Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

97 Milk is a 501(c)3 non-profit. Donations are tax deductible.

By Sherry Bunting, Farmshine, November 22, 2024

EPHRATA, Pa. – Farmshine readers are no-doubt aware of the work of the volunteers operating the 97 MILK education efforts. But awareness and thank you’s don’t pay the bills.

First of all, 97 MILK is a 501c3 non profit, meaning donations are tax deductible.

Secondly, 97 MILK is managed and operated by volunteers. Not a single person doing any of this great work is paid a dime or a nickel (not even a penny) for their time and only in some cases are personal expenses for projects reimbursed

97 MILK has made huge strides on literally a shoestring budget.

However, even the frugal cannot survive without donations because printers have to be paid for printing materials like the popular and eye-opening 6×6 cards.

Website hosts and programmers have to be paid to keep the platform up and running.

When whole milk isn’t donated for an event, it has to be purchased.

When dieticians or other experts are interviewed for a Q&A at the website or on social media platforms, they expect their expert time to be paid.

Boosting the best and most informative ad posts on facebook also comes at a cost.

The list goes on, and it doesn’t even cover the things 97 MILK wants to do that are expensive, like BILLBOARDS.

There’s a reason Nelson Troutman started this movement by painting a wrapped round bale, or BALEBOARD — because the billboards were too expensive, but wouldn’t it be nice to amplify the good work of 97 MILK with a few larger than life billboards?

These are tangible costs that surround the small but strong and dedicated army of 97 MILK volunteers.

When it comes to the content created, the daily social media posts, the educational printed materials, the interactions with followers to answer their questions on social media, the constant monitoring of social media conversations, along with the answering of emailed questions at the website question desk, the compiling of new information for the website designer to keep it refreshed, the staffing of booths at consumer-facing events, the painting of bales, the miles driven, time spent talking to consumers, time spent designing eye catching ads to show consumers, time spent actually communicating with consumers – that is all done by volunteers who take time away from their paid livelihoods to voluntarily promote whole milk education, often not even being reimbursed their personal costs for supplies.

We are in the season of Thanksgiving. A great way to show some gratitude to the hardworking 97 MILK volunteers is to help keep the boat afloat with a donation. Apart from a few regular givers, donations have not come into this volunteer effort for a long time, and the shoestring is baring thread, despite the important advances this educational effort has made for dairy farmers and the many agribusinesses that serve and depend on them.

A recent Dairy Foods Magazine website panel discussed the State of the Dairy Industry in 2024. One panelist observed that their monitoring data show a 30% increase in social media conversations about milk and dairy products. We can chalk some of that gain up to 97 MILK, posting six days a week and reaching hundreds of thousands of consumers every quarter, with many reacting and having conversations with 97 MILK volunteers — engaging directly.

The website, alone, is averaging 200 users per day, most of them new users. That’s a big number.

Total page views at 97milk.com were 11,000 over the past 30 days – another big number.

Facebook reached tens of thousands of people last week, without any paid ads, but reaches tens of thousands more with boosting. Of these numbers, the nationwide reach is broad. Nope, they don’t all come from Pennsylvania. The places with the highest views register as California and Texas, along with states all in between East to West and North to South.

Of the website interactions, the No. 1 draw is the Milk Facts section. Visitors to the website spend an average of 2 minutes and 40 seconds there. In today’s fast-paced digital world, that’s a long visit!

97 MILK is doing things right.

And guess what? Have you read the Oct. 16, 2024 Farmshine story about fluid milk trends? Do you read Market Moos keeping you up to date on the monthly estimated packaged fluid milk report by USDA?

Fluid milk sales are UP year-to-date over year ago, and have been trending this way since partway through last year. In fact, the long-term fluid milk sales downturn was slowed and flattened ever since 97 MILK was formed in February 2019. But in the past 18 months, it’s turning slightly higher. There is momentum now — enough that industry trade organizations and other farm publications are beginning to take notice.

This is spurred by the big increases in whole milk sales as one of the main categories turning the trend around when looking at the volume, not just the percentage of increase on a smaller volume category. Whole milk sales are up 21% since 2019 when 97 MILK was formed.

Consumers want to eat and drink more healthfully. They want to know about milk!

97 MILK has caught their attention, piqued their curiosity to learn more, and helped reveal the details about the nutrition in a glass of whole milk. Not to mention, the Whole Milk for Healthy Kids Act that passed the House of Representatives 330 to 99 last December got this far because of one thing: Whole Milk Education.

Whole milk bill champion, Representative G.T. Thompson, Chair of the House Ag Committee, said it best during a 97 MILK meeting attended by farmers in 2021, and he’s repeated similar statements at other meetings and panels where the subject of whole milk in schools comes up:

“Keep doing what you are doing with the well-designed combination of influencing, marketing and providing factual information. Keep up the education. It’s working,” said G.T.

I personally want to thank each and every person who has donated funds and / or donated their time to help keep this whole milk education movement going. Thank you 97 MILK for all you’ve done for America’s dairy farmers and consumers – and above all for America’s children!

So, what are you waiting for? Want 97 MILK to continue and do more? If so, go to https://www.97milk.com/donate/ and prove it, or mail your donation to 97 MILK, PO Box 87, Bird In Hand, PA 17505.

AUTHOR’S NOTE: Who’s the wizard behind the curtain on USDA’s last-minute milk pricing surprise, the splitting of the Class I baby to favor ESL? Vilsack, of course, with a little help from his checkoff cronies at Midwest Dairy and DMI — masquerading as ‘dairy farmers.’

By Sherry Bunting

USDA’s recommended decision on Federal Milk Marketing Order Class I (fluid milk) formulas brought a big surprise getting very little attention. That surprise: “splitting the Class I baby” and adding what constitutes a “fifth Class” of milk — TWO Class I movers announced each month.

ZERO proposals to divide Class I into a two-mover system were aired at the national hearing. Even USDA’s analysis shows the two movers would differ by as much as $1 apart — or more — in any given month.

The hearing record is woefully inadequate, indeed completely void of testimony for a second Class I mover. No proposal. No evidence. No testimony. No analysis. No parameters. No definition.

What does this surprise two-mover decision mean?

Fresh, conventionally processed (HTST) milk would go back to being priced by the prior method, using the higher of the Class III or IV advance pricing factors to determine the Class I skim milk base price portion of the mover.

On the other hand, milk used to make extended shelf life (ESL) fluid milk products, defined only as “good for 60 days or more,” would continue to be priced using the average of these two pricing factors, plus-or-minus a rolling adjuster of the difference between the higher-of and average-of for 24 months, with a 12-month lag.

Confused yet?

The industry is calling this surprise two-mover twist ‘innovative’ and ‘creative’, even ‘brilliant.’ But let’s hold the horses a moment.

With two movers, fluid milk costs could be different for plants in the same location based on shelf life. Could processors change the label to move between the movers and pay whichever mover was lower? Who knows? There is no clear definition for the new class, and the parameters to qualify are non-existent.

ESL processors will know the rolling adjuster 12 months in advance, due to the “lag.” They will know the two advance-priced movers a month in advance. They will have it charted in an algorithm no doubt, and make decisions accordingly.

Dairy farmers, on the other hand, will find out how their milk was used and priced two weeks after all their milk for the month was trucked off the farm. If the two-price Class I system becomes law, dairy producers’ milk checks will be even less transparent than they are now!

Not only does the USDA hearing record and decision fail to clearly define ESL, the industry doesn’t even have an exact and generally-accepted definition or standard for ESL.

ESL is both a loose and specific term.

Generally speaking, ESL is a term covering a broad range of products — ranging from UHT (ultra high temperature) or ultra pasteurization, aseptic packaging, to the inclusion of a process that combines microfiltration, skim separation, and indirect heating (in stages). These processes yield what is more specifically referred to as ESL fresh milk with a longer shelf life in refrigeration, but is not shelf-stable.

What’s at the root here?

Dairy checkoff personnel have openly identified ESL — especially shelf stable aseptically packaged milk — as its “new milk beverage platform.” Dairy farmers’ promotion funds are being used to research and promote ESL milk, as well as studying and showing how consumers can be “taught” to accept it.

For the past few years, the four research centers supported by the checkoff have been drilling into milk’s elements to sift, sort, and test different combinations to reinvent milk as new beverages.

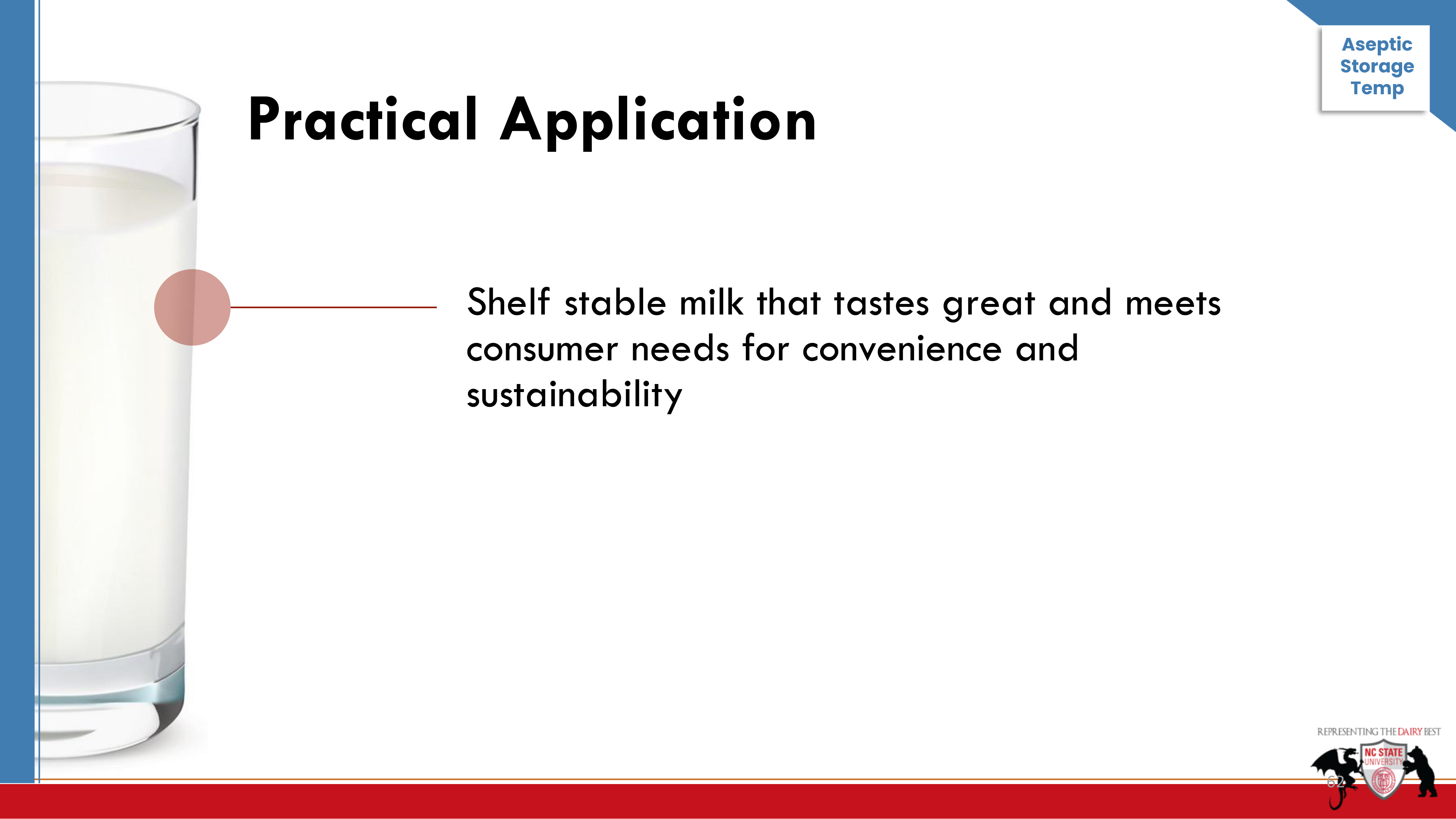

In 2023, North Carolina State researcher Dr. MaryAnne Drake —speaking at the 2023 Georgia Dairy Conference — talked about this “new milk beverage platform. We are after a shelf-stable milk that tastes great and meets our consumer’s sensory needs and our industry’s sustainability needs,” she said.

Bingo. Dairy checkoff funds for ESL are being driven by the net-zero sustainability targets. And now USDA’s federal milk order changes are proposing to lower dairy farmers’ Class I income and/or competitively favor, and in a way subsidize, ESL processors over fresh HTST fluid milk processors. Follow the money.

Dr. Michael Dykes of IDFA, at the Georgia Dairy Conference in January 2024, told dairy producers that “this is the direction we (processors) are moving… to get to some economies of scale and bring margin back to the business.” He said the planned new fluid milk processing capacity investments are largely ultra-filtered, aseptic, and ESL — 10 of the 11 new fluid plants on the IDFA map he displayed are ESL. Some will also make ultrafiltered milk and plant-based beverages too.

