Covering Ag since 1981. The faces, places, markets and issues of dairy and livestock production. Hard-hitting topics, market updates and inspirational stories from the notebook of a veteran ag journalist. Contributing reporter for Farmshine since 1987; Editor of former Livestock Reporter 1981-1998; Before that I milked cows. @Agmoos on Twitter, @AgmoosInsight on FB #MilkMarketMoos

EAST EARL, Pa. – In December, the House passed Congressman G.T. Thompson’s Whole Milk for Healthy Kids Act, H.R. 1147. This is a major milestone for this bill, which passed in the U.S. House of Representatives by an overwhelming bipartisan 330 to 99 vote.

Pictured are a few of the members of the Grassroots Pennsylvania Dairy Advisory Committee and others who joined them for a staff briefing at the Capitol last summer. The focus now is on the U.S. Senate. From left are Christine Ebersole, school nurse in Blair County, Pa.; John Bates, then executive director of The Nutrition Coalition; Nelson Troutman, Berks County dairy farmer and his granddaughter Madelyn, 2022-23 Lebanon County Dairy Maid; Congressman G.T. Thompson (R-PA-15), the champion and prime House sponsor of the Whole Milk for Healthy Kids Act; Sara Haag, 2023-24 Berks County Dairy Princess; Krista Byler, school foodservice director in Crawford County, Pa.; and Sherry Bunting, Farmshine contributor and volunteer advocate for whole milk in schools. Photo courtesy Maddison Stone

“The next stop is the Senate, and we are going to have to work hard to get the Senate bill (S. 1957) to the floor and passed. In Pennsylvania, we need to work on our Senator Bob Casey. We already have Senator John Fetterman as a cosponsor of the bill, but we need Senator Casey also,” says Nelson Troutman, Berks County farmer and originator of the Drink Whole Milk 97% Fat Free baleboards that led to the 97 Milk effort and 97milk.com

“We also need more Senators to cosponsor S. 1957 from across the country,” adds Bernie Morrissey, retired agriculture advocate from Robesonia, Pa. “We need dairy farmers, agribusinesses, organizations and citizens all across the country to reach out to their Senators to cosponsor this bill.”

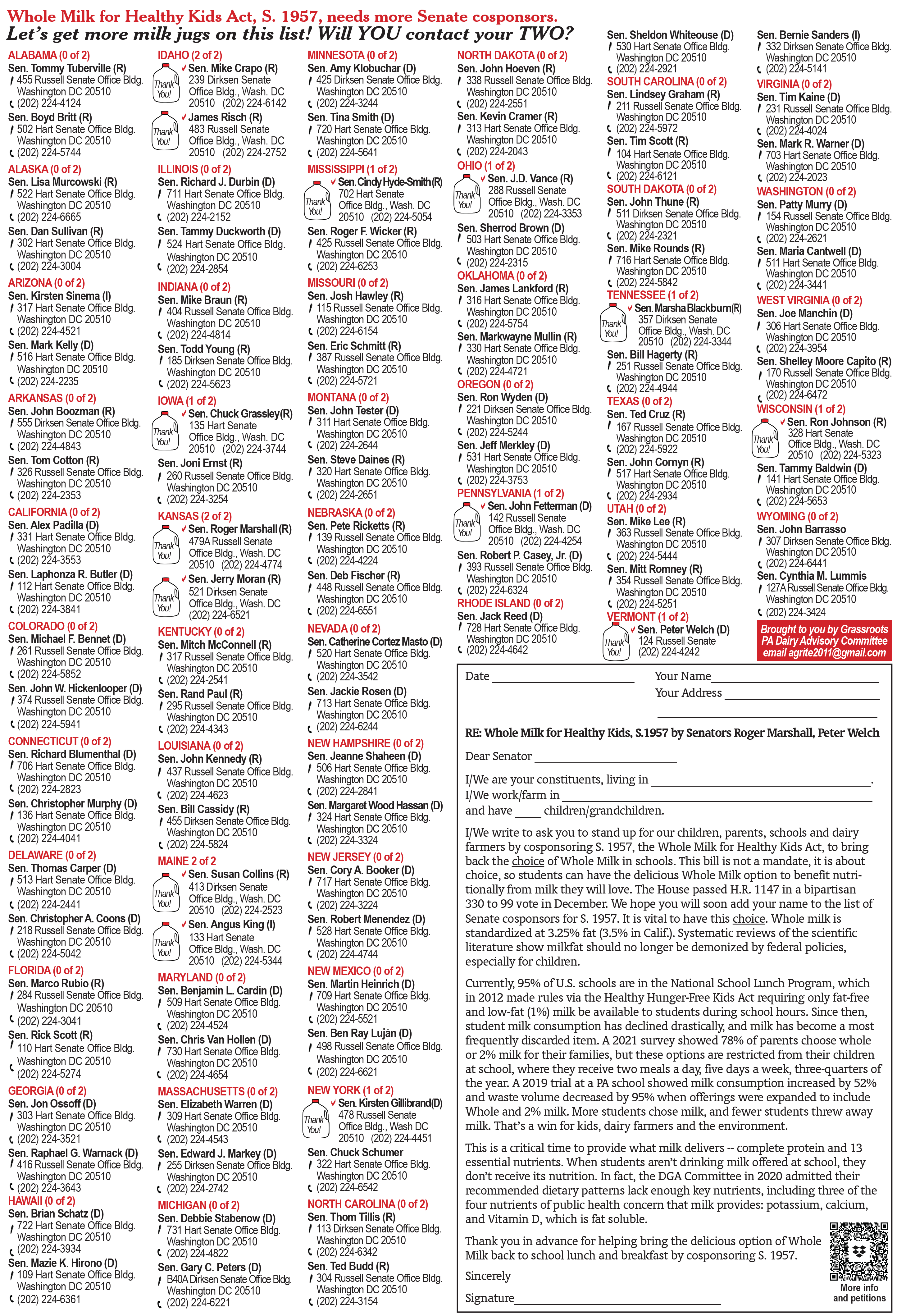

The Senate bill has 14 cosponsors from 11 states as of January 20th. They include Republicans, Democrats and an Independent as follows: both Dr. Roger Marshall (prime sponsor) and Jerry Moran of Kansas, Peter Welch (prime cosponsor) of Vermont, Ron Johnson of Wisconsin, John Fetterman of Pennsylvania, both James Risch and Mike Crapo of Idaho, both Susan Collins and Angus King of Maine, Kirsten Gillibrand of New York, Cindy Hyde-Smith of Mississippi, Chuck Grassley of Iowa, J.D. Vance of Ohio, and Marsha Blackburn of Tennessee.

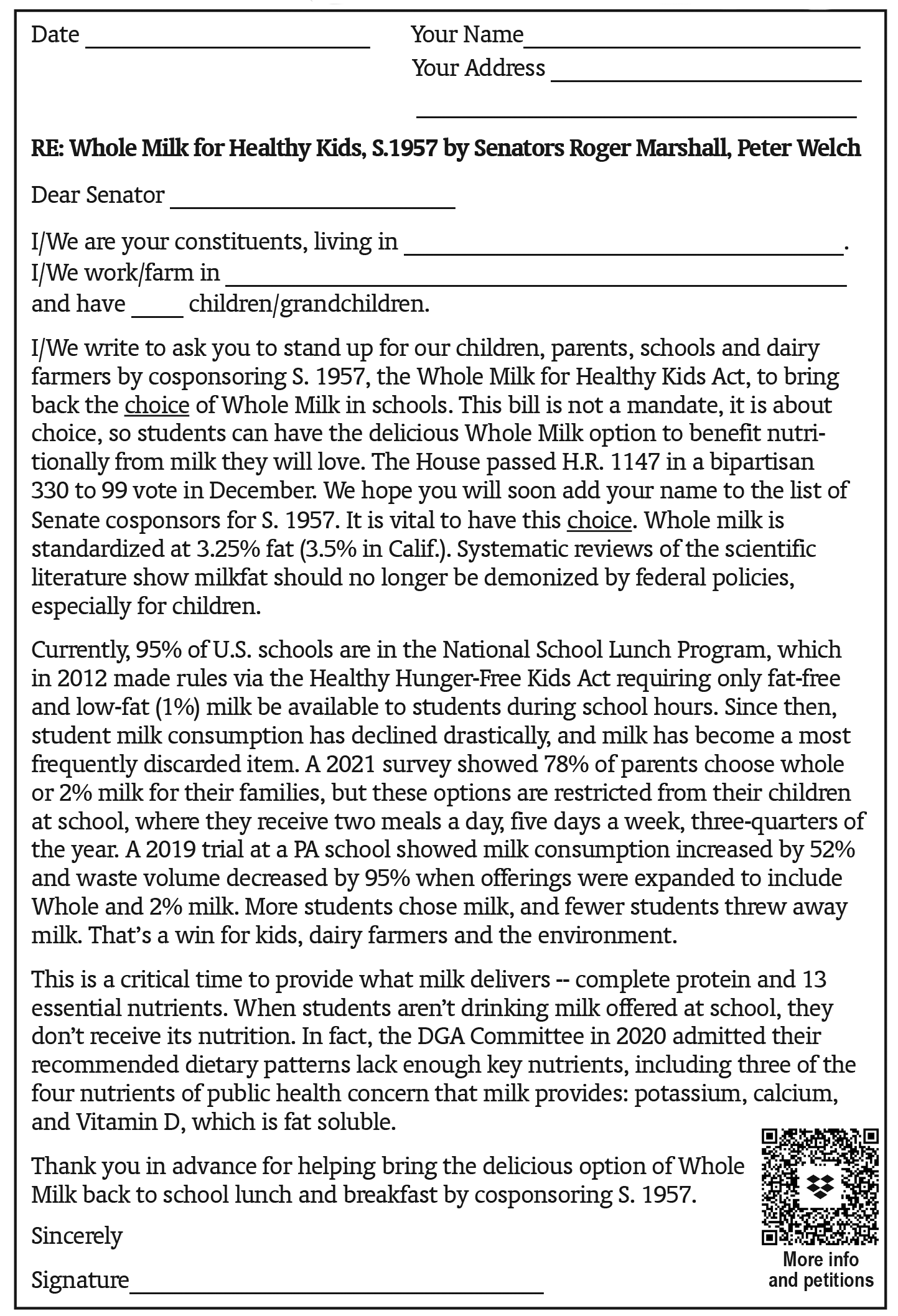

“Every state has two United States Senators. We want every dairy farmer, every organization and business calling their two Senators. If they are already a cosponsor, thank them. If they are not a cosponsor, please write to them, and use our sample letter (or the template at the end of this article),” Bernie explains.

