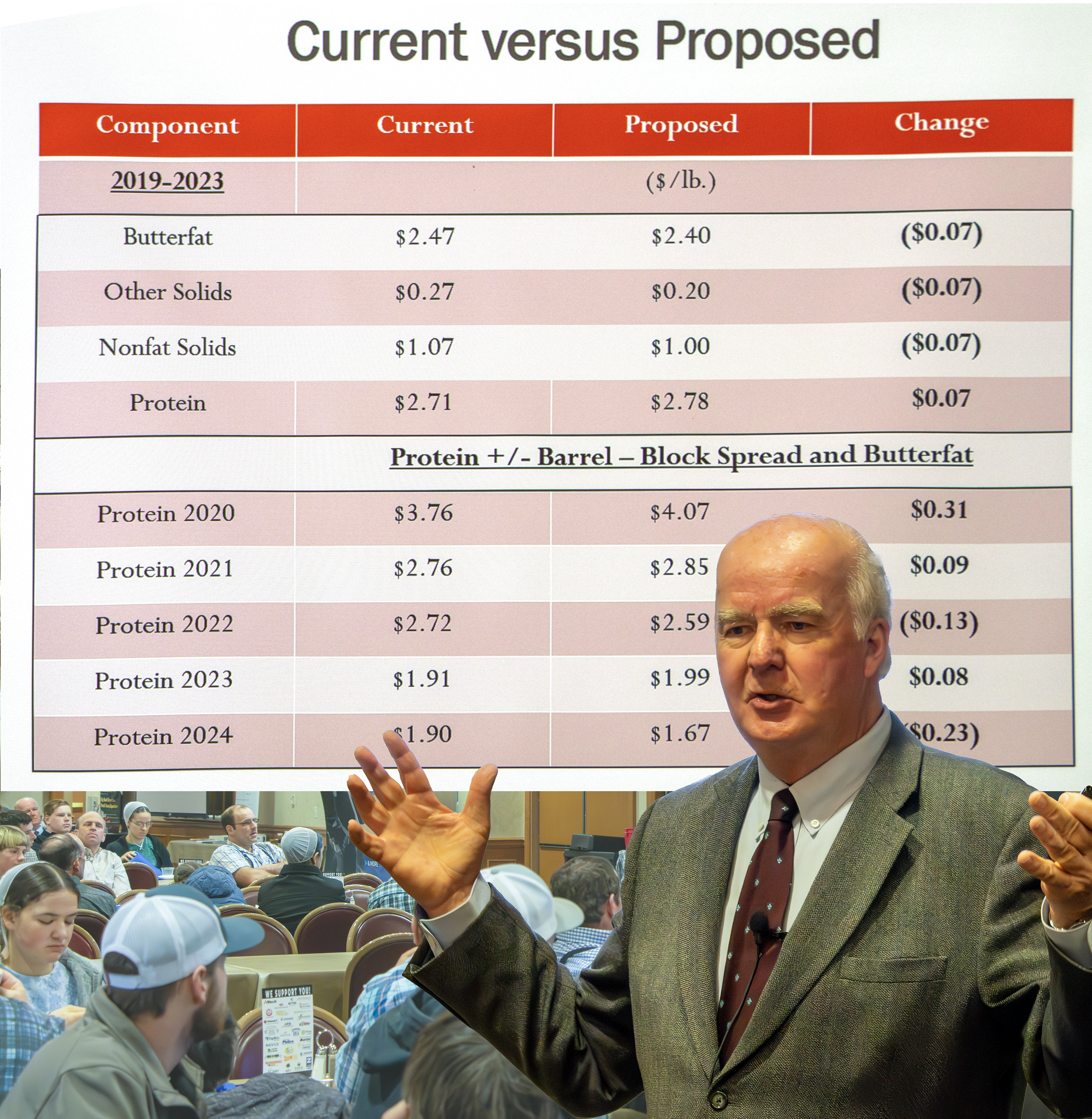

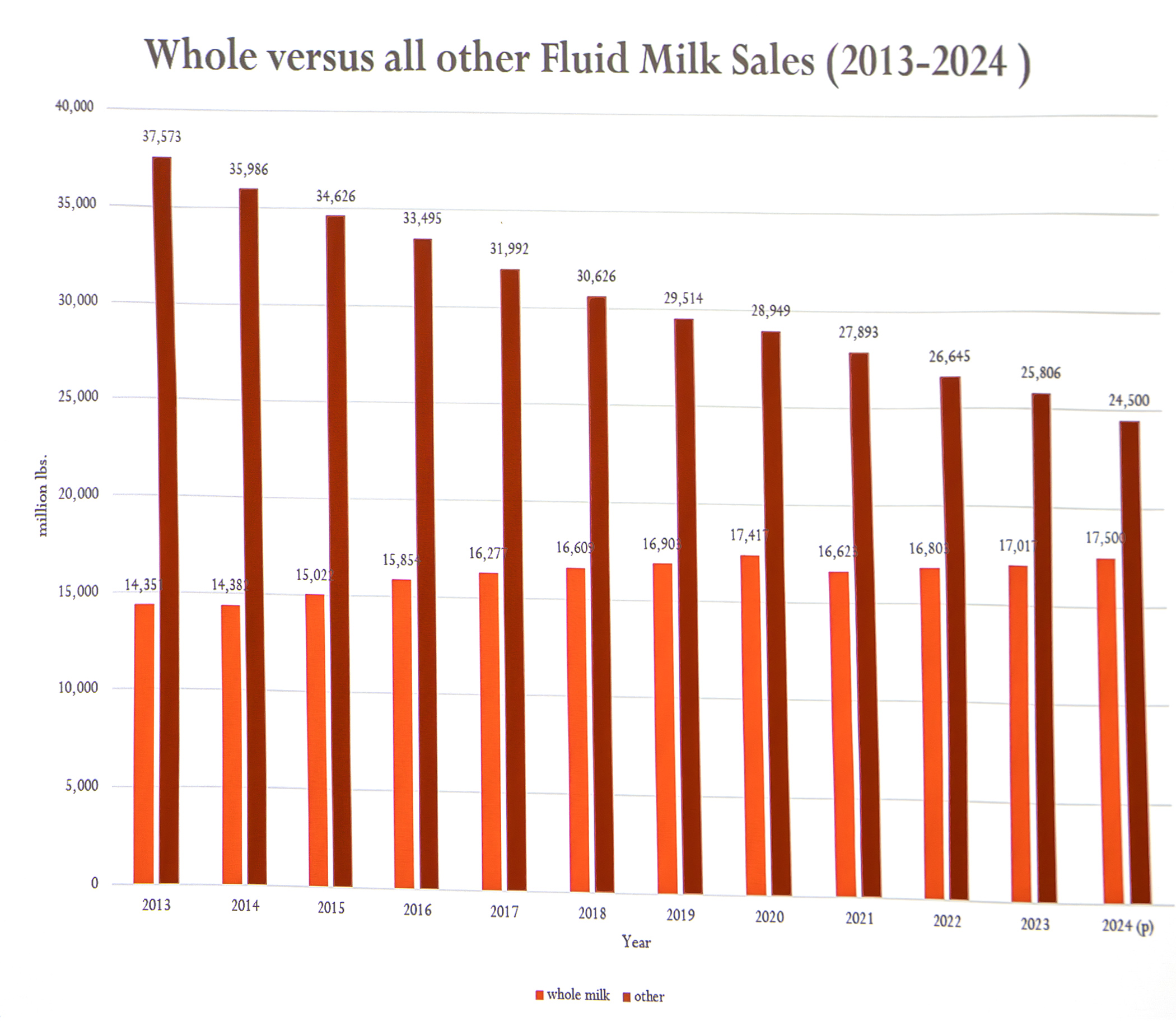

As longtime milk market guru Calvin Covington noted at the R&J Dairy Consulting seminar in eastern Lancaster County Jan. 28th, kudos go to the grassroots efforts. He showed the increase in whole milk sales nationally, while other fluid milk categories have declined. This has somewhat stabilized the steep losses the entire fluid milk category has suffered most steeply in the past 14 years.

“My hat’s off to all of you and what you have done here in Pennsylvania, throughout the state and country, in promoting whole milk. I just wish other dairy farmers would be grassroots like you are and get involved,” said Covington. “Your work has paid off. Look at this graph. In 2013, whole milk sales were a little over 14 billion pounds. Last year (2024 with 11 months of data) I’m estimating 17.5 billion pounds. Whole milk is coming up, and everything else is going down.”

Covington dug into the graph (above) further to show that in 2019, the amount of whole milk sold was 16.9 billion pounds. “But look what happened in 2020, it jumped up to 17.4 and then back down to 16.62 in 2021. That was the pandemic. People were home. Schools were closed,” he said.