The linchpin to regional dairy systems and markets for milk from farms that fit USDA’s description of small businesses is the processing of fresh, conventionally pasteurized (HTST) fluid milk.

Meanwhile, dairy checkoff overseers, in cahoots with processors, are making big bets that consumers will embrace the obvious conversion underway to the consolidating shelf stable ESL milk, emboldened by the average-of pricing that has failed farmers miserably over the past five years and is now part of the proposed two-price Class I system mysteriously added to the USDA recommended decision when a two-price Class I system was never noticed as part of the hearing scope.

In the recommended decision, USDA notes that ESL currently represents 8 to 10% of total fluid milk sales but does not present the full picture of how the industry began aggressively converting to ESL since 2019 when Class I average-of was implemented. More of these accelerated investments will become operational in 2024-26.

Before we know it, the industry will have converted to ESL, and dairy farmers will once again experience disorderly marketing, depooling, and the basis risk of the mysterious average-of mover.

Dairy farmers have seen this movie before.

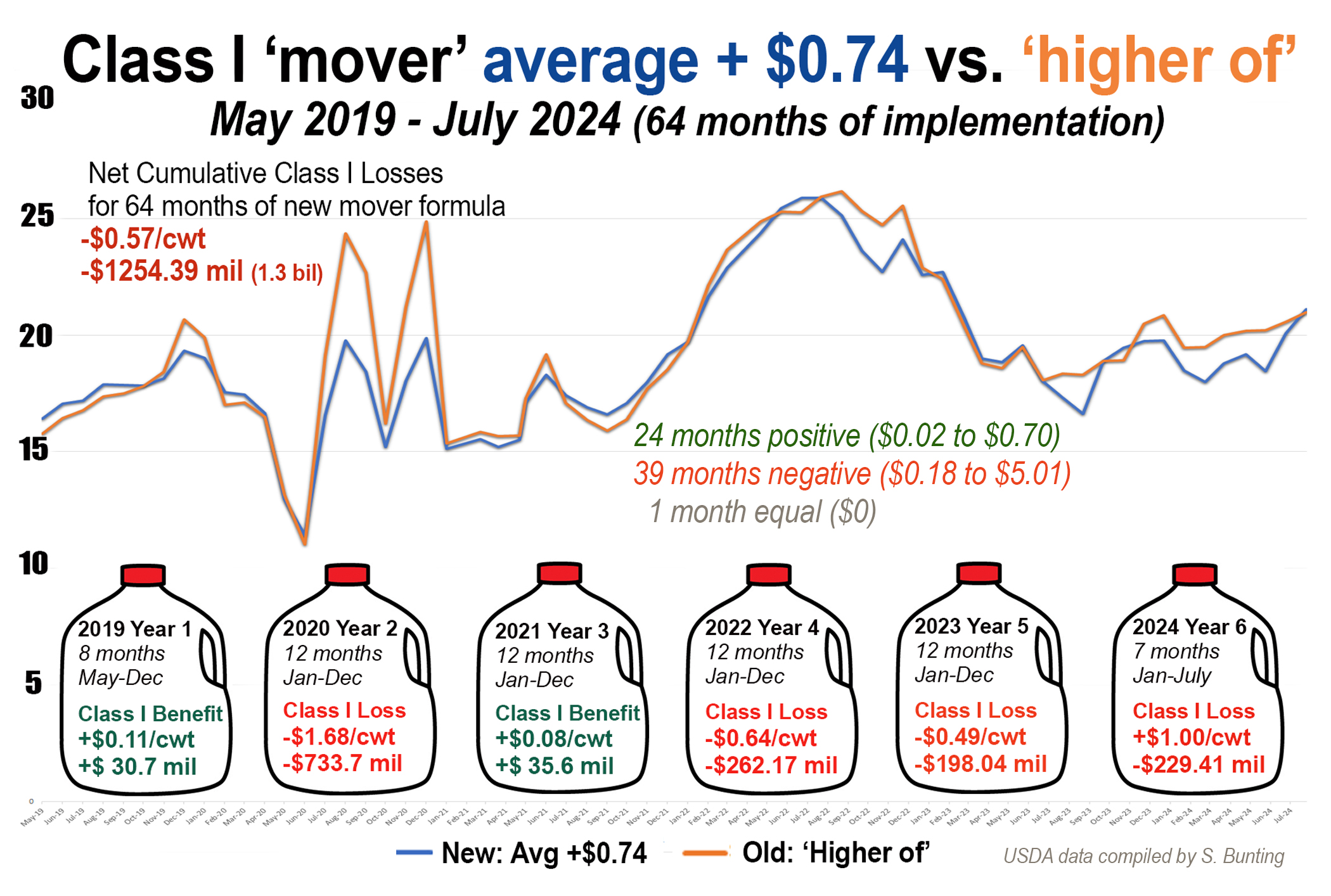

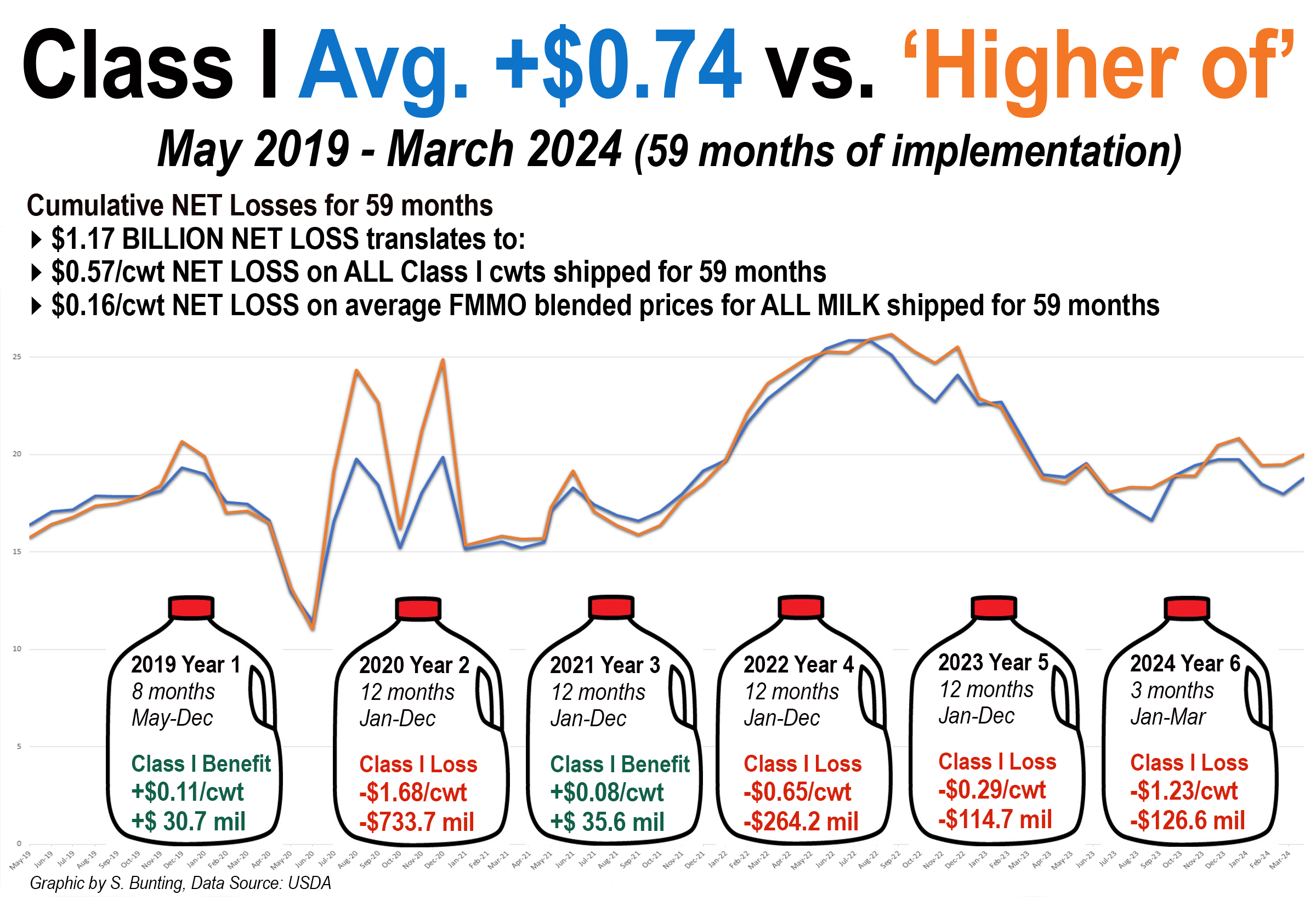

In 2018, the average-of method — which changed how the Class I base was calculated — was portrayed by National Milk and the IDFA as “revenue neutral.” But at the recent national milk order hearing, testimony revealed that farmers experienced Class I revenue losses totaling nearly $1.25 billion from May 2019 through July 2024… and other impacts.

Disorderly markets via the ‘average-of’ continue to result in losses and disrupt performance of risk management tools that fail to protect farmers against the intervals of extreme basis risk.

Proponents say the proposed rolling 36-to-13-month ESL adjuster on the second mover in USDA’s decision provides compensation to farmers for the difference between average-of and higher-of. However, that occurs gradually — over time — with a lagged interval. If tight milk supplies boost commodity prices and drive up all classes of milk, then dairy farmers’ incomes will at least partially lag years behind real-time markets!

ESL processors like Nestle and fairlife testified that the average-of method over the past five years allowed them to use Class III and IV hedges on the CME to offer flat 9- to-12-month pricing to wholesale customers and increase their sales. Nice to know the big corporations made money on that inequitable Class I pricing system.

Would a two-mover system ultimately reduce farmers’ access to milk markets in some regions and diminish the food security of those consumers? Watch the impact of a new, unregulated ESL plant now being built in Idaho!

Many legitimate questions lack answers

Milk is commonly prized as the freshest, least processed, most regionally local food at the supermarket. Will the USDA recommended decision accelerate consolidation and a reduction in fresh fluid milk availability for consumers?

Has USDA considered the purpose of the FMMO system is to promote orderly marketing and the adequate supply of fresh fluid milk? Will consumers accept the taste of the not-so-fresh ESL, or migrate faster to other beverages if fresh fluid milk is less available to them?

How will the two-mover system impact dairy farms located outside of the industry’s very specific identified growth centers?

Will this perpetuate the wide divergence between Classes III and IV that has been an issue since 2019, further punishing dairy farmers with disorderly marketing and opportunistic depooling?

Who knows? The hearing failed to define, examine, or obtain evidence on any such questions… or any other questions that the hearing process is meant to be open to because this decision falls outside of the hearing scope!

Vilsack strikes again?

This proposal — a price break favoring ESL milk — fits the climate and export goals set forth by Ag-Secretary-then-DMI-executive-then-Secretary-again, Tom Vilsack. The pathway to rapidly consolidate the dairy industry to meet those goals is to tilt the table against fresh fluid milk. This is something Vilsack already put a big dent in by removing whole milk from schools.

It’s like one well respected veterinarian in the industry observed recently in conversation: “Someone decided: Thou shalt drink low-fat milk and like it.”

That “someone” is apparently equally convinced that the industry shall move to ESL and aseptic milk processing… while using dairy farmers’ checkoff funds to figure out how to get consumers to like that too.

EAST EARL, Pa. – “Those who don’t learn from history are doomed to repeat it.” That was the theme of the American Dairy Coalition’s webinar on the USDA’s proposed Federal Milk Marketing Order (FMMO) pricing changes, which I participated in last Thursday, August 29th.

Over 125 people participated, including state dairy and state farm bureau organization leaders and individual producers. American Farm Bureau economist Danny Munch helped producers understand the proposed changes and walked through the areas of mutual concern. Other panelists offered information, and participants’ questions were addressed.

“This webinar was a grassroots dairy producer undertaking,” said moderator Kim Bremmer of Wisconsin-based Ag Inspirations. “ADC planned it to make sure dairy farmers have a way to ask questions before the public comment period closes on Sept. 13th. We know the last update to milk pricing occurred in that 2018 farm bill, and that was without your input, and it cost dairy producers over a billion dollars across the country. It is really important that your voices are heard.”

Four primary areas of concern were discussed: the processor make allowance increase, the size of the whey make allowance relative to the price, delayed timing of beneficial updates to milk composition, and the surprising 2-mover system for Class I, effectively adding a 5th class of milk to the FMMO pricing scheme.

A 2-mover system was not vetted during the very lengthy USDA hearing. It appears to be “thrown in” as a last-minute compromise to appease processors investing in extended shelf life (ESL) fluid milk capacity.

Nestle and Fairlife had testified to sales volume growth when they offered 9 to 12-month flat-pricing after the average-of was implemented in May 2019. They said they must have average-of pricing to manage their risk so they can offer long-term pricing to grow sales.

Make allowance increases quite large

USDA proposes to raise processor make allowance credits by 29 to 33% above the current level. That equates to a 75-cents to $1.00 per hundredweight new deduction from milk checks, embedded in the pricing formulas, depending on how the milk was utilized.