(Find the Washington addresses and phone numbers for your state’s Senators at https://www.senate.gov/ – Click the icon in the top left corner, select your state from drop-down menu to see how to contact them. Go to the end of this article to learn about email options. Some additional resources can be found in a folder at https://qrco.de/WholeMilk-Info )

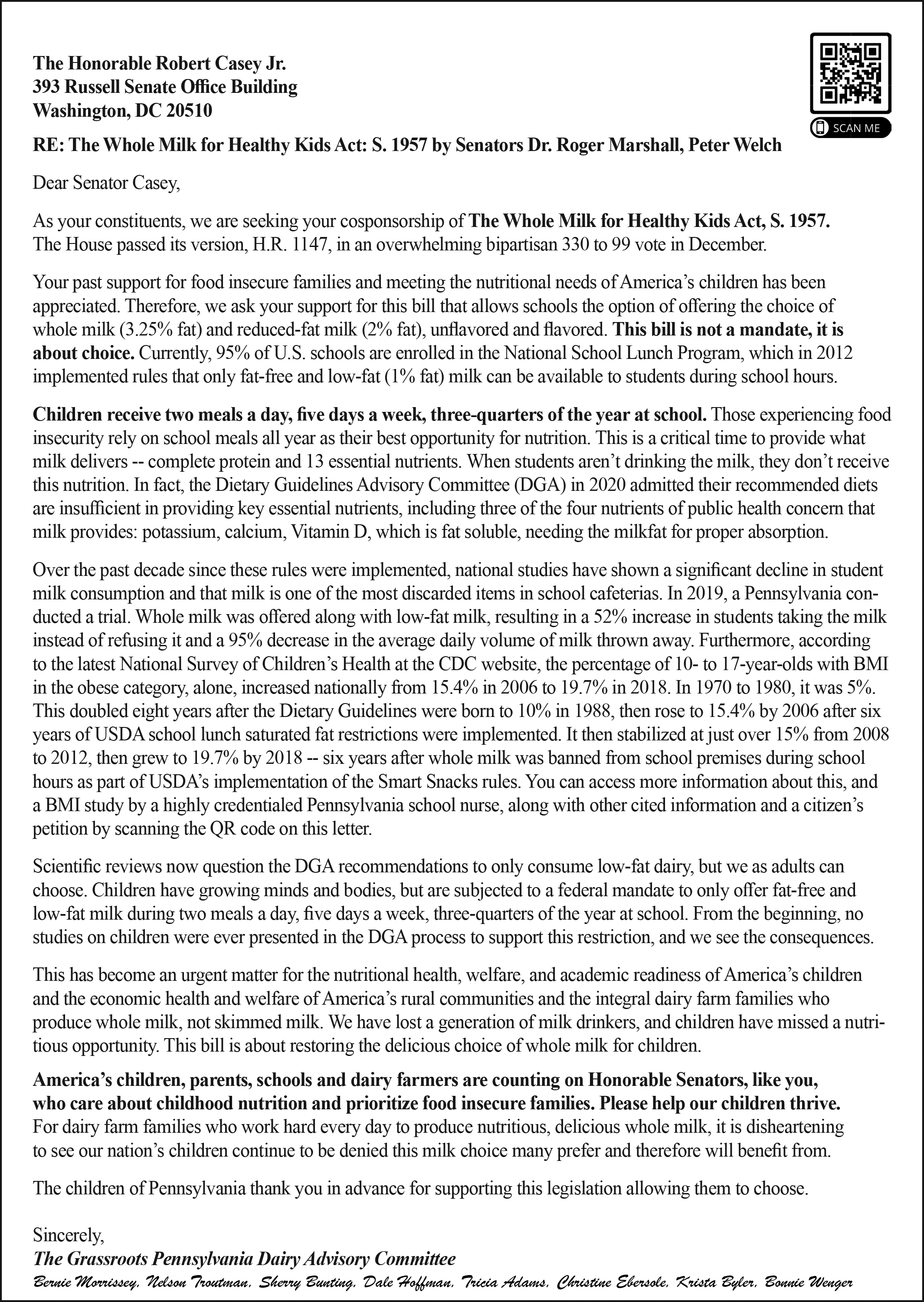

“We have written to Senator Casey (see letter at top) to let him know how important this is to us, to the children of Pennsylvania, and to the dairy farmers. We need more people, organizations, and businesses to write to him also. If this doesn’t work, it will be our own fault for not getting involved,” he stresses, adding that constituent phone calls and visits are also welcome.

“We must also contact Senate Ag Committee Chairwoman Debbie Stabenow of Michigan. It is important that she knows how vital this bill is to come through her committee to the Senate floor,” Bernie notes. (The call-in notice below was published in the Jan. 5 Farmshine).

The Grassroots Pennsylvania Dairy Advisory Committee asks organizations and agribusinesses to use the sample letter on this page as-is or tailor it to their state’s Senators and also send it out to all their members or customers asking them to each sign it and send it to their two Senators as well.

“Let us know if you did this,” Bernie continues. “We want to know: Did YOU contact your TWO?” (Email Sherry Bunting at agrite2011@gmail.com or text or call 717.587.3706 to confirm you contacted your two.)

“After all,” Bernie observes: “If the dairy farmer’s next generation of consumers – the children — cannot choose milk they will love, what is your future as a dairy farmer? And what is their future as tomorrow’s leaders?”

“Whole milk is nutritious and delicious. Science supports this choice. It’s up to each one of us to get it done.”

-30-

To email your Senators directly, go to https://democracy.io/ – type in your own address, city and zip code, click submit. Your two Senators and one Representative will show up with red checkmarks. Click ‘Write to them,’ and on the next screen compose the body of your letter. First, say who you are and where you live/work/farm and mention if you have children or grandchildren in school, if you wish. Sample text about cosponsoring S. 1957 can then be copied and pasted from the template below:

———————————————————————————————————————-

Dear Senator,

I write to ask you to stand up for our children, parents, schools and dairy farmers by cosponsoring S. 1957, the Whole Milk for Healthy Kids Act, to bring back the choice of Whole Milk in schools. This bill is not a mandate, it is about choice, so students can have the delicious Whole Milk option to benefit nutritionally from milk they will love. The House passed H.R. 1147 in a bipartisan 330 to 99 vote in December. We hope you will soon add your name to the list of Senate cosponsors for S. 1957.

It is vital to have this choice. Whole milk is standardized at 3.25% fat (3.5% in Calif.). Systematic reviews of the scientific literature show milkfat should no longer be demonized by federal policies, especially for children.

Currently, 95% of U.S. schools are in the National School Lunch Program, which in 2012 made rules via the Healthy Hunger-Free Kids Act requiring only fat-free and low-fat (1%) milk be available to students during school hours. Since then, student milk consumption has declined drastically, and milk has become a most frequently discarded item. A 2021 survey showed 78% of parents choose whole or 2% milk for their families, but these options are restricted from their children at school, where they receive two meals a day, five days a week, three-quarters of the year. A 2019 trial at a PA school showed milk consumption increased by 52% and waste volume decreased by 95% when offerings were expanded to include Whole and 2% milk. More students chose milk, and fewer students threw away milk. That’s a win for kids, dairy farmers and the environment.

This is a critical time to provide what milk delivers — complete protein and 13 essential nutrients. When students aren’t drinking milk offered at school, they don’t receive its nutrition. In fact, the DGA Committee in 2020 admitted their recommended dietary patterns lack enough key nutrients, including three of the four nutrients of public health concern that milk provides: potassium, calcium, and Vitamin D, which is fat soluble.

Thank you in advance for helping bring the delicious option of Whole Milk back to school lunch and breakfast by cosponsoring S. 1957.

USDA’s cross examination reveals possible flaw in simulator model result

By Sherry Bunting, Farmshine, Jan. 19, 2024

CARMEL, Ind. — Shadow pricing, demand elasticity, commoditized loss of prior incentives, balancing cost, give-up cost, base differential, uniform differential, market-clearing price…

These terms ruled the day when the USDA National Hearing on Federal Milk Marketing Order (FMMO) proposals resumed in Carmel, Indiana this week after a more than four-week recess.

The hearing began in late August. It did not conclude by Fri., Jan. 19, so it will again recess until Jan. 29.

American Farm Bureau estimates that another 270 days of post-hearing processes must follow before a USDA decision could be implemented, and even this is subject to proposals that seek a 15-month delay between decision and implementation due to potential impacts on CME futures-based risk management tools, such as Dairy Revenue Protection (DRP).

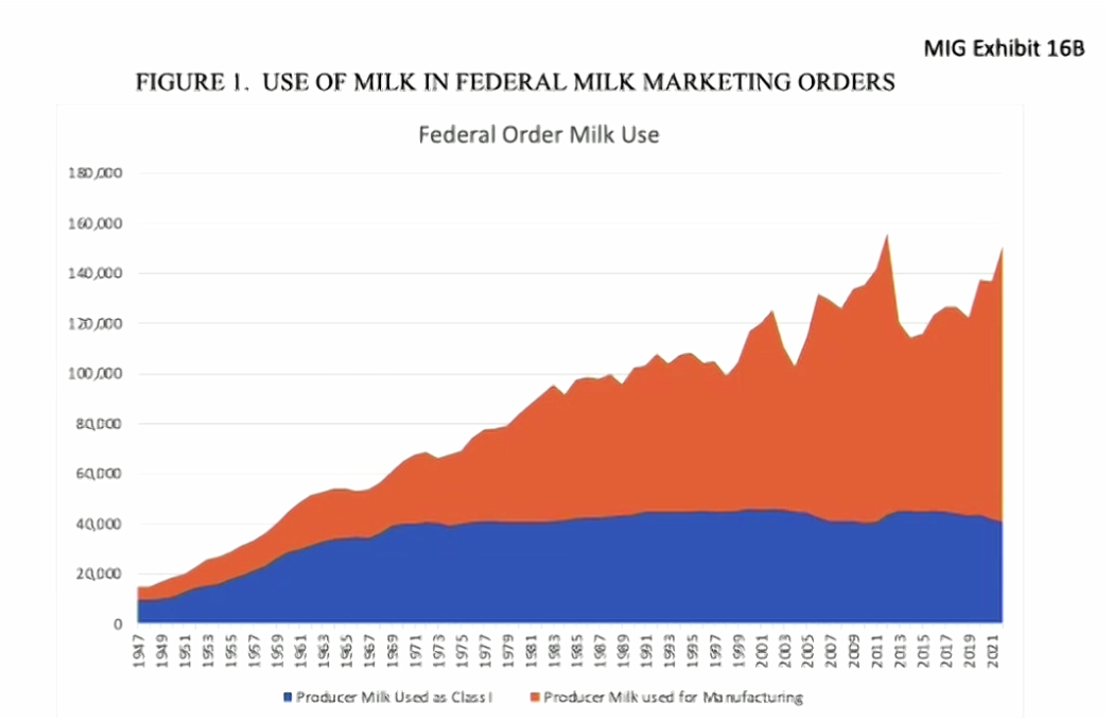

This is far from over, and hanging in the balance is the Class I price calculation, now based on an averaging method, under which farmers have lost more than $1.02 billion since May 2019 vs. the previous ‘higher of’.

Testimony Tues., Jan. 16 included Dr. Mark Stephenson, retired UW-Madison dairy economist on behalf of Milk Innovation Group (MIG), made up of ‘innovative’ and branded fluid milk processors, including fairlife, HP Hood, Anderson-Erickson, Danone North America, Shamrock, Organic Valley, Aurora Organic, and Pennsylvania’s own Turner Dairy Farms.

Dr. Stephenson delivered his bombshell for MIG that was based on analysis he did using 2016 data in a simulator model, from which he made “certain discoveries.”

First, Stephenson suggested that fluid milk is shifting to become price-elastic vs. the long-held belief that fluid milk sales are price-inelastic. This was followed up by fluid milk processor representatives showing post-Covid fluid milk sales volumes declined as prices rose.

Stephenson cautioned USDA to refrain from setting regulated prices too high, saying this would reduce returns to producers by reducing total fluid milk sales.

This suggestion was challenged in cross examination. In fact, AFBF chief economist Dr. Roger Cryan noted the FMMO focus on fluid milk was originally partly predicated on its “public good” as a food staple, almost akin to a “public utility.”

In cross examination on Jan. 17, Stephenson also revealed he was paid by MIG to analyze the $1.60 base differential, and his work began before MIG finalized its proposal to remove the $1.60 per cwt. base differential all the way down to zero for all Class I milk, nationwide.

Currently, the $1.60 base differential is built uniformly into the Class I price for every regulated county across all FMMOs. The varied location differentials are added to the base differential and spread across the revenue-sharing pools.