“When they were home, they drank good-tasting milk, but unfortunately when the schools opened back up, they had to go back to the other stuff. But my hat’s off to what you’ve done here. We’re selling more whole milk, and one thing people forget is that 100 pounds of Class I milk sales with higher fat content — last year it averaged 2.4 in this market compared to what it was 15 years ago when it averaged less than 2% — the more fat sold in Class I milk, the more income for you as dairy farmers. Class I butterfat is worth more than butterfat in the other markets, so my hat’s off to what you’re doing.”

(Author’s Note: Yes, Covington is speaking of the good work, the hard work, of 97 Milk volunteers who formed the non-profit in 2019 after dairy farmer Nelson Troutman’s painted bales began appearing. This good work is sustained by a handful of volunteers and donations. Just think what could be accomplished with more involvement. One of those volunteers is Jackie Behr of R&J, who puts her marketing skills to work for 97 Milk. She reminded farmers that donations are needed to keep the milk education movement going. An Amish Wedding Feast fundraiser is scheduled for Feb. 8 at Solanco Fairgrounds, with sponsorships still available. The next 97 Milk meeting open to all dairy farmers is March 25 at Durlach-Mt. Airy Fire Hall near Ephrata, Pennsylvania. Check out 97milk.com to learn more about the milk education movement, and hit the donate tab to find out how you can help.)

-30-