Munch said make allowances are part of the formulas that start with surveying market prices for the four base commodities – 40-lb cheddar cheese blocks, butter, nonfat dry milk, and dry whey. USDA works backwards from the surveyed price to derive a value for the raw milk.

He used a cartoon imagining of “little Zippy selling cheese at his cheese stand.” (a light-hearted reference to AFBF president Zippy Duvall, a former dairyman).

“USDA is surveying the volume and value that he is selling it at — out in the marketplace — and then is using that price to derive a raw milk price,” Munch said, explaining that, “working backward, there has to be a part of the formula that accounts for the cost for Little Zippy to convert the raw milk into the cheese. He uses non-dairy ingredients like cultures and salts. It’s his own labor as well as overhead and equipment that he uses to convert raw milk into cheese. In the FMMO system, that deduction that accounts for his costs is called the make allowance,” he continued.

But today, the Little Zippys of the dairy industry are not so little, and they report much less on the USDA price survey, and they make so much more of the products that are NOT price-surveyed. These other products — such as mozzarella cheese, pizza cheese, other non-cheddar cheeses or cheddar cheeses in other bulk package sizes, whey protein concentrate, skim milk powder, whole milk powder, unsalted butter, and on and on — are not part of the formula and do not contribute value to the farmer’s milk check. Class I and II products are not price-surveyed either.

“When we look at the surveys, so many things are made out of the wonderful perfect nutrition of milk made on our farms, so what is the percent of products that are actually represented in the surveys?” asked Indiana dairy producer Sam Schwoeppe, who moderated the webinar Q&A

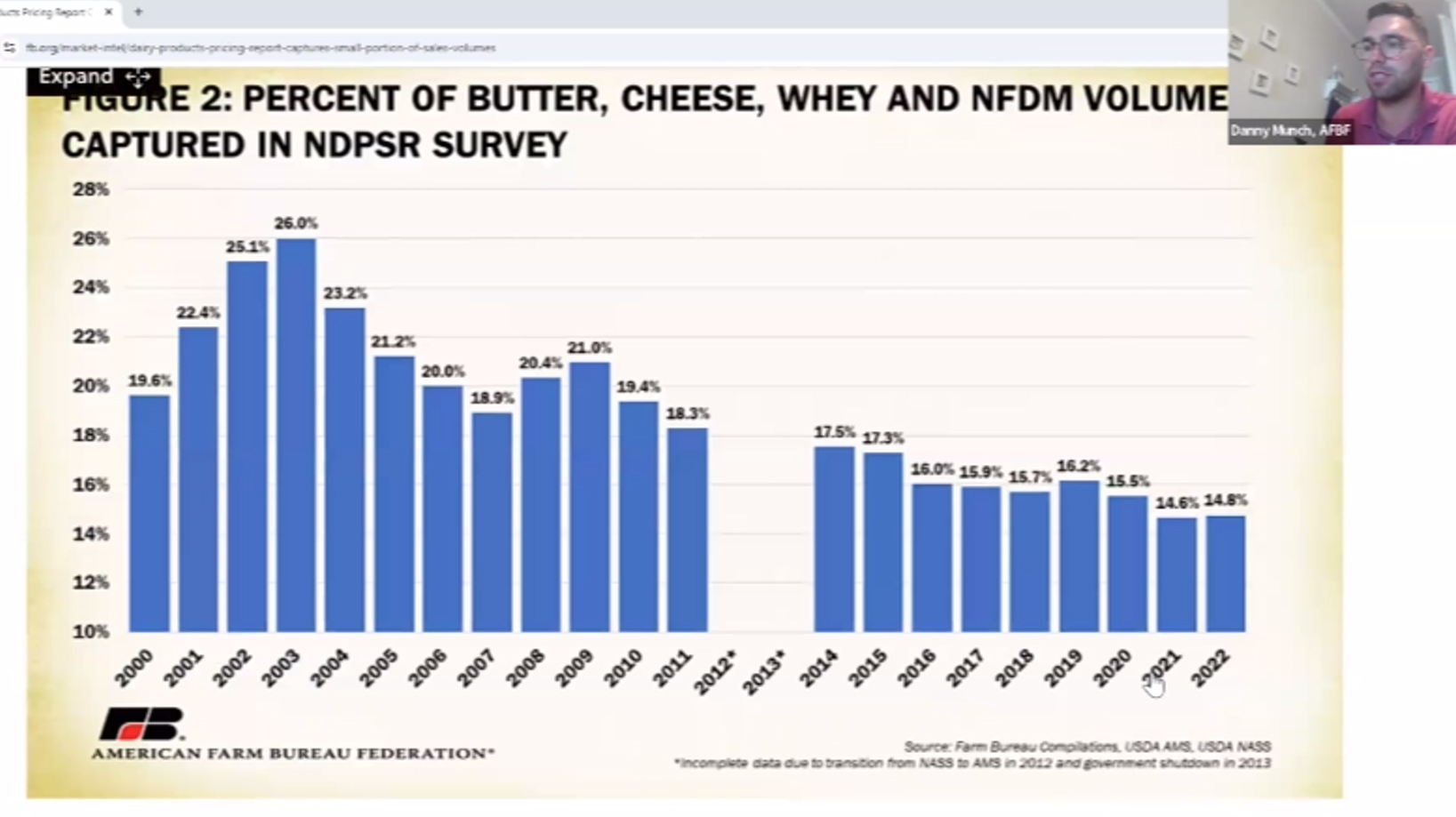

Survey volume quite small

Munch said the volume captured is “quite small and declining” to 14.8% in 2022 after being a high of 26.4% in 2002. “But those are just the products that are actually surveyed. There’s a lot of products that are not even surveyed, and that means the percent is even less.”

American Farm Bureau, American Dairy Coalition, and others pushed for some other bulk products to be added, but those proposals were rejected in this USDA decision.

So, how can current make allowance levels be too low when processors are spending billions to expand? Or, are dairy farmers expected to pay this debt service?

Dr. Michael Dykes, the CEO of the International Dairy Foods Association (IDFA), representing processors, told dairy farmers at the Georgia Dairy Conference in January 2024 that, “7 billion in new processing investments (below) will be coming online in the next two to three years. There’s a lot of cheese in those plans. These are going to be efficient plants. You’re going to see consolidation.”

The proposed make allowance increases of 5 to nearly 7 cents per pound across the four commodities equate to a new embedded milk check deduction of nearly $1.00 per hundredweight for Class III and around 75 cents for Class IV – over and above the current make allowances that already equate to $2.20 to $3.40 per hundredweight. Class I would see this embedded in advance skim and fat pricing factors that are used to set the base price mover.

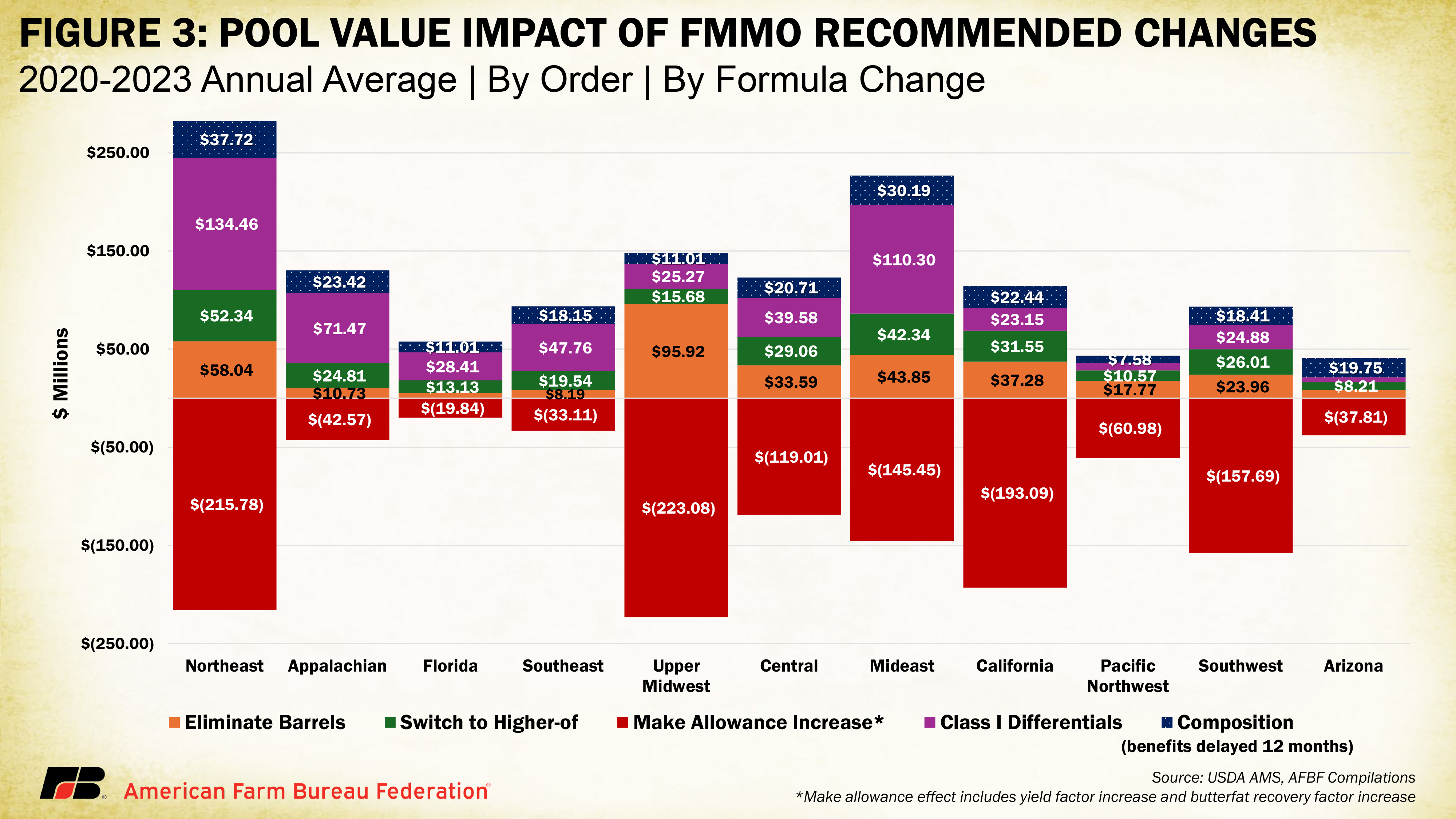

Collectively, the make allowance increases could remove $1.25 billion annually from FMMO pools, Munch showed in a 5-year static analysis based on prior pool composition, (See chart at top). Other aspects of USDA’s full proposal will defray some or all of the loss, mainly in the FMMOs with more Class I utilization. USDA’s proposal includes increases in location differentials for Class I fluid milk.

What happened in 2008-09?

Learn from the past or be doomed to repeat it? The last time make allowances were increased in 2008, a dairy market crash followed. As a webinar panelist and ag journalist, I pointed out that the dry whey price fell below the dry whey make allowance for the first seven months of that implementation from October 2008 through April 2009, resulting in penalties deducted from milk checks on every pound of other solids in the milk.

This time, the proposed dry whey make allowance is the largest of all – up 33.2% from $0.1991/lb now to $0.2653/lb. If in effect a year ago, dairy farmers would have again seen negative other solids penalties on their milk checks in July and August 2023 when milk prices were at their lowest. Meanwhile, processors made less dry whey, instead making more value-added products that are not price-surveyed.

Munch noted that only 66% of the plants on the price survey actually participated in the voluntary cost survey used by USDA to set the proposed new make allowances. AFBF, ADC and other organizations have been on record opposing make allowance increases until mandatory, audited surveys are conducted by USDA.

Conversion from fresh milk to ESL?

Learn from the past or be doomed to repeat it? On the Class I side, the 2018 farm bill changed the base price calculation. Farmers were told this would be revenue neutral, but the change cost them – at minimum — $1.25 billion over the past five years.

USDA now proposes to restore the higher-of calculation, but only for conventionally pasteurized HTST (or fresh) milk. Extended shelf life (or ESL) fluid milk products — labeled good for 60 days or more — would be priced using a new average-of method with a rolling adjuster.

Shouldn’t ESL have been defined in the hearing, and the economic impacts studied? This idea of two different Class I movers was not vetted in the hearing.

With two movers, fluid milk costs could be different from the same location based on shelf life. Webinar comments questioned USDA’s loose definition of ESL; Could processors change the label to move between the movers and pay whichever mover was lower?