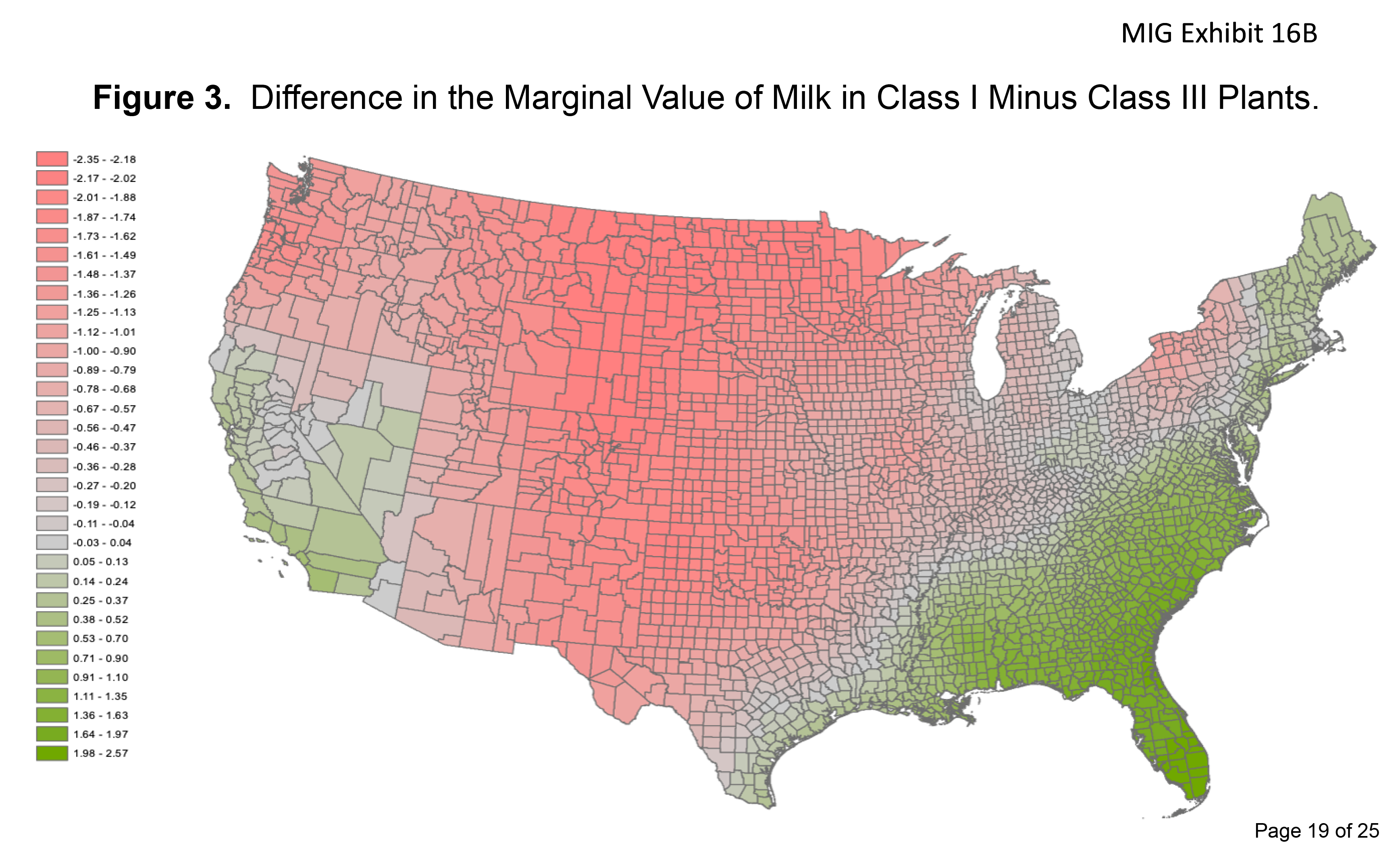

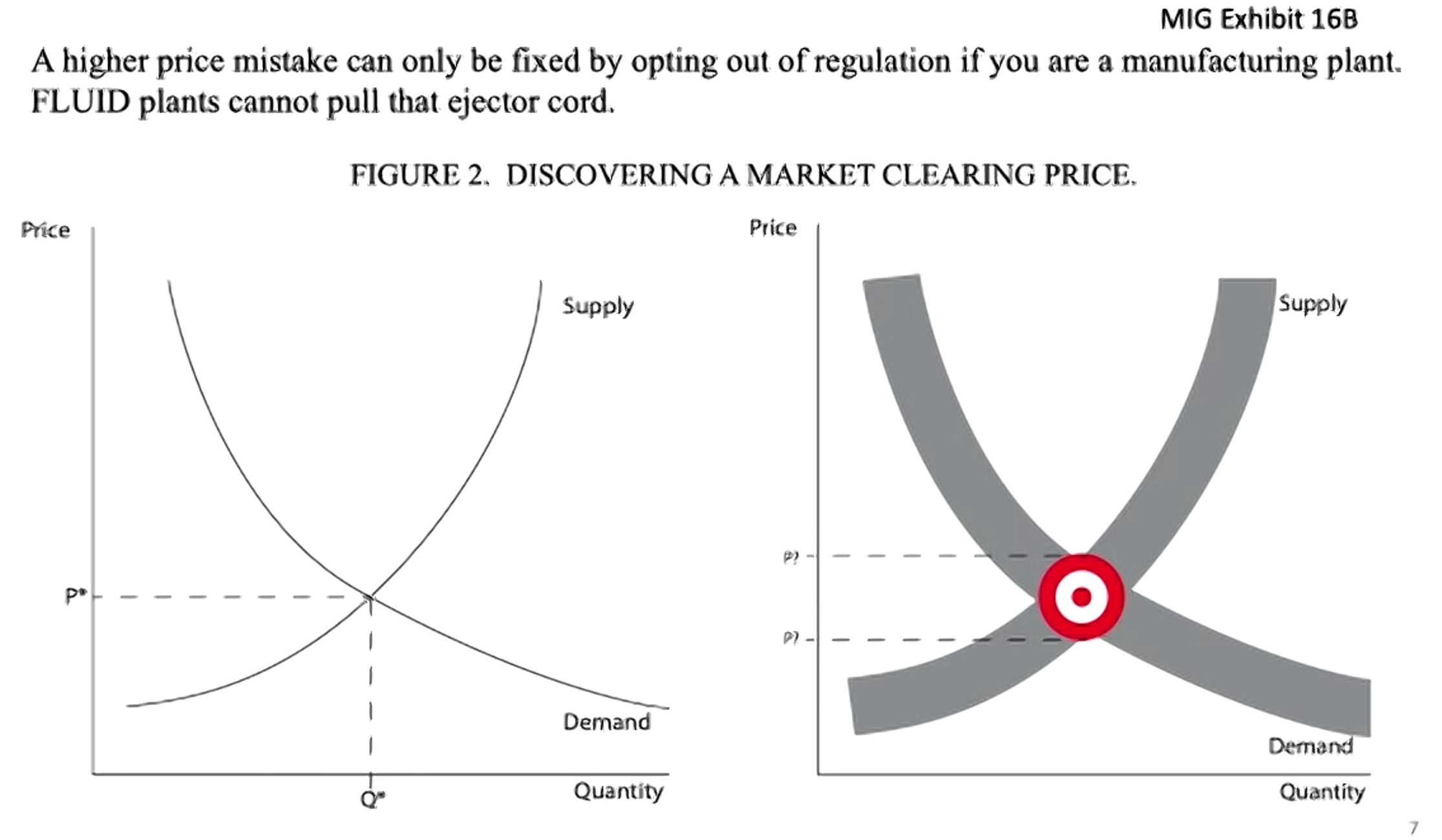

Stephenson used the U.S. Dairy Sector Simulator Model (USDSS) to develop a map as though a “milk-dictator” could efficiently “move milk to its highest global use” through various constraints.

In the marginal value map result, Stephenson said the U.S. average value of the differences was minus-38 cents, indicating on a national average, it is more valuable (cost saving) to the model to have milk in a cheese plant than in a fluid plant in most counties. The range goes from somewhat more than $2 per cwt more favorable to a cheese plant (in red) to somewhat more than $2 per cwt more favorable to a fluid plant (in green) in the Southeast. From this “potent revelation,” Dr. Stephenson concludes that, “The model result bolsters the argument to not dilute the value of the $1.60 into the pool if that value represents a balancing cost for fluid and an opportunity cost (give-up) for manufacturing plants. Rather, require the fluid plants to pay the $1.60, but let the fluid plants pay that directly to the farms, cooperatives or manufacturing plants who supply the milk” to the fluid plant.

The map showed the incremental differences in ‘Class I minus Class III “shadow pricing,” across the country.

These marginal value differences, said Stephenson, reflect the opportunity costs of getting manufacturing plants to give up milk to fluid plants in the Central U.S., where milk production exceeds population vs. the cost to balance fluid milk markets in the East, particularly the Southeast, as well as in California and southern Nevada, where population exceeds milk production.

It was the questioning from USDA AMS administrator Erin Taylor on the ‘shadow pricing’ figures in various anchor cities that prompted Stephenson to concede: “You may have caught a major flaw in what I have done here, so I would want to look at this more carefully.”

Yes, he will be back to address such questions when the ever-lengthening hearing resumes on January 29.

Notwithstanding exposure of a possible flaw in the simulator analysis, Stephenson said the ‘market-clearing’ price is the target to aim at, and the system of setting regulated minimum prices “should err on the side of being too-low instead of too-high.”

He said processors will pay premiums in the breach of a ‘too-low’ minimum price, but there are few options for processors to deal with a ‘too-high’ minimum price — other than to opt out of regulation for manufacturing plants (de-pool), but that fluid milk plants have no ability to opt out. They are required to remain regulated by FMMOs.

“Manufacturing is by far the largest use of milk in our dairy industry,” he said, noting that Class I fluid use at 18% of total U.S. milk production (regulated and unregulated). Therefore, he said, manufacturing use should no longer be treated in the FMMO system as “the trailing spouse in the marriage.”

On MIG’s behalf, he introduced a new way of looking at the marginal value between Class III and Class I, and a mechanical change that could be made in how the $1.60 base differential is paid as needed directly to producers, cooperatives and plants that actually supply milk to Class I plants, instead of being paid to the FMMO pools.

The $1.60 became a uniform part of the Class I price in the 1999 Order Reform. About 40 cents of this $1.60 was included to represent the cost of farmers transitioning from Grade B to Grade A. The rest represents ‘give up’ costs from manufacturing to Class I and balancing costs to serve the fluid market.

Stephenson backed up MIG’s assertion that farmers don’t need any of this $1.60 base differential because virtually all milk produced today is now Grade A. During cross examination, NMPF attorneys brought up the cost farmers have to maintain Grade A status. Don’t their costs count here?

Undeterred, Stephenson suggested that these costs are accounted for in the classified pricing since all milk for all uses is Grade A, today. He said that USDA uses ‘minimum pricing’ as a tool so that the regulated price leaves space for voluntary premiums that processors can pay to “incentivize something else.”

“Being chronically above the market-clearing price creates a surplus product, which the market can’t clear,” said Stephenson. “Our dairy markets have always walked on a knife’s edge. Being plus or minus 1% on milk supplies can cause some pretty big swings in prices as the markets do attempt to clear that.”

As for removing the $1.60 uniform price differential either from the price or the pool, Stephenson said it is like “other premiums” that have become “commoditized.”

He likened it to the rbST premium and milk quality premiums, saying those premiums have also become “commoditized.”

For example, when farmers were first asked to give up rbST and sign pledges, a premium was offered. Now, that premium is not paid, he said, because the practice of abandoning rbST is now “commoditized.”

Likewise, said Stephenson: “Milk quality (low SCC) has improved so much that those premiums are not there anymore. They have also become commoditized.”

So, the better dairy farmers get, the more their incentive premiums — and even big chunks of their regulated minimum price — are at risk to be cannibalized by milk buyers because the farmers have now done what they’ve been incentivized to do, so they don’t need to be paid to do it.

MIG also seeks to stop NMPF’s proposal to tweak and raise location differentials across the Class I surface map, putting on the stand some of their members to show how unfair competition arises between independent bottlers and cooperatively owned fluid milk plants in the same region.

For his part, Stephenson noted the concept of pulling the $1.60 base differential out of the pool may discourage non-productive distant pooling.

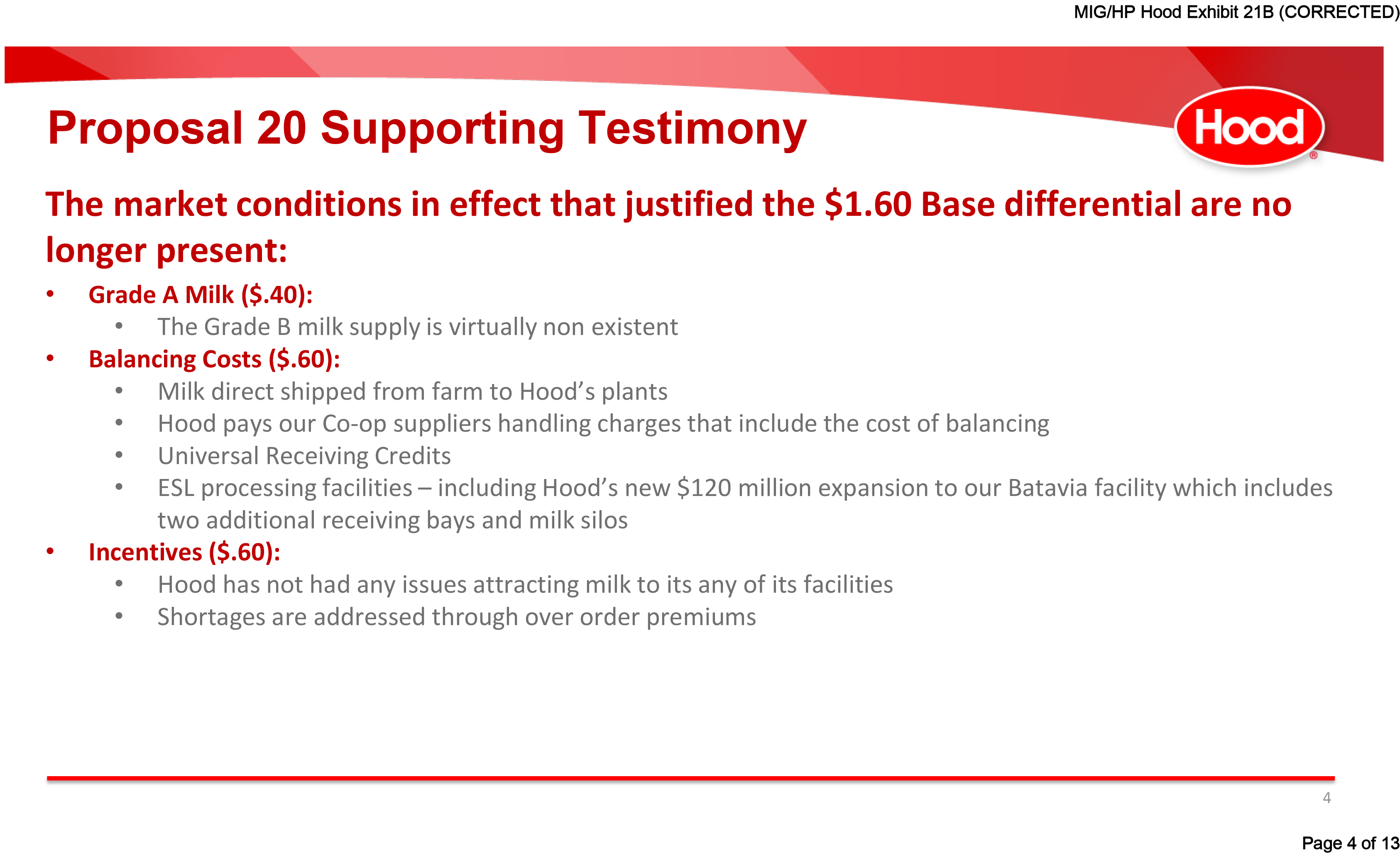

This week was certainly eye-opening as MIG is all about the processor costs with zero regard for producer costs. They even put an HP Hood representative on the stand who included the $120 million recently announced for expanding the Extended Shelf Life (ESL) plant in Batavia, NY as a “balancing cost,” that somehow justifies giving back the base differential to processors even though processors can pass their costs on to consumers, whereas farmers cannot.

Under cross examination, Hood’s representative admitted that plant-based beverages are also bottled in those so-called ESL ‘milk balancing’ facilities, along with premium products like Lactaid.

Meanwhile farmers continue to incur costs associated with a whole host of improvements that were at one time incentivized. It appears the processors expect farmers to forgo being paid for those costs simply “because everyone’s doing it” and incentives are no longer needed.

The idea here is to deflate regulated minimum prices as much as possible in search of the elusive and not-well-defined Holy Grail: the market-clearing price.

Processors want cheaper milk, and they’ve got multiple proposals to accomplish that. They want to deflate the regulated minimum milk price to free up their ability to pay premiums for “something else.”

In fact, in his testimony, Stephenson admitted that as these costs and premiums are “commoditized,” space is freed up to “pay premiums for something else.”

What is the “something else” that processors will pay to incentivize after they potentially succeed in reducing the regulated minimum price in multiple ways through multiple proposals?

Are climate premiums the next thing coming once the milk price is deflated far enough? Will USDA buy what MIG and IDFA are selling?

From whole milk in schools to farm bill to climate-warped food transformation,scientists and lawmakers are getting busy, farmers need to get busy too

In the global anti-animal assault, real science must lock horns with political science and defend American farmers — the climate superheroes that form the basis of our national security. Photo by Sherry Bunting

By Sherry Bunting, Farmshine, Jan. 5, 2024

EAST EARL, Pa. – It’s a New Year, and we have new hope on several fronts that are all linked together, in my analysis.

Top 2023 headlines for dairy farmers revolved around dairy markets that underperformed, successes and challenges in the quest to get Whole Milk choice back in schools, a plethora of draft USDA and FDA proposals that dilute real dairy, farm losses and governmental hearings on federal milk pricing, negotiations and extensions for the farm bill, and acceleration of ‘climate-smart’ positives and negatives buckling down for business in an area where political science is trumping real science on the rollercoaster ride ahead.

All of these headlines are inextricably linked. There is a global anti-animal assault underway, but people are wising up to the not-so-hidden agenda that is grounded in climate transitions and food transformation that give more power and control over food to global corporations while diminishing what little power farmers have in Rural America where our national security is at risk.

Real science locks horns with political science

As we head into 2024, a bit of good news is emerging as scientists are mobilizing to defend the nutritional, environmental and social honor of livestock — especially the much-maligned cow.

After an international summit of scientists in October 2022, work has been underway to bring together an international pact.

Dubbed the Dublin Declaration of Scientists, experts around the world have authored and are getting colleagues to sign-on to this document that calls for governments, companies, and NGOs to stop ignoring important scientific arguments when pushing their anti-animal agendas in the name of climate, transformation, and the Global Methane Pledge.

To date, nearly 1200 scientists have signed the Dublin Declaration, aimed foremost at the Irish government’s proposal to slaughter cows to meet methane targets. The Dublin Declaration represents the work of scientists across the globe for a global audience beyond Ireland.

Here in the U.S., we are sitting on the cusp of Scope 3 emissions targets of global milk buyers that have been hastily formulated based on the science of greed, not the science of greenhouse gas emissions. It’s time for the dairy organizations and land grant universities that represent, serve and rely on farmers to drink up on their milk and strengthen their spines.

Farmshine has brought readers the news about what has been happening in Europe, such as in the Netherlands and Ireland, regarding proposed farm seizures and cow slaughter, and the response of farmers there has been to challenge the political establishment.

The U.S. is not far behind. At COP28 recently, American cattle industries were criticized, and even Congressional Ag Leaders are miffed by what they heard.

Still, some of our dairy organizations brag about being at COP26, 27, 28 and taking part. Even the dairy farmers’ own checkoff program is caught flat-footed. They’ve already caved to the Danone’s, the Nestles, the Unilevers, and such.

In fact, DMI’s yearend review touted its increase in U.S. Dairy Stewardship Commitment adopters to 39 companies representing 75% of the milk supply with membership in the Dairy Sustainability Alliance standing at 200 member companies and organizations. But what are they doing with those relationships to STAND UP ON SCIENCE FOR THE COWS?

The Stewardship Commitment includes DMI’s Net-Zero Initiative, where the cyclical short-lived nature of methane and the role of cattle in the carbon cycle is still not appropriately accounted for and is one of the points made in the Dublin Declaration of Scientists.

In the U.S. dairy industry, the trend on GHG revolves around DMI’s Innovation Center for U.S. Dairy, which placates large multinational corporations in the development of voluntary programs, telling farmers they are in control with their organizations as a sort of gatekeeper. That is, until those programs become mandatorily enforced by those milk buying corporations, while the science on methane and the cow’s role in the carbon cycle as well as U.S. data vs. global data continue to be ignored when they are sitting in the midst of UN Food Transformation Summits, COP26, 27 and 28, and the WEF at Davos.

In fact, during the annual meeting webinar of American Dairy Coalition in December, U.S. House Ag Chairman G.T. Thompson of Pennsylvania was asked his thoughts on some of the statements that came out of COP28 recently criticizing American dairy and livestock consumption.

“My first response was to find it laughable because it really shows you the difference between political science and real science,” he said. “It’s sad when people are so illiterate about the industry that provides food and fiber that they don’t understand how livestock contribute to carbon sequestration.

“We have a real battle,” Thompson said, adding that those putting out such statements criticizing American livestock “don’t even know which end the methane comes from. The world needs more U.S. farmers and less UN if we want a better world. The facts and the science are on our side. Let’s not let the other side control the narrative.”

Bottomline for Thompson is this: “The American farmers are climate heroes sequestering 10% more carbon that we emit. No one does it better anywhere in the world. Let’s be speaking up and speaking out. We can push it back with the facts and the science. I would encourage each of us to do that and become effective just telling that story,”

In the same ADC webinar in December, Trey Forsythe, professional staff for Senate Ag Committee Ranking Member John Boozman of Arkansas agreed.

“The language coming out of COP28, a likely European-led effort, shows what we are up against from people with no background on the role of dairy and livestock. We have to keep beating that drum on the efficiency of U.S. dairy and livestock farms,” he said.

In the same accord, scientists are getting busy, and we all need to get more involved.

In a dynamic white paper released last year, scientists made 10 critical arguments on this topic of livestock greenhouse gas emissions (GHG). Here’s what the scientists behind the Dublin Declaration are saying and why it’s so important for our land grant university scientists to sign on.

“Livestock agriculture creates GHG emissions, which is a serious challenge for future food systems. However, arguing that climate change mitigation requires a radical dietary transition to either veganism or vegetarianism, or the restriction of meat and dairy consumption to very small amounts is overly simplistic and possibly counterproductive,” the scientists wrote in a recent description of the Dublin Declaration.

“Such reasoning overlooks that dietary change has only a modest impact on fossil fuel-intensive lifestyle budgets, that enteric methane is part of a natural carbon cycle and has different global warming kinetics than CO2, that the rewilding of agricultural land would generate its own emissions and that afforestation comes with many limitations, that global data should not be generalized to evaluate local contexts, that there are still ample opportunities to improve livestock efficiency, that livestock not only emit but also sequester carbon, and that foods should be compared based on nutritional value. Such calls for nuance are often ignored by those arguing for a shift to plant-based diets,” they continued, listing these 10 Arguments with scientific explanations for each one.