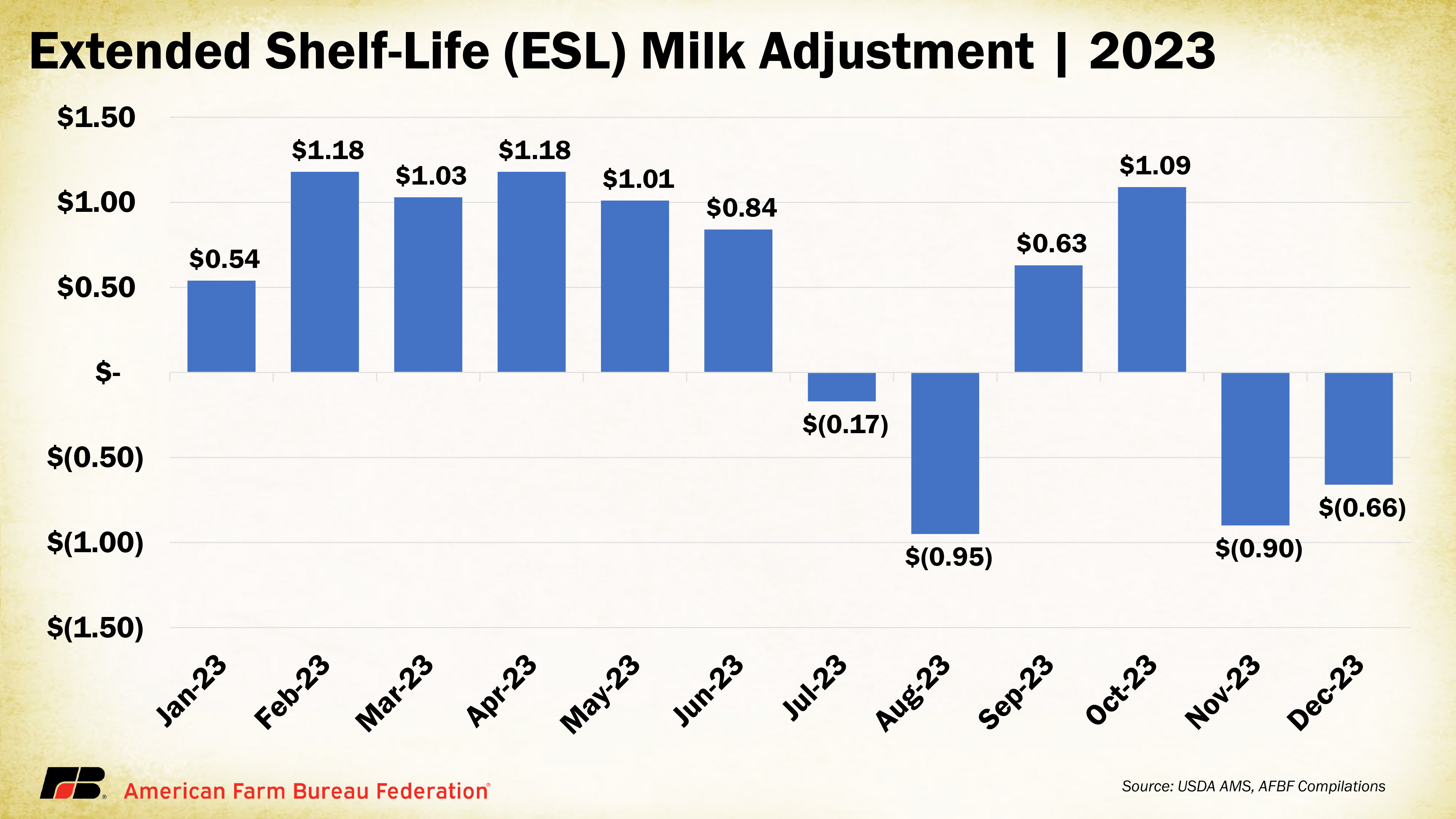

The USDA’s one-year static analysis showed the ESL Class I mover would have ranged from being $1.18 per hundredweight over to 95 cents under the HTST Class I mover in various months of 2023. That’s a big spread.

What’s at the root here? The dairy checkoff has openly identified ESL milk as the new milk beverage platform, using dairy farmer funds to research and promote it and to show consumers can be ‘taught’ to accept it.

Dr. Dykes of IDFA, at the Georgia meeting in January 2024, also told dairy producers that “this is the direction we (processors) are moving… to get to some economies of scale and bring margin back to the business.” He said the planned new fluid milk processing capacity investments are largely ultra-filtered, aseptic, and ESL. (10 of the 11 fluid milk plants on the IDFA map above are ESL and/or aseptic fluid milk plants. Some will also make ultrafiltered milk, and some will make plant-based beverages at the same location.)

Has USDA considered the purpose of the FMMO system is to promote orderly marketing and the adequate supply of FRESH FLUID MILK? Will consumers accept the taste of the not-so-fresh ESL and aseptic milk, or migrate faster to other beverages if fresh fluid milk is less available to them?

Would a 2-mover system ultimately reduce farmers’ access to milk markets in some regions and diminish the food security of those consumers? Prized as the freshest, least processed, most regionally local food at the supermarket, will the USDA decision reduce fresh fluid milk availability down the road?

How will the 2-mover system impact dairy farms located outside of the industry’s very specific identified growth centers? And will this perpetuate the wide divergence between Classes III and IV that has been an issue since 2019, further punishing dairy farmers with disorderly marketing and opportunistic depooling?

Webinar participants asked: “Will commenting even matter? Or is the USDA Secretary’s mind made up? How important is individual farmer input?”

“It’s extremely important for farmers to get involved. Even with talking points, really tell your own story with it,” said Munch. “They like hearing from you, and the stories of the impacts to your balance sheet, to your future revenue or the stability of your local community. They want to know the impact on small businesses. That’s one of the driving points.”

American Dairy Coalition has prepared an official comment, so other like-minded organizations and individuals can sign on before the filing deadline, which is 11:59 p.m. Friday evening, Sept. 13, 2024.

Click here to read the ADC’s comment that will be filed before the deadline Friday evening at Sept. 13 at 11:59 p.m. Dairy farmers and organizations wanting to associate themselves with the comment can click here.

This was my first thought, when former President Donald Trump announced Senator J.D. Vance of Ohio as his running mate in the Republican campaign. (Vance is an early cosponsor of S. 1957, the Senate’s whole milk bill.)

Like others, I’ve been involved in the effort to bring the choice of whole milk back to schools for more than a decade. It’s about natural, simple goodness — to simply strip away the federal ban and allow hungry, learning children to be nourished by milk they will love.

Looking back at the years of this long fight, I realize that if it’s so painstakingly hard to get something so simple and so right accomplished for America’s children and farmers, we’ve got problems in this country.

With President Joe Biden now withdrawing from the campaign for a second term, and Vice President Kamala Harris as presumptive nominee launching her campaign this week in the Dairyland State, I’m reminded of where she stands on such things.

Harris is no friend to livestock agriculture. She was an original cosponsor of the Senate version of “The Green New Deal.” She has strong positions on climate change that may lead to harsher rules on methane emissions and water consumption in the dairy industry, while perhaps promoting methane digesters, which are not an equitable nor necessary solution. Cows are NOT the problem!

As a presidential candidate in 2019, in a CNN town hall, she was specifically asked: “Would you support changing the Dietary Guidelines to reduce red meat specifically to reduce emissions?”

“Yes, I would,” Harris replied, with a burst of laughter.

It’s not funny.

Earlier, she had said she “enjoys a cheeseburger from time to time,” but the balance to be struck is “what government can and should do around creating incentives, and then banning certain behaviors… that we will eat in a healthy way, and that we will be educated about the effect of our eating habits on our environment. We have to do a much better job at that, and the government has to do a much better job at that.”

Read those words again: “creating incentives and then banning certain behaviors.” In plain English, that means dangling the carrot and then showing us the stick.

As President Biden’s approval ratings fell, there were indications she would bring her side of the aisle to the table to negotiate a compromise to get the farm bill done this year.

Now that Biden has withdrawn from the race, and the pundits, media, and party organizers are breathless with excitement over Harris as presumptive nominee, it appears that the farm bill negotiations between the Committee-passed House version, the Republican Senate version and the Democrat Senate version have fallen apart.

House Ag Chair G.T. Thompson (R-Pa.) has called upon his colleagues to get to the table and do the work because a perfect storm is brewing in Rural America as net farm income is forecast to fall by 27% this year on top of the 19% decline last year.

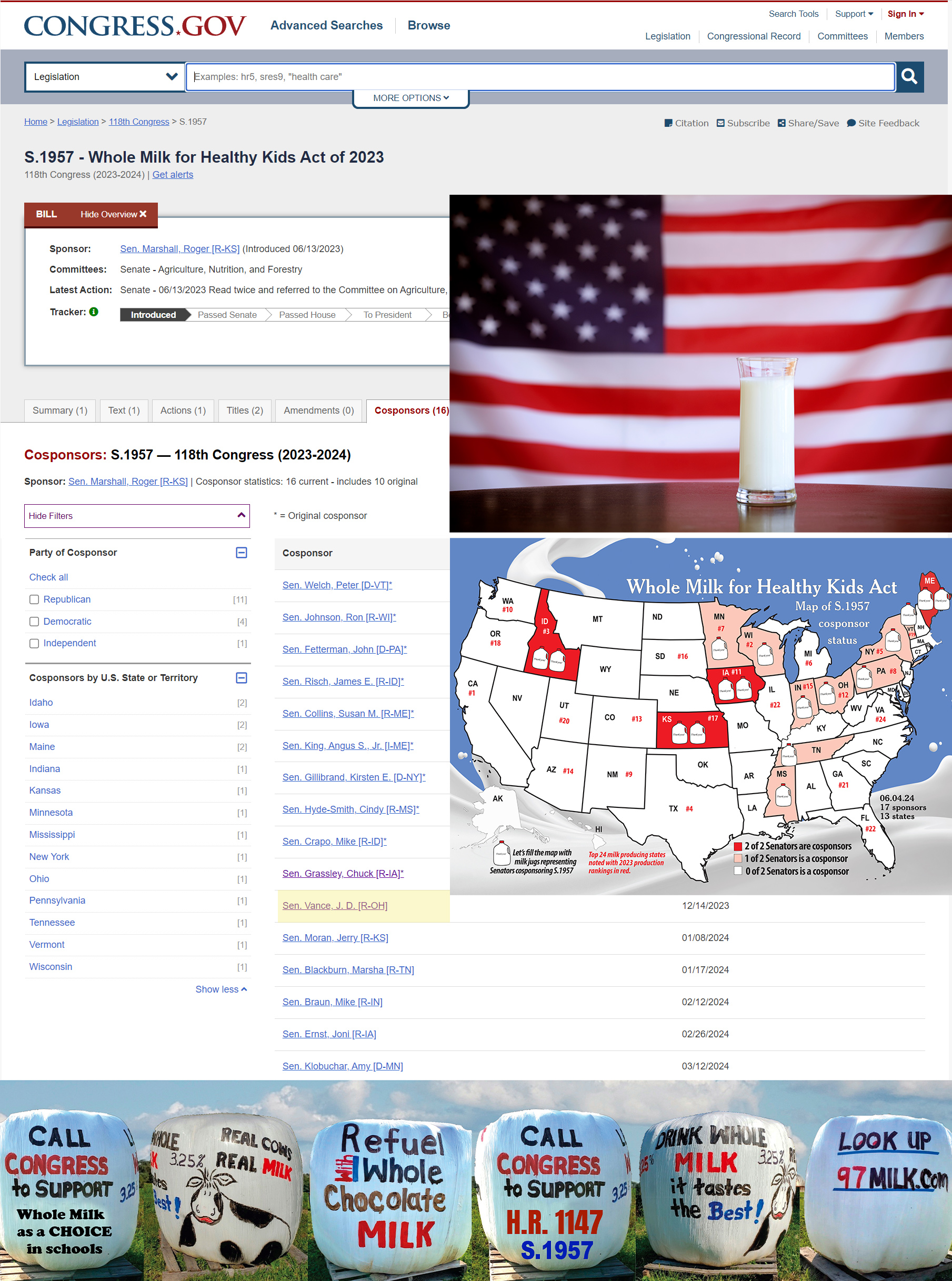

Meanwhile, there is political upheaval everywhere we look. Seeing Vance picked as Trump’s running mate and knowing he was among the early cosponsors of Senate Bill 1957 – The Whole Milk for Healthy Kids Act – offers some hope.

That bill — in true bipartisan spirit — was introduced in the U.S.Senate in June 2023 by Senator Dr. Roger Marshall (R-Kan.) with prime cosponsors Peter Welch (D-Vt.), Ron Johnson (R-Wis.), Kirsten Gillibrand (D-N.Y.), Chuck Grassley (R-Iowa), John Fetterman (D-Penna.), Mike Crapo and James Risch (R-Idaho), Susan Collins (R-Maine), Angus King (I-Maine), and Cindy Hyde-Smith (R-Miss.). The bill eventually earned cosponsorship from other Senators, including the influential Democrat from Minnesota, Amy Klobuchar.

Vance signed on as cosponsor on December 14, 2023, one day after the U.S. House of Representatives had passed their version of the bill by an overwhelming bipartisan majority of 330 to 99.

The Senate bill 1957 is identical to the successful House whole milk bill H.R. 1147, which was authored by Pennsylvania’s own Representative GT Thompson.

GT is a man of courage, conviction, compassion, of humility and humanity. I’ve heard him say more than once: “God gave us two ears and only one mouth for a reason.”

He is a determined man, doing the work. He included whole milk bill in the House Committee-passed farm bill. He’s standing firm on his pledge to put the farm back in the farm bill. He is concerned about the financial crisis in agriculture on the horizon, and held a hearing July 23 with witnesses from agriculture and banking giving stark warnings.

Even though whole milk choice in schools seems like a minor issue in the grand scheme of things today, it is really a linchpin. If we could just get something with broad bipartisan support accomplished, this could lead to other steps on common ground.

As the whole milk choice remains hung up in the Senate, let’s pause to think about how ridiculous it is that we adults get to choose, but our growing children do not. For them, whole milk is banned at two meals a day, five days a week, three-quarters of the year at school. (The federal government, via USDA school lunch rules, only allows fat-free and 1% milk to be offered with the meal or even a la carte.)

Maybe the Harris ticket would like to ban food choice behaviors for adults as well.

We have Republicans and Democrats supporting whole milk choice in schools. Both parties say they care about our nation’s farmers and ranchers who feed us and are the backbone of our national security.

As new milk beverage platform is developed, it sounds to me like people want the many attributes fresh whole unfooled-around-with fluid milk already delivers. It checks all the boxes! Maybe children just need to be allowed to have whole milk at school and daycare where they eat most of their meals, and maybe new generations of adults need the education about why and how the dairy protein and natural nutrition in real milk beat the imposters, hands down.

By Sherry Bunting, republished from March 2023 editions of Farmshine

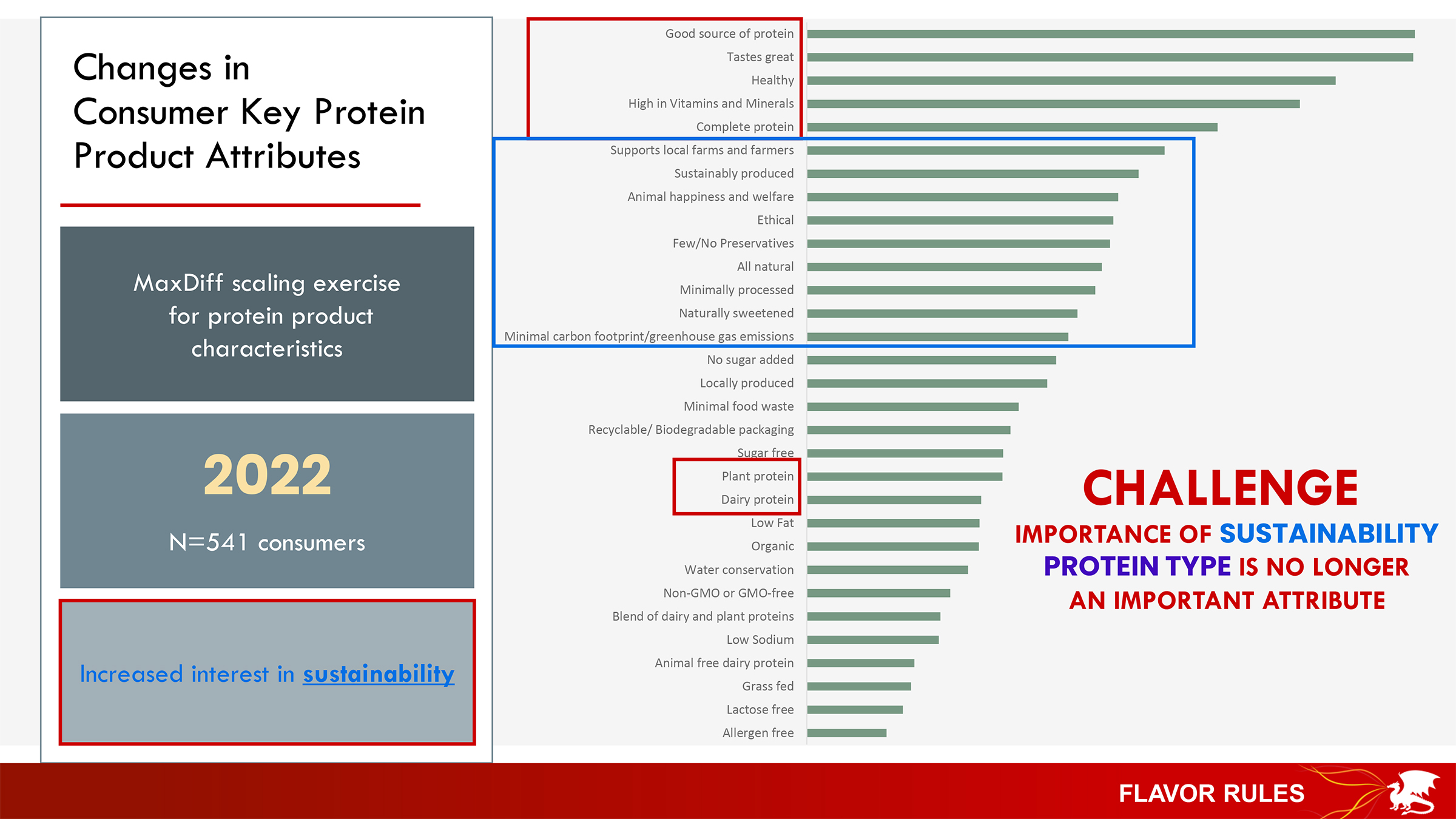

SAVANNAH, Ga. — Dairy checkoff-funded researchers say a new milk beverage platform is being developed to provide “the keys to the kingdom.”

Their consumer studies show people want clean labels, and at the same time they want more attributes. On the one hand, they want energy and protein. On yet anotherhand, they want indulgent creaminess.

Consumers also want flavor, but they want less sugar. They want sweeteners, but not artificial sweeteners. They want thickness without the thickeners. They do not want gums or gels, but they are okay with fibers and starches.

Some consumers want higher protein products. Others want everyday nutrition that is reasonably priced.

These are some of the highlights that were shared back in January 2023 during the Georgia Dairy Conference in Savannah. There, Dr. MaryAnne Drake, professor of food science at North Carolina State University and director of the Southeast Dairy Foods Research Center talked about the fluid milk innovation work funded through DMI.

The ‘new milk beverage platform’ leverages different processing applications for flavor and functionality around dairy protein, based on global protein trends in a rapidly growing nutritional drink market.

ESL shelf-stable milk: key to kingdom?

“We are after a shelf-stable milk that tastes great and meets our consumer’s sensory needs and our industry’s sustainability needs,” said Drake about the work of the four university research centers, including North Carolina State and Cornell, that are drilling into milk’s elements to sift, sort, and test different combinations, as part of the checkoff-funded Innovation Center for U.S. Dairy, under the DMI umbrella.

Through processes like membrane technology, ultrafiltration, and aseptic packaging, the physical, nutritional and sensory elements of milk are being isolated at a molecular level to create beverages that aim to deliver this broad list of what consumers say they are looking for.

At the same time, researchers are using interpretive surveys to understand how consumer desires actually translate into purchases, and then work with processors to build relationships with retailers to get these new beverage products into stores.

Reinventing milk

What does all of this mean? Reinventing milk by focusing on the domains in which real milk has a clear advantage for consumers among so many plant-based and now cell-based options.

For example, said Drake: “Consumers want to know from a credible source what the immune-boosting elements are in milk, not what we have added. They tell us they want to know the science. That’s new.”

Drake explained that the findings from their interpretive surveys represent a huge and divergent set of innovations to sort through and capitalize on as part of a new strategy.

“Consumers don’t see the perceived value of animal protein vs. plant protein, so we had them graph what they want and don’t want, what they know and don’t know,” she said, adding that consumers gave the slight edge to plant protein over dairy protein. They rated the top three protein categories as plant protein, whey protein, and milk protein — in that order. (A large percentage believed whey protein is plant protein.)

As their familiarity with the differences between plant and animal protein increased, their liking of dairy protein increased, the researchers learned.

In other words, consumers do not know the science about the nutritional differences between plant and animal protein, and if they knew the differences, they would rank milk protein as number one.

Clearly, this is a failure in consumer education and messaging. Isn’t that the domain of the dairy checkoff?

New strategy

Drake indicated that educating consumers about dairy protein as a ‘complete protein’ is one thing that can help. However, she said, the functionality around dairy protein is the innovation strategy that is being pursued by the industry.

“The number one label claim consumers are looking for in a protein beverage is ‘naturally sweetened.’ We own that, and this is where we can deliver,” Drake declared.

“We own protein functionality. We understand the process parameters that impact flavor and functionality, and we can leverage this over plant proteins on this platform,” she said.

Bottom line: The surveys and flavor panels showed that consumers want “desirable flavor, texture and appearance. They want a protein drink that is nutritious, naturally sweetened, and has a clean label with simple ingredients,” said Drake.

“They also want education, messaging and positioning, and they are looking at sustainability,” she added.

“We are working on what does clean label mean? It’s not what we think it is,” Drake reported. “It’s costing us sales if what they actually want is not on the shelf. We have the opportunity to deliver what consumers still want. We just have to find those things they want — that we have — and be more strategic in how we deliver them.”

Food technology and engineering was a big part of the picture painted for attendees that day.

Diversify processing

Producers were urged to challenge the status quo and to not just add processing, but to diversify it. They were also reminded that the 10 southeastern states had lost eight fluid milk plants in the previous roughly two-year period (2020-22).

During his annual market outlook that year, retired co-op executive Calvin Covington hit the nail on the head with this reminder, saying “that’s done some damage. The major challenge for milk markets in the Southeast is we need more of them,” he said. “A lot of the fluid milk products that are sold in the Southeast are not processed here. If we are going to have a viable dairy industry in the Southeast, we need growing and stable markets for milk produced in the Southeast.”

Covington also differentiated the trends for domestic and export demand, showing that both lagged their respective 5-year-average annual growth in 2022, with domestic demand growing by just 0.5%, while exports grew by 3.5%.

Keeping in mind as exports are expected to top 20% of U.S. milk production on a total solids basis in the next two years and fluid milk sales as a percentage of total milk production have fallen to just under 20%, seismic shifts are already occurring in the heavily fluid milk market of the Southeast.

Transformation brings investors

Geri Berdak, CEO of Dairy Alliance, the Southeast regional checkoff organization, talked about “creating a path forward” with objectives centered on driving milk volume, increasing dairy’s reputation and transforming dairy while building checkoff support.

She said transformation is necessary to “identify high-growth opportunities and stimulate outside investment, technology and innovation.”

The need for processing is big as plants are closing in response to declining fluid milk demand, leaving the the need for more diverse processing assets.

Exports drive innovation

“The biggest thing exports do is to drive value and innovation,” said Patti Smith, a food technology specialist and CEO of DairyAmerica, now wholly-owned by California Dairies Inc. (CDI) milk cooperative. Earlier in her career, Smith held a leadership position with Fonterra and has served at board and officer levels with IDFA and USDEC.

“Exports are a lot more than powder today. Our biggest item is still excess powder,” she said. “But we also export many other products — even UHT (ultra high temperature) and ESL (extended shelf life) fluid milk and cream.”

What Smith sees into the future are “opportunities for the right products and the right product configurations. We have the opportunities to capitalize on them and the technologies to grow them.”

Smith said the biggest benefit of exports to-date is to have a home for milk that grows the dairy industry without relying on core domestic demand for that growth, but that U.S. dairy processing infrastructure is not quite reflective of the new export era.

“We need to make our industry world renown, through a strategic plan that the whole industry will work on together, with digitized supply chains and infrastructure for growth that is reliable and can be consistently demonstrated, and that includes shipping,” said Smith, citing the Innovation Center for U.S. Dairy as the nexus, where the industry’s “strategic plan” for global trade is being built.

Developing ‘new milk beverage platform’

Emanating from the DMI-founded and checkoff-funded Innovation Center for U.S. Dairy is the marketing and promotion arm of new product alliances and the National Dairy Research arm through several universities looking to essentially create a milk beverage platform by drilling into milk’s elements, sifting, sorting and testing different combinations.

Dr. Drake said the new milk beverage platform holds the “keys to the kingdom” as global protein trends were valued at $38.5 million in 2020 and projected to grow. Meanwhile, the nutritional drink markets are growing steadily, with 42% of consumers eating healthy as a higher priority since Covid, and the number of conversations about protein (95% positive) steadily flowing across social media platforms.

Those keys, she said, are membrane technology, ultrafiltration, aseptic packaging and research exploring all of the physical, nutritional and sensory elements of milk at the molecular level to bottle up what consumers say they are looking for, while also gauging through interpretive surveys how this translates to purchases, and then working with processors to build relationships with retailers to get new products into stores.

Drake shared details about the roadmap to play to dairy’s strengths through nutrition, education, capitalizing on calming and immune benefits and using dairy protein functionality to limit added ingredients in beverages to satisfy the clean label trend.

She talked about how elements like fat, protein and lactose at different levels impact milk’s flavor and appearance: “We want to determine the impact of ultrafiltration levels for different concentrations of fat and protein for different sensory or physical experiences.”

She talked about ultrafiltration in conjunction with aseptic packaging for shelf-stable storage using an elaborate diagram of processes.

Bottomline, she said: “The chemistry of these (aseptic) milks is different.”