Here is how the growing number of international scientists, including Dr. Frank Mitloehner of UC-Davis, situate the problem:

Argument 1 – Global data should not be used to evaluate local contexts

Argument 2 – Further mitigation is possible and ongoing

Argument 3 – Only a relatively small gain can be obtained from restricting animal source foods

Argument 4 – Dietary focus distracts from more impactful interventions

Argument 5 – Nutritional quality should not be overlooked when comparing foods

Argument 6 – Co-product benefits of livestock agriculture should be accounted for

Argument 7 – Livestock farming also sequesters carbon, partially offsetting its emissions

Argument 8 – Rewilding comes with its own climate impact

Argument 9 – Large-scale afforestation of grasslands is not a panacea

Argument 10 – Methane should be evaluated differently than CO2

These arguments take nothing away from the technologies that are being developed to help dairy and livestock producers further reduce emissions and sequester carbon. Technology has a role in amplifying the cow’s position as a solution, not to cure a problem she does not have! And farmers deserve to get credit for what they’ve already achieved.

Farm, food, and national security interdependent

The 2018 Farm Bill was extended for another year at the end of 2023, but the urgency to complete a new one continues as a big priority for House Ag Committee Chairman G.T. Thompson. In the recent ADC annual meeting webinar, he said: “You don’t want us writing farm bill legislation — or any legislation — just listening to voices inside the Beltway in Washington. It would not work out well.”

He thanked and encouraged farmers for being part of the process, saying there’s more to do.

“We’re building this farm bill listening to your voices, the voices of those who produce, those who process, and those who consume — all around the country,” said Thompson, noting nearly 40 states were visited for nearly 80 listening sessions over 2.5 years on the House side.

“This farm bill is about farm security. It’s about food security. And it’s about national security – all three of those are interdependent,” he added.

The extension and funding of the current farm bill for another year — while Congress works on the new one — means programs like Dairy Margin Coverage will continue for 2024, but the enrollment announcement has not yet been made by USDA.

In past years, the enrollment began in October of the previous year and ended at the end of January for that program year. When DMC first replaced the precursor MPP, enrollment was announced late and continued into March of the first program year (2019). At that time, farms could sign up for five years through 2023 or do it annually.

In 2023, DMC paid out a total of $1.27 billion in DMC payments for the first 10 months of the year.

Chairman Thompson noted that effective farm policy is the key, and the extension means no disruptions, he said: “We attached good data for dairy with policy changes, including for DMC, and some positive changes for the nutrition title within the debt ceiling discussion.”

On DMC, the supplemental production history was added in the legislation extending the current farm bill that was signed by the President at the end of November.

“It provides our dairy farmers the certainty that their additional production will be covered moving forward,” Thompson confirmed, adding that they are looking at moving up the tier one cap to be more reflective of the industry.

The farm bill is also being crafted to use no new tax dollars by reworking priorities, looking at the Inflation Reduction Act (IRA) funds, administrative funds and shoring up funds from the Commodity Credit Corporation (CCC) priorities to secure the farm bill baseline for the future.

The $20 billion in IRA funds being thrown about for conservation and environmental programs as well as ‘climate-smart’ grants is already down to $15 billion without spending a dime because of how it is designed to phase down and go away in 2031 and the fact that USDA is believed to not have the authority to keep these funds outside of the farm bill, Thompson explained. Negotiations are considering bringing this into the farm bill baseline so that it is there – and used for farmers – now and in the future.

“(The IRA) is not a victory if agriculture does not get the full benefit of these dollars. We can make that happen in this farm bill,” said Thompson. “Reinvesting the IRA dollars into the farm bill baseline will allow us to perpetually fund conservation in the future.”

Conservation programs are historically oversubscribed and underfunded.

Thompson expects crafting and advancing of the next farm bill to continue in earnest. He hopes to have a chairman’s mark of the bill released by the end of January and have it before the House by the end of February. Much of this timeline depends on House leadership, and the Senate has its own time frame, said Thompson.

He urged dairy farmers to spread the word to their members of Congress that farm security and food security are national security.

He also noted that the nutrition title had some of its toughest elements ironed out during the continuing resolution process in which the farm bill was extended.

“I’ve managed this in such a way that we’ve accomplished already the hard things in that title,” said Thompson.

Deploying dairy farmers on legislative efforts

“Passage of the Whole Milk for Healthy Kids Act is good for kids good for the dairy industry, and good for the economy. It simply restores the option, the choice, of whole milk and flavored whole milk, and holds harmless our hardworking school cafeteria folks by making sure the milkfat does not count toward the meal recipe limitations,” Thompson reported.

He wanted well over 300 votes for H.R. 1147 in the House to send a strong message to the Senate. On Dec. 13, the House gave him 330 ‘yes’ votes for Whole Milk for Healthy Kids.

“I would like to deploy you now on the Senate. The bill in the Senate (S. 1957) has the same language and it is tri-partisan with Republican Senator Roger Marshall, a medical doctor, Democrat Peter Welch and Independent Angus King as original sponsors,” said Thompson to dairy farmers gathered virtually for the ADC annual meeting webinar.

“There are other co-sponsors as well (12), and from my state of Pennsylvania, Senator John Fetterman is a cosponsor. Our other Senator (Bob Casey, Jr.) has not cosponsored and seems to be in opposition to it,” he said. “We need you to weigh in with your senators that this is about nutrition and health of our kids and the health of our rural communities. You are in a good position to tell the story of what happened in 2010 when fat was taken out of the milk in schools.”

Thompson noted that, “As you are doing that, you are developing relationships that will help us in the farm bill also. On the farm bill, talk about return on investment, the number of jobs and economic activity and taxes from agribusinesses, about the food security and national security and environmental benefits, science, technology and innovation in agriculture,” he said.

“Less than 1.75% of what we spend nationally is the farm bill. That’s a big return on investment, again, for food security and national security.”

Questioned about the milk labeling bill of Pennsylvania Congressman John Joyce, a doctor, Thompson said it is a strong bill. He confessed his dismay with USDA caving on this question and called FDA “a problem child” on milk labeling.

“This bill is not self-serving for dairy. This is about consumers having the information to make proper decisions on their nutrition,” he said.

New owner is global giant with $47 billion portfolio

By Sherry Bunting, Farmshine, Jan. 5, 2024

PARIS — On the first day of 2024, another brand of fluid milk was sold to a private equity firm.

This time was no surprise: Paris, France-based Danone announced on Jan.1st its agreement to sell organic dairy businesses, including flagship Horizon Organic, to Platinum Equity, based in Los Angeles, California.

The sale is said to be part of the Renew Danone Strategy announced in March 2022 and is mentioned in Danone’s 2023 Climate Transition Plan.

Danone graphs its “Impact Journey” this way in its 2023 “Climate Transition Plan,” which includes reducing methane emissions by 30% by 2030, aligning with the Global Methane Pledge, and achieving Net-Zero emissions by 2050 as the global giant says it will “continue to transform the food system.” (Web image from Danone Climate Transition Plan)

The company reported its organic dairy sector represented approximately 3% of its global revenues in 2022 and had a “dilutive impact” on sales growth and operating margin.

But mainly, said CEO Antoine de Saint-Affrique, the organic dairy business “fell outside our priority growth areas of focus,” he said, reiterating his very words to investors a year ago when he first announced “eyeing sale” of Horizon Organic and Wallaby.

Terms of sale were not disclosed, but Danone will retain a non-consolidated minority stake in the business, executives said. The closing of the transaction is subject to customary conditions and regulatory approvals.

“Today marks an important milestone in delivering this (Renew Danone) commitment while giving the Horizon Organic and Wallaby businesses the opportunity to thrive under new leadership. This sale, once completed, will allow us to concentrate further on our current portfolio of strong, health-focused brands and reinvest in our growth priorities,” said de Saint-Affrique.

According to Platinum Equity’s New Year’s Day announcement of the acquisition, Horizon Organic is deemed the largest organic fluid milk company in the world and the first brand of organic milk available coast to coast in the United States. It has since grown to include organic creamers, yogurt, cheese and butter.

Platinum Equity Co-President Louis Samson said the acquisition will “build on that legacy and support Horizon Organic’s growth as a standalone company.”

Horizon Organic became the first public organic food company in 1994 and was purchased by Dean Foods in 2004, where it became part of WhiteWave holdings alongside International Delight, Silk and other fake-milk brands. A 2012 spin-off separated WhiteWave from Dean, taking former Dean CEO Gregg Engles with it as the WhiteWave CEO. In April of 2017, Danone purchased WhiteWave, and Engles continued as a current Danone S.A. board member.

Wallaby is an Australian-style organic yogurt found mostly in natural food stores as well as the Whole Foods chain throughout the U.S.

Platinum Equity estimates that the total U.S. dairy category is valued at $68 billion in sales with fluid milk comprising approximately $17 billion of that total. Of that $17 billion in packaged fluid milk sales, organic milk sales comprised 6.7% of the volume for the first 10 months of 2023, according to the most recent USDA Monthly Packaged Fluid Milk Sales Report.

Meanwhile, Danone has launched full-force into expanding the fake side of its 2017 WhiteWave purchase, adding products and launching new brands of plant-based and AI-engineered biological concoctions of fake-milk, fake-yogurt, fake-cheese, and other fake-dairy products in its quest for so-called “Climate Transition” and “Food Transformation.”

The sale of Horizon to a global private equity firm that specializes in mergers and acquisitions also comes on the heels of Danone’s December 2021 decision to end contracts with all of its New England and eastern New York dairy farms after sourcing milk from larger organic farms to the west and south.

After the sale of Horizon Organic is completed, Danone will be able to completely withdraw from Federal Milk Marketing Orders (FMMO) to do Cost Performance Model (CPM) pricing with a much smaller number of dairy farms, just like with other ingredient sources. Only Class I fluid milk sales are required to participate in FMMOs, and the sale of Horizon Organic to Platinum Equity ends Class I milk sales for Danone because the rest of their former WhiteWave beverage holdings are plant-based.

While Danone moves on to grow its fake-dairy business, owning the largest plant-based manufacturing facility in the world located in northern Pennsylvania and launching new plant-based alternatives to disrupt the dairy case, the Managing Director of Horizon Organic’s new owner, Adam Cooper, sees organic and value-added products as the “premium offerings” that are “driving growth in the dairy milk category.

“Horizon Organic is a pioneer of that segment and is in position to continue capitalizing on and accelerating the trend,” said Cooper.

Platinum Equity has completed more than 450 acquisitions over the past 28 years, and today operates about 50 global businesses that have been shaken loose from larger corporate entities. The global firm’s current $47 billion portfolio includes a few other companies in the food and beverage sector, such as biscuits, wine, seafood, packaged meat and bakery products, and food ingredients distribution.

“We are excited about Horizon Organic’s potential as an independent business with a renewed sense of focus and a commitment to investing in its success,” said Cooper. “We look forward to partnering with Horizon Organic’s management team to ensure a seamless transition and chart a path for continued growth and expansion.”

Already deemed a “component stock of leading sustainability indexes,” Danone’s ambitions are entrenched with ESG investors, the Global Methane Pledge, Climate Transition, Food Transformation and aspirations to be the publicly-traded global company that is B-Corp certified at the global level in 2025. (Danone is already B-Corp certified in the U.S.)

Over the past seven years, Danone North America has moved toward branding its ‘sustainability’ as increasingly plant-based.

In 2022, Danone North America received a $70 million USDA Climate-Smart grant, which the company says will be used to: 1) reduce methane emissions for dairy through innovative manure management, 2) create infrastructure to sustainably grow and trace U.S. food-grade oats and soybeans, and 3) build processing for traceable organic soy.

During the White House Conference on Hunger, Nutrition and Health in September 2022, Danone announced a $22 million investment by 2030 to improve access to, and availability of, “nutritious and health-promoting foods,” the bulk of these funds will be used to “educate consumers and healthcare providers” (aka, marketing).

Shortly thereafter, the FDA Milk Labeling Proposed Rule hit the Federal Register for comment requiring only voluntary compliance for nutrition comparisons on labels of fake-milk using the term ‘milk.’ This rule has not been finalized as FDA continues to look the other way when it comes to milk and dairy label standards of identity abuses.

(Rest assured, Danone’s big goal is to become ‘net zero’ by 2050 by transforming food. Sound familiar?)

DANONE FOOD TRANSFORMATION TIMELINE

July 2016, Danone launched the Dannon Pledge for non-GMO verified, positioning its conventional milk supply around a concept of ‘almost-organic.’

Apr. 2017, Danone purchased the Dean WhiteWave spinoff, which included Horizon Organic and Silk, So Delicious, and Alpro plant-based brands. The DOJ Antitrust Division required Danone to simultaneously divest its Stonyfield Farms subsidiary.

Apr. 2018, Danone quietly notified smaller Horizon Organic dairy farms in the western states that their future contracts would not be renewed amid a glut of organic milk and differences in how USDA’s organic livestock origin rules were being applied. Some of these producers were offered conventional non-GMO milk contracts using Danone’s proprietary Cost Performance Model (CPM). Some found other markets, and many exited the business. According to Danone’s 2021 Regenerative Agriculture Report, more than half of all U.S. milk collected by Danone now comes from farms with CPM contracts.

Feb. 2019, Danone completed construction of the world’s largest plant-based yogurt factory in Dubois, Pennsylvania, where other non-dairy lookalike products are also made.

Feb. 2020, Danone told investors the rising global temperature is a business opportunity, and the company would accelerate food transformation with climate at the core of its growth strategy.

Oct. 2020, Danone announced its partnership with a bioscience startup to use artificial intelligence to explore new formulations to improve taste and texture of plant-based dairy alternatives.

Jan. 2021, Danone’s So Delicious launched its first plant-based cheese and Danone S.A. was acknowledged as the largest plant-based company in the world with 10% of total sales coming from plant-based dairy alternatives. The company told investors it would grow this with further acquisitions and a “plant-based acceleration unit.”

Apr. 2021, Danone and the EAT Lancet Commission announced a strategic partnership to promote a so-called “healthier and more sustainable food system by driving a change to planetary diets.” Danone pledged to use its ‘One Planet. One Health’ framework to “accelerate this food revolution.”

July 2021, Danone announced three new plant-based fake-milk launches for 2022, along with a list of other lookalikes. During the July 2021 earnings call, Danone executives identified the U.S. as a “key plant-based market,” but noted 60% of U.S. consumers are not in the category because of product taste and texture. They announced a plan to win them over “with new dairy-like technology under Silk NextMilk, under So Delicious Wondermilk and under Alpro Not Milk.”

Aug. 2021, Danone sent letters notifying all 89 of its organic dairy farms in New England and eastern New York that their milk contracts would be terminated in 12 months’ time. Later, under pressure from organic groups, officials and consumers, Danone agreed to a Feb. 2023 extension.

Jan. 2022, Danone launched the three new fake-milks: NextMilk, Wondermilk, and Not Milk.

(Interestingly, the Silk NextMilk Whole Fat has 6 grams of saturated fat from processed coconut and seed oils. That’s more saturated fat per serving than Real Whole Dairy Milk naturally from cows. Danone’s Silk NextMilk is packaged in red and white cartons with the words ‘Whole Fat’ appearing directly under the brand name to mimic the Whole Milk appearance. Interestingly, the FDA’s proposed healthy labeling rule sets a tougher threshold for saturated fat in dairy products compared to saturated fats from plant-sources.)

Mar. 2022, Danone described its Horizon Organic and “traditional dairy” holdings as “troubled offerings,” telling investors: “There are no sacred cows,” as they “keep pruning” the portfolio to “boost growth” and “distance” the company from “underperformance”… by investing more in “winning products” and selling existing brands or buying new ones.

May 2022, Danone launched its “Dairy & Plants Blend” baby formula (60% plant-based, 40% dairy) “to expose children to food tastes early in life that can help shape their future food preferences… while shifting toward plant-rich diets and embracing alternative sources of protein to help reduce carbon emissions.”

Sept. 2022, Danone joined the White House Conference on Hunger, Nutrition, and Health to announce a $22 million ‘nutrition and health’ investment by 2030 with $15 of the $22 mil. Earmarked “to further nutrition education for consumers and healthcare providers.” (Sounds like marketing). This includes Danone’s new pledge to increase the nutrient density of its plant-based beverages.

Sept. 2022 — Danone was part of a team that was awarded a $70 million USDA Climate Smart grant for projects that include: 1) Reducing methane emissions for dairy through innovative manure management, 2) Creating the infrastructure to sustainably grow and trace U.S. food-grade oats and soybeans, 3) Building processing for traceable organic soy.

Oct. 2022, Danone announced it would use artificial intelligence through its bioscience partner BrightSeed, to reformulate over 70% of its plant-based fake-milk alternatives to reduce added sugars and increase nutrient density. At the same time, it allocated $15 million to “partner with retailers on healthy eating education” and $7 million to partner with community-based programs that provide nutritious foods.

(Timing is everything: Danone is among the financial supporters of the infamous Tufts University Food Compass, launched recently into the federal nutrition policy arena through the Biden-Harris Hunger, Health and Nutrition Strategy and the FDA proposed rule on “healthy labeling.” The Food Compass nutrition profiling algorithm rates nonfat dairy yogurt high as an encouraged food, along with plant-based fake-milks; but real milk and cheese are rated lower as foods to moderate or discourage. More artificial intelligence, to be sure.)

Jan. 2023, Danone announced it was looking for a buyer for Horizon Organic, saying it fell outside of their growth areas of focus.

Feb. 2023, Contract extensions ended for terminated Horizon Organic dairy farms in the Northeast. Some have gone out of business. Others have gone to Stonyfield or Organic Valley, which eventually agreed to take on the remaining Northeast farms facing Horizon termination, along with 40 organic dairies cut last year by Maple Hill in New York.

Mar. 2023, Danone launched a fake-milk-mustache campaign for its Silk NextMilk brand using children, nieces, and nephews of three original real-milk-mustache celebrities to twist the knife.

Apr. 2023, Danone launched an organic alternative beverage: ‘So Delicious Organic Oatmilk’ in ‘original’ and ‘extra creamy.’

May 2023, Danone launched So Delicious Dairy-Free Yogurt

Jan. 2024, Danone announced its agreement to sell organic dairy businesses — Horizon Organic fluid milk and Wallaby yogurt to Platinum Equity.

— Along with more imports and shifts in cheese production, major manure-driven expansion in cheese-heavy Central U.S. put pressure on region’s ‘disrupted’ processing capacity

By Sherry Bunting, Farmshine, Updated in reflection from original publication in July 7, 2023 Farmshine

EAST EARL, Pa. — What has driven the rockier road for 2023 milk prices? Many things, and manure may be top on the list.

In fact, we’ll cover the ‘manure effect’ in a future article. But are we beginning to see the methane wheel-of-fortune behave with the ‘cobra effect’? (The British government, concerned about the number of venomous cobras in Delhi, offered a bounty for every dead cobra. Eventually, however, enterprising locals bred cobras for the income.)

This happened with greenhouse gases in the past. It happened with a byproduct gas of making refrigeration coolant. In 2005, when the UN Intergovernmental Panel on Climate Change began an incentive scheme. Companies disposing of gases were rewarded with carbon credits, which could eventually get converted into cash. The program set prices according to how serious the environmental damage was of the pollutant. (Like making cow methane seem like new methane when it’s not). As a result, companies began to produce more of the coolant in order to destroy more of the byproduct gas, and collect millions of dollars in credits. This increased production also caused the price of the refrigerant to decrease significantly.

With this prelude, let’s look back in retrospect on what I reported in the July 7, 2023 Farmshine when milk markets were in a tailspin hitting their low for the year — just 10 days before the gradual turnaround began.

As losses in the CME spot cheese markets and Class III milk futures markets continued through July 6, the Federal Order benchmark Class III price for June was pushed down to $14.91 per cwt. and protein down to $1.51/lb, July and August futures went well below the $15 mark, with Class III below $14.

Let’s look at the supply side of the January through June 2023 supply and demand equation.

Looking at the May Milk Production Report that was released in June, it’s hard to believe the bearish response we saw in milk futures and spot cheese markets that occurred based on a mere 13,000 more cows nationwide that month. It was a paltry 0.1% increase over a flat 2022, along with 11 more pounds of milk output per cow for the month (up 0.5% over flat 2022).

This flipped the switch from a gradually lower-than-2022 market to one that plunged sharply and suddently into the dumps – and all the analysts said: ‘We’ve got too much milk for demand.’ (In fact, two months later, processors are pointing to June and July milk dumping and $10 under class spot milk price as proof that USDA is setting Federal Milk Marketing Order minimum prices too high! — I digress).

As noted in Part One of this series that was published in the june 30 edition of Farmshine, other converging supply-and-demand factors plagued cheese markets that month until July 17 — despite basic fundamentals of these milk production reports not being all that bad.

USDA Dairy Market News said spot loads of milk were being discounted in June by as much as $11 below the already abysmal FMMO Class III price in the Midwest. The milk dumping that reportedly began in May in Minnesota moved into Wisconsin through June and into July. The July 5th Milwaukee Journal Sentinel reported “Truckloads of fresh farm milk have been flushed down the drain into Milwaukee’s sewer system recently as dairy plants, filled to the brim, couldn’t accept more.” The story notes this had gone on for weeks, and the amount has declined to 5 trailer loads per week by the time The Milwaukee Journal Sentinel published its report.

For the price and milk dumping fallout, economists and analysts blamed the higher milk production (though it was modest on a national basis but huge in the Central U.S.). They blamed the higher cheddar cheese production (not accompanied by higher inventory), and they blamed the lower volume of exports (modestly below year ago on a year-to-date solids basis).

Globally, milk production was up (it is declining this fall), they said, suggesting U.S. prices needed to get below the falling global prices in order to recover more export volume (instead of dumping in the sewer). Well, they got what they wanted as the U.S. prices dropped like a rock through June until the turnaround on July 17.

Of course, no one (but Farmshine) mentioned the rising imports that were reported in Part One of this series.

Looking for context on the imports, we reached out to retired cooperative executive Calvin Covington, who follows these things on a total solids basis and has been watching the whey market as a leading milk market indicator. We learned that his calculations on a total solids basis, pegged January through April 2023 imports of dairy products into the U.S. at levels 15% higher than a year ago!

“The 15% equals 39.3 million lbs. more solids,” Covington wrote in an email response to a Farmshine question. “Most of the imports are coming from Europe. Dairy demand is very weak in Europe, consumers have less money to spend. Those milk solids are moving out of Europe.”

Noted Covington in June: “On a total solids basis, ending dairy stocks as of April 30th are 3% higher than last April. The 3% equals 61.5 million lbs. more solids.”

This means the 15% increase in January through April dairy product imports — on a total solids basis — were equal to more than half (63%) of the 3% increase that was reported in April domestic ending stocks of all dairy product inventories on a total solids basis.

Think about that for a minute. Product came in and was inventoried while domestic milk was dumped, and producer prices were crushed so that the domestic price could fall below the global price so then the U.S. dairy exports could increase? It makes the head spin.

Class I sales were down during this time, especially in the Midwest where some fluid plants have closed. Fresh Italian cheese production was down, and that’s a big one for Wisconsin. Together these factors pushed more milk to make more American cheese at that time, some of it delivered to consumers in smaller packages (rationing).

A wrinkle in the market-fabric comes from the dairy foods complex importing higher volumes, and there are the fake bioengineered microorganisms from which excrement is harvested and described as ‘dairy casein or whey protein without the cow.’ These analogs are being heavily marketed to large food manufacturers making dairy and bakery products as carbon-footprint-lowering dairy protein ‘extenders.’

However, as we look at the modest milk production increase for the first half of 2023, overall, and compare it to 2022, the total comparison was flattish then and it is declining now as we move toward Q3.

But there’s another major twist to this supply-demand equation:

The location and purpose of dairy expansion is undergoing accelerated transformation on a geographic and structural basis. This transformation is part of the “U.S. Dairy transformation” that the national dairy checkoff has promoted in its Pathways to Net Zero Initiative… and it is affecting the milk pricing for all U.S. dairy farmers, everywhere.

Here’s the problem: Milk production in the Central U.S. has expanded by much more than the national average.

Even University of Wisconsin economics professor emeritus Bob Cropp noted in his writing after the May report that growth in the Midwest — where cheese rules the milk check — was outpacing processing capacity, and the existing capacity to process all this milk was being reduced by labor and transportation challenges.

The concentrated expansion of milk production in the Central U.S. has been accelerating since 2018, but a new paradigm is now in effect: New concrete is being poured in the targeted growth areas driven more by manure, than by milk, and new dairy processing plant construction that is completed and in the works is targeting the same areas.

This is creating a production bubble that is a flood within calmer seas.

Some are calling it the California RNG gold-rush as developers construct Renewable Natural Gas (RNG) projects — especially on new large dairies — for the California RNG market and to collect the low-carbon-fuel credits for the California exchange and other exchanges that are and will be emerging, thanks to the USDA Climate Smart wheel-of-fortune.

We’ve heard the national dairy checkoff managers from DMI talk about profitable sustainability, markets for manure, promotion of other revenue streams for dairy farms as part of the mantra the checkoff has assumed for itself as speaker for all-things-dairy for all-dairy-farmers on what is “sustainable” for the industry.

When the Net-Zero Initiative was launched — along with DMI’s industry transformation plan — it was something that had been in the works since 2008 and emerged more prominently in the 2017-21 period when the former and current U.S. Ag Secretary Tom Vilsack did his stint as top-paid DMI executive, presiding over the U.S. Dairy Export Center (USDEC) under DMI’s umbrella and as a top-talker on the Innovation Center for U.S. Dairy, also under DMI’s umbrella.

All three: DMI, USDEC, and Innovation Center for U.S. Dairy are 501c6 non-profit organizations contracted to spend checkoff dollars. A 501c6 is essentially a non-profit that can lobby policymakers, whereas the 501c3 National Dairy Board cannot.

In 2020 and 2021, the Innovation Center — filing tax returns under the name Dairy Center for Strategic Innovation and Collaboration Inc. — doubled its revenue from around $100 to $150 million annually to $300 to $350 million.

We all heard it, read it, thought about it – maybe – that the checkoff was morphing into a facilitator for the transformation of the dairy industry led by manure-promotion, not necessarily milk promotion, with the mantra of feeding the world, being top-dog internationally, and meeting international climate targets with a Net Zero greenhouse gas pledge. (That pledge and the methane calculation are another story Farmshine readers are aware of, but we’ll leave that big driver off the table for this discussion.)

Here we are, now seeing an industry being created from within the broader dairy industry with new production driven by manure, in regions where new or expanding cheese, whey and ingredient plants are being located and potentially displacing production from plants and farms elsewhere that are not tied-into this manure-to-methane wheel-of-fortune using dubious science and math to overpeg a cow’s global warming impact.

While that production bubble is building in targeted growth regions with cheese-heavy milk checks, driven in part by manure-focused expansion, it bursted at the seams this summer due to a processing capacity bottleneck, compounded by supply chain disruptions and a sudden decrease in the production of fresh cheese at other plants and a sudden 18% decline in the amount of milk processed for Class I fluid use in the Upper Midwest.

Here’s the sticky wicket. A review of the 2022 end-of-year milk production report along with reports issued in the first half of 2023, revealed that, indeed, the Central U.S. was “awash in milk.”

Zooming in on the milk production reports, we see South Dakota continuing its fast and uninterrupted growth — up 15.5% for 2022 vs. 2021, and up 7.4% Jan-May 2023 vs. 2022 — having leapfrogged Vermont, Oregon and Kansas and closing in on Indiana in the state rankings.

Neighboring Iowa leapfrogged Ohio in 2022 with a 4.7% gain in milk production Jan-May 2023 vs. 2022. Number 7 Minnesota grew again after taking a breather with a 0.6% decline in 2022, then increasing 2% in production Jan-May 2023.

The tristate I-29 corridor, where cheese processing capacity has been expanding, was up 3.3% in milk production collectively with 19,000 more cows Jan-May 2023. Add to this the 1.3% increase in number 2 Wisconsin’s May milk production, and we saw the quad-state’s collective increase was 203 million pounds of additional milk in the region vs. year ago in May, although Wisconsin’s contribution came from 3000 fewer cows, according to USDA.

Just west in number 3 Idaho, production jumped 3.1% with 7,000 more cows Jan-May 2023.

To the east in the Michigan-Indiana-Ohio tri-state region — where the large new cheese plant in St. John’s, Michigan is fully operational — collective milk output was up 2% over year ago with 11,000 more cows. In 2022, this tri-state region was down 2 to 3% for the year compared with 2021.

Number 5 New York made 2.1% more milk with 7,000 more cows in May vs. year ago, with most of this expansion in the western lake region.

Number 1 California shrank milk production by 0.7% in May with 2000 fewer cows, and number 4 Texas flattened out its multi-year accelerated growth curve to make just 0.8% more milk in May than a year ago with just 1000 more cows, largely affected by the devastating Texas barn April fire resulting in the loss of around 20,000 cows.

Neighboring New Mexico continued its multi-year downward slide, ranked number 9 behind a flat-to-slightly-lower milk output in number 8, Pennsylvania.

Milk production in New Mexico fell 3.8% in May vs. year ago with 10,000 fewer cows. This followed an 8.4% decline in milk production and a 30,000-head cut in cow numbers for the year in 2022. Producers there cite well-access limitations, severe drought, high feed costs with reduced feed availability, as well as receiving the rock-bottom milk price as the reasons dairies in New Mexico are closing or relocating.

With all of these factors in play, the production reports show a clear paradigm shift in how the dairy industry expands via transformation. It is being driven to where feed is available and milk output per cow is higher, and it’s now being driven by a non-milk-related factor: MANURE for the RNG ‘goldrush’

A saving grace is cattle are in short supply, with replacements bringing high prices. This fact is slowing the bubble, production is declining now, and prices are recovering from those unanticipated lows.

NMPF, NAJ say higher solids worth more nutritionally,Seek FMMO updates to avoid misalignments and disorderly marketing

Calvin Covington (left) for Southeast Milk and Peter Vitaliano for National Milk Producers Federation testified on what the outdated skim milk component standards mean in terms of underpaying farmers and eroding producer price differentials (PPD), leading to disorderly marketing. This occurs because the skim portion of the milk that is utilized in manufactured products (Class III and IV) is paid per pound of actual protein, solids nonfat and other solids; whereas the skim portion of the milk bottled for fluid use (Class I) is paid on a per hundredweight basis using the outdated standard skim solids levels. The fat portion is not an issue because it is already paid per pound in milk class uses. Screen captures, hearing livestream

By Sherry Bunting, Farmshine, Sept. 8, 2023

CARMEL, Ind. – The national Federal Milk Marketing Order hearing completed two weeks of proceedings, so far, in Carmel, Indiana. The entire hearing is expected to last six to eight weeks, covering 21 proposals in five categories.

Picking up the livestream online, when possible, gives valuable insight into a changing dairy industry and how federal pricing proposals could update key pricing factors.

The first week dug into several proposals to update standard skim milk components to reflect today’s national averages in the skim portion of the Class I price.

Here is a bite-sized piece of that multi-day tackle.

National Milk Producers Federation (NMPF) put forward several witnesses to show what the outdated component levels mean in terms of underpaying farmers, and how paying for the skim portion based on outdated component levels has eroded producer price differentials (PPD), leading to disorderly marketing.

IDFA’s attorney Steven Rosenbaum grilled NMPF economist Peter Vitaliano on this. He tried on seven attempts to establish that the fat/skim orders in the Southeast don’t have component levels as high as the national average, suggesting this change would “overpay” producers in some markets.

In his questioning, Rosenbaum stressed that fluid milk processors can’t recoup the updated skim component values if those components do not “fill more jugs.”

Vitaliano responded to say that protein beverages are a big deal to consumers, and some milk marketing is being done on a protein basis. Rosenbaum asked for a study showing how many fluid processors are actually doing this.

Attorneys for opposing parties kept going back to this theme that the skim solids should not be updated because the FMMOs are based on “minimum” pricing. They contend that processors can pay “premiums” for the extra value if they have a way of recouping the extra value by making more product or marketing what they make as more valuable.

Vitaliano disagreed, saying that even though many processors do not choose to market protein on the fluid milk label, “more protein makes fluid milk more valuable to consumers.”

Attorney Chip English went so far as to ask Calvin Covington on the stand: Why should my clients (Milk Innovation Group) have to pay more for the additional solids in the milk when they are removing some of those solids by removing the lactose?

“Consumers don’t want lactose,” English declared.

Covington, representing Southeast Milk and NMPF, responded to say: “I don’t know that to be true. It is unfair to suggest all.”

Bottomline, said Covington, raising standard skim solids to reflect the composition of milk today vs. 25 years ago adds money to the pool to assist with the PPD erosion so that Federal Orders can function as they were intended and so producers are paid for the value.

As English further questioned whether consumers even care about the higher skim solids and protein levels of milk today, Covington replied: “Skim milk solids have a value in Class I, or fluid milk. People don’t buy milk for colored water. The solids give it the nutritional value. That’s the reason they buy milk. That’s why FDA set minimum standards in some states. Why would you drink milk if not for the nutritional value?”

He also pointed out that the increase in solids nonfat over the past 20-plus years has improved the consistency of lower fat milk options. As noted previously, the milkfat is a separate discussion and is not included in this proposal because farmers are already paid per pound for their actual production of butterfat in all classes, including Class I.

Under cross examination, Covington explained that the Class I price in all Federal Orders pays for skim on a standardized per hundredweight basis and pays for fat on actual per pound basis. Meanwhile, the manufacturing classes pay for both skim and fat on a per pound of actual components basis.

As skim component levels have risen in the milk, the alignment of Class I to the manufacturing classes narrows because of the differences in how the skim is paid for. When this happens, it becomes more difficult to attract milk to Class I markets. That’s one example of disorderly marketing. PPD erosion and depooling of more valuable manufacturing class milk is another example.

Covington explained the impact of this misalignment on moving milk from surplus markets to deficit Class I markets, that the lower skim value becomes a disincentive.

Vitaliano explained the depooling issue as “creating disorderly marketing conditions also, and great unhappiness when one farm is paid a certain price and another handler pays a different price (in the same marketing area). That’s disorderly unhappiness for the Federal Order program,” he said.

He noted that the fundamental reason for pooling is to take the uses in a given area with different values to achieve marketwide pooling where producers in that Federal Milk Marketing Area are paid similarly, regardless of what class of product their milk goes into.

“This removes the incentive for any one group to undercut the marketwide price to get that higher price (for themselves),” he said. “The Orders create orderly marketing with a uniform price. Depooling undermines that fundamental purpose that is designed to create orderly marketing.”

Either way, whether indirectly paying to bring supplemental milk into Class I markets from markets with higher manufacturing use, or in the case of depooling, the dairy farmers end up paying for the fallout from this erosion of the PPD.

Since the beginning, even before 2000 Order Reform, figuring the Class I base milk price had to begin somewhere, according to Covington. Federal pricing has always used the manufacturing class values in determining that base fluid milk price.

The trouble today is that Class III and IV handlers pay farmers per pound of actual skim components in the milk they receive, while the Class I handlers pay per hundredweight based on an arbitrary outdated national average skim component standard. Thus, the “opportunity cost” of moving this now higher component milk to manufacturing classes that pay by the actual pound of protein, for example, instead of by the old standard average protein levels is not accounted for in the Class I price that still uses the old standard average levels.

Pressed again on how it makes sense to raise Class I prices by raising the component level of the skim to more adequately reflect the national average today, Covington said: “It adds to the nutrition, and I stand by that. In proposal one, the price will go up (estimated 63 cents per cwt or a nickel per gallon). I am comfortable charging that extra price to Class I processors.”

Attorney English, representing MIG, retorted that, “The handlers who buy milk and then by adding a neutralizing agent remove the lactose, they’re going to pay more for the milk that they then have to process to subtract the lactose.”

Covington responded that, “There are consumers who think about lactose. There are consumers who buy lactose-free products, yes, because it is on the shelf, but it’s not all consumers.”

On the higher protein, English asked Covington how Class I processors are supposed to monetize that protein in a label-less commodity, a commodity that is declining in its share of total milk utilization?

“We are still selling 45 billion pounds of packaged fluid milk (annually) in this country,” said Covington. “Consumers wouldn’t buy that 45 billion pounds if it wouldn’t have some nutrition.”

English argued that milk is sold as whole, 2%, 1% and non-fat. It is not sold by its protein, so isn’t it “so highly regulated in ways that alternatives are not that any increase in price hinders sales of fluid milk?”

Covington acknowledged that, “yes, it is regulated, but I’m not convinced that this proposal will hinder fluid milk sales. Again, (higher components) add to the nutrition and I stand by that.”

Opponents kept coming back to these value questions, while proponents focused on the price alignment issue and orderly marketing.

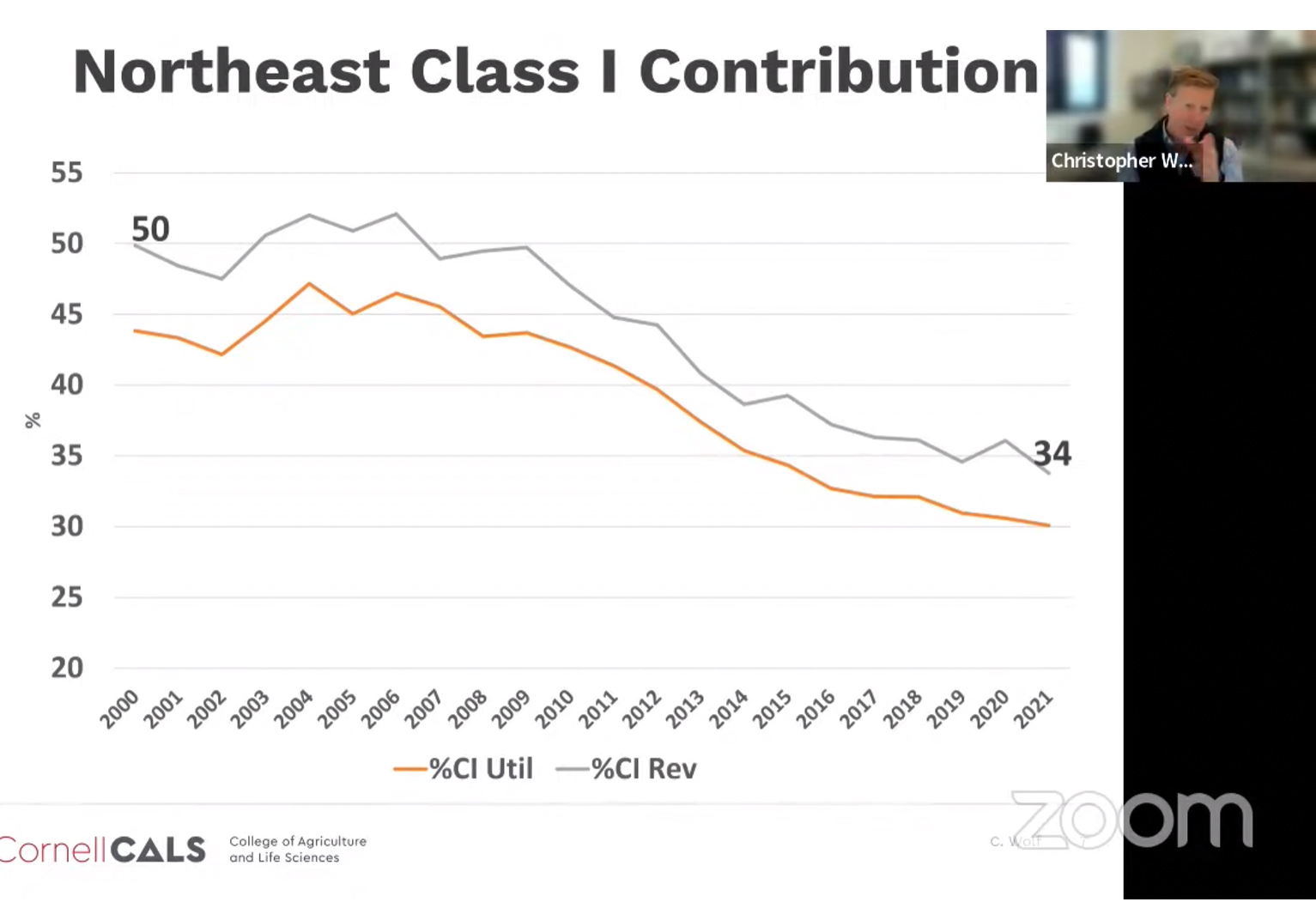

Using the Northeast as an example of a multiple component pricing Federal Milk Marketing Order that still has significant Class I utilization, Dr. Chris Wolf showed how long-term trends and other factors have reduced the Class I utilization and Class I revenue from 50% in 2000 to 34% in 2021 in FMMO 1. The most dramatic part of this decline occurred after 2010 — leaving not enough money to go around with less Class I value in the pool. FMMOs were structured for Class I fluid markets not for the dairy product and export markets where growth is occurring today. Screen capture from Center for Dairy Excellence Protecting Your Profits webinar with CDE’s Zach Myers and his guest Dr. Chris Wolf, Cornell University dairy economist.

By Sherry Bunting

WASHINGTON – There are irons in two fires when it comes to federal milk pricing and dairy policy. One is to do modernization through the Federal Milk Marketing Order (FMMO) hearing petition process. The other is to make some adjustments or seek authorizing language through the dairy title of the 2023 Farm Bill.

On the farm bill front, the May 12 CBO baseline score shows this could be the first trillion-dollar farm bill. Food assistance programs, like SNAP, are eating into the capacity to do other things, say top-level staff for the Senate Ag Committee.

For dairy and livestock, the Dairy Margin Coverage (DMC) baseline now includes $1 billion in additional outlays projected over the 10-years, while livestock disaster outlays have doubled – even without making any changes in these programs that some are suggesting.

Still, farmers and organizations that represent them are seeking some expansion for the DMC, livestock disaster, and other programs and safety nets, and some are seeking language to instruct the Secretary to do hearings on the Class I ‘mover’, or to expand the flexibility of the scope of a hearing, or to require mandatory reporting germaine to things like raising make allowances.

The jury is out on whether a farm bill gets done by September 2023 after the May 12 baseline was announced by CBO in the current political environment, but members of the House and Senate Ag Committees and their chairpersons are gathering information in earnest toward that goal.

On the FMMO hearing front, as previously reported in Farmshine, the USDA responded April 28 to the March 30 petitions from two processor organizations by asking for more information instead of granting or denying a hearing on their make allowance update request.

The two petitions from International Dairy Foods Association (IDFA) and Wisconsin Cheese Makers Association (WCMA) both requested a hearing focused exclusively on updating the ‘make allowances’, which are processor credits that are subtracted from the wholesale end-product prices used to derive farm level milk class and component prices.

Make allowances were last updated in 2008 using 2006 plant cost data.

Four days later on May 2, the National Milk Producers Federation (NMPF) submitted its petition seeking an FMMO hearing on a range of national amendments.

NMPF is petitioning USDA for a hearing on these five items:

1. Increase make allowances in the component price formulas to the following levels: Butter $0.21 per pound, Nonfat dry milk $0.21 per pound, Cheese $0.24 per pound, Dry Whey $0.23 per pound

2. Discontinue use of barrel cheese in the protein component price formula

3. Return to the “higher-of” Class I mover

4. Update the milk component factors for protein, other solids, and nonfat solids in the Class III and Class IV skim milk price formulas

5. Update the Class I differential pricing surface throughout the U.S.

Not noted within this list is a point that NMPF’s board approved on the legislative front, and that is to seek language in the 2023 farm bill directing USDA to do periodic mandatory and audited plant cost surveys instead of voluntary surveys for future hearings on make allowances.

The American Farm Bureau Federation took a positive approach in their response letter to USDA, showing support for the fact that NMPF’s petition is comprehensive and includes areas of strong consensus among farmers such as returning the Class I mover to the ‘higher of.’

However, AFBF president Zippy Duvall also points out in the response letter that the Secretary of Agriculture already has the authority under the Agricultural Marketing Agreement Act to require processors to provide information relevant to FMMO pricing. This could include mandatory surveys of plant cost data when used to determine the processor credit, or make allowance, in the pricing formulas.

It is Farm Bureau’s position that make allowances should only be updated based on mandatory and audited plant cost surveys.

This leaves a bit of a loophole in the discussion about how to acquire the data to make current or future updates. The Secretary may have the authority to require data from plants that participate in FMMOs. However, it is unclear if the Secretary has this authority to require cost data from plants that do not participate in the FMMOs.

The end-product pricing formulas are based on wholesale prices that are collected mandatorily by USDA AMS on a weekly basis through the Livestock Mandatory Reporting Act on only those products that are used in FMMO formulas. This includes butter, nonfat dry milk, dry whey and 40-lb block and 500-lb barrel cheddar cheese.

The USDA AMS weekly National Dairy Product Sales Report surveys 168 plants for this price data. Therefore, if make allowances are updated as processor credits against those prices, then all 168 plants should have to report their costs, and only the costs that pertain to those specific products, whether or not they participate in FMMOs. In a recent voluntary cost survey, more than 70% of those plants did not report their cost data.

During a Center for Dairy Excellence Protect Your Profits zoom call recently, risk management educator Zach Myers had as his guest Cornell dairy economist Dr. Chris Wolf to talk about the FMMO reform process and background from an economist’s perspective.

Dr. Wolf gave some important and relevant background and statistics.

The FMMOs have been around for 85 years and were created because of disorderly milk marketing conditions. Their primary function is to make markets function “smoothly” with a second stated objective to provide price stability.

“If we were to re-do them today, I would say price adequacy should be addressed,” Wolf opined, noting that “we have times that the milk prices are very stable, but not very adequate.”

Other stated objectives of FMMOs are to assure adequate and wholesome supplies of fluid milk and equitable pricing to farmers.

“These things are still important today,” Wolf suggests, adding that the auditing, certification and a certain level of market information that is provided by the FMMOs benefits all participants and contributes to the public good.

He explained that FMMOs are changing.

“The primary sources of dissatisfaction with FMMOs in recent years arise because there is not enough money to go around, and some of this is related to the longer-term trends (in Class I sales),” Wolf explains.

He showed that while per capita dairy consumption has been increasing roughly three pounds per person per year, the decline in Class I fluid milk is the underlying factor.

“It really is startling how much of that decline (in Class I) in most areas really happened since 2010,” Wolf illustrated with graphs.