She described consumer flavor panels where shelf-stable and fresh fluid milk were served cold and compared. The flavor panels evaluated two different storage temperatures for the shelf-stable milk.

The North Carolina researchers worked with their Northeast Dairy Foods Research counterpart at Cornell and with Byrne Dairy, running grad students from North Carolina to Syracuse, New York when batches were available for study. (The Southeast and Northeast as well as Midwest and California Dairy Foods Research Centers all receive funding from checkoff and other sources.)

‘Training consumers’

“Consumer panels still liked the HTST (fresh fluid) milk best overall, but in 14-day and 6-month follow up, we found we can train them,” said Drake, reporting the two best storage temperature options for aseptic milk saw longer-term increase in acceptance.

HTST is the acronym for High Temperature Short Time pasteurization that is basically commodity fresh fluid milk vs. ‘value added’ UHT (ultra high temperature) and ESL (extended shelf life) as well as aseptically-packaged, which is milk processed for longer shelf life and then bottled in a special sterile process and package to last months without refrigeration, but will taste best served cold.

Schools are the gateway

“For 25 years, consumers have not liked aseptic milk,” said Drake, “but we are changing that. Consumers may not like it or want it, yet, but it is great for schools.”

She reported the practical applications to come up with “great tasting school lunch milk that contains no lactose (no natural sugar).” Another practical application is to “determine the impact of storage temperature of 1% aseptic milk on physical and sensory properties.”

This partially checkoff-funded research is also working on “changing the chocolate milk formula to have zero sugar,” she said. “When we think about school milk, the question is how to get the sugar out of it. We want a chocolate milk that tastes great and new government standards on low- or no-added-sugars. Right now, chocolate milk has 8.5 grams of added sugar and 12 grams of natural sugar (lactose).”

In addition to ultrafiltration removing natural sugar, or lactose, they are exploring “non-nutritive” sweeteners like monk fruit and stevia. Additionally, they are looking at “lactose-hydrolized” to boost the flavor profile at much lower levels of sugars or other sweetener.

Whether talking about consumers or children, parents, and schools, the milk beverage platform is tricky “They want to know from a credible source what the immune-boosting elements are in milk, not what we have added. They tell us they want to know the science. That’s new.

“We have a huge and divergent set of innovations to sort through,” said Drake.

By Sherry Bunting, Milk Market Moos column in Farmshine, July 5, 2024 (with updates)

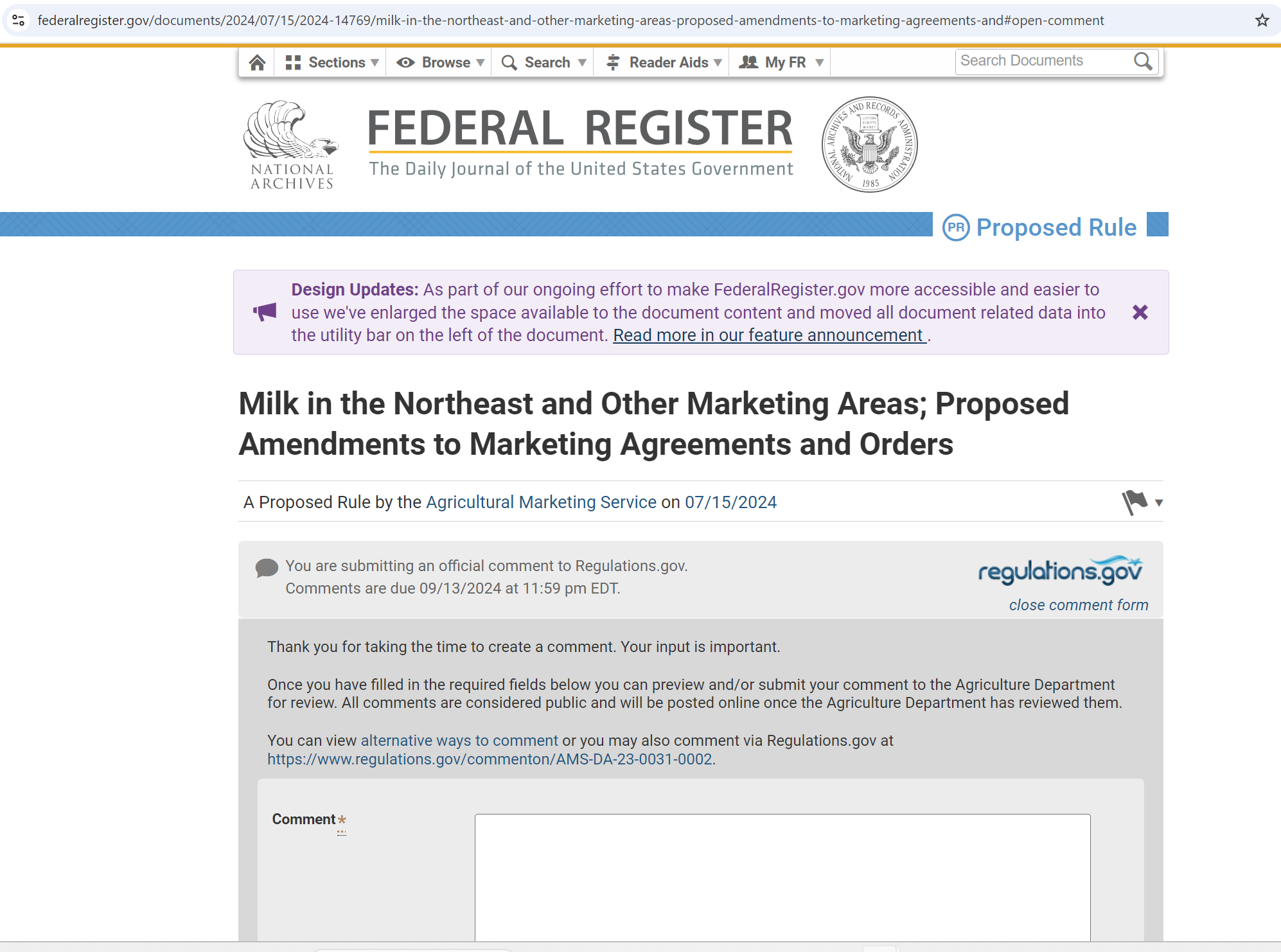

USDA issued a 332-page recommended decision on July 1 for changes to pricing formulas in all 11 Federal Milk Marketing Orders, which was later published in the Federal Register July 15.

The bottom line is a mixed bag of positives, negatives, and questions requiring further study.

USDA AMS professionals did yeoman’s work with the 49 hearing days across five months of proceedings on 21 proposals, yielding 500 exhibits; more than 12,000 pages of transcripts of testimony from farmers, cooperatives, processors and others, along with cross-examination; and over 30 post hearing briefs and correspondence.

Once the draft decision is officially published in the Federal Register in the coming weeks, the 60-day public comment period begins, followed by 60 days of USDA evaluation of the feedback, followed by a final rule, followed by a producer referendum.

According to the FAQ section at the USDA AMS national hearing website, only producers who are pooled in the selected representative month in each Federal Order will be eligible to vote. Each of the 11 Orders votes separately.

If two-thirds of those eligible dairy farmers OR two-thirds of the pooled volume they represent in an Order vote “yes,” then that Order continues, as amended. If neither two-thirds threshold is met, then that Order is terminated. *AMS answered our question on the two-thirds determination that it is determined by the number of eligible (pooled) producers who actually participate in the vote, stating: “If a producer receives a ballot but does not return it, the producer is not included in either the numerator or the denominator of the two-thirds calculation.”

1) Milk Composition Factors: USDA recommends updating the milk composition factors to 3.3% true protein, 6.0% other solids, and 9.3% nonfat solids. This would mainly affect Class I in all Orders and the other Class prices in the fat/skim priced Orders.

2) Surveyed Commodity Products: The recommendation here is to remove the 500-pound barrel cheese prices from the Dairy Product Mandatory Reporting Program survey and rely solely on the 40-pound block cheddar cheese price to determine the monthly average cheese price used in the Class III and protein formulas. National Milk Producers Federation (NMPF) proposed this and International Dairy Foods Association (IDFA) opposed it. American Farm Bureau Federation (AFBF) had proposed adding unsalted butter and 640-lb block cheddar to the survey, and California Dairy Campaign had proposed adding bulk mozzarella. Neither of these proposals were included in USDA’s recommended decision.

AFBF chief economist Roger Cryan discussed this recently on Farm Bureau Newsline, where he also talked about USDA decision not to include AFBF’s proposal to raise the Class II differential.

3) Class III and Class IV Formula Factors: USDA chose to recommend make allowance increases that fall in between the lower increase proposed by NMPF and the higher increase proposed by IDFA and Wisconsin Cheesemakers. The USDA recommendation is to raise these manufacturing allowances from current levels to these new levels: Cheese: $0.2504; Butter: $0.2257; NFDM: $0.2268; and Dry Whey: $0.2653. The recommended decision also proposes updating the butterfat recovery factor to 91%.

By our calculations, the proposed make allowance increase would equate to roughly an additional 80 cents per hundredweight deduction from milk checks embedded in the pricing formulas. Current make allowances total up to about $2.75 to $3.60 per hundredweight, depending on product mix. New make allowances would total up to about $3.25 to $4.50 per hundredweight, depending on product mix.

AFBF economist Danny Munch was interviewed by Brownfield Ag on July 2, noting the increase is 5 to 7 cents per pound. “When we loop that into a per-hundredweight value, that means farmers will be seeing 75 cents to 87 cents less per hundredweight on their milk checks because of the increased make allowance.” He says the data used for the make allowances was based on voluntary cost of production surveys.

Farm Bureau president Zippy Duvall did not mince words: “We strongly believe make allowances should not be changed without a mandatory, audited survey of processors’ costs. Our dairy farmers deserve fairness in their milk checks and transparency in the formula, but the milk marketing order system can’t deliver that unless make allowances are based on accurate and unbiased data,” he said in an AFBF news release.

American Dairy Coalition CEO Laurie Fischer also weighed in: “We are disappointed that USDA has proposed higher make allowance credits for processors, which are — in effect — deductions from farmer milk checks that are embedded within the pricing formulas. The industry does not yet have mandatory, audited cost surveys, and there is no connection between increased processor credits and a transparent, adequate price paid to farmers,” she said in an ADC news release, adding that these two elements have been key policy priorities for ADC since January of 2022.

4) Class I differentials: USDA recommends updating Class I differential values to reflect the increased cost of servicing the Class I market. The base differential for all counties stays at $1.60, and the county-specific Class I differentials are specified in the decision at levels higher than they are currently, but by less than the increases that had been proposed by NMPF.

5) Base Class I Skim Milk Price: USDA recommends going back to the higher-of the advanced Class III or Class IV skim milk prices to set the Class I mover each month. However, the Department did not go with Farm Bureau’s request to do this on an emergency expedited basis.

And, here’s where it gets tricky, the higher-of method would only apply to fresh fluid milk, while adopting a rolling monthly adjuster that incorporates the average-of for milk that is used to make extended shelf life (ESL) fluid products, including shelf-stable milk.

This means ESL milk would be priced differently from conventional fresh fluid milk within the same Class I category. A simple averaging method would be used as part of this special ESL adjuster, which would incorporate a 24-month rolling average (with a 12-month lag) of the difference between the higher-of minus the average-of, which is added to the current month simple average-of, and then the current month higher-of is subtracted from that sum. This adjuster could be either a positive or negative number.

In fact, we’ve learned that this ESL adjuster, using months 13 through 36 counting backward from the implementation date, would allow milk for ESL products to recoup, over time, some of the very large prior losses experienced by all dairy farmers during the average-of method that has been in place since May 2019. Because a simple average is used for the adjuster calculation, without the 74 cents, more would be recouped than the actual loss difference experienced under the years of the average plus 74 cents method. On the other hand, the rolling adjuster look back will include months in which a smaller make allowance was in effect than could be the case in the future if USDA’s make allowance recommendation becomes final.

Meanwhile, producers of milk bottled as ‘regular’ fresh fluid milk would start right out of the implementation gate at the higher-of and recoup zero prior loss endured under the current form of average-of, and be subjected to the higher make allowance, which is built into the advance pricing factors. (More on this feature of the USDA recommended decision in a future article.)

In its ‘notice to trade,’ USDA states that the ESL adjuster was developed to “provide for better price equity for ESL products whose marketing characteristics are distinct from other Class I products.”

Meanwhile, in his July 3rd CEO’s Corner, NMPF’s Gregg Doud appears to embrace what is essentially a fifth milk class given the different pricing methods proposed in the recommended decision for Class I — depending on shelf-life classification.

Doud writes: “Recognizing the need to restore orderly milk marketing, USDA decided to go back to the higher-of, with an accommodation for extended shelf-life milk, thus granting NMPF’s request for the vast majority of U.S. fluid milk. USDA’s solution is, frankly, as innovative as it is fair – a classic case of two sides not getting all that everyone wanted, but everyone getting what they most needed.”

Splitting the baby was not part of any hearing proposal that we could find; apparently processors made their case with USDA as to needing the average-of method (with calculated adjuster) to sell ESL milk products deemed the new milk beverage platform.

During the national hearing in Carmel, Indiana, representatives from Nestle, a major maker of ESL fluid milk products, said their sales increased once the average-of method was implemented in May 2019 through legislative language in the 2018 farm bill. They testified that they could manage risk when providing 9 to 12 month future pricing on shelf-stable fluid products to foodservice and convenience stores. They lamented that losing the average-of would hurt their sales.

Representatives for fairlife testified that forward pricing of their ESL products was critical to their ability to grow sales and that losing the average-of would impact future plans, including the size of the new plant being planned for New York State and other expansions elsewhere in the future.

However, since this bifurcation of Class I was not a proposal subject to vetting, no one had the opportunity to present evidence on future impacts.

Public comments on the recommended proposals will be accepted for 60 calendar days after the decision is published in the Federal Register. Comments should be submitted at the Federal eRulemaking portal: http://www.regulations.gov or the Office of the Hearing Clerk, U.S. Department of Agriculture, 1400 Independence Ave., SW, Stop 9203, Room 1031, Washington, DC 20250-9203; Fax: (844) 325-6940.

OTHER MOOS — July 3, 2024

Milk futures swap trends: Cl. IV up, III down

Class III milk futures moved lower this week especially on August and Sept. 2024 contracts; while Class IV milk futures were higher on 2024 contracts, steady to firm for 2025. On Tues., July 2, Class III milk futures for the next 12 months averaged $19.28, down 24 cents from the previous Wednesday. The 12-month lass IV milk futures average was $21.19, up 14 cents. This put the spread between Class IV over III at nearly $2.00 per cwt.

Block cheese, whey higher

Pre-holiday trade was firm to higher with little volume moved on most products. But nonfat dry milk lost ground, and the 500-lb barrel cheese trade was active at lower prices. The 40-lb block Cheddar price was pegged at $1.90/lb on Tues., July 2, up 2 cents from the previous Wednesday, with just 2 loads trading the first 2 days. The 500-lb barrel cheese market lost 2 cents, pegged at $1.88/lb Tuesday with 12 loads trading the first two days. (Update gained it back July 3 at $1.9025/lb with 2 loads trading). Dry whey gained a half-penny on the week at 49 cents/lb; one load traded.

Butter higher, powder weak

The butter market saw no trades the first two days this week. By Tues., July 2, the daily CME spot price was pegged nearly a nickel higher at $3.1375/lb. Grade A nonfat dry milk lost a penny and a half at $1.17/lb Tuesday with 4 loads changing hands. (Update, NFDM up July 3 at $1.18/lb, 2 loads traded)

May All-Milk $22.00, DMC margin $10.52

USDA announced the All-Milk price for May at $22.00, up $1.50 from April and $2.90 higher than a year ago. The national average fat test was 4.17, up 0.02 from the previous month and up 0.11 from a year ago. The Pennsylvania All-Milk price for May, at $22.50, was just 70 cents higher than for April, and fat test fell by 0.10 from April to May.

USDA announced the May Dairy Margin Coverage (DMC) margin at $10.52/cwt, up 92 cents from April and up a whopping $5.69 per cwt from the May margin a year ago. This is the third consecutive month in which no DMC margin payments were triggered as the margin remains above the highest coverage level of $9.50/cwt. The $1.50/cwt gain in the national average All-Milk price in May outpaced the 58 cents/cwt increase in feed cost.

H5N1 detections fall to 57 in just 7 states

As of July 2, 2024, the confirmed cases of H5N1 in dairy cows decreased to 57 herds in now just 7 states as South Dakota moved past the 30-day window and off the active map. Colorado has the most detections at 23 in the past 30 days, 27 cumulatively since April 25. This has created some questions as it represents 20 to 25% of the 110 herds in the 13th largest milk-producing state. Colorado is followed by Iowa (12), Idaho (9), Minnesota (6), Texas (5), while Michigan’s previously high numbers over 25 have dropped to one, and Wyoming still has just one. Michigan and Wyoming will be past their 30 days on July 7 and 12, respectively, if no new detections are confirmed.

EAST EARL, Pa. — Year-to-date Whole Milk sales for the first two months of 2024 are up a whopping 5% year-over-year (YOY) at 2.57 million pounds. Even when adjusted for Leap Year, the average daily increase is a substantial 3% surge, compared with the past several years of steady 1% increases YOY.

Flavored whole milk sales, year-to-date (YTD) are up a whopping18.6% YOY. Adjusted for Leap Year, the increase is a substantial 14%.

As the number one volume category representing more than one-third of the fluid milk category since 2020, the recent surge in whole milk sales has been enough to reverse the decline in total packaged fluid milk sales in four of the past five months.

USDA tallied 2023’s total packaged fluid milk sales down by a smaller margin of 1.5% for the year compared with previous years of decline; however, October and November sales were up 1% and 0.3% YOY for the first time since the months of the Covid shutdown when families ate at home. December’s total packaged fluid milk sales trailed year-earlier, but January and February 2024 have come back strong.

USDA estimates total fluid milk sales were up 2.4% and 2.5% YOY for January and February, respectively. When adjusted for Leap Year, the February increase is a respectable 0.8%. Similarly, when we adjust the YTD total of 7.325 million pounds in total fluid milk sales to reflect the extra consumption day in February, this is also 0.8% higher on an average daily basis vs. year ago.

This is good news! Let’s keep this upward trend MOOVING in fluid milk sales, led by surging whole milk sales — thanks to volunteers spreading the good word.

Now, if we could just get the United States Senate off the sidelines and into cosponsoring S. 1957 Whole Milk for Healthy Kids, we could really gain some ground — and America’s kids would be free to choose milk they love at school where they receive 2 meals a day, 5 days a week, 3/4 of the year.

Thanks to the U.S. House of Representatives and the leadership of Congressman G.T. Thompson of Pennsylvania, the Whole Milk for Healthy Kids Act (H.R. 1147) passed the House on December 13, 2023 by an overwhelming bipartisan majority 330 to 99. If the U.S. Senate doesn’t have the opportunity to vote it through by December 31, 2024, we must start all over again in the next legislative session 2025-26!

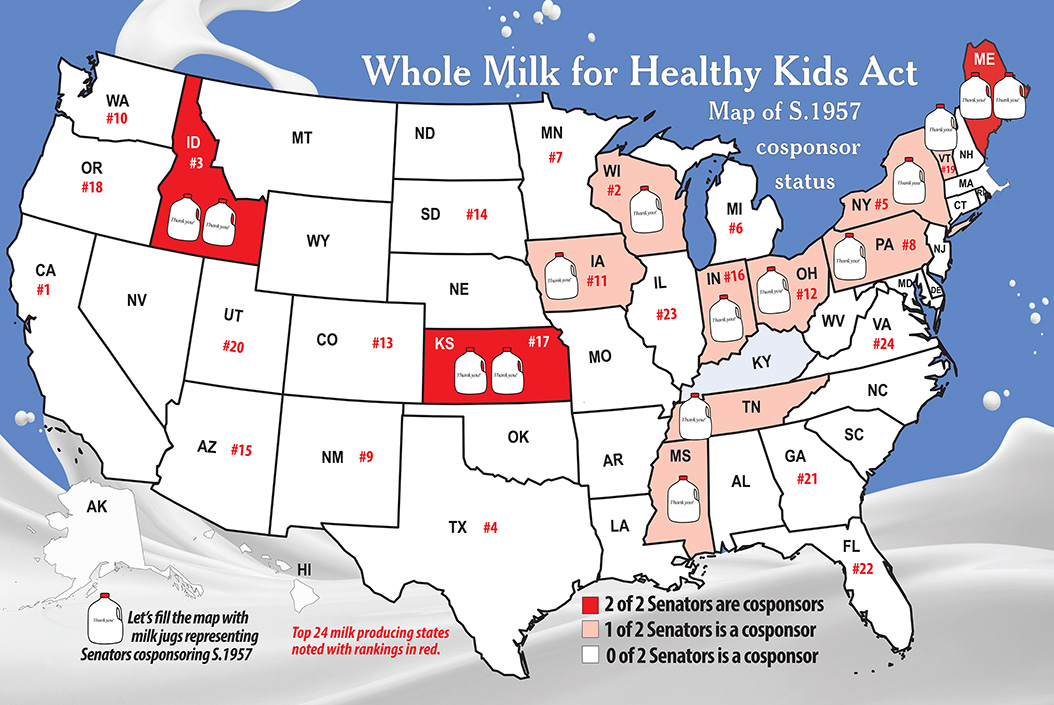

Check out the map above to see how S. 1957 remains stalled for the past 60 days at just 17 sponsors from 13 states.

Where do your state’s U.S. Senators stand? Ask them! And think about their answers when going to the polls this fall. Elections have consequences.

Also consider asking your state senators and representatives to follow Tennessee’s lead and get a whole milk bill passed in your state and signed by your Governor.

Pennsylvania and New York State tried to be first, but leaders are afraid of USDA’s monetary penalties. Maybe the No. 8 and No. 5 milk producing states can be second and third in state whole milk bill passage.

Just think what would happen if more states passed bills that ALLOWED choice and sought creative language to let their schools choose to let children choose. Tennessee will make it available in bulk dispensers separate from the school lunch line. Pennsylvania sought to do it as a wholly in-state proposition.

Meanwhile, DMI sent a press release on April 29 touting their “checkoff-led pilot in Cincinnati schools that offered lactose-free chocolate milk increased milk consumption…” Specifically, the pilot schools experienced a 16% increase in milk consumption and a 7% higher meal participation, according to DMI.

(Of course, this lactose-free pilot was also fat-free per the USDA rules for milk at school built on the Dietary Guidelines that the dairy checkoff agreed to “advance” when the memorandum of understanding was signed between the USDA, National Dairy Council, GENYOUth and the NFL in 2010).

Remember, this reporter warned several years ago that checkoff and dairy industry leaders would wait until lactose-free shelf-stable milk was firmly entrenched in schools before pushing whole milk choice through. Senate Ag Chairwoman Debbie Stabenow is the main blockade this time around. She hails from the No. 6 milk producing state of Michigan, where the foundation fairlife plant is located, collecting milk from large producers in Michigan, Indiana and Ohio.

Wonder what consumption looks like when whole milk is offered as a choice. That’s right! A Grassroots PA Dairy Advisory Committee / 97 Milk trial in a school in northwestern Pennsylvania saw consumption grow 52% and waste decline 95%.

So, drink up Senators! Talk to your constituent Moms this Mother’s Day. Sales data and surveys both show what Moms think, and most don’t even realize the federal ban, the bait-and-switch their kids face at school where milk and dairy are concerned.

Then pour a tall cold glass of delicious, nutritious whole milk. It may just strengthen those political spines!

EAST EARL, Pa. — The status of the Whole Milk for Healthy Kids Act, S. 1957, has 17 Senate sponsors from 13 states, including 12 Republicans, 4 Democrats, and 1 Independent.

Even though both NMPF and IDFA have shown support for the measure, a bit of resignation can be sensed — riding the overwhelming House vote as enough progress for one legislative session. After taking bows for the performance of the bill in the House, representatives of both NMPF and IDFA – while speaking at winter meetings – have indicated a prevailing view that Senate opposition to S. 1957, is a big barrier.

They say they are working to get the science in front of the Dietary Guidelines Committee, which has been tried before – over and over.

The DGA committee operates under a USDA that does not want whole milk options in schools or SNAP or WIC. This same USDA is proposing to remove chocolate milk options from schools, except for senior high students, and is proposing to reduce WIC milk by 3 gallons per recipient per month. This same USDA projects 20 billion more pounds of milk will be produced in the U.S. by 2030, according to IDFA CEO Michael Dykes, presenting future trends at the Georgia Dairy Conference in Savannah.

Seeds of doubt about the whole milk bill are being sown among farmers. Some asked me recently if their co-ops will lose money on the deal.

This week we look at the second C: ‘Consternation’ — a fancy word for fear.

“What will they do with all of our skim?” farmers asked me at a recent event. Is this something they are hearing from a milk buyer or inspector?

Here are some facts: Whole milk sales move the skim with the fat — leaving some of the fat through standardization, but not leaving any skim. Therefore, an increase in whole milk sales does not burden the skim milk market.

Surely, the practice of holding schoolchildren hostage to drinking the byproduct skim of butter and cream product manufacturing is a poor business model if we care about childhood nutrition, health, and future milk sales.

Furthermore, the market for skim milk powder and nonfat dry milk is running strong as inventories are at multi-year lows in the U.S. and globally.

Cheese production, on the other hand, is what is cranking up, and it has been the market dog for 18 months. Like whole milk sales, cheesemaking uses both fat and skim. But cheesemaking leaves byproduct lactose and whey, and it can leave some residual fat depending on the ratios per cheese type.

Things are pretty bad for farmers right now in cheesemilk country. Some tough discussions are being had around kitchen tables. The 2022 Ag Census released last week showed the dire straits for farmers nationwide over the last five years as the number of U.S. dairy farms declined below 25,000, down a whopping 40% since 2017.

Wouldn’t an increase in whole milk sales through the school milk channels help pull some milk away from rampant excess cheese production that is currently depressing the Class III milk price, leading to price divergence and market dysfunction?

While there is no one data source to specifically document the percentage of the milk supply that is sold to schools, the estimates run from 6 to 7% of total fluid milk sales (Jim Mulhern, NMPF, 2019), to 8% of the U.S. milk supply (Michael Dykes, IDFA, 2023), to 9.75% of total fluid milk sales (Calvin Covington, independent analysis, 2024).

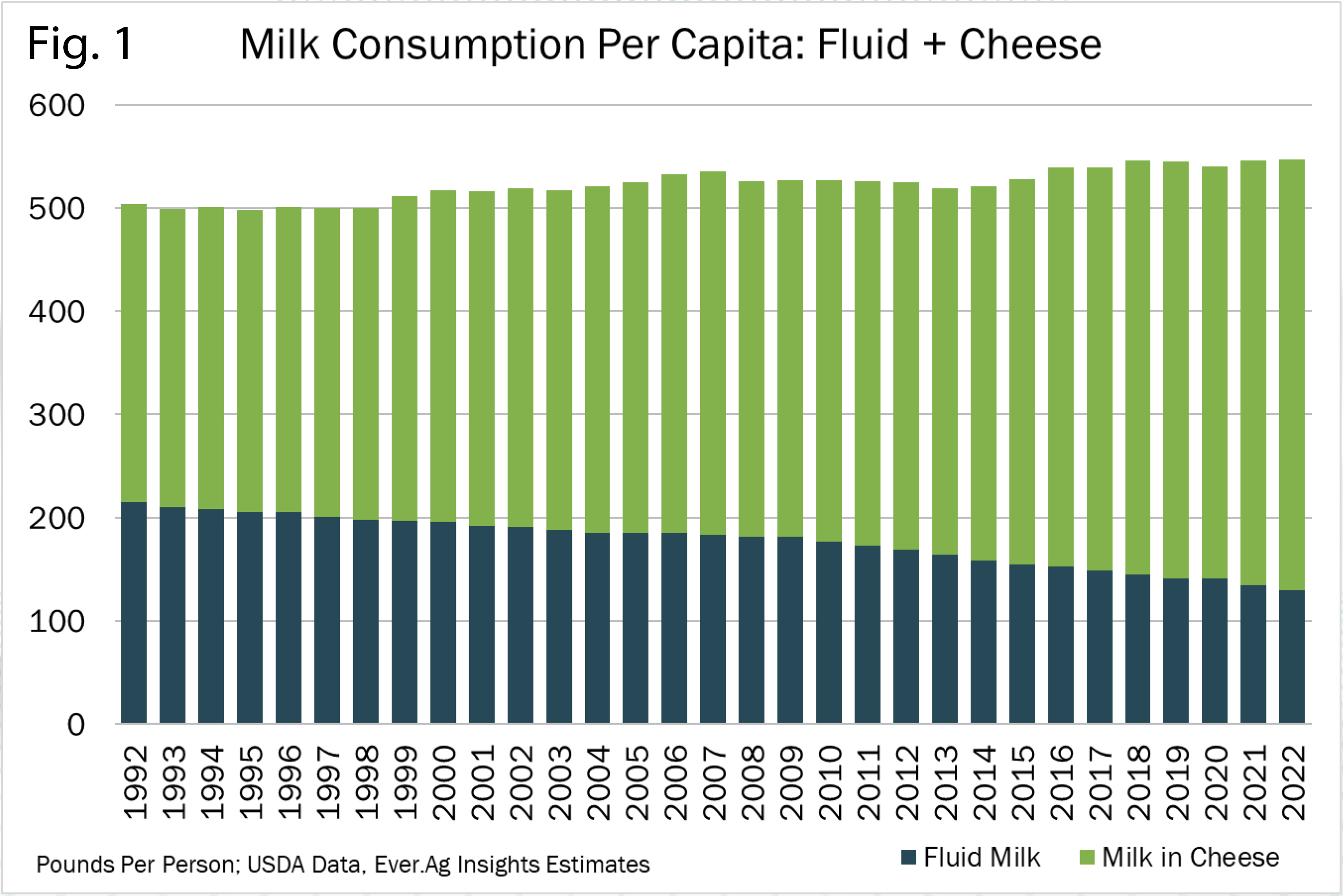

If even half of these sales became whole milk sales, it could modestly positively impact the amount of excess cheese being made even as processors say they plan to make more cheese because people eat more of their milk than are drinking it. (Fig. 1)

Meanwhile, the cheese price is under so much downward price pressure that there is a $2 to $4 divergence of Class IV over Class III causing farmers to lose money under the ‘averaging’ formula for Class I milk. In many parts of the country, farmers lose additional money when the milk that is used in Classes II and IV is depooled out of FMMOs.

Without the ‘higher of’ pricing mechanism that was in place from the year 2000 until May 2019, Class I can fall below the higher manufacturing price, removing incentive to pool, which leaves pooled producers with smaller payments for their milk and leaves the decision about what to pay depooled farmers up to the processors after they’ve succeeded in reducing the benchmark minimum by depooling.

Ultrafiltered (UF) milk represents 2.4% of fluid milk market share, having grown by more than 10% per year for four years with sales up 7.7% in 2023 vs. 2022, according to Circana-tracked market data shared by Dykes.

UF milk is also cheese-vat-ready-milk with capability to remove not just the lactose but also the whey as permeate at the front end for use in distilleries that are now funneling lactose into ethanol production in Michigan and whey into alcoholic beverages in Michigan and Minnesota.

Processors want farmers to do “a tradeoff” to decide how much revenue comes to their milk checks and how much goes to processing investments for the future. The future is being dictated by where we are in fluid milk consumption relative to cheese production.

This is one reason IDFA and Wisconsin Cheesemakers, as well as NMPF, had proposals asking USDA to increase the processor credits (make allowances) that are embedded in the dairy product price formulas. IDFA and Milk Innovation Group also put forward other proposals to further reduce regulated minimum prices.

We wonder with these new processing investments, how is it that the make allowances are too small? Only bulk butter, nonfat dry milk, dry whey, 40-lb block Cheddar and 500-lb barrel cheese (yellow not white) are surveyed for the circular class and component price formulas. Everything else that doesn’t meet CME spec for these specific product exchanges is excluded.

This means the costs to make innovative new products and even many bulk commodity-style products, such as bulk mozzarella, unsalted butter, whey protein concentrate and skim milk powder, can be passed on to consumers without being factored back into the FMMO regulated minimum prices paid to farmers.

If market principles are applied, processors wanting to encourage more milk production, to make more cheese, would pay more for the milk – not less. But when the margin can be assured with a make allowance that yields a return on investment, all bets are off. Cheese gets made for the ‘make’ not the market.

We saw processors petition USDA in the recent Federal Milk Marketing Order hearing to reduce the minimum prices in multiple ways so they can have the ability to pay market premiums to attract new milk. This would be value coming out of the regulated FMMO minimum price benchmark for all farmers to get added back in by the processors wherever they want to direct it.

Cheese is in demand globally, and the U.S. dairy industry is investing to meet this. Dykes told Georgia producers that processors want to grow and producers want to grow. He wasn’t wondering what to do with all of the skim when he asked: “Where will the milk come from for the over $7 billion in new processing investments that will be coming online in the next two to three years?”

This is happening, said Dykes, “due to market changes from fluid milk to more cheese production (Fig. 1). There’s a lot of cheese in those plans. With over $7 billion in investment… These are going to be efficient plants. You’re going to see consolidation. If you are part of a co-op, you’re going to decide how much (revenue) comes in through your milk check and how much goes into investment in processing for the long-run, for the future. That’s the debate your boards of directors will have.”

Even the planned new fluid milk processing capacity is largely ultra-filtered, aseptic and extended shelf life, according to Dykes.

“That’s the direction we are moving,” he said. “We are seeing that move because as we think about schools, are we still going to be able to send that truck driver 20 miles in any direction with 3 or 4 cases of milk 5 days a week? Or do we do that with aseptic so they can store it and put it in the refrigerator one night before, and get some economies of scale out of that, and maybe bring some margin back to the business?”

As the Class III milk price continues to be the market dog, we don’t see milk moving from Class III manufacturing to Class IV, perhaps because of the dairy processing shifts that have been led by reduced fluid milk consumption.

Allowing schoolchildren to have the choice of whole milk at school is about nutrition, healthy choices, future milk consumers, and the relevance of fresh fluid milk produced by local family farms in communities across the country. Having a home for skim does not appear to be the primary factor affecting milk prices where Class III is dragging things down.

Bottomline, dairy farmers should have no consternation (fear) over what processors are going to do with “all of that skim” once they are (hopefully) allowed to offer schoolchildren milk with more fat.

Next time, we’ll address the third ‘C’ – Competition – If kids are offered whole milk in schools, will it reduce the butterfat supply and impact the industry’s cheese-centered future?

A final note, just in case the question about ‘what to do with all that skim’ still bothers anyone… What’s wrong with animal feed markets for skim milk powder? Protein is valuable in animal health, there are livestock to feed, and people spend major bucks on their pets too. Did you know dog treats made with nonfat dry milk powder, flour and grated cheese are a thing?

That idea got a good laugh from those farmers when I suggested it.

However, Cornell dairy economist Dr. Chris Wolf noted recently how China’s purchases are what drive global skim milk powder and whey protein prices, and that much of that market for both is to feed… you guessed it… Pigs.

EAST EARL, Pa. — While decades of scientific debate in terms of childhood health and nutrition is the curtain opponents hide behind, the anti-animal agenda is the top hurdle for the Whole Milk for Healthy Kids Act in the Senate.

Senator Roger Marshall (R-Kan.) is the prime sponsor of the Senate bill, and he is a medical doctor in obstetrics and is taking a beating from billboards sponsored by Physicians Committee for Responsible Medicine (PCRM) in his home state of Kansas. PCRM is a known arm of PETA. This tells us quite a bit, doesn’t it?

Meanwhile, the top 3 C’s facing the bill within the dairy industry, itself, need to be addressed.

1) Confusion… Will it really improve milk prices? Addressed in this article

2) Consternation (fear)… What will processors do with “all of that skim”? Addressed in Part II here

3) Competition… Will it reduce the butterfat supply and affect the ramp up in cheese manufacturing or other dairy products? Addressed in Part III here

Plus…. the Checkoff Commitments… Will it interfere with checkoff-funded Milk Molecules Initiative for new beverages that identify and separate specific milk molecules for specific benefits (sleep drinks, energy drinks, immune function drinks, specific protein type drinks)?

All of these questions are quietly floating around and sowing seeds of doubt, leading to analysis-paralysis, while the industry focus is on innovation and exports, not on fresh milk, or a healthy next generation of U.S. milk consumers.

All of these questions will be answered one at a time over the next several weeks, starting with the first “C”: Confusion.

“Will this bill really improve our milk prices?” was the question I was asked by a few farmers at a recent farm show. My response was to ask them if they are concerned about kids having healthy milk options they enjoy and if they are concerned about seeing further erosion of fluid milk sales, and losing another generation of milk drinkers?

I reached out to Calvin Covington, former milk cooperative CEO in the fluid milk markets of the Southeast and a primary architect of pricing milk by component yield even before Order Reform during his years with American Jersey Cattle Breeders.

Covington ran the numbers using 2023 average prices, and calculating pounds of milk, fat, and skim, utilization, and values, which yield a gross value of a hundredweight of milk being used for fluid processing at different fat levels.

“At a $3.00 Class I differential, a hundredweight of milk going for 3.25 fluid milk (whole milk as standardized), returns an additional 25 cents per hundredweight over skim milk,” Covington writes, noting that the difference will change based on different Class I differentials.

Even in the counties with small or zero location differentials on the map, the base differential of $1.60 per hundredweight is still included, which means at least a 13 cents per hundredweight difference.

Previously, Covington has noted in presentations that milk prices improve as the average fat level of total fluid milk sales increases. The current average of all sales, nationwide, stands at 2%. A few years ago, it was below 2%. A fractional change in either direction influences Federal Milk Marketing Order blend prices.

Fluid milk demand also plays a role in manufacturing class prices, affecting farmers in regions where prices are based almost exclusively on cheese.

That’s especially true right now as cheese production has been exploding, and the Class III milk price has been imploding, creating a wide spread below Class IV and pushing FMMO blend prices lower as milk is not moving out of Class III to the higher value Class IV. But the Federal Milk Marketing Law gives Class I dibs to attract milk. So Class I demand is relevant for cheese milk pricing too.

As whole milk sales have increased year-over-year, whole milk became the largest category of fluid milk sales in 2021. It is a bright spot in the fluid milk category.

In 2023, gains in whole milk sales and in lactose-free milk sales are credited with boosting the entire fluid milk category for year-over-year gains in back-to-back months of October and November. This helped flatten the year-to-date loss-curve on total fluid milk sales that had been running 2 to 4% lower year-over-year to be just 1.5% lower cumulatively at year end compared with 2022, according to USDA’s December estimated packaged fluid milk sales report, released in mid-